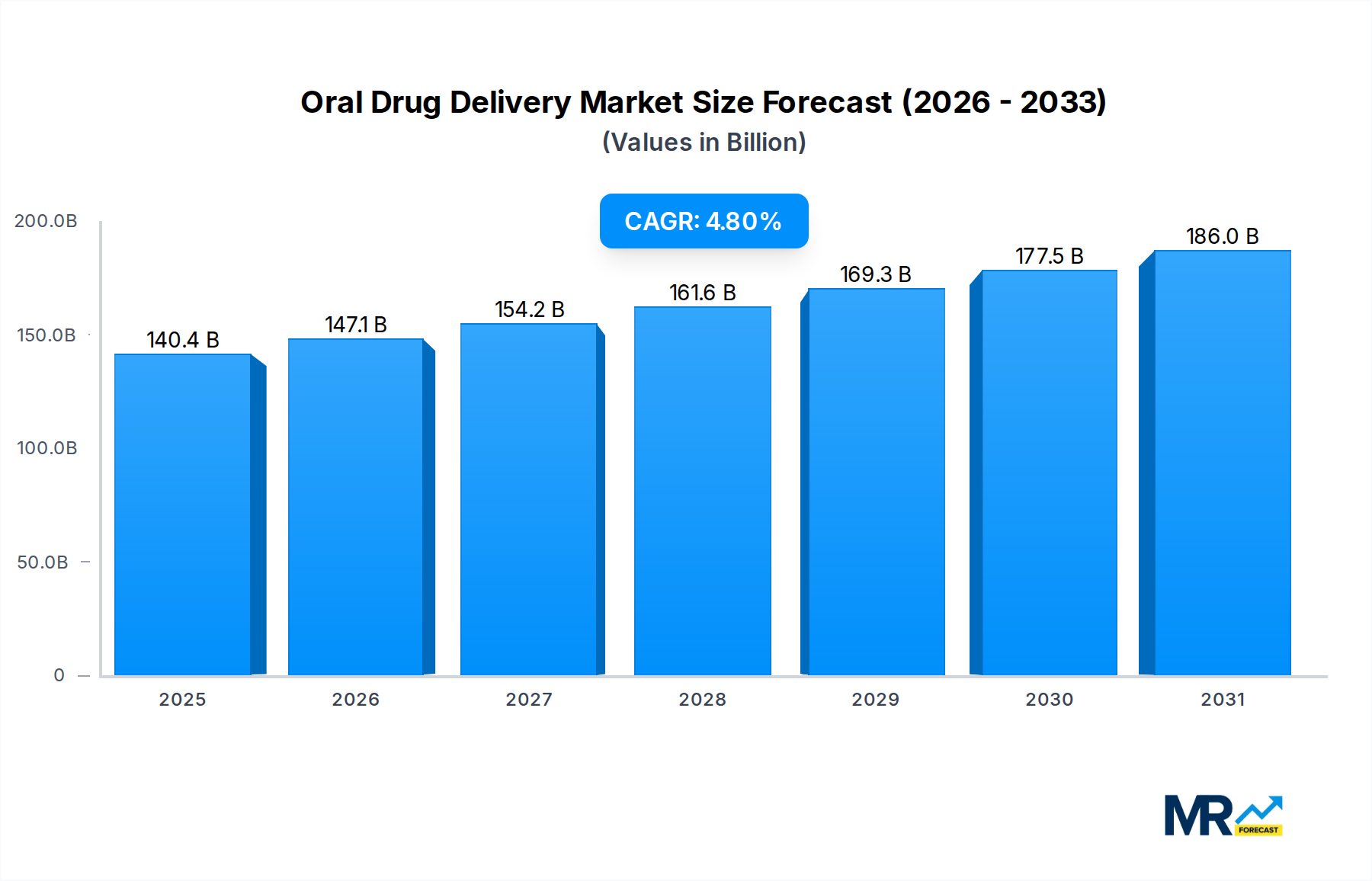

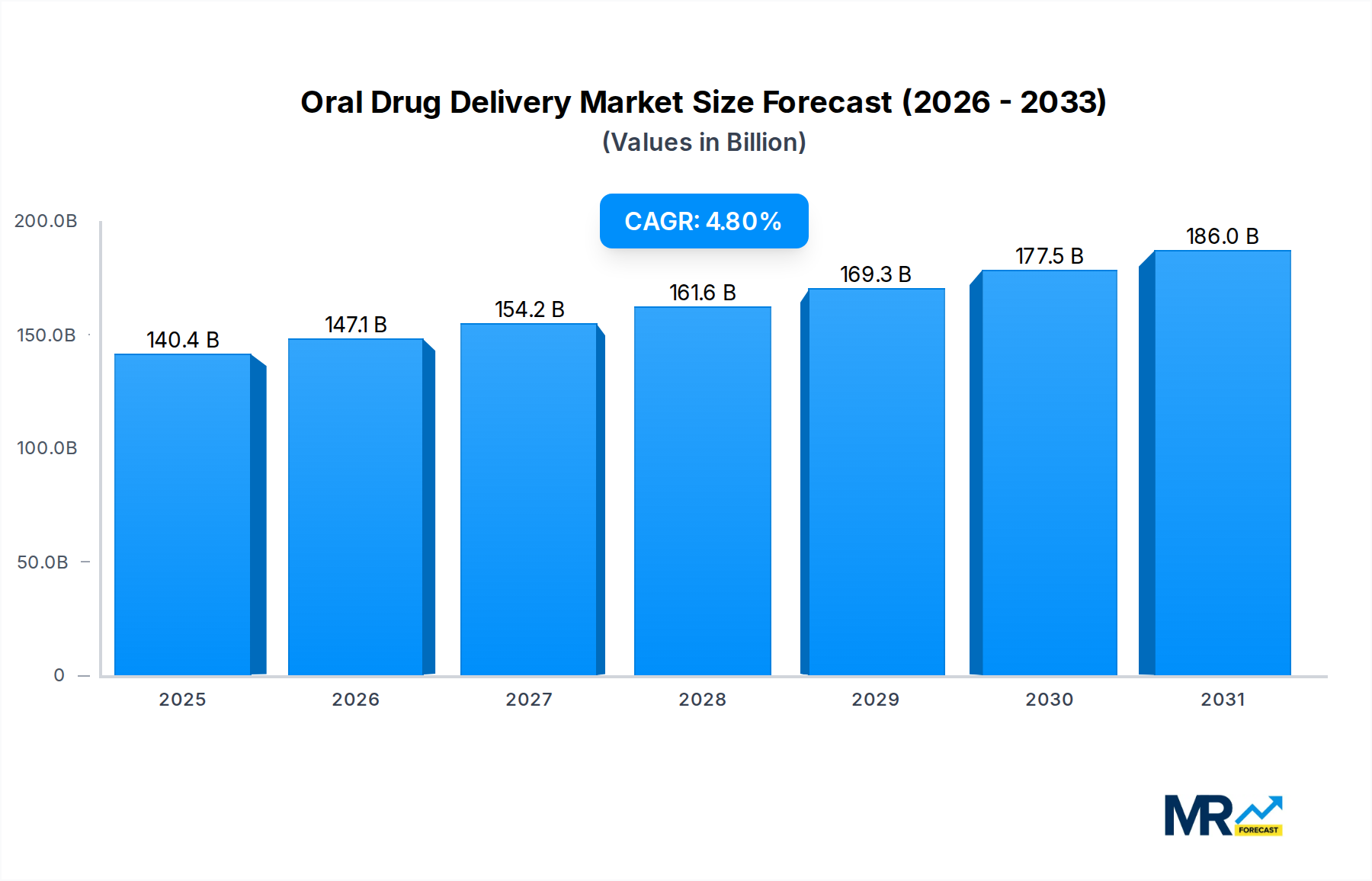

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oral Drug Delivery?

The projected CAGR is approximately 4.8%.

Oral Drug Delivery

Oral Drug DeliveryOral Drug Delivery by Dosage Form (Tablets, Capsules, Powders, Syrups, Gels), by Release Mechanism (Immediate Release, Controlled/Sustained Release, Delayed Release, Targeted Release), by Therapeutic Indication (Cardiovascular Diseases, Oncology, Infectious Diseases, Diabetes, Gastrointestinal Disorders, Central Nervous System (CNS), Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), by End User (Hospitals, Specialty Clinics, Ambulatory Care Centers, Homecare, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Oral Drug Delivery Market is poised for substantial expansion, driven by persistent demand for patient-centric, non-invasive drug administration methods. Valued at an estimated $133.94 billion in 2025, the market is projected to reach approximately $194.88 billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 4.8% over the forecast period. This growth trajectory is underpinned by several critical demand drivers, including the escalating global burden of chronic diseases such as cardiovascular conditions, diabetes, and oncology, where long-term oral medication adherence is crucial. The inherent convenience and cost-effectiveness of oral formulations, coupled with continuous advancements in drug delivery technologies aimed at enhancing bioavailability and precise drug targeting, are significant accelerators. Innovations in solubility enhancement, such as amorphous solid dispersions and nanosuspensions, are extending the oral route's applicability to a broader spectrum of active pharmaceutical ingredients (APIs).

Macroeconomic tailwinds further buoy the Oral Drug Delivery Market. Increased healthcare expenditure worldwide, particularly in emerging economies, is improving access to pharmaceuticals. Demographic shifts, notably a growing aging population, necessitate easier-to-administer drug forms. Furthermore, intensified R&D efforts within the broader Drug Delivery Systems Market are yielding novel excipients and formulation strategies that overcome traditional challenges like poor solubility and first-pass metabolism. The robust pipeline of generic and biosimilar drugs also favors oral delivery due to established manufacturing processes and reduced development costs. As pharmaceutical companies increasingly focus on improving patient compliance and reducing overall healthcare costs, the strategic importance of oral dosage forms continues to grow. The shift towards homecare and self-administration of medications further solidifies the market's positive outlook, positioning oral drug delivery as a cornerstone of modern pharmacotherapy and a critical enabler for the expanding Biopharmaceuticals Market.

The Dosage Form segment is a foundational pillar of the Oral Drug Delivery Market, with tablets consistently representing the largest share due to their unparalleled versatility, patient acceptance, and manufacturing efficiency. Tablets dominate the oral drug delivery landscape due to several intrinsic advantages. They offer precise dosing, excellent chemical and physical stability, and are highly adaptable to various release mechanisms, including immediate, controlled, and delayed release. This adaptability allows them to cater to a wide range of therapeutic needs, from acute pain management to chronic disease control. The established manufacturing infrastructure for tablets is extensive, allowing for high-volume, cost-effective production, which is crucial for meeting global pharmaceutical demands. Furthermore, patient compliance is significantly higher with tablets compared to other invasive or complex administration routes, fostering better therapeutic outcomes.

Closely following tablets, the Capsules Market also holds a substantial share, particularly favored for highly potent or unpleasant-tasting drugs, and for formulations requiring rapid dissolution or specific enteric coatings. The flexibility of capsules in encapsulating various fill materials—powders, granules, liquids, or pastes—makes them a preferred choice for complex formulations, including those designed for the Controlled Release Drug Delivery Market. Key players in this segment are not only the large pharmaceutical companies like Pfizer and Novartis, which produce a vast array of proprietary and generic oral medications, but also specialized contract development and manufacturing organizations (CDMOs) such as Catalent and Lonza. These CDMOs provide critical expertise in formulation development and large-scale manufacturing, supporting both established pharmaceutical giants and emerging biotech firms.

Companies like Colorcon and Roquette are pivotal suppliers of excipients, offering specialized coatings, binders, and disintegrants essential for tablet and capsule performance. The continuous innovation in excipient technology, particularly within the Pharmaceutical Excipients Market, is vital for enhancing drug stability, improving bioavailability, and enabling advanced release profiles in tablets and capsules. While the market share of tablets remains robust, there is ongoing innovation within the segment, with orally disintegrating tablets (ODTs), chewable tablets, and multi-layer tablets gaining traction. These innovations aim to further improve patient experience and address specific patient populations, such as pediatric and geriatric patients, ensuring the sustained dominance and evolution of the tablets segment within the broader Oral Drug Delivery Market.

The Oral Drug Delivery Market is influenced by a confluence of drivers and constraints that shape its trajectory. A primary driver is patient preference and compliance. Oral administration is inherently non-invasive, generally pain-free, and convenient, leading to significantly higher patient adherence to medication regimens compared to parenteral routes. This preference translates directly into improved therapeutic outcomes and reduced healthcare burdens, making oral formulations a priority for drug developers.

Another significant driver is the escalating global burden of chronic diseases. Conditions such as cardiovascular diseases, diabetes, and various forms of cancer require long-term medication, where oral drugs are often the most practical and sustainable solution. For instance, the Oncology Therapeutics Market heavily relies on oral agents, with a growing number of targeted therapies available in tablet or capsule form, allowing patients to manage their conditions from home. Similarly, the increasing prevalence of infectious diseases, which fuels the Infectious Disease Therapeutics Market, often benefits from oral antibiotics and antivirals due to their accessibility and ease of use in community settings. The rise in self-medication and home care settings further accentuates the demand for simple oral dosage forms.

Advancements in formulation technologies also act as a powerful driver. Innovations in solubility enhancement techniques (e.g., solid dispersions, lipid-based systems) and the development of sophisticated release mechanisms (e.g., osmotic pumps, multi-particulate systems) are expanding the utility of oral drugs, allowing for the oral delivery of complex molecules that previously required injections. These technological leaps are instrumental in driving the Controlled Release Drug Delivery Market and the Targeted Drug Delivery Market, optimizing drug profiles and reducing dosing frequency.

However, several constraints temper this growth. Bioavailability challenges pose a significant hurdle. Many new chemical entities (NCEs) exhibit poor aqueous solubility and/or permeability, leading to low and variable oral absorption. This necessitates complex and costly formulation strategies. First-pass metabolism in the gastrointestinal tract and liver can significantly reduce the systemic availability of orally administered drugs, limiting their efficacy and requiring higher doses. Furthermore, drug-food interactions and individual physiological variations can unpredictably alter drug absorption and metabolism, complicating dosing regimens. Stringent regulatory requirements for new oral formulations regarding safety, efficacy, and quality add to development timelines and costs, impacting market entry for novel products. These factors collectively necessitate continuous innovation and careful clinical development within the Oral Drug Delivery Market.

The Oral Drug Delivery Market is characterized by a diverse competitive landscape, encompassing pharmaceutical giants, specialized contract development and manufacturing organizations (CDMOs), and excipient providers. Strategic alliances, mergers, and acquisitions are common as companies seek to expand their technological capabilities and market reach.

The Oral Drug Delivery Market is continuously evolving with new advancements in formulation science, material innovation, and strategic collaborations aimed at improving drug efficacy, safety, and patient experience.

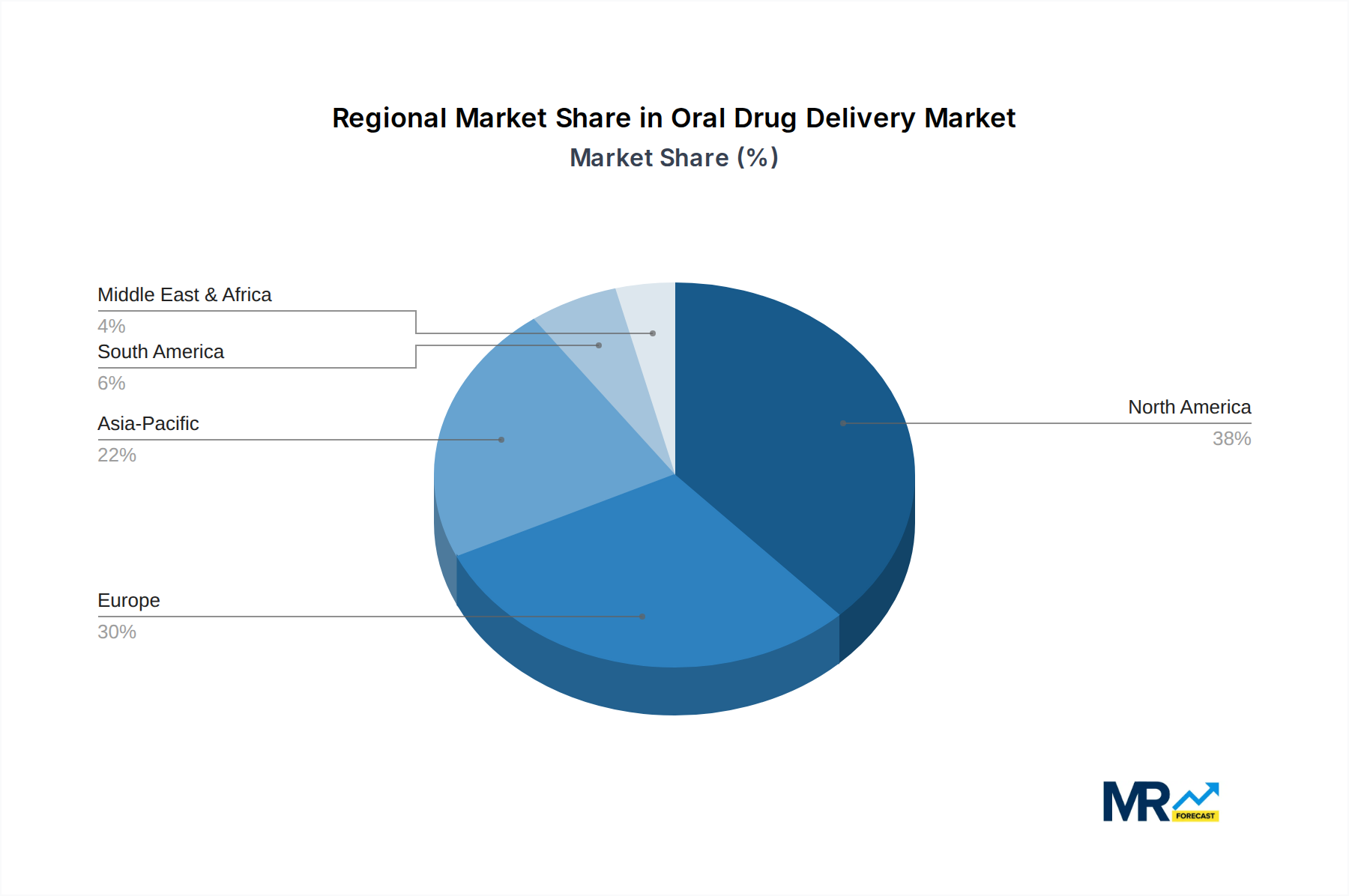

The Oral Drug Delivery Market exhibits distinct dynamics across various global regions, influenced by healthcare infrastructure, disease prevalence, regulatory environments, and economic factors.

North America holds the largest revenue share in the Oral Drug Delivery Market, primarily driven by its advanced healthcare system, high expenditure on pharmaceuticals, robust R&D activities, and a significant prevalence of chronic diseases. The United States, in particular, leads in adopting innovative drug delivery technologies and has a strong presence of major pharmaceutical companies and CDMOs. While a mature market, North America maintains a steady growth rate, largely due to ongoing innovation in formulation sciences and high patient demand for convenient oral therapies. The presence of a sophisticated Drug Delivery Systems Market here also ensures continuous development and adoption of novel oral dosage forms.

Europe represents the second-largest market, characterized by an aging population, universal healthcare coverage in many countries, and strong pharmaceutical manufacturing capabilities, particularly in Germany, France, and the UK. The region sees consistent demand for both innovative and generic oral drugs. Regulatory harmonization through the European Medicines Agency (EMA) facilitates market entry for new oral formulations across member states. Growth is stable, propelled by therapeutic advancements and a strong focus on patient adherence.

Asia Pacific is projected to be the fastest-growing region in the Oral Drug Delivery Market, driven by rapidly expanding healthcare infrastructure, increasing disposable incomes, and a vast patient pool, especially in populous countries like China and India. The rising prevalence of lifestyle diseases, coupled with improving access to modern medicines, fuels demand for oral drug delivery systems. Government initiatives to promote local manufacturing and reduce healthcare costs also contribute to the robust growth of the Tablets Market and Capsules Market within this region. Investments in R&D and manufacturing capabilities are making the region a significant hub for pharmaceutical production.

Latin America and Middle East & Africa are emerging markets demonstrating considerable growth potential. In Latin America, countries like Brazil and Mexico are experiencing increased healthcare investments and a growing middle class, leading to higher pharmaceutical consumption. The demand for affordable oral generics is a key driver. Similarly, in the Middle East & Africa, improvements in healthcare access, urbanization, and a rising burden of non-communicable diseases are stimulating the demand for accessible oral medications. Both regions are witnessing an increase in the adoption of oral drug delivery due to its cost-effectiveness and ease of administration, vital for expanding healthcare access to underserved populations.

The Oral Drug Delivery Market is increasingly subject to sustainability and Environmental, Social, and Governance (ESG) pressures, influencing product development, manufacturing, and supply chain practices. Environmental regulations, such as those targeting carbon emissions and waste reduction, compel pharmaceutical manufacturers to adopt greener production processes. This includes optimizing energy consumption in tablet and capsule production, minimizing solvent use in formulation, and reducing water footprint. There's a growing emphasis on lifecycle assessment for oral drug products, from raw material sourcing (especially for excipients) to end-of-life disposal, promoting circular economy principles. For instance, companies within the Pharmaceutical Excipients Market are exploring bio-based and biodegradable excipients to lessen environmental impact.

Carbon neutrality targets are driving investments in renewable energy sources for manufacturing facilities and optimizing logistics for ingredient and product distribution. Packaging innovations are also crucial; the shift towards recyclable, biodegradable, or minimal packaging materials for oral dosage forms aims to reduce plastic waste and landfill burden. From a social perspective, the accessibility of oral drugs, particularly essential medicines in underserved regions, is a key ESG consideration. Companies are under pressure to ensure equitable access and affordable pricing, aligning with global health initiatives. Ethical sourcing of raw materials and transparency in supply chains are also paramount, addressing concerns related to labor practices and environmental impact.

Governance aspects include robust corporate ethics, anti-corruption policies, and transparent reporting on ESG performance. Investors are increasingly incorporating ESG criteria into their decision-making, favoring companies that demonstrate strong commitment to sustainable practices. This pressure translates into R&D strategies focused on developing more environmentally friendly formulations, reducing reliance on hazardous chemicals, and improving drug stability to extend shelf life and minimize waste. The long-term viability and public perception of companies within the Oral Drug Delivery Market are becoming intrinsically linked to their ability to demonstrate strong ESG credentials, influencing everything from investor relations to consumer trust and regulatory compliance.

The customer base for the Oral Drug Delivery Market is diverse, spanning various end-users with distinct purchasing criteria and procurement channels. The primary end-users, as identified, include Hospitals, Specialty Clinics, Ambulatory Care Centers, and Homecare settings, each exhibiting unique buying behaviors.

Hospitals often procure oral medications in bulk, prioritizing cost-effectiveness, established efficacy, and adherence to formularies. Their buying behavior is driven by clinical guidelines, patient volume, and inventory management considerations. Safety profiles and the ability to integrate with existing patient care protocols are paramount. For specialized oral therapies, particularly in areas like the Oncology Therapeutics Market, hospitals focus on advanced formulations that offer improved patient outcomes and reduced side effects.

Specialty Clinics, focusing on specific therapeutic areas (e.g., cardiology, diabetes, infectious diseases), require oral drugs that are highly effective for their patient demographic. Their purchasing decisions are often influenced by clinical specialists, patient-specific needs, and the latest treatment guidelines. While price is a factor, the emphasis on targeted efficacy and patient convenience, especially for conditions managed with Controlled Release Drug Delivery Market products, can sometimes outweigh cost considerations.

Ambulatory Care Centers prioritize ease of administration, rapid availability, and cost-efficiency for common conditions. They seek reliable and readily available oral medications for immediate patient needs, often favoring widely accepted generic and branded oral drugs that simplify outpatient treatment. This setting is less likely to stock highly specialized or rare oral formulations unless it aligns with a specific chronic care program.

Homecare is a rapidly growing segment, driven by the desire for patients to manage chronic conditions in their own environments. This segment's buying behavior is heavily influenced by patient convenience, ease of self-administration, and formulations that simplify complex dosing regimens. Products within the Tablets Market and Capsules Market that are designed for patient-friendly packaging, clear instructions, and minimal side effects are highly valued. Price sensitivity can be moderate to high, especially for long-term therapies. The rise of homecare also fuels the growth of Online Pharmacies Market as a procurement channel.

Across all segments, key purchasing criteria include drug efficacy, safety profile, patient compliance (often enhanced by user-friendly oral forms), stability, and cost. There's an increasing preference for formulations that improve bioavailability and offer sustained or Targeted Drug Delivery Market capabilities, reducing the frequency of dosing and improving patient adherence. Procurement channels vary from direct contracts with manufacturers for large hospital systems, to wholesale distributors for retail pharmacies, and increasingly, direct-to-consumer models through online platforms. Recent shifts indicate a growing demand for personalized medicine approaches, patient-centric formulations, and a heightened awareness of drug affordability, especially in the context of long-term treatment for chronic diseases like those addressed by the Infectious Disease Therapeutics Market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.8%.

Key companies in the market include Catalent, Lonza, Evonik Industries, Colorcon, Roquette, Pfizer, Novartis, AstraZeneca, Merck & Co., AbbVie, Johnson & Johnson, Boehringer Ingelheim, Teva Pharmaceutical Industries, Abbott Laboratories, Others.

The market segments include Dosage Form, Release Mechanism, Therapeutic Indication, Distribution Channel, End User.

The market size is estimated to be USD 133.94 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Oral Drug Delivery," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Oral Drug Delivery, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.