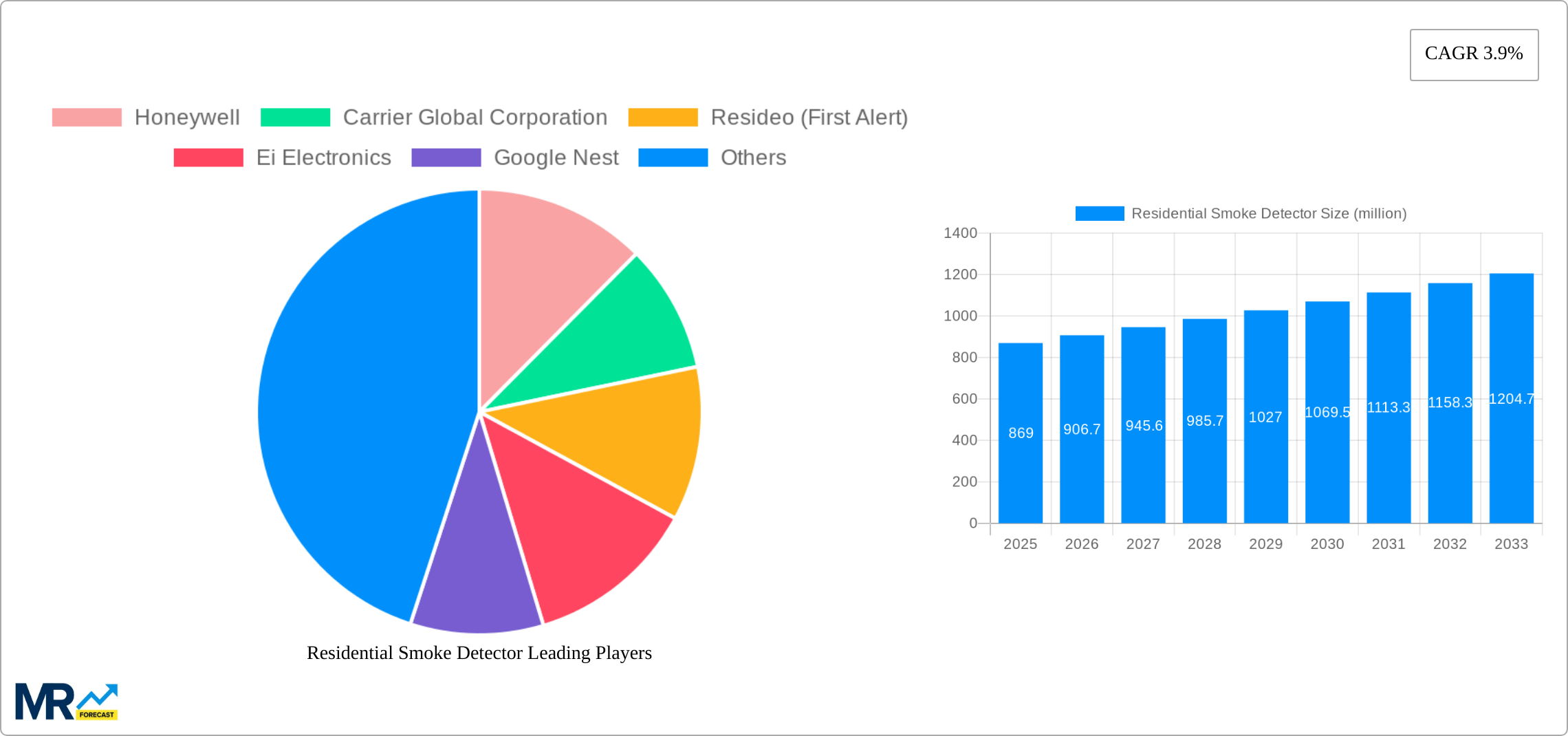

1. What is the projected Compound Annual Growth Rate (CAGR) of the Residential Smoke Detector?

The projected CAGR is approximately 3.9%.

Residential Smoke Detector

Residential Smoke DetectorResidential Smoke Detector by Type (Photoelectric Smoke Detector, Dual-Sensor Smoke Detector, Ionization Smoke Detector, Online, Offline), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

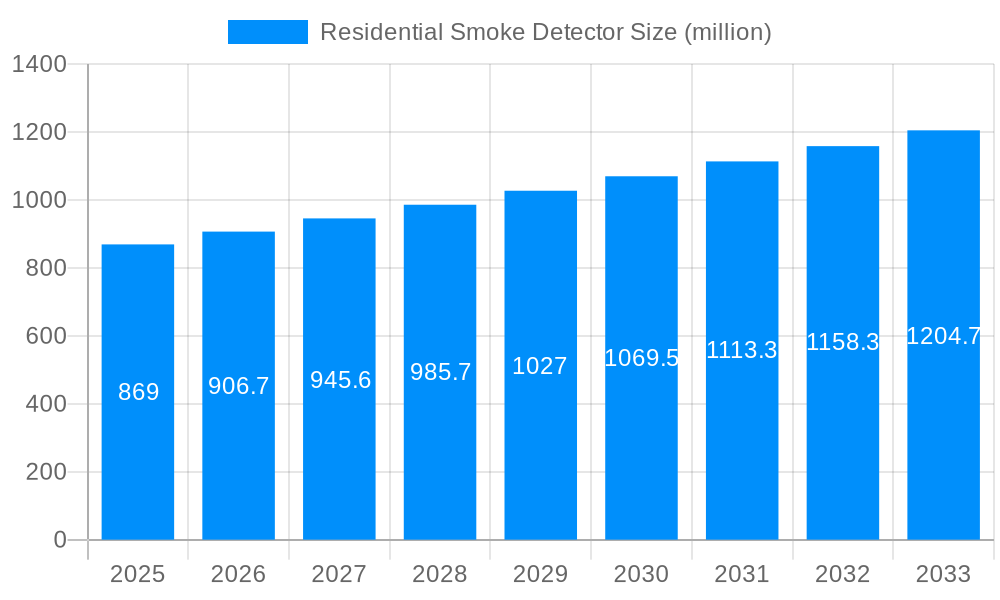

The global residential smoke detector market, currently valued at $869 million (2025 estimated), is projected to experience steady growth, driven by stringent building codes mandating smoke detector installation in new constructions and renovations across major regions. The 3.9% CAGR (2025-2033) reflects a sustained demand fueled by increasing awareness of fire safety, particularly in residential settings. Key growth drivers include the rising adoption of smart home technologies, integrating smoke detectors with broader home security systems and offering features like remote monitoring and app-based alerts. The market is segmented by detector type (photoelectric, dual-sensor, ionization), with dual-sensor detectors gaining traction due to their enhanced sensitivity and reduced false alarms. Sales channels are broadly categorized as online and offline, with online sales expected to show stronger growth due to e-commerce expansion and increasing consumer preference for convenient purchasing. While pricing pressures and the maturity of the market could pose some restraints, ongoing technological advancements, such as improved battery life and connectivity features, are expected to offset these challenges, ensuring consistent market expansion.

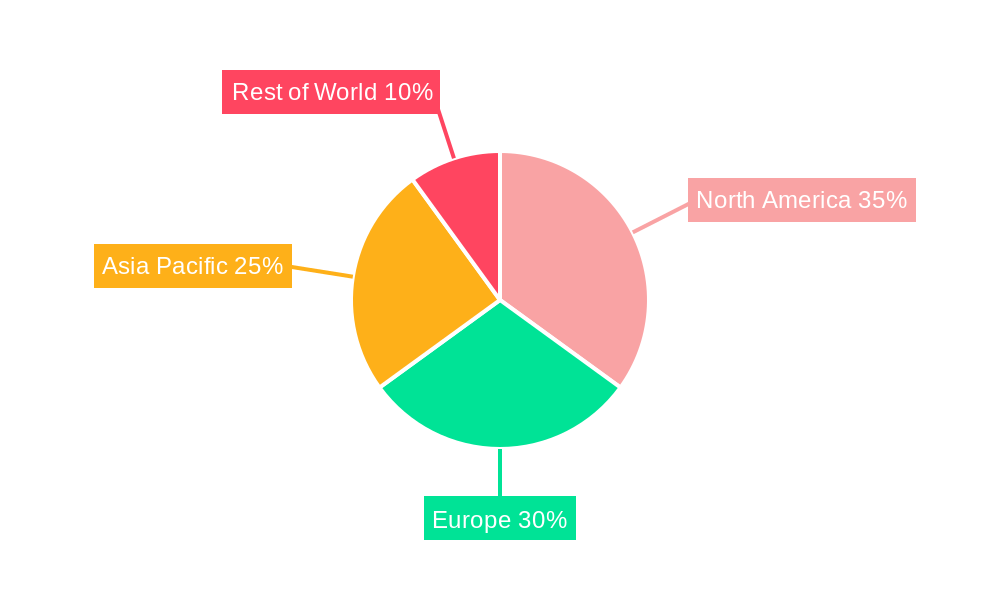

Despite a mature market, several factors contribute to continued growth. The increasing prevalence of interconnected smart home ecosystems encourages the integration of smoke detectors, offering features like mobile notifications and remote monitoring capabilities that enhance safety and convenience. Furthermore, government regulations and initiatives promoting fire safety awareness campaigns are indirectly driving demand, particularly in developing economies. The competitive landscape is characterized by established players like Honeywell, Resideo (First Alert), and Johnson Controls, alongside emerging technology companies offering innovative features and cost-effective solutions. Regional variations exist, with North America and Europe expected to maintain significant market shares due to high adoption rates and stringent safety standards. However, growth in Asia-Pacific is anticipated to be noteworthy driven by increasing urbanization and rising disposable incomes.

The global residential smoke detector market, valued at several billion USD in 2024, is experiencing robust growth, projected to reach tens of billions of USD by 2033. This expansion is driven by a confluence of factors, including increasing awareness of fire safety, stringent building codes mandating smoke detector installation, and the rising adoption of smart home technologies. The market is witnessing a significant shift towards advanced sensor technologies, with dual-sensor detectors gaining popularity over traditional ionization or photoelectric models. This is due to their superior detection capabilities across various fire types. Furthermore, the integration of smart features such as interconnected alarms, mobile app notifications, and voice control is driving premiumization and enhancing user experience. The market demonstrates a clear preference for online sales channels, reflecting broader e-commerce trends. However, offline channels still maintain a substantial share, particularly in regions with lower internet penetration. Key players are focusing on strategic partnerships, product innovations, and geographical expansion to maintain a competitive edge in this rapidly evolving landscape. The market is segmented based on detector type (ionization, photoelectric, dual-sensor), sales channel (online, offline), and geography, providing granular insights into consumption patterns. Millions of units are sold annually, with significant regional variations reflecting differences in building regulations, consumer awareness, and economic development. The forecast period (2025-2033) shows a sustained trajectory of growth, fueled by continuous technological advancements and escalating demand for safer living environments. Specific growth rates vary by region and segment, with certain regions showing significantly higher adoption rates than others.

Several key factors are fueling the growth of the residential smoke detector market. Firstly, the increasing awareness of fire safety and its devastating consequences is a major driver. Public education campaigns, coupled with tragic fire incidents, are prompting homeowners to prioritize fire prevention measures. Secondly, stringent building codes and regulations in many countries mandate the installation of smoke detectors in residential buildings, further boosting market demand. Thirdly, the rising adoption of smart home technologies is a significant catalyst. Consumers are increasingly integrating smart devices into their homes, and smart smoke detectors offer enhanced features like remote monitoring, interconnected alarms, and integration with other smart home systems. This provides a more holistic approach to home security. Furthermore, the continuous development of advanced sensor technologies, such as dual-sensor detectors, offers superior fire detection capabilities, attracting a wider consumer base. The affordability of smoke detectors, particularly in the more basic models, also plays a role. Finally, the expansion of e-commerce and online retail channels is facilitating easier access to smoke detectors for consumers, leading to increased sales.

Despite the positive growth trajectory, the residential smoke detector market faces certain challenges. One significant restraint is the prevalence of outdated or malfunctioning detectors in many homes. These devices may not provide adequate protection and contribute to underreporting of fire incidents. Another challenge is the high initial cost of installing and maintaining advanced smart detectors, particularly for budget-conscious consumers. This price barrier could limit adoption, especially in developing economies. Furthermore, the complexity of integrating smart smoke detectors into existing home security systems can pose a hurdle for some users. Battery life and maintenance are also important factors influencing consumer decisions. The need for regular battery replacements can be inconvenient for some homeowners, leading to neglected devices. Competition from less expensive or lower-quality products also affects the market. Finally, regional disparities in building codes and consumer awareness contribute to uneven market penetration across different geographical areas.

The North American and European markets currently dominate the residential smoke detector market, driven by high consumer awareness, stringent building codes, and higher disposable incomes. However, the Asia-Pacific region is experiencing rapid growth, propelled by increasing urbanization, rising middle-class incomes, and government initiatives promoting fire safety.

North America: This region benefits from strong consumer awareness and established building codes that mandate smoke detector installations. The high adoption of smart home technologies also contributes to the region's market dominance.

Europe: Similar to North America, Europe also demonstrates high consumer awareness and strict building regulations related to fire safety. The region showcases diverse market segments catering to varying consumer preferences and technological advancements.

Asia-Pacific: This region is characterized by rapid growth, driven by increasing urbanization, a burgeoning middle class, and governments prioritizing fire safety. The market is witnessing increased demand for both basic and advanced smoke detectors.

Dominant Segment: The dual-sensor smoke detector segment is experiencing the fastest growth due to its superior detection capabilities compared to ionization or photoelectric detectors alone. Dual-sensor detectors offer more reliable protection against a wider variety of fire types, leading to increased consumer preference and market share. This segment is expected to witness significant expansion in the forecast period due to its enhanced safety features and technological advancements. Online sales channels are also demonstrating strong growth, reflecting broader e-commerce trends and providing consumers with convenient access to a wider range of products.

The residential smoke detector industry is fueled by several key growth catalysts, including increasing consumer awareness of fire safety, the mandatory installation requirements in building codes, and the growing adoption of smart home technologies. These factors combine to create a robust demand for both basic and advanced smoke detectors, driving market expansion across various regions and segments. Technological advancements, such as the development of more sensitive and reliable sensors, also contribute to the market's growth.

This report provides a comprehensive overview of the residential smoke detector market, covering key trends, growth drivers, challenges, and leading players. It offers detailed analysis across various segments, including detector type, sales channel, and geography, providing valuable insights for industry stakeholders. The report utilizes a robust forecasting methodology to project market growth over the forecast period (2025-2033), empowering informed decision-making. The extensive market data and detailed company profiles provide a complete picture of the current market landscape and future growth prospects.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.9%.

Key companies in the market include Honeywell, Carrier Global Corporation, Resideo (First Alert), Ei Electronics, Google Nest, Johnson Controls, Swiss Securitas Group, Bosch, WAGNER, FireAngel Safety Technology, ABB (Busch-jaeger), Schneider Electric, Halma, Siemens, Legrand, Smartwares, ABUS, Panasonic Fire & Security, Hochiki, Nittan Group, Zeta Alarms, Nohmi Bosai Limited, Elotec, Eaton, Fireguard, Fireblitz (FireHawk), Inim Electronics, Hugo Brennenstuhl GmbH, SOMFY, eQ-3 (Homematic IP), Minimax, Patol, FARE, Olympia Electronics SA, USI (Universal Security Instruments, Inc.), MTS (UNITEC), Siterwell Electronics, Jade Bird Fire, X-Sense Technology, LEADER Group, Shenzhen Heiman Technology, Zhongxiaoyun Technology, Shenzhen HTI Sanjiang Electronics, Ningbo Kingdun Electronic Industry, Shanghai Songjiang Feifan Electronic, Shenzhen Yanjen Technology, HIKVISION, Dahua Technology.

The market segments include Type.

The market size is estimated to be USD 869 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Residential Smoke Detector," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Residential Smoke Detector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.