1. What is the projected Compound Annual Growth Rate (CAGR) of the Peptic Ulcer Drugs?

The projected CAGR is approximately 5.1%.

Peptic Ulcer Drugs

Peptic Ulcer DrugsPeptic Ulcer Drugs by Type (Proton Pump Inhibitors, H2-Antagonists, Antacids, Others), by Application (Hospital and Clinic, Drugstore), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

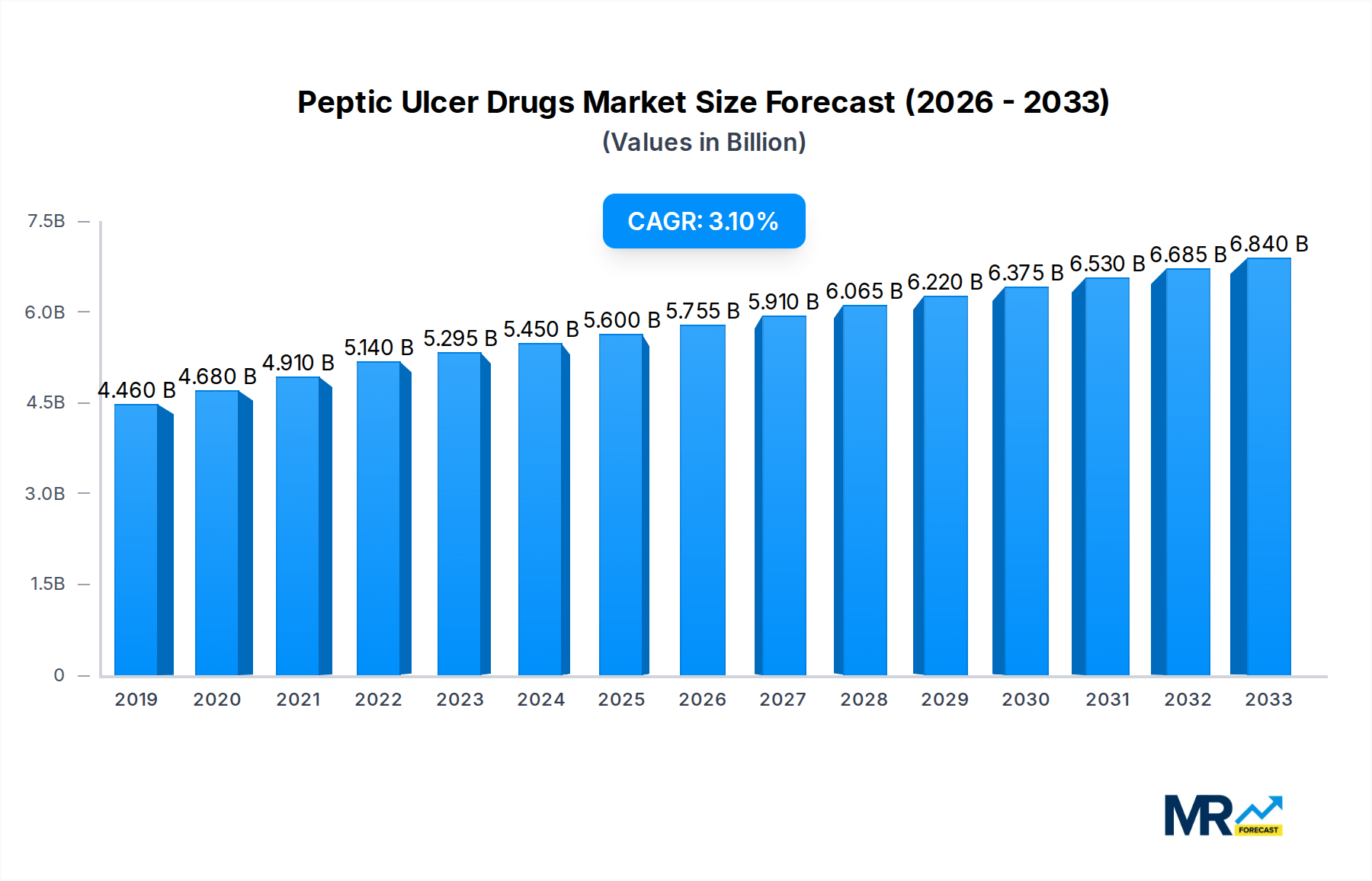

The global peptic ulcer drugs market is poised for robust expansion, projected to reach an estimated USD 5.33 billion by the base year 2025, with a commendable Compound Annual Growth Rate (CAGR) of 5.1%. This sustained growth, anticipated to continue through the forecast period extending to 2033, is primarily fueled by the increasing prevalence of peptic ulcer diseases globally. Factors contributing to this rise include evolving lifestyle patterns, dietary habits, higher stress levels, and the widespread use of non-steroidal anti-inflammatory drugs (NSAIDs), a significant trigger for ulcer development. The market's dynamism is further supported by continuous advancements in pharmaceutical research and development, leading to the introduction of more effective and targeted therapies. Key market drivers include a growing awareness among patients and healthcare professionals about peptic ulcer conditions and their management, alongside favorable reimbursement policies in several key regions.

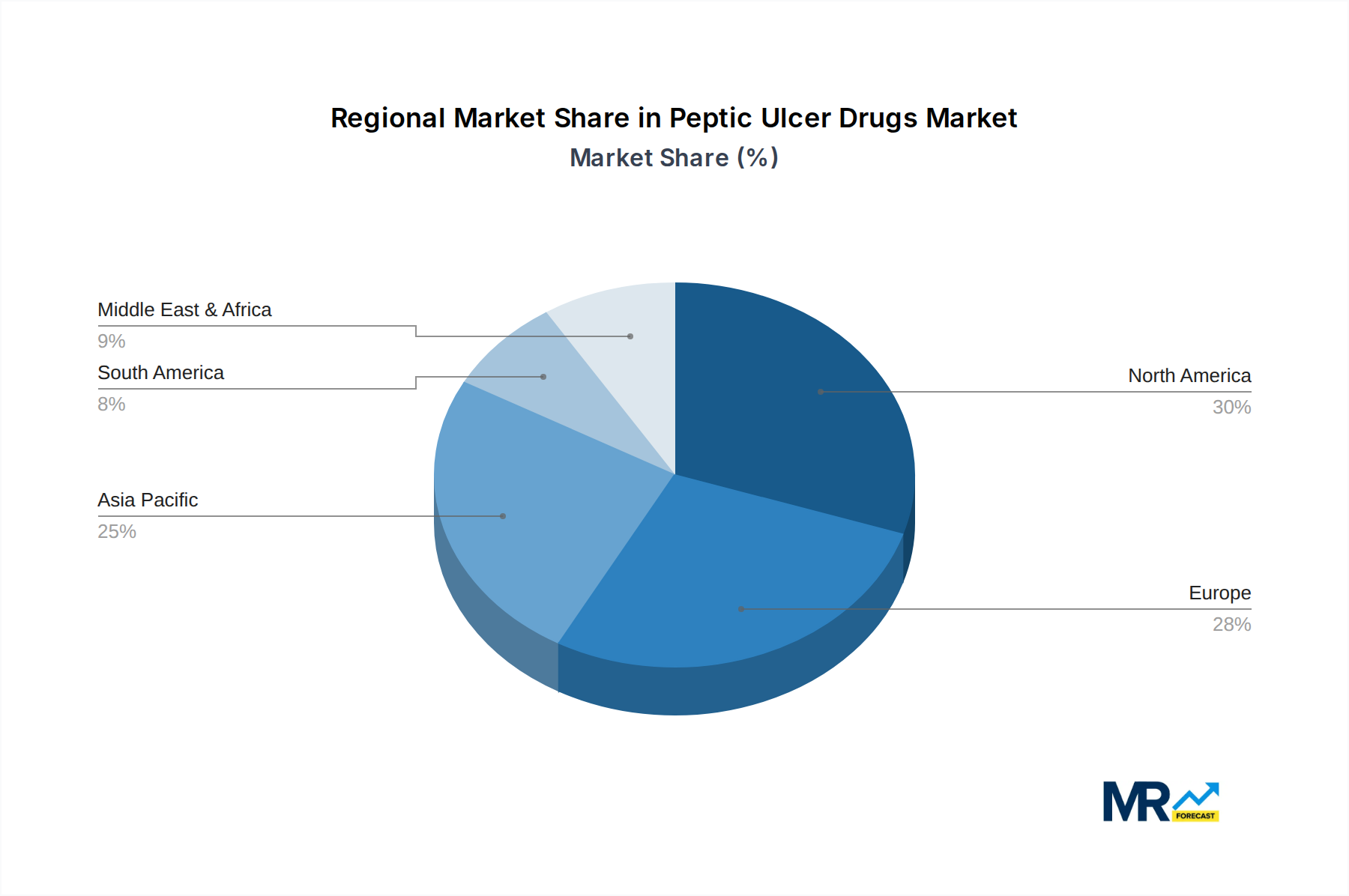

The market segmentation reveals a diverse landscape with Proton Pump Inhibitors (PPIs) likely dominating the Type segment due to their high efficacy in reducing gastric acid secretion, followed by H2-Antagonists. Antacids will also hold a significant share, offering immediate relief. In terms of Application, the Hospital and Clinic segment is expected to lead, driven by the need for professional diagnosis and treatment of severe ulcer cases, while the Drugstore segment will cater to over-the-counter remedies and patient self-management. Geographically, the Asia Pacific region, particularly China and India, is anticipated to witness substantial growth, owing to a large patient pool, increasing healthcare expenditure, and rising accessibility to advanced treatments. North America and Europe are expected to remain mature yet significant markets, characterized by high adoption of innovative therapies and strong healthcare infrastructures.

This comprehensive report delves into the intricate dynamics of the global Peptic Ulcer Drugs market, offering an in-depth analysis of its historical trajectory, current landscape, and future potential. Spanning the Study Period: 2019-2033, with a keen focus on the Base Year: 2025 and Estimated Year: 2025, the report meticulously examines market performance across the Historical Period: 2019-2024 and projects insights through the Forecast Period: 2025-2033. The research provides a holistic view, encompassing key market segments and influential industry players, to equip stakeholders with actionable intelligence for strategic decision-making.

The global Peptic Ulcer Drugs market is poised for robust growth, projected to reach a valuation of approximately $XX billion by 2025. This expansion is underpinned by an increasing prevalence of peptic ulcer diseases, driven by factors such as aging populations, the widespread use of NSAIDs, and the persistent threat of Helicobacter pylori infections. The market is characterized by a dynamic interplay of established therapeutic classes and the emergence of novel treatment approaches. Proton Pump Inhibitors (PPIs) continue to dominate, accounting for a substantial share of the market due to their efficacy in reducing gastric acid secretion. However, concerns regarding long-term PPI use, including potential links to nutrient deficiencies and increased risk of certain infections, are prompting a renewed interest in alternative and adjunctive therapies. H2-Antagonists, while less potent than PPIs, maintain a significant presence, particularly in milder cases and as a cost-effective option. The market is also witnessing a gradual evolution in the "Others" category, which encompasses a range of treatments including antacids, mucosal protectants, and emerging biologics, reflecting a push towards more personalized and targeted therapeutic strategies.

The evolving treatment landscape is also influenced by advancements in diagnostics, leading to earlier and more accurate identification of peptic ulcer causes. This, in turn, facilitates more timely and effective intervention. Furthermore, the increasing emphasis on lifestyle modifications and preventive measures, alongside pharmacological interventions, is shaping the overall approach to managing peptic ulcer disease. The market is characterized by a strong geographical distribution, with Asia Pacific emerging as a significant contributor due to its large population, rising healthcare expenditure, and the growing burden of gastrointestinal disorders. North America and Europe, with their well-established healthcare infrastructures and advanced research capabilities, also represent key markets. The competitive landscape is marked by the presence of both global pharmaceutical giants and regional players, fostering innovation and a drive towards more effective and safer treatment options.

The market is witnessing a trend towards combination therapies, leveraging the strengths of different drug classes to achieve synergistic effects and better patient outcomes. For instance, the combination of PPIs with antibiotics for H. pylori eradication remains a cornerstone of treatment. Additionally, the development of novel formulations, such as extended-release PPIs, aims to improve patient compliance and provide sustained symptom relief. The increasing focus on eradicating the root cause of ulcers, particularly H. pylori infections, is driving research into more effective and less resistant antibiotic regimens. The future of the peptic ulcer drugs market will likely be shaped by the development of therapies that offer enhanced efficacy, improved safety profiles, and address the growing challenge of antibiotic resistance.

The global Peptic Ulcer Drugs market is propelled by a confluence of powerful drivers that ensure its sustained growth and evolution. Foremost among these is the persistent and, in some demographics, increasing prevalence of peptic ulcer diseases. This surge is directly linked to an aging global population, where individuals are more susceptible to gastrointestinal issues. Furthermore, the widespread and often indiscriminate use of Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) for pain management across various age groups significantly contributes to the erosion of the protective mucosal lining of the stomach and duodenum, thus escalating ulcer formation. The enduring challenge posed by Helicobacter pylori (H. pylori) infections, a primary etiological agent for a substantial proportion of peptic ulcers, continues to necessitate effective pharmaceutical interventions for its eradication. This persistent microbial threat acts as a constant demand generator for antibacterial and acid-suppressing therapies.

Moreover, advancements in medical diagnostics have improved the early detection and accurate identification of peptic ulcer causes. This heightened diagnostic capability enables healthcare professionals to initiate timely and appropriate treatment regimens, thereby preventing complications and improving patient outcomes. The growing awareness among both healthcare providers and the general public regarding the symptoms and consequences of peptic ulcers also plays a crucial role in driving demand for effective drug treatments. As awareness rises, more individuals seek medical attention, leading to increased prescriptions and over-the-counter sales of relevant medications. This multifaceted combination of disease prevalence, treatment necessity, and improved awareness forms the bedrock of the peptic ulcer drugs market's upward trajectory.

Despite the promising growth prospects, the Peptic Ulcer Drugs market is not without its significant challenges and restraints. One of the most pressing concerns is the growing issue of antibiotic resistance, particularly concerning Helicobacter pylori. The overuse and misuse of antibiotics have led to the emergence of H. pylori strains that are increasingly resistant to standard eradication therapies, necessitating the development of novel antibiotic combinations and treatment protocols, which can be more complex and costly. Another significant challenge pertains to the long-term safety concerns associated with the prolonged use of Proton Pump Inhibitors (PPIs). Emerging research has linked chronic PPI use to potential side effects, including an increased risk of bone fractures, kidney disease, Clostridium difficile infections, and nutrient deficiencies (such as vitamin B12 and magnesium). These concerns are leading to greater scrutiny from regulatory bodies and a push towards more judicious prescribing practices.

Furthermore, the development of generic versions of blockbuster peptic ulcer drugs leads to price erosion, impacting the revenue streams of originator companies and potentially hindering investment in new research and development. While beneficial for patients in terms of cost, it presents a revenue challenge for pharmaceutical manufacturers. The market also faces stringent regulatory hurdles for drug approval, with extensive clinical trials required to demonstrate efficacy and safety. This lengthy and expensive process can delay the introduction of new therapies and increase the overall cost of bringing a drug to market. Finally, the increasing emphasis on lifestyle modifications and alternative therapies by some patient segments, although generally complementary, can also represent a restraint on the overall demand for conventional pharmaceutical interventions.

The Peptic Ulcer Drugs market is characterized by a dynamic regional and segmental dominance, with specific areas exhibiting significant growth and consumption.

Key Dominating Segments:

Dominating Regions:

In summary, Proton Pump Inhibitors, primarily prescribed in Hospital and Clinic settings, represent the leading therapeutic and application segments. Geographically, the Asia Pacific region is set to dominate in terms of growth, while North America remains a strong, established market. This interplay of dominant segments and regions underscores the current and future landscape of the global Peptic Ulcer Drugs market.

Several factors are acting as potent growth catalysts for the Peptic Ulcer Drugs industry. The continuous rise in the global prevalence of peptic ulcer diseases, exacerbated by aging populations and the ubiquitous use of NSAIDs, creates a sustained demand for effective treatments. Furthermore, the persistent threat of Helicobacter pylori infections necessitates ongoing development and utilization of eradication therapies. Advancements in diagnostic technologies are enabling earlier and more accurate identification of ulcer causes, leading to prompt treatment initiation. As healthcare expenditure rises globally and awareness about gastrointestinal health increases, more individuals are seeking and affording appropriate medical interventions, thereby fueling market expansion.

This report offers a granular and expansive view of the Peptic Ulcer Drugs market, going beyond surface-level analysis to provide actionable insights. It meticulously dissects the market by therapeutic type, including the dominant Proton Pump Inhibitors, established H2-Antagonists, accessible Antacids, and the burgeoning "Others" category. The report also thoroughly examines application segments, highlighting the critical roles of Hospitals and Clinics, as well as Drugstores, in market dynamics. Leveraging a robust methodology, the research analyzes the historical performance from 2019-2024, provides an in-depth assessment for the Base Year: 2025 and Estimated Year: 2025, and projects future trends throughout the Forecast Period: 2025-2033 under the overarching Study Period: 2019-2033. This comprehensive coverage equips stakeholders with a deep understanding of market drivers, challenges, regional dominance, and the strategic positioning of key players.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.1%.

Key companies in the market include AstraZeneca, Livzon Pharmaceutical, Jiangsu Aosaikang Pharmaceutical, CTTQ, Luoxin Pharmaceuticals, Takeda, Eisai, Jumpcan Pharmaceutical, Zhejiang Conba Pharmaceutical, Youcare Pharmaceutical, Chongqing Lummy Pharmaceutical, Huadong Medicine, Hansoh Pharmaceutical, CR Double-Crane, Hunan Warrant Pharmaceutical, Changzhou Siyao Pharmaceuticals, Chongqing Pharscin Pharmaceutical, Lionco Pharmaceutical, Jiangsu Wuzhong Pharmaceutical, Cisen Pharmaceutical.

The market segments include Type, Application.

The market size is estimated to be USD 5.33 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Peptic Ulcer Drugs," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Peptic Ulcer Drugs, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.