1. What is the projected Compound Annual Growth Rate (CAGR) of the Punctal Plugs?

The projected CAGR is approximately 7.33%.

Punctal Plugs

Punctal PlugsPunctal Plugs by Application (Hospitals, Clinic, Others, World Punctal Plugs Production ), by Type (Permanent, Temporary, World Punctal Plugs Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

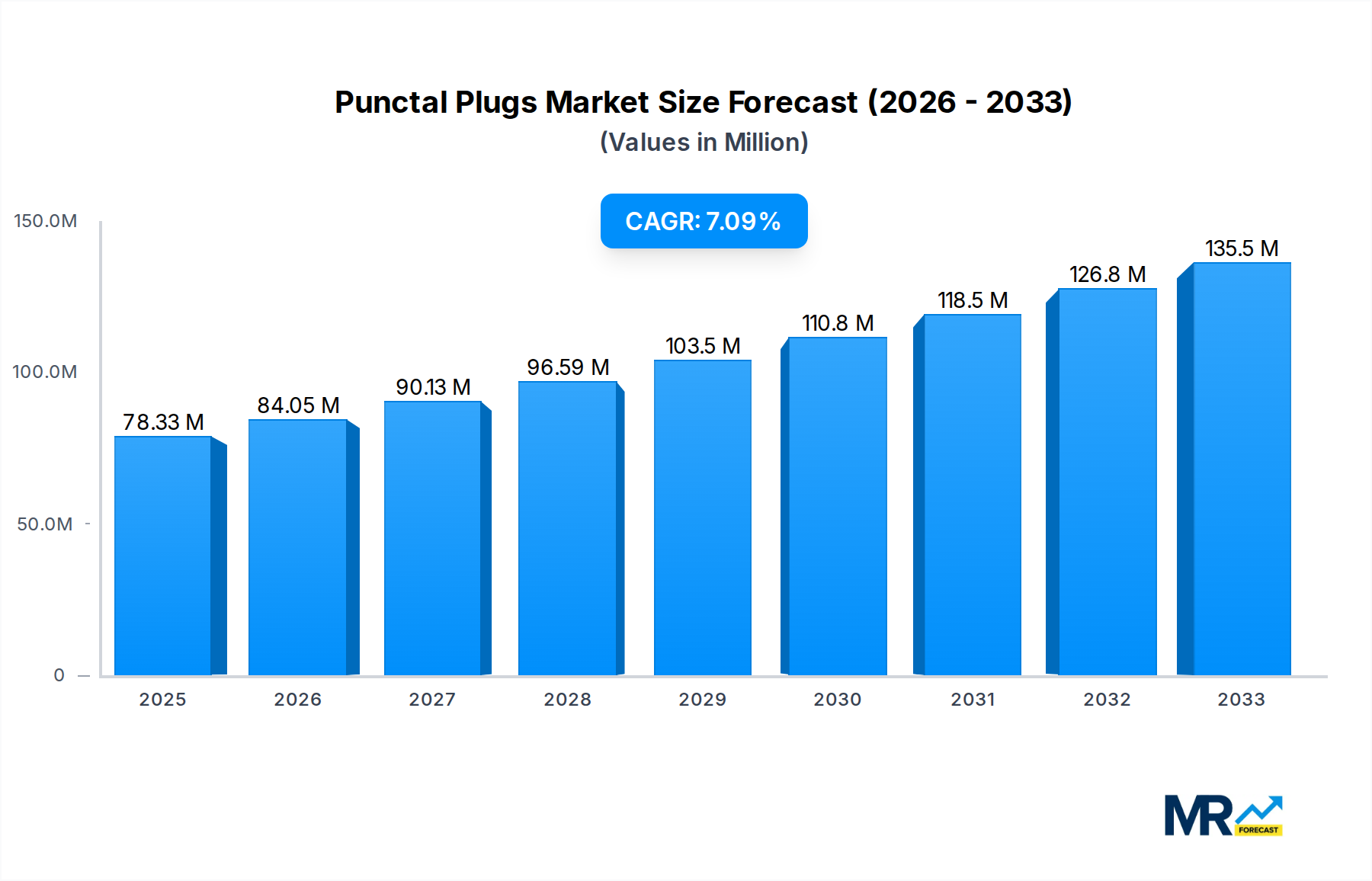

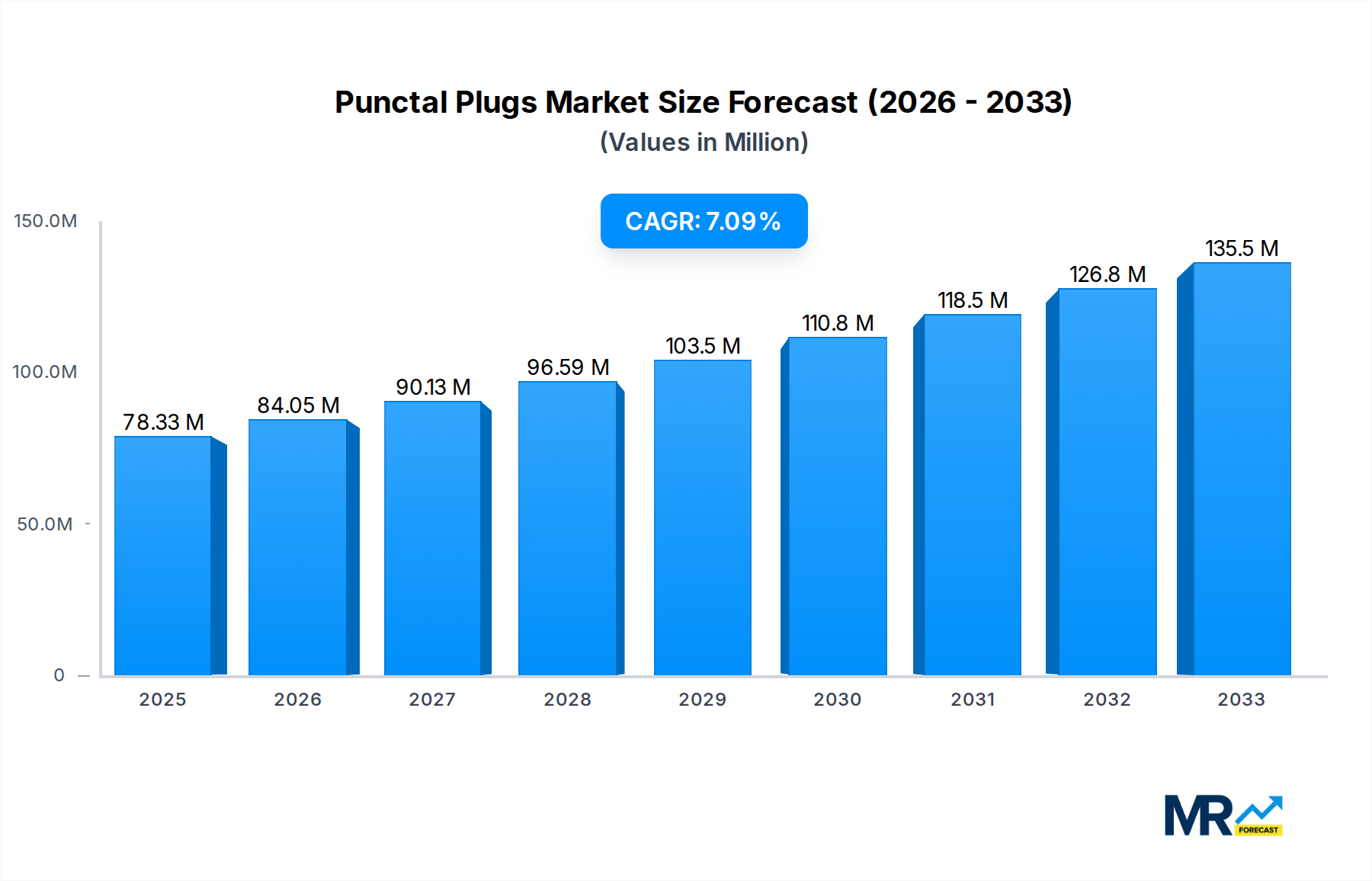

The global punctal plugs market is poised for robust expansion, projected to reach an estimated USD 78.33 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 7.33%. This growth trajectory, expected to extend through 2033, is underpinned by several critical factors. The increasing prevalence of dry eye disease, driven by factors such as an aging population, extended screen time, and environmental pollutants, is a primary catalyst. Furthermore, the growing awareness and diagnosis of ocular surface diseases, coupled with advancements in punctal plug technology leading to improved patient comfort and efficacy, are significant market drivers. The market is segmented by application into hospitals, clinics, and others, with hospitals and specialized ophthalmology clinics expected to lead in adoption due to higher patient volumes and advanced treatment infrastructure. The production landscape is also categorized by type, with both permanent and temporary punctal plugs catering to diverse patient needs and treatment durations.

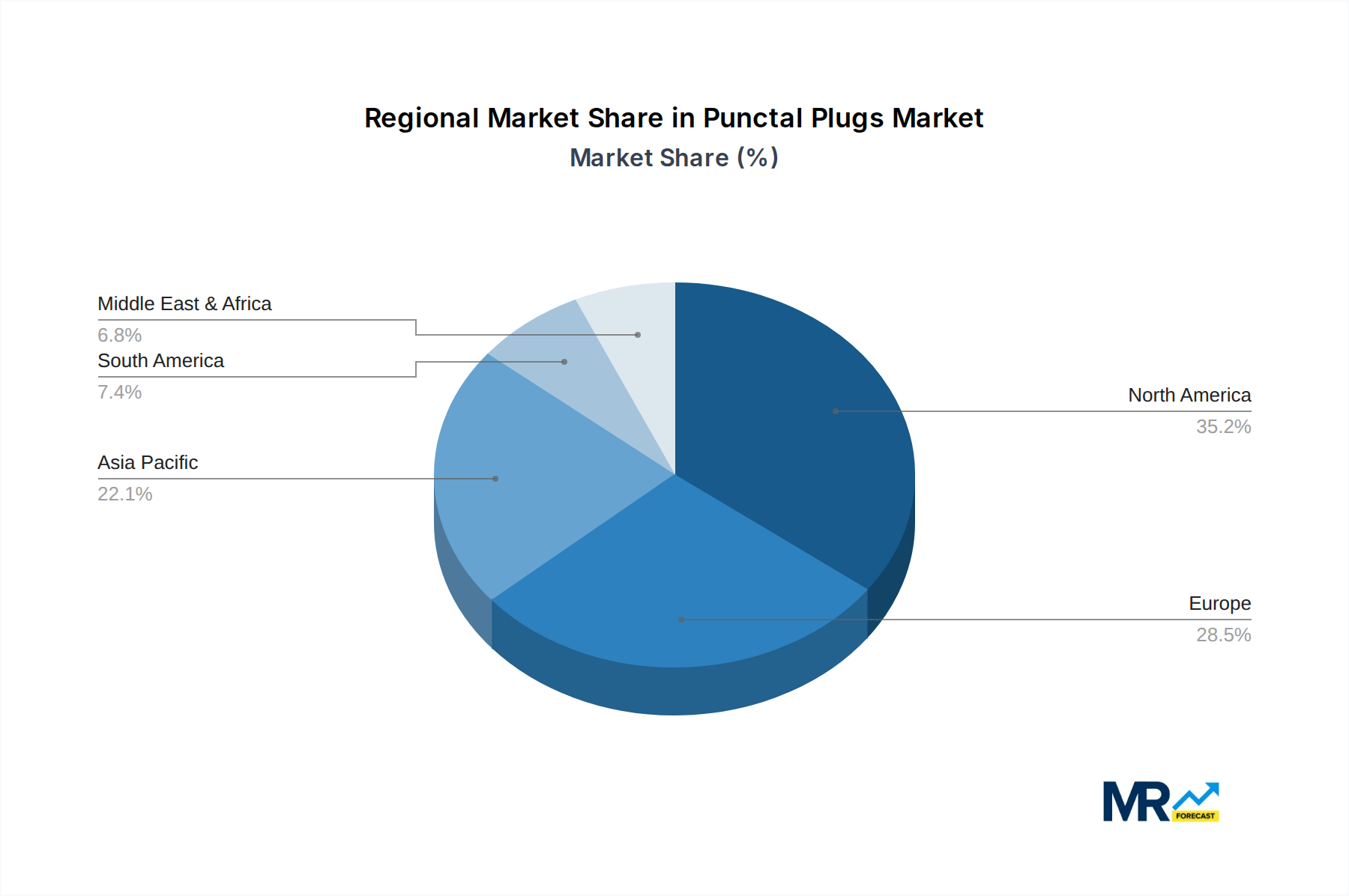

Geographically, North America is anticipated to maintain a dominant market share, fueled by high healthcare expenditure, widespread adoption of advanced medical devices, and a strong emphasis on eye care. Europe follows closely, benefiting from established healthcare systems and a growing elderly demographic susceptible to dry eye conditions. The Asia Pacific region presents a significant growth opportunity, driven by improving healthcare accessibility, rising disposable incomes, and increasing awareness of ophthalmological treatments in countries like China and India. Key market players, including FCI, OASIS Medical, Surgical Specialties Corporation, Medennium, Summit Medical, Eyebright Medical, and MDCO, are actively engaged in product innovation and strategic partnerships to capitalize on these market trends and cater to the escalating demand for effective dry eye management solutions. The market is expected to witness a steady increase in the demand for both permanent and temporary plugs, reflecting a dynamic and responsive industry.

This report offers an in-depth analysis of the global punctal plugs market, forecasting its trajectory from 2019 to 2033, with a base year of 2025. We meticulously examine historical trends from 2019-2024 and provide robust estimations for the forecast period of 2025-2033. The analysis encompasses a detailed breakdown of market dynamics, including key players, technological advancements, and the impact of various end-user segments. With an estimated market size expected to reach millions by 2025, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving punctal plugs landscape.

The global punctal plugs market is poised for significant expansion, driven by a confluence of factors that are reshaping the landscape of dry eye management. Over the historical period of 2019-2024, the market demonstrated steady growth, a trend anticipated to accelerate into the forecast period of 2025-2033. The estimated market size for 2025, projected to be in the millions, underscores the growing importance of these devices in addressing the pervasive issue of dry eye disease. A key trend observed is the increasing preference for minimally invasive treatments, making punctal plugs a highly attractive option for both ophthalmologists and patients. The aging global population is a significant demographic driver, as the incidence of dry eye disease naturally escalates with age. Furthermore, increased awareness campaigns surrounding dry eye symptoms and treatment options are contributing to a larger patient pool seeking effective solutions. The market is also witnessing a continuous evolution in plug materials and designs, with a focus on enhanced biocompatibility, prolonged retention, and improved patient comfort. Innovations in dissolvable and bio-absorbable materials are gaining traction, offering a less invasive alternative for patients. The competitive landscape is characterized by the presence of several key players, each vying for market share through product differentiation and strategic collaborations. The regulatory environment, while generally supportive of medical devices aimed at improving patient outcomes, also plays a crucial role in shaping market access and adoption rates. As the prevalence of digital screen usage continues to rise, leading to increased instances of digital eye strain and associated dry eye, the demand for effective interventions like punctal plugs is expected to surge. The integration of advanced manufacturing techniques is also contributing to cost-effectiveness and scalability, further bolstering market growth. The shift towards personalized medicine and tailored treatment approaches also influences the punctal plugs market, with the development of plugs suited for specific patient needs and tear film characteristics. Ultimately, the punctal plugs market is on an upward trajectory, fueled by both demographic shifts and technological advancements, promising a robust future for this critical segment of ophthalmic care.

Several potent forces are collectively propelling the punctal plugs market towards sustained growth. Foremost among these is the escalating global prevalence of dry eye disease. Factors such as the aging demographic, increased environmental irritants, and widespread digital device usage are contributing to a larger patient population experiencing dry eye symptoms. This growing incidence directly translates into a heightened demand for effective and minimally invasive treatment modalities, a niche perfectly filled by punctal plugs. The inherent advantages of punctal plugs, including their non-invasive nature, rapid procedure time, and immediate symptom relief, make them a preferred choice for both ophthalmologists and patients seeking conservative management options. Unlike other treatments that may require consistent application or carry a higher risk of side effects, punctal plugs offer a simple yet effective solution for prolonging tear retention. Furthermore, advancements in material science and device design are continuously enhancing the efficacy and patient experience. The development of more biocompatible and dissolvable materials is reducing the risk of complications and improving patient comfort, thereby increasing adoption rates. Increased patient and physician awareness regarding the benefits and availability of punctal plugs is also a significant driver. As educational initiatives and marketing efforts highlight the effectiveness of punctal plugs in managing dry eye, more individuals are seeking this treatment option. The supportive regulatory landscape for ophthalmic medical devices, particularly those that demonstrate clear clinical benefits and patient safety, further facilitates market expansion. Finally, the healthcare sector's increasing focus on cost-effectiveness and outpatient procedures aligns well with the economic advantages offered by punctal plug insertion, making it an attractive option for healthcare providers and payers.

Despite its promising growth trajectory, the punctal plugs market encounters several hurdles that can temper its expansion. A primary challenge lies in the perception and awareness surrounding punctal plugs. While physician awareness is generally high, patient understanding and acceptance of punctal plugs as a viable and safe treatment option may still be limited in certain regions. This can stem from a lack of information or a preference for more familiar, albeit sometimes less effective, over-the-counter remedies. The availability of alternative dry eye treatments, including artificial tears, prescription eye drops, and other surgical interventions, presents a competitive restraint. Patients and physicians may opt for these alternatives based on perceived efficacy, cost, or familiarity, potentially delaying or bypassing punctal plug consideration. Reimbursement policies and insurance coverage can also pose a significant challenge. In some healthcare systems, the reimbursement for punctal plug procedures may be inconsistent or inadequate, leading to higher out-of-pocket costs for patients and discouraging widespread adoption. Palpable insertion site reactions or discomfort, though generally rare with modern plugs, can also be a concern for some patients. While advancements in materials have minimized these issues, the possibility of minor irritation, foreign body sensation, or even plug expulsion can lead to patient hesitancy and negatively impact market growth. Furthermore, the specialized nature of punctal plug insertion requires trained medical professionals. A shortage of ophthalmologists or optometrists skilled in this specific procedure in certain geographic areas could limit access and thus market penetration. Finally, the ongoing research and development of novel dry eye treatments, including advanced biologics and sustained-release drug delivery systems, could potentially offer superior efficacy or convenience, thereby posing a future threat to the punctal plugs market if they achieve widespread adoption and prove to be more cost-effective.

The global punctal plugs market is characterized by a dynamic interplay between geographical regions and market segments, with certain areas and applications poised for significant dominance.

Dominant Regions:

North America: This region is expected to maintain its leading position in the punctal plugs market. This dominance is attributed to several factors:

Europe: Europe is another significant market for punctal plugs, driven by similar factors to North America.

Dominant Segments:

Application: Clinics:

Type: Permanent Punctal Plugs:

World Punctal Plugs Production:

While Hospitals also contribute to the application segment, their role is often for more complex cases or when initial treatments have failed. The "Others" segment might encompass specialized eye care centers or research facilities, but clinics remain the predominant application for routine punctal plug procedures. Similarly, Temporary punctal plugs serve a specific purpose, particularly for short-term relief or diagnostic purposes, but the long-term benefits of permanent plugs are driving their higher market penetration, contributing significantly to the millions of units produced and sold worldwide. The synergy between a growing patient pool experiencing dry eye and the development of advanced, convenient, and effective punctal plug solutions solidifies the dominance of clinics and permanent plugs in the global market.

The punctal plugs industry is experiencing several potent growth catalysts that are fueling its expansion. The increasing global prevalence of dry eye disease, driven by an aging population and heightened digital device usage, creates a larger patient pool actively seeking effective relief. Advancements in punctal plug materials and designs, focusing on enhanced biocompatibility, patient comfort, and extended retention, are making these devices more attractive and accessible. Furthermore, growing awareness among both patients and healthcare professionals regarding the efficacy and minimally invasive nature of punctal plugs is a significant driver. The shift towards value-based healthcare and the preference for cost-effective outpatient procedures further position punctal plugs as a favorable treatment option.

This report provides a comprehensive and granular analysis of the global punctal plugs market, offering a deep dive into its intricacies. It covers an extensive study period from 2019-2033, with a pivotal base and estimated year of 2025, and a detailed forecast period of 2025-2033. The report dissects key market trends, including the estimated millions in market value, and explores the driving forces behind market expansion, such as the rising prevalence of dry eye disease and technological innovations. Crucially, it also addresses the challenges and restraints impacting market growth, including reimbursement issues and alternative treatments. The analysis meticulously identifies key regions and segments, such as clinics and permanent punctal plugs, that are expected to dominate the market, supported by millions of units in production and application. Furthermore, it highlights significant growth catalysts and provides a list of leading players. Finally, the report details significant industry developments and concludes with a thorough overview, making it an indispensable tool for stakeholders seeking to navigate and succeed in the evolving punctal plugs landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.33% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.33%.

Key companies in the market include FCI, OASIS Medical, Surgical Specialties Corporation, Medennium, Summit Medical, Eyebright Medical, MDCO.

The market segments include Application, Type.

The market size is estimated to be USD 78.33 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Punctal Plugs," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Punctal Plugs, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.