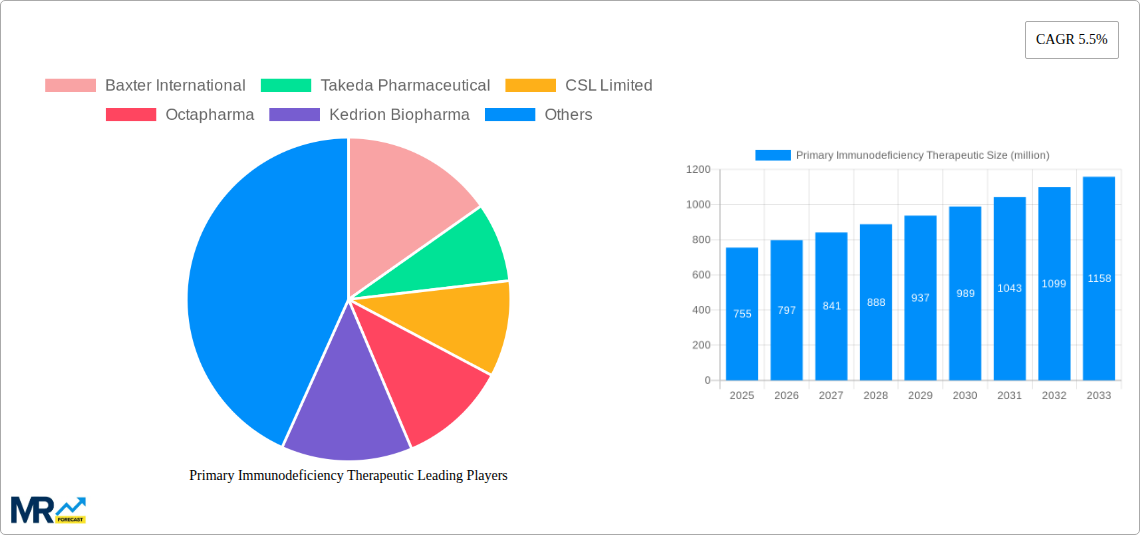

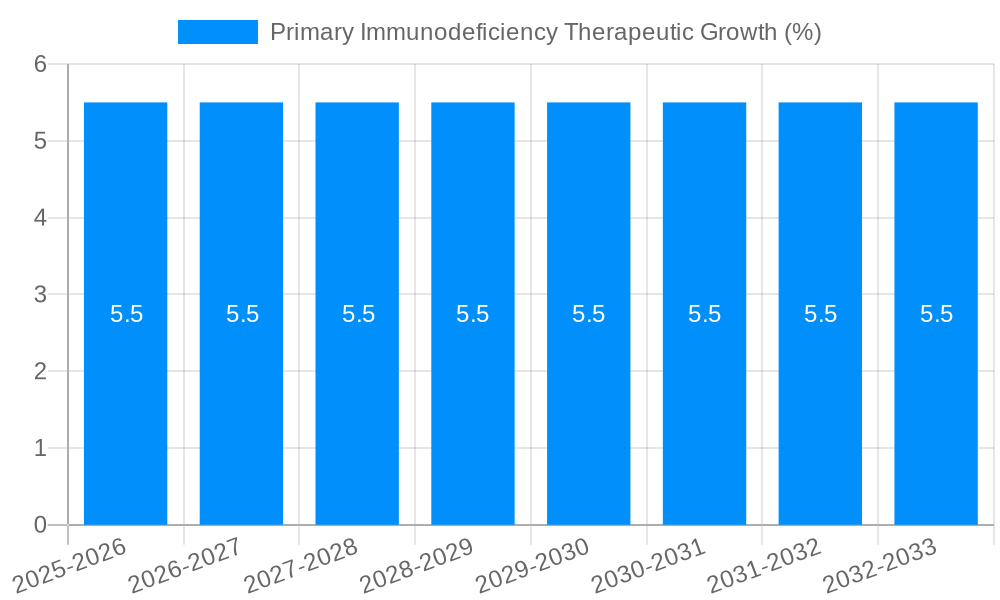

1. What is the projected Compound Annual Growth Rate (CAGR) of the Primary Immunodeficiency Therapeutic?

The projected CAGR is approximately 5.5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Primary Immunodeficiency Therapeutic

Primary Immunodeficiency TherapeuticPrimary Immunodeficiency Therapeutic by Type (Immunoglobulin Replacement Therapy, Stem Cell or Bone Marrow Transplantation, Antibiotic Therapy, Gene Therapy, Others), by Application (Antibody Deficiency, Cellular Immunodeficiency, Innate Immune Disorders, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Primary Immunodeficiency Therapeutic market is poised for significant expansion, currently valued at an estimated USD 755 million. This robust growth is underpinned by a projected Compound Annual Growth Rate (CAGR) of 5.5%, indicating a dynamic and expanding sector driven by increasing awareness, improved diagnostic capabilities, and advancements in treatment modalities. The market is primarily propelled by the rising prevalence of antibody deficiencies and cellular immunodeficiencies, which are becoming more accurately identified and managed. Immunoglobulin Replacement Therapy stands as a dominant segment, benefiting from its established efficacy and widespread adoption in managing antibody deficiencies. Concurrently, the development and increasing accessibility of more advanced treatments like gene therapy and stem cell/bone marrow transplantation are creating new avenues for market growth, particularly for patients with severe or complex immune disorders. The market's trajectory is also influenced by a growing understanding of innate immune disorders, further broadening the therapeutic landscape.

Several key trends are shaping the Primary Immunodeficiency Therapeutic market. The increasing investment in research and development by leading pharmaceutical companies, including Baxter International, Takeda Pharmaceutical, and CSL Limited, is a critical driver. These investments are focused on developing novel therapies and improving existing ones, leading to enhanced treatment outcomes and patient quality of life. Furthermore, supportive government initiatives and growing healthcare expenditure in developed and emerging economies are creating a more conducive environment for market penetration. While the market enjoys strong growth drivers, potential restraints include the high cost of certain advanced therapies, particularly gene and stem cell therapies, which can limit accessibility for a segment of the patient population. Additionally, challenges related to diagnosis in rare and less common primary immunodeficiencies can pose a hurdle. However, the overall outlook remains highly positive, with continuous innovation and expanding treatment options set to overcome these challenges and fuel sustained market expansion over the forecast period.

Here's a unique report description on Primary Immunodeficiency Therapeutics, incorporating the provided details:

The global Primary Immunodeficiency (PID) Therapeutics market is poised for substantial growth, driven by increasing disease awareness, advancements in diagnostic capabilities, and the development of novel treatment modalities. Historically, from 2019 to 2024, the market experienced steady expansion, largely anchored by immunoglobulin replacement therapies which represented a significant portion of treatment protocols. The estimated market size in the base year, 2025, is projected to be in the several billion unit range, reflecting the ongoing demand for effective PID management. Looking ahead through the forecast period of 2025-2033, this trajectory is expected to accelerate, with the market potentially reaching tens of billions of units by 2033. This upward trend is further amplified by the introduction of more targeted therapies and an expanding understanding of the underlying genetic causes of various PID types. Key market insights reveal a growing preference for individualized treatment plans, moving beyond a one-size-fits-all approach. The increasing incidence of rare diseases, coupled with improved patient registries and genetic screening programs, is contributing to a more precise identification of patients requiring specific interventions. Furthermore, the economic burden associated with untreated or poorly managed PID is prompting greater investment in both research and accessible treatment options. The base year 2025 serves as a crucial inflection point, with ongoing clinical trials and regulatory approvals set to reshape the treatment landscape. The market's growth is not uniform across all segments, with certain therapeutic types and applications showing more robust expansion than others. The increasing adoption of advanced treatment modalities, such as gene therapy, while still nascent, holds immense promise for long-term disease modification, and its impact will become more pronounced during the latter half of the forecast period. Overall, the PID therapeutics market is characterized by a dynamic interplay of scientific innovation, evolving clinical practice, and increasing patient advocacy, all contributing to a promising future.

Several potent forces are actively propelling the Primary Immunodeficiency Therapeutics market forward. Foremost among these is the escalating global prevalence of PID, driven by improved diagnostic tools and heightened awareness among healthcare professionals and the general public. This increased identification of affected individuals directly translates into a larger patient pool requiring therapeutic intervention. Secondly, remarkable strides in biomedical research have unlocked a deeper understanding of the intricate mechanisms underlying various PID types. This knowledge is crucial for the development of more precise and effective therapeutic strategies. The growing investment by pharmaceutical and biotechnology companies in R&D, particularly in areas like gene therapy and advanced immunoglobulin formulations, is a significant catalyst. Furthermore, the increasing accessibility of advanced diagnostic technologies, including genetic sequencing, allows for earlier and more accurate diagnosis, leading to timely initiation of treatment and better patient outcomes. The unmet medical needs associated with severe and complex PIDs continue to incentivize innovation and the pursuit of breakthrough therapies that can offer transformative benefits.

Despite the promising growth trajectory, the Primary Immunodeficiency Therapeutics market faces several significant challenges and restraints that could temper its expansion. A primary hurdle is the inherent complexity and rarity of many PID subtypes, leading to diagnostic delays and challenges in patient identification. This can result in delayed treatment initiation, potentially impacting long-term outcomes and market penetration for specific therapies. The high cost of advanced PID therapies, particularly novel biologics and gene therapies, poses a significant barrier to accessibility for many patients and healthcare systems globally. This economic burden can limit widespread adoption and create disparities in treatment access. Furthermore, the limited availability of specialized treatment centers and trained healthcare professionals in certain regions can restrict the delivery of optimal care. The long-term safety and efficacy data for some newer therapeutic modalities, such as gene therapy, are still being gathered, which can create hesitation among some prescribers and payers. Regulatory hurdles and lengthy approval processes for innovative treatments can also slow down market entry and adoption.

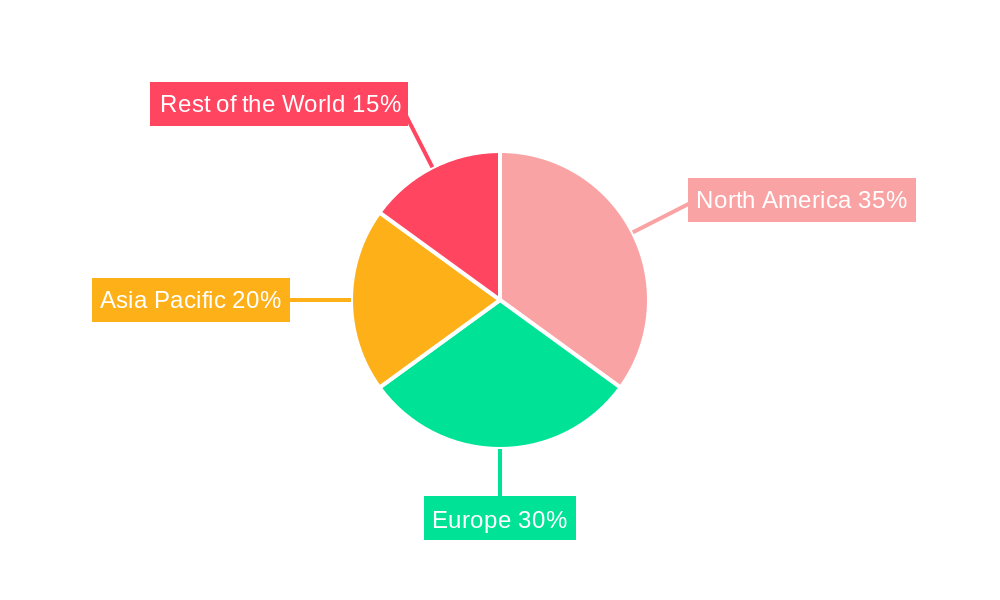

The Primary Immunodeficiency Therapeutic market is poised for dominance by specific regions and segments that are strategically positioned to leverage current trends and future advancements.

Key Regions/Countries Expected to Lead:

North America (United States & Canada): This region is anticipated to maintain its leading position due to several factors. The well-established healthcare infrastructure, high disposable income, and strong emphasis on research and development foster rapid adoption of novel therapies. The presence of leading pharmaceutical companies actively engaged in PID research and manufacturing contributes significantly to market growth. Furthermore, a high prevalence of diagnostic capabilities and patient registries enables better identification and management of PID cases. The reimbursement landscape, while complex, generally supports access to advanced treatments for eligible patients.

Europe (Germany, United Kingdom, France): Europe is another powerhouse in the PID therapeutics market. Countries like Germany and the UK have robust healthcare systems with a strong focus on patient care and innovation. Significant government and private funding for medical research, coupled with a growing understanding of rare diseases, fuels market expansion. The increasing prevalence of genetic testing and a proactive approach to rare disease management contribute to its dominance. The market here is characterized by a strong presence of key industry players and a sophisticated regulatory environment that encourages innovation while ensuring patient safety.

Asia Pacific (China, Japan, India): While currently a developing market, the Asia Pacific region is projected to witness the most substantial growth rate in the coming years. This is attributed to a burgeoning awareness of PID, improving healthcare infrastructure, and a growing middle class with increased purchasing power. Government initiatives aimed at enhancing healthcare access and a rising number of clinical trials conducted in the region are further driving market penetration. The sheer population size of countries like China and India presents a vast untapped market for PID therapeutics.

Dominant Segment: Immunoglobulin Replacement Therapy (IRT)

Market Share and Rationale: Immunoglobulin Replacement Therapy (IRT) is expected to continue its reign as the dominant segment within the PID therapeutics market. This dominance is multifaceted, stemming from its established efficacy, broad applicability across numerous PID types, and its historical role as the cornerstone of PID management. The vast majority of PID patients, particularly those with antibody deficiencies, rely on IRT for survival and to prevent severe infections.

Dominant Application: Antibody Deficiency

Prevalence and Impact: Antibody Deficiency remains the most prevalent category of PID, directly contributing to the dominance of IRT. Conditions such as Common Variable Immunodeficiency (CVID), X-linked Agammaglobulinemia (XLA), and Selective IgA Deficiency fall under this umbrella, collectively representing a significant portion of the diagnosed PID population.

While other segments like Gene Therapy are poised for significant future growth and hold immense potential for curative treatments, their current market penetration is limited by factors such as high cost, complexity of administration, and the need for extensive long-term safety data. Consequently, Immunoglobulin Replacement Therapy for Antibody Deficiencies will continue to be the bedrock of the PID therapeutics market for the foreseeable future.

Several key growth catalysts are fueling the expansion of the Primary Immunodeficiency Therapeutics industry. The most significant is the ongoing discovery and characterization of novel PID genes, leading to a more comprehensive understanding of disease pathogenesis and the identification of new therapeutic targets. This scientific advancement directly translates into the development of innovative treatment options. Furthermore, the increasing adoption of genetic sequencing technologies is enabling earlier and more accurate diagnosis, expanding the diagnosed patient pool and consequently the demand for treatments. Improvements in diagnostic algorithms and increased awareness among healthcare providers are also crucial catalysts. Finally, the growing pipeline of advanced therapies, including gene therapies and novel biologics, promises to offer more effective and potentially curative solutions, attracting substantial investment and driving market growth.

This comprehensive report delves deep into the Primary Immunodeficiency Therapeutics market, providing a detailed analysis from the historical period of 2019-2024 through to an extensive forecast period of 2025-2033. The base year of 2025 serves as a crucial benchmark for understanding current market dynamics, with an estimated valuation in the billions of units. The report meticulously examines the prevailing trends, highlighting the dominance of Immunoglobulin Replacement Therapy as the primary treatment modality for Antibody Deficiencies. It further dissects the driving forces behind market expansion, including increased disease awareness, diagnostic advancements, and robust R&D investments. Conversely, the report also sheds light on the challenges and restraints, such as the high cost of advanced therapies and diagnostic complexities. A significant portion is dedicated to identifying key regions and segments poised for market leadership, with a detailed exploration of factors contributing to their dominance. Leading players are identified, alongside a timeline of significant industry developments. The report offers unparalleled insights into market segmentation by therapeutic type, application, and geographical landscape, providing a holistic view for stakeholders navigating this dynamic sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.5%.

Key companies in the market include Baxter International, Takeda Pharmaceutical, CSL Limited, Octapharma, Kedrion Biopharma, Bio Products Laboratory, LFB group, Grifols, Lupin Pharmaceuticals.

The market segments include Type, Application.

The market size is estimated to be USD 755 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Primary Immunodeficiency Therapeutic," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Primary Immunodeficiency Therapeutic, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.