1. What is the projected Compound Annual Growth Rate (CAGR) of the Proton Therapy for Cancer?

The projected CAGR is approximately XX%.

Proton Therapy for Cancer

Proton Therapy for CancerProton Therapy for Cancer by Application (Hosptial, Proton Treatment Center), by Type (Synchrotron, Cyclotron, Synchrocyclotron, Linear accelerator), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

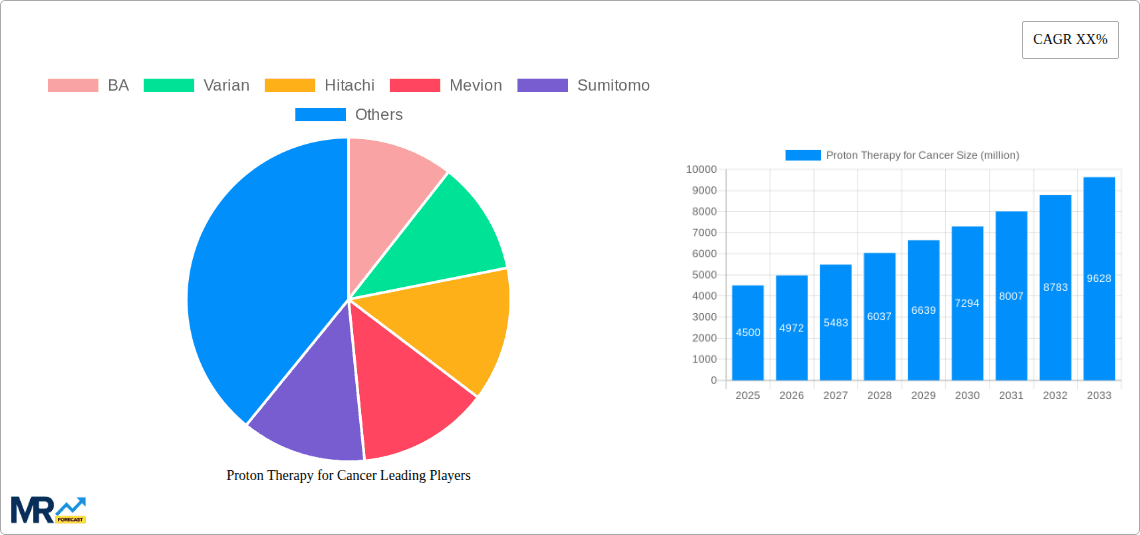

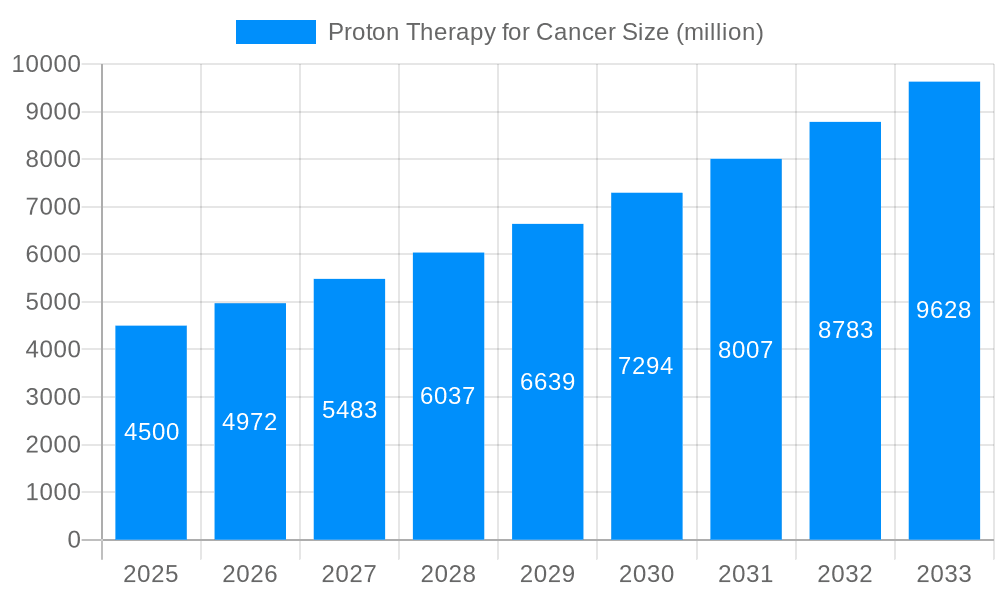

The global market for Proton Therapy for Cancer is poised for substantial expansion, projected to reach approximately $4,500 million by 2025, with a remarkable Compound Annual Growth Rate (CAGR) of 10.5% anticipated through 2033. This robust growth trajectory is primarily fueled by an increasing global incidence of cancer, driving greater demand for advanced and more precise treatment modalities. Proton therapy, known for its superior efficacy in targeting tumors while minimizing damage to surrounding healthy tissues, is gaining significant traction as a preferred treatment option for a wide spectrum of cancers, including brain tumors, head and neck cancers, prostate cancer, and pediatric malignancies. The continuous advancements in technology, leading to more compact and cost-effective cyclotron and synchrotron systems, are further democratizing access to this life-saving therapy, expanding its reach beyond specialized centers. Furthermore, heightened awareness among patients and healthcare providers regarding the benefits of proton therapy, such as reduced side effects and improved quality of life post-treatment, is a critical driver of market adoption.

The market's growth is further propelled by increasing investments in research and development by leading companies like Varian, Hitachi, and Mevion, focused on enhancing treatment delivery systems and expanding the therapeutic applications of proton therapy. The expansion of proton treatment centers globally, coupled with supportive government initiatives and reimbursement policies in various regions, also contributes significantly to market dynamics. While the high initial cost of setting up proton therapy facilities and a shortage of trained personnel present certain restraints, the long-term clinical benefits and improving economic viability are steadily overcoming these challenges. Key market segments include hospitals and dedicated proton treatment centers, with synchrotron and cyclotron technologies dominating the market. North America and Europe currently lead in market share, driven by advanced healthcare infrastructure and early adoption, but the Asia Pacific region is emerging as a high-growth market due to escalating cancer rates and increasing healthcare expenditure.

The global proton therapy market, a rapidly evolving segment within cancer treatment, is projected to witness substantial growth over the Study Period of 2019-2033, with the Base Year and Estimated Year set at 2025, and a Forecast Period spanning 2025-2033. This advanced form of radiation therapy, known for its precision in targeting cancerous cells while minimizing damage to surrounding healthy tissues, has garnered significant attention from medical professionals and patients alike. The Historical Period (2019-2024) has laid a strong foundation, characterized by increasing adoption rates and technological advancements that have driven down costs and improved treatment efficacy. Key market insights reveal a strong upward trajectory, with the market value expected to reach several million dollars. For instance, by 2025, the estimated market value is likely to be in the range of $2,000 million to $3,000 million. By the end of the Forecast Period in 2033, this figure is anticipated to climb significantly, potentially exceeding $6,000 million. This growth is fueled by a confluence of factors, including the rising global cancer incidence, a growing awareness among patients about advanced treatment options, and supportive government initiatives aimed at enhancing cancer care infrastructure. Furthermore, ongoing research and development efforts are continuously refining proton therapy techniques, leading to improved patient outcomes and a broader range of applicable cancer types. The integration of artificial intelligence and machine learning in treatment planning and delivery is further enhancing the precision and efficiency of proton therapy, making it a more attractive option for complex cases. The market is also experiencing a geographical expansion, with new treatment centers emerging in regions previously underserved, thus broadening access to this life-saving technology. The increasing preference for non-invasive and targeted cancer therapies over traditional methods like surgery and conventional radiotherapy is another crucial trend. This shift is driven by the desire to reduce treatment side effects and improve the quality of life for cancer survivors. The development of more compact and cost-effective proton therapy systems is also playing a pivotal role in democratizing access to this technology, making it feasible for a wider array of healthcare institutions. The increasing number of clinical trials and the growing body of evidence supporting the efficacy of proton therapy for various cancer types are further solidifying its position as a cornerstone of modern oncology.

The burgeoning demand for proton therapy for cancer is propelled by a multifaceted set of drivers that are fundamentally reshaping the landscape of oncology. A primary impetus is the escalating global burden of cancer, with increasing incidence rates across various age groups and cancer types. This surge necessitates the adoption of more effective and less debilitating treatment modalities, a role that proton therapy is increasingly fulfilling. Patients and oncologists are actively seeking treatments that offer superior tumor control with significantly reduced toxicity to healthy tissues, thereby improving survival rates and enhancing the quality of life for survivors. The technological advancements within the proton therapy sector are also a significant driving force. Innovations in beam delivery systems, imaging technologies, and treatment planning software are leading to greater precision, improved therapeutic ratios, and ultimately, better patient outcomes. For instance, the evolution from single-room systems to more integrated, multi-room facilities, coupled with advancements in superconducting cyclotrons and synchrotrons, has made proton therapy more accessible and efficient. Furthermore, supportive government policies and reimbursement schemes in many developed and developing nations are playing a crucial role in facilitating the establishment and adoption of proton therapy centers. These policies often include grants for facility construction, funding for research, and favorable reimbursement rates for proton therapy procedures, thereby lowering the financial barrier for both institutions and patients. The growing awareness and positive perception of proton therapy among the general public, driven by successful patient stories and media coverage, are also contributing to its increasing demand. As more evidence of its efficacy emerges from clinical studies and real-world data, the confidence in proton therapy as a frontline treatment option is steadily growing, further accelerating its market penetration.

Despite its promising trajectory, the proton therapy for cancer market is not without its significant challenges and restraints. Foremost among these is the exceptionally high initial capital investment required for establishing a proton therapy center. The complex infrastructure, including specialized equipment like cyclotrons or synchrotrons, shielding, and treatment rooms, necessitates an expenditure often running into tens or even hundreds of millions of dollars, making it a prohibitive cost for many healthcare providers, particularly in resource-constrained regions. This substantial financial hurdle limits the widespread availability and accessibility of proton therapy. Compounding this issue is the relatively higher cost of proton therapy treatments compared to conventional radiotherapy. While the long-term benefits in terms of reduced side effects and improved outcomes may justify the cost, the immediate financial burden for patients and healthcare systems remains a significant obstacle. This cost disparity often impacts insurance coverage policies, leading to challenges in reimbursement for proton therapy procedures in certain regions or for specific cancer types. Another considerable challenge lies in the limited availability of trained personnel. Operating and maintaining proton therapy facilities requires a specialized workforce, including medical physicists, radiation oncologists, and dosimetrists with expertise in this complex technology. The scarcity of such skilled professionals can hinder the expansion and efficient functioning of existing centers and the establishment of new ones. Furthermore, the learning curve associated with adopting proton therapy for new indications and patient populations can be steep. Extensive research and clinical validation are often required to establish its efficacy and safety for a wider range of cancers, which takes time and resources. Lastly, the physical footprint of traditional proton therapy facilities, requiring large dedicated spaces for the accelerator and treatment rooms, can be a constraint in densely populated urban areas or in existing hospitals with limited expansion capabilities.

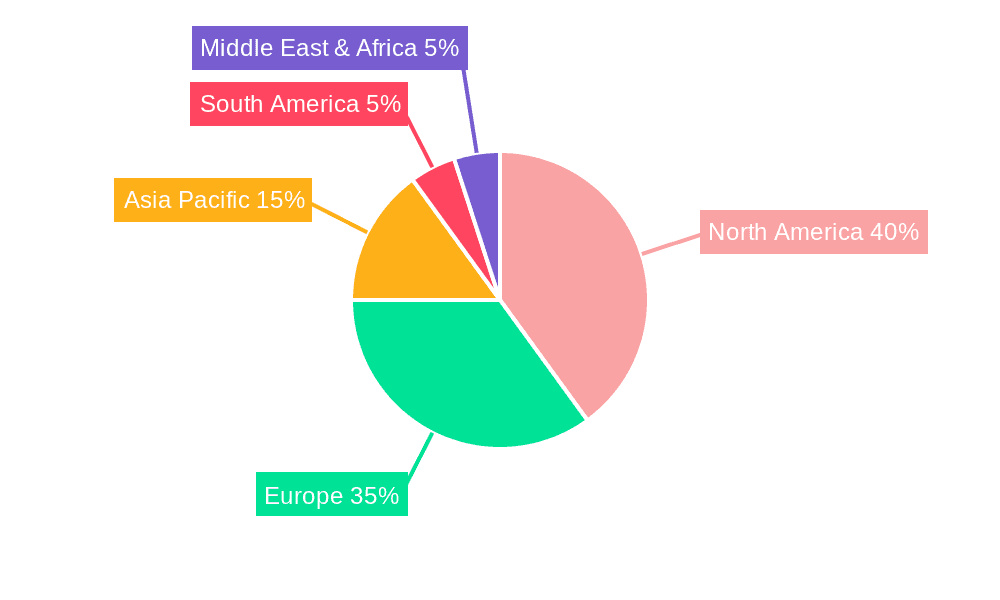

Dominant Region/Country: North America, particularly the United States, is poised to continue its dominance in the proton therapy for cancer market. This leadership is attributed to a confluence of factors, including a robust healthcare infrastructure, a high prevalence of cancer, a well-established ecosystem for advanced medical technologies, and significant investment in research and development. The United States has been at the forefront of adopting and refining proton therapy, with a considerable number of operational centers and ongoing expansion plans. Favorable reimbursement policies from private insurers and government programs like Medicare, though subject to scrutiny, have historically supported the adoption of proton therapy. The presence of leading research institutions and academic medical centers actively involved in clinical trials and technological innovation further solidifies North America's lead. By 2025, the market share held by North America is estimated to be in the range of 40-50%, with the US accounting for the lion's share of this. By the end of the Forecast Period in 2033, this dominance is expected to persist, though the gap with other emerging regions might narrow as global adoption increases.

Dominant Segment: Within the proton therapy market, the Hospital application segment is projected to be the primary driver of growth and market share. While dedicated Proton Treatment Centers play a crucial role, the integration of proton therapy within established hospital systems offers significant advantages. Hospitals possess existing patient bases, established referral networks, and comprehensive ancillary services (oncology, surgery, diagnostic imaging, pathology) that complement proton therapy. This integrated approach allows for more seamless patient management, multidisciplinary care, and potentially greater cost efficiencies by leveraging existing hospital infrastructure and resources. By 2025, the Hospital segment is expected to account for over 60% of the total market revenue. The trend towards establishing proton therapy units as part of comprehensive cancer centers within larger hospitals is anticipated to accelerate, driven by the desire to offer the most advanced treatment options under one roof. This also facilitates easier access for patients who may require other forms of cancer treatment alongside or in conjunction with proton therapy.

Type of Accelerator - Synchrotron: Among the types of accelerators used for proton therapy, the Synchrotron is expected to be a leading segment, particularly in terms of market share and technological advancement. Synchrotrons offer greater flexibility in beam energy modulation, which is crucial for delivering precise doses to tumors of varying depths and shapes. Their ability to precisely control the proton beam's energy allows for more sophisticated treatment techniques, such as pencil beam scanning, which is highly effective in conformally irradiating tumors. By 2025, the Synchrotron segment is projected to hold a significant portion, estimated at around 45-55%, of the accelerator market for proton therapy. While cyclotrons are more compact and cost-effective, the advanced capabilities and treatment precision offered by synchrotrons, especially for complex cases and advanced clinical protocols, are driving their continued adoption and market dominance. The ongoing development of more compact and efficient synchrotron designs is further bolstering their appeal.

The proton therapy industry is experiencing significant growth catalysts, primarily driven by the continuous advancement in technology, leading to more compact and cost-effective systems. This includes innovations in superconducting magnets and beam delivery components, making installation and operation more feasible for a broader range of healthcare facilities. The expanding body of clinical evidence demonstrating superior outcomes and reduced side effects compared to conventional radiotherapy for specific cancer types is a crucial catalyst, enhancing physician confidence and patient demand. Furthermore, increasing government support and favorable reimbursement policies in several key markets are significantly lowering the financial barriers to adoption and treatment. The growing global awareness among patients about advanced cancer treatment options and their potential benefits is also a major catalyst, driving demand for proton therapy services.

This comprehensive report delves into the intricate dynamics of the proton therapy for cancer market, providing an in-depth analysis of its historical performance, current status, and future projections. It offers a granular examination of market trends, driven by rising cancer incidence, technological innovations, and evolving patient preferences for less invasive treatments. The report meticulously outlines the key driving forces, including technological advancements in accelerators and beam delivery, alongside supportive government initiatives and increasing global awareness. Conversely, it addresses the significant challenges such as high capital expenditure, treatment costs, and the scarcity of skilled professionals that need to be overcome for widespread adoption. The report provides a detailed segmentation of the market by application (Hospital, Proton Treatment Center), type of accelerator (Synchrotron, Cyclotron, Synchrocyclotron, Linear accelerator), and geographical regions, identifying key areas and segments poised for dominance. It also highlights critical growth catalysts, significant industry developments, and the strategic approaches of leading players like BA, Varian, Hitachi, Mevion, Sumitomo, and ProNova. The report’s extensive coverage, spanning the Study Period of 2019-2033, with a Base Year of 2025 and a Forecast Period of 2025-2033, equips stakeholders with invaluable insights for strategic decision-making in this rapidly advancing field of oncology.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include BA, Varian, Hitachi, Mevion, Sumitomo, ProNova, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Proton Therapy for Cancer," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Proton Therapy for Cancer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.