1. What is the projected Compound Annual Growth Rate (CAGR) of the Packaging Gap Fillers?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Packaging Gap Fillers

Packaging Gap FillersPackaging Gap Fillers by Type (Expanded Polystyrene, Bubble Wrap, Others), by Application (Electronics, Consumer Goods, Cosmetic and Personal Care, Foods and Beverages, Pharmaceuticals, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

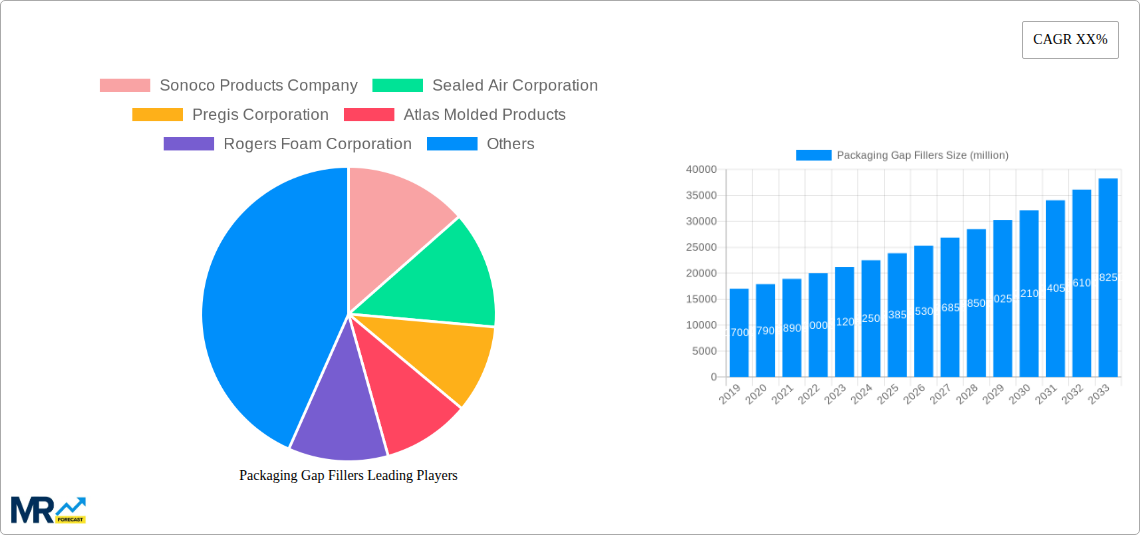

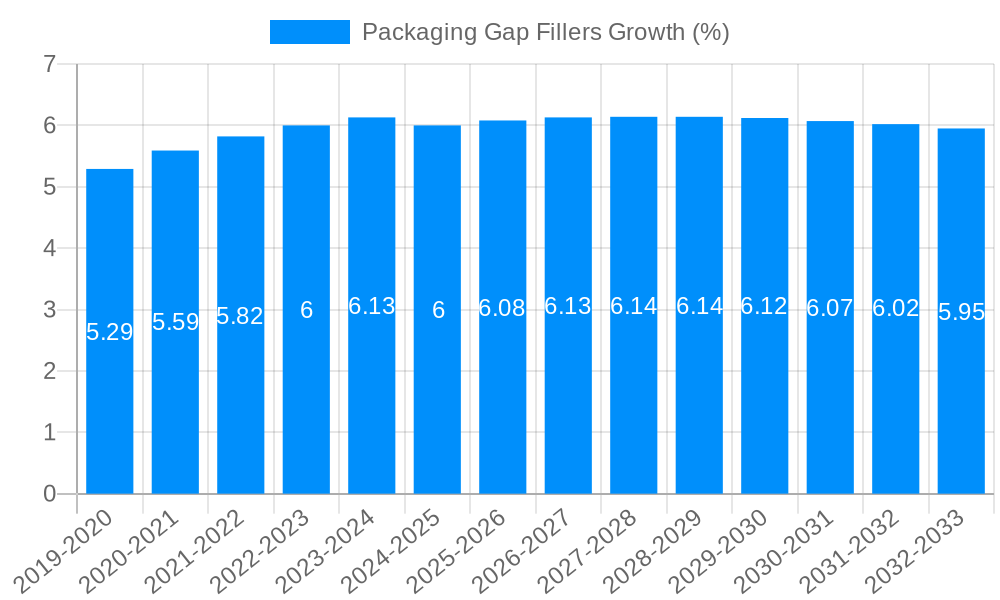

The global Packaging Gap Fillers market is experiencing robust growth, projected to reach an estimated USD 25,000 million by 2025, with a Compound Annual Growth Rate (CAGR) of 6.5% through 2033. This expansion is primarily fueled by the escalating e-commerce sector, which demands efficient and protective packaging solutions for a diverse range of products. The convenience and speed associated with online shopping have led to a significant increase in shipped goods, thereby boosting the need for gap-filling materials to prevent damage during transit. Furthermore, a growing consumer awareness regarding product integrity and the desire for a positive unboxing experience are compelling manufacturers to invest in superior cushioning and void-filling technologies. The market is also influenced by the increasing demand from the food and beverage and pharmaceutical industries, where product safety and shelf-life are paramount, necessitating specialized and often eco-friendly gap-filling solutions.

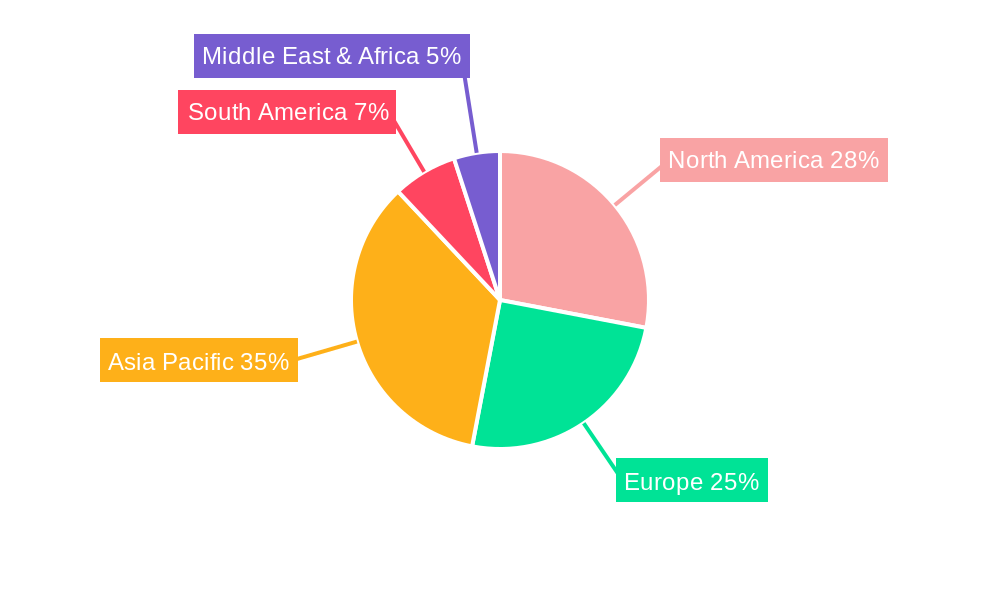

The market is characterized by a dynamic interplay of established players and emerging innovators, with companies like Sonoco Products Company, Sealed Air Corporation, and Smurfit Kappa Group holding significant market share. The segment of Expanded Polystyrene (EPS) continues to dominate due to its cost-effectiveness and protective properties, especially in electronics and consumer goods packaging. However, there is a discernible trend towards more sustainable alternatives, with Bubble Wrap and other innovative materials gaining traction. Restraints such as the rising cost of raw materials and the environmental concerns associated with certain traditional gap fillers present challenges, prompting a push towards biodegradable and recyclable options. Regional dominance is currently observed in the Asia Pacific due to its vast manufacturing base and burgeoning e-commerce landscape, followed closely by North America and Europe, both of which are actively adopting advanced packaging technologies and sustainable practices.

Here's a unique report description for "Packaging Gap Fillers" incorporating your specific requirements.

The global Packaging Gap Fillers market is poised for significant expansion, driven by evolving e-commerce logistics and a heightened demand for product protection across diverse industries. During the Study Period (2019-2033), the market witnessed a steady ascent, with the Base Year (2025) serving as a crucial pivot for projecting future growth trajectories. The estimated market size in 2025, projected to reach several hundred million units, underscores the increasing reliance on specialized void fill solutions. The historical period (2019-2024) laid the groundwork, characterized by a burgeoning e-commerce landscape and a growing awareness of the financial and environmental costs associated with damaged goods. As we move into the Forecast Period (2025-2033), the market is expected to accelerate, fueled by technological innovations, a wider adoption of sustainable materials, and the continuous diversification of product shipments. The inherent need to safeguard products during transit, from delicate electronics to everyday consumer goods, ensures a persistent demand for effective and efficient gap-filling solutions. This trend is further amplified by the increasing complexity of supply chains and the growing emphasis on customer satisfaction, where product condition upon arrival plays a pivotal role. The market's trajectory is also influenced by global economic conditions, regulatory shifts pertaining to packaging materials, and the ongoing pursuit of cost-optimization by manufacturers and logistics providers.

The Packaging Gap Fillers market is experiencing a robust upward trend, primarily propelled by the relentless expansion of e-commerce. As online shopping continues its meteoric rise, the volume of goods being shipped globally has surged, creating an unprecedented demand for effective protective packaging solutions. This surge necessitates the use of gap fillers to prevent items from shifting, rattling, or colliding during transit, thereby minimizing damage and reducing costly returns and replacements. Beyond e-commerce, the growth of diverse industries such as electronics, which requires specialized cushioning for sensitive components, and the pharmaceutical sector, where product integrity is paramount, further contributes to market acceleration. Furthermore, increasing consumer expectations for undamaged product delivery are pushing businesses to invest more in superior void fill materials. This focus on customer experience, coupled with a growing awareness of the economic advantages of preventing damage, acts as a significant impetus for market growth. The continuous innovation in material science, leading to more sustainable and cost-effective gap-filling options, also plays a crucial role in driving adoption.

Despite the optimistic growth outlook, the Packaging Gap Fillers market faces certain inherent challenges and restraints that could temper its expansion. One of the primary concerns revolves around the environmental impact of traditional packaging materials, particularly Expanded Polystyrene (EPS). Growing regulatory scrutiny and consumer preference for eco-friendly alternatives are pushing manufacturers to develop and adopt sustainable options, which can sometimes come with higher production costs. The disposal and recycling infrastructure for certain gap-filling materials also remain a point of contention, posing challenges for waste management. Additionally, the fluctuating raw material prices for plastics and other components used in gap fillers can impact profitability and create pricing volatility, making it difficult for businesses to maintain consistent margins. Intense market competition, with numerous players vying for market share, can also lead to price wars, squeezing profit margins and potentially hindering investment in research and development. Lastly, the logistics of distributing bulky or lightweight gap-filling materials can present operational complexities and add to overall shipping costs, which might be passed on to the end consumer or absorbed by businesses, impacting their bottom line.

The Electronics segment, within the Packaging Gap Fillers market, is projected to be a dominant force, propelled by the ever-increasing global demand for electronic devices and the inherent fragility of these high-value products. This dominance is further amplified by the strong presence of major electronics manufacturing hubs and significant e-commerce penetration in regions like North America and Asia Pacific.

Dominant Segment: Electronics

Dominant Region/Country: North America and Asia Pacific

North America: This region boasts a highly developed e-commerce infrastructure and a robust consumer market for electronics and a wide array of consumer goods. The presence of leading packaging manufacturers such as Sonoco Products Company, Sealed Air Corporation, and Pregis Corporation, with their extensive product portfolios and R&D capabilities, further strengthens the market. The increasing adoption of advanced packaging technologies and a strong emphasis on supply chain efficiency contribute to North America's leading position. The strict quality control standards prevalent in the region also mandate the use of reliable gap fillers to ensure product integrity.

Asia Pacific: This region is experiencing unprecedented growth in e-commerce, driven by a burgeoning middle class and increasing internet penetration. It is also a global manufacturing powerhouse for electronics, leading to substantial domestic and export-oriented shipments of these goods. Countries like China, Japan, and South Korea are key players in both consumption and production. The presence of both global players and rapidly growing local manufacturers like Haijing and Smurfit Kappa Group (with its regional operations) is fueling demand. The increasing focus on sustainable packaging solutions within this region, alongside the persistent need for cost-effective protection, is shaping the market dynamics. The vast scale of operations and the sheer volume of goods being shipped make Asia Pacific a critical and dominant market for packaging gap fillers.

The Packaging Gap Fillers industry is experiencing growth catalyzed by several key factors. The relentless expansion of the e-commerce sector continues to be a primary driver, as more businesses rely on efficient and protective shipping solutions to meet consumer demands. The increasing value and fragility of goods, particularly in the electronics and pharmaceutical sectors, necessitate advanced void fill materials to prevent damage during transit. Furthermore, a growing global emphasis on sustainability is fostering innovation in eco-friendly gap fillers, opening new market opportunities for biodegradable and recyclable materials.

This comprehensive report provides an in-depth analysis of the Packaging Gap Fillers market, spanning the Study Period of 2019-2033. It delves into the intricate dynamics of market trends, drivers, challenges, and opportunities, utilizing the Base Year (2025) as a crucial reference point for projections. The report meticulously examines key segments such as Expanded Polystyrene, Bubble Wrap, and Others, alongside critical applications including Electronics, Consumer Goods, Cosmetic and Personal Care, Foods and Beverages, Pharmaceuticals, and Others. It offers detailed regional analysis, identifying dominant markets and their contributing factors, while also highlighting significant industry developments and the key players shaping the landscape. The report's objective is to equip stakeholders with the knowledge to navigate this evolving market, understand its growth catalysts, and capitalize on future opportunities, projecting a robust expansion fueled by e-commerce and specialized protection needs.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Sonoco Products Company, Sealed Air Corporation, Pregis Corporation, Atlas Molded Products, Rogers Foam Corporation, Plymouth Foam, Foam Fabricators, Tucson Container Corporation, Plastifoam Company, Wisconsin Foam Products, Polyfoam Corporation, Woodbridge, Recticel, Teamway, Haijing, Smurfit Kappa Group, Storopack Hans Reichenecker GmbH, FROMM Packaging Systems Inc., Automated Packaging Systems, Inc., Polyair Inter Pack.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Packaging Gap Fillers," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Packaging Gap Fillers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.