1. What is the projected Compound Annual Growth Rate (CAGR) of the Plastic Intake Manifold?

The projected CAGR is approximately XX%.

Plastic Intake Manifold

Plastic Intake ManifoldPlastic Intake Manifold by Type (PA6, PP, Others, World Plastic Intake Manifold Production ), by Application (OEM, Aftermarket, World Plastic Intake Manifold Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

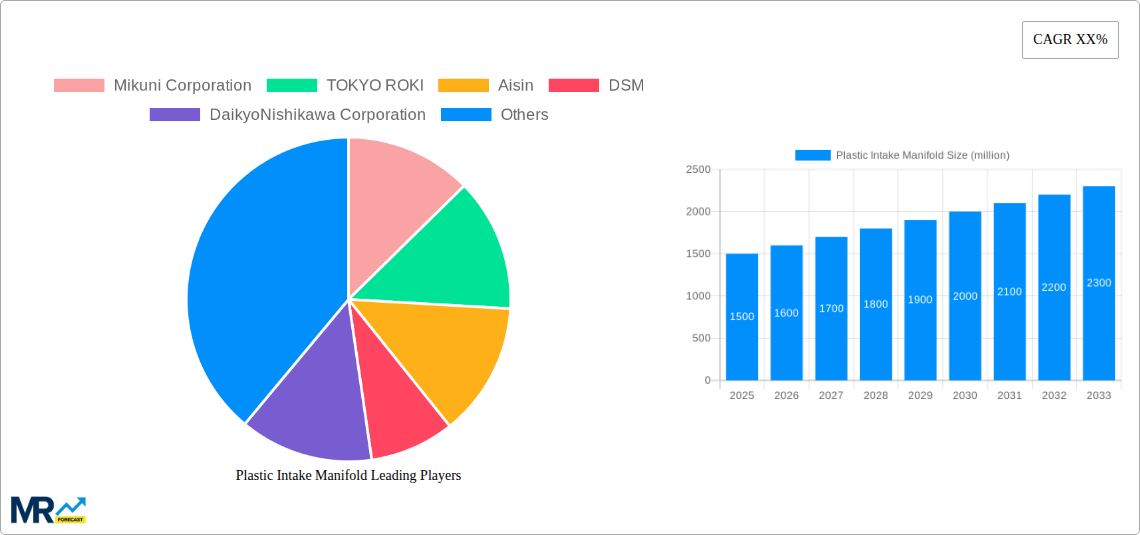

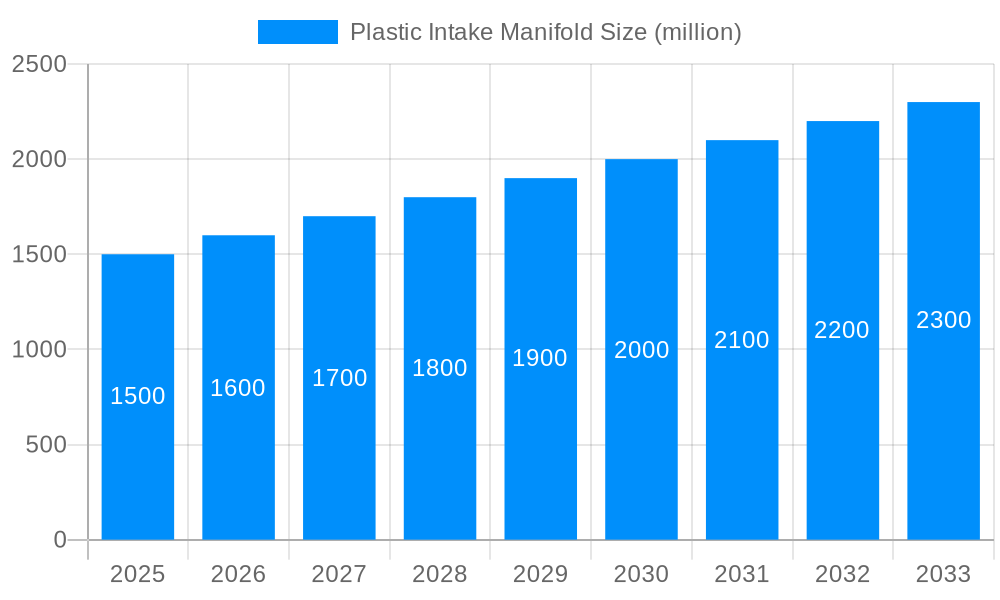

The global Plastic Intake Manifold market is poised for significant expansion, projected to reach a substantial size of 2091.9 million by 2033. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period of 2025-2033. Key drivers underpinning this expansion include the escalating demand for lightweight and fuel-efficient automotive components, driven by increasingly stringent emission regulations worldwide. The inherent advantages of plastic intake manifolds over traditional metal counterparts, such as reduced weight, improved thermal insulation, and enhanced design flexibility, are making them the preferred choice for modern vehicle manufacturing. Furthermore, the continuous innovation in polymer technology, leading to more durable and cost-effective plastic materials, is also playing a crucial role in market penetration.

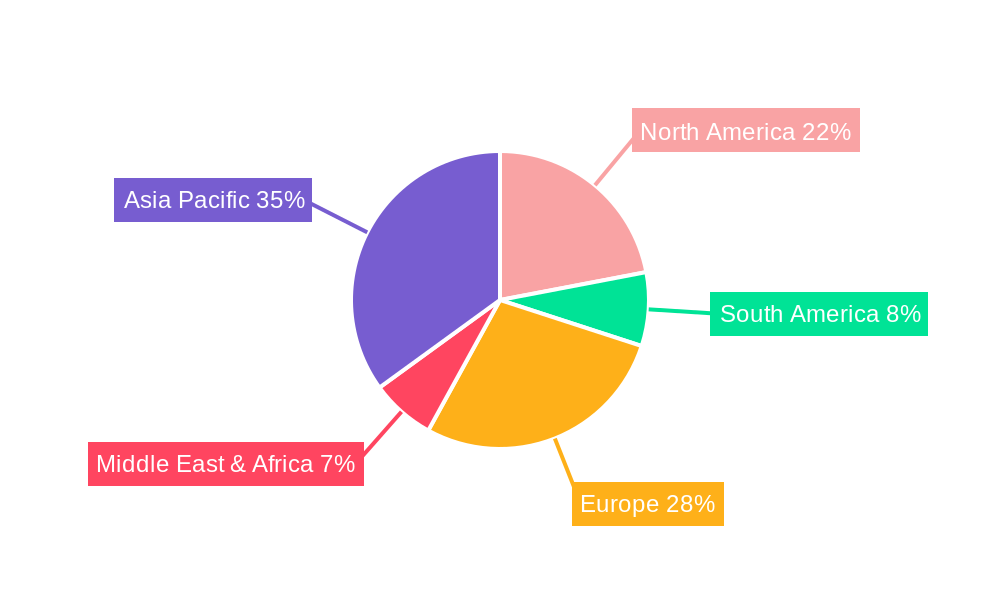

The market is segmented by material type, with Polypropylene (PP) and Polyamide 6 (PA6) holding significant shares, reflecting their widespread adoption in automotive applications due to their excellent mechanical properties and processability. The "Others" category likely encompasses advanced composites and specialized polymers catering to niche performance requirements. In terms of application, both the Original Equipment Manufacturer (OEM) and aftermarket segments are expected to witness steady growth, driven by new vehicle production and the replacement needs of the existing automotive fleet. Geographically, the Asia Pacific region, particularly China and India, is emerging as a dominant force due to its massive automotive production base and growing domestic consumption. North America and Europe remain crucial markets, driven by technological advancements and the presence of major automotive players. However, challenges such as the volatility of raw material prices and the need for robust recycling infrastructure for end-of-life components may present some restraints to the otherwise promising market outlook.

This comprehensive report delves into the dynamic world of plastic intake manifolds, offering a granular analysis of its market trajectory from 2019 to 2033. With 2025 as the base and estimated year, and a detailed forecast from 2025-2033, this study leverages data from the historical period of 2019-2024 to provide actionable insights. The global plastic intake manifold market is projected to witness substantial growth, driven by evolving automotive manufacturing trends and technological advancements. Our analysis encompasses a detailed examination of production volumes, with a focus on the World Plastic Intake Manifold Production, estimated to reach millions of units. We meticulously dissect the market by material type, including PA6, PP, and Others, and by application, differentiating between OEM and Aftermarket segments. Industry-specific developments and emerging trends are also thoroughly investigated.

The global plastic intake manifold market is poised for significant expansion, driven by a confluence of factors that are reshaping the automotive landscape. XXX, the dominant trend observed throughout the study period (2019-2033), is the relentless pursuit of enhanced fuel efficiency and reduced emissions in internal combustion engine vehicles. Plastic intake manifolds, by virtue of their lightweight nature compared to their metal counterparts, contribute directly to this goal by reducing overall vehicle weight. This weight reduction translates into improved fuel economy and a lower carbon footprint, aligning perfectly with increasingly stringent environmental regulations worldwide. The shift towards advanced composite materials, particularly within the PA6 and PP segments, is another pivotal trend. These materials offer superior thermal resistance, chemical stability, and vibration damping capabilities, making them ideal for the demanding environment within an engine bay. Furthermore, the increasing complexity of engine designs, with a focus on optimized airflow and integrated sensor functionalities, necessitates the use of sophisticated plastic molding techniques. This has led to a rise in custom-engineered plastic intake manifolds that can accommodate a wider array of components and intricate designs, thereby enhancing engine performance and drivability. The aftermarket segment is also experiencing robust growth, fueled by the increasing vehicle parc and the demand for cost-effective and durable replacement parts. As vehicles age, worn-out metal intake manifolds are increasingly being replaced by their lighter and more resilient plastic alternatives, offering a long-term solution. The integration of advanced manufacturing technologies, such as additive manufacturing, is also beginning to influence the production of specialized or low-volume plastic intake manifolds, enabling greater design freedom and rapid prototyping. The consistent upward trajectory of World Plastic Intake Manifold Production, projected to reach tens of millions of units by the end of the forecast period, underscores the growing importance and widespread adoption of these components across the global automotive industry. This growth is not merely incremental; it represents a fundamental shift in material preference and manufacturing philosophy within the engine intake system.

The ascendant growth of the plastic intake manifold market is underpinned by a potent blend of technological advancements, regulatory pressures, and economic considerations. Primarily, the unwavering global push for improved fuel economy and reduced vehicular emissions acts as a monumental driving force. As governments worldwide implement stricter environmental standards, automotive manufacturers are compelled to seek innovative solutions for weight reduction. Plastic intake manifolds, significantly lighter than their cast iron or aluminum predecessors, directly contribute to this objective, leading to a tangible improvement in fuel efficiency and a decrease in CO2 emissions. This aligns with the broader industry objective of achieving fleet-wide emission targets. Secondly, advancements in polymer science and manufacturing processes have significantly enhanced the performance and durability of plastic intake manifolds. Modern materials like Polyamide 6 (PA6) and Polypropylene (PP) offer superior resistance to high temperatures, chemicals, and vibrations commonly encountered within an engine compartment. This enhanced material capability allows plastic manifolds to meet and often exceed the performance requirements of traditional metal components, offering a compelling alternative. Thirdly, the cost-effectiveness of plastic intake manifolds, both in terms of raw material and manufacturing, presents a substantial advantage. Injection molding processes for plastics are generally more efficient and less energy-intensive than those for metals, leading to lower production costs. This cost advantage is particularly attractive for mass-produced vehicles, contributing to the overall affordability of automobiles.

Despite the robust growth trajectory, the plastic intake manifold market is not without its impediments. A primary challenge revolves around the perception of durability and longevity associated with plastic components compared to traditional metal alternatives. While modern plastics have made significant strides in performance, ingrained consumer and some industry-level skepticism regarding their long-term reliability under extreme engine conditions remains a hurdle. This necessitates continuous innovation and rigorous testing to build further confidence. Another significant restraint is the inherent temperature limitation of certain plastic materials. While advancements have been made, the extremely high temperatures experienced in certain engine configurations or under severe operating conditions can still pose a challenge, potentially leading to material degradation or deformation. This often requires the use of specialized, higher-cost polymers or supplementary heat shielding, impacting overall cost-effectiveness. The increasing complexity of engine designs, while driving innovation, also presents challenges in terms of intricate mold design and manufacturing for plastic intake manifolds. Achieving precise tolerances and ensuring structural integrity in highly complex geometries can be technically demanding and costly. Furthermore, the fluctuating prices of petrochemical feedstocks, which are the primary source for many plastic materials, can introduce volatility into raw material costs. This price instability can impact the profitability of manufacturers and create uncertainty in long-term cost projections. Finally, the potential for cracking or damage due to road debris or impacts, particularly in certain vehicle applications, represents another area of concern that requires careful material selection and design considerations.

The World Plastic Intake Manifold Production segment, particularly within the OEM Application, is poised to exhibit significant dominance in the global market. This dominance is intrinsically linked to the sheer volume of new vehicle production worldwide. The automotive Original Equipment Manufacturer (OEM) segment represents the primary consumer of plastic intake manifolds, as these components are integral to the assembly of new vehicles. Regions with high automotive manufacturing output are therefore expected to lead in terms of demand and production of plastic intake manifolds.

Asia-Pacific: This region is projected to be the undisputed leader in the plastic intake manifold market.

Europe: This region is expected to hold a significant market share, driven by stringent emission regulations and a strong emphasis on fuel efficiency.

North America: While mature, this market continues to be a significant contributor, especially with the growing trend towards fuel-efficient vehicles.

Segment Dominance:

The growth of the plastic intake manifold industry is significantly propelled by the escalating demand for lightweight vehicle components to enhance fuel efficiency and reduce emissions. This is further bolstered by increasingly stringent global environmental regulations, compelling automakers to adopt advanced materials. Advancements in polymer technology, leading to improved thermal and chemical resistance of plastics, are expanding their application scope. Moreover, the cost-effectiveness of plastic manufacturing processes compared to traditional metal casting provides a compelling economic incentive for widespread adoption. The expanding global automotive parc, particularly in emerging economies, also contributes to sustained demand for both OEM and aftermarket plastic intake manifolds.

This report offers an unparalleled deep dive into the global plastic intake manifold market, providing a holistic understanding of its present and future landscape. From analyzing intricate market trends and identifying the key driving forces to meticulously detailing the challenges and restraints, the report leaves no stone unturned. It further pinpoints the dominant regions and segments, offering strategic insights into where growth opportunities are most pronounced. The report also highlights critical growth catalysts and identifies the leading players shaping the industry. With a comprehensive historical analysis from 2019-2024, and a forward-looking perspective up to 2033, this study equips stakeholders with the essential data and expert analysis needed to navigate this evolving market effectively. The detailed examination of World Plastic Intake Manifold Production volumes and the nuanced breakdown by material type (PA6, PP, Others) and application (OEM, Aftermarket) ensures a robust understanding of market dynamics.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Mikuni Corporation, TOKYO ROKI, Aisin, DSM, DaikyoNishikawa Corporation, Jiangxi Xin Tian car industry Co., Ltd., .

The market segments include Type, Application.

The market size is estimated to be USD 2091.9 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Plastic Intake Manifold," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Plastic Intake Manifold, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.