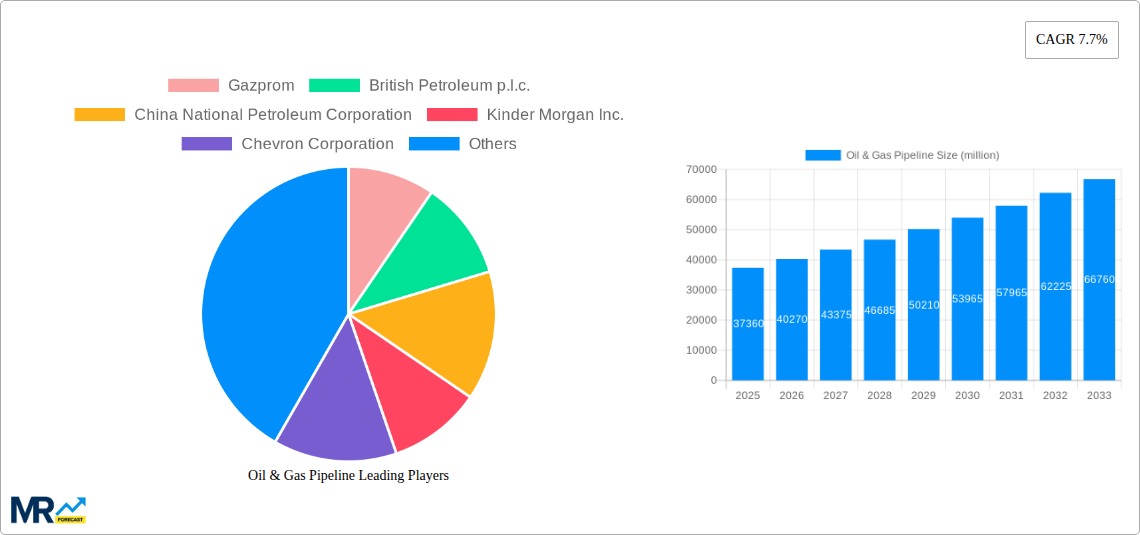

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil & Gas Pipeline?

The projected CAGR is approximately 7.7%.

Oil & Gas Pipeline

Oil & Gas PipelineOil & Gas Pipeline by Type (Electric Resistance Welding Steel Pipe, Submerged Arc Welding Steel Pipe, Seamless Steel Pipe, Polyethylene & Composite), by Application (Oil Delivery, Natural Gas Delivery), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

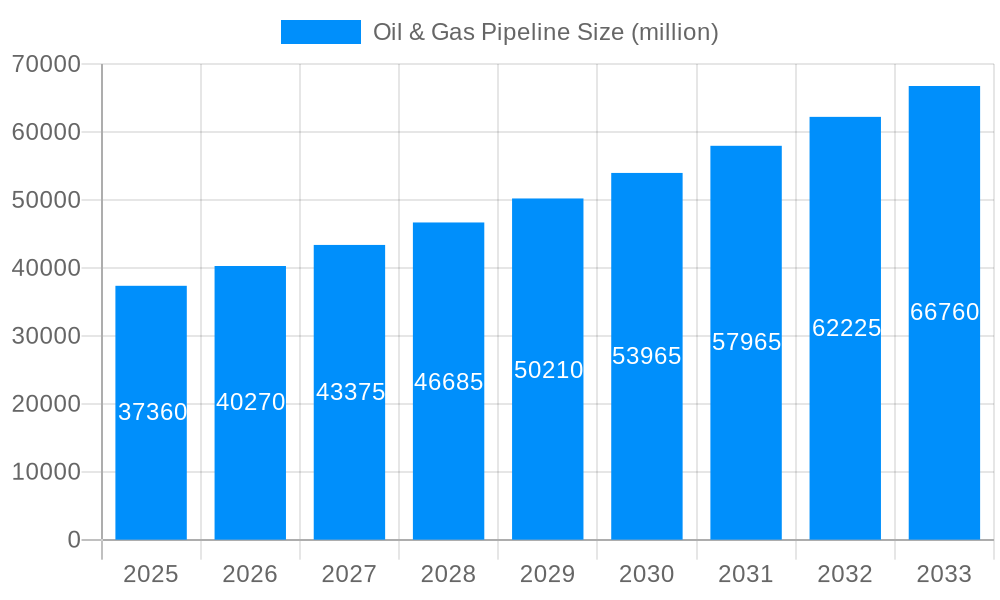

The global Oil & Gas Pipeline market is poised for substantial expansion, projected to reach a market size of approximately USD 37,360 million by 2025. This growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 7.7% anticipated from 2025 to 2033. The primary drivers fueling this expansion include the ever-increasing global demand for energy, necessitating efficient and extensive transportation networks for crude oil and natural gas. Significant investments in the exploration and production of hydrocarbons, particularly in emerging economies, further propel the need for advanced pipeline infrastructure. The ongoing development of offshore oil and gas fields, coupled with the expansion of onshore transmission capabilities, will be critical in meeting this growing energy appetite. Additionally, the strategic importance of energy security for many nations is a key factor encouraging the construction and maintenance of resilient pipeline systems.

The market is characterized by a diverse range of segments and a dynamic competitive landscape. In terms of type, Seamless Steel Pipes are expected to command a significant share due to their superior strength and durability, making them ideal for high-pressure applications. Electric Resistance Welding (ERW) Steel Pipe and Submerged Arc Welding (SAW) Steel Pipe will also play crucial roles, particularly in onshore and offshore transmission projects respectively, offering cost-effectiveness and reliability. Polyethylene & Composite pipes are gaining traction for specific applications, especially in distribution networks. On the application front, Natural Gas Delivery is anticipated to be a dominant segment, driven by the global shift towards cleaner energy sources and the expanding natural gas infrastructure. Oil Delivery remains a cornerstone, with continuous upgrades and expansions of existing networks. Key players like Gazprom, British Petroleum, China National Petroleum Corporation, and Kinder Morgan Inc. are actively investing in technological advancements, geographical expansion, and strategic collaborations to secure their market positions in this evolving sector.

This comprehensive report offers an in-depth analysis of the global Oil & Gas Pipeline market, providing critical insights and future projections for stakeholders. Spanning a Study Period from 2019-2033, the report leverages a robust methodology, with the Base Year and Estimated Year both set at 2025. The detailed Forecast Period of 2025-2033 is built upon a thorough examination of the Historical Period (2019-2024). The report delves into market dynamics, including key trends, driving forces, challenges, and growth catalysts, offering a panoramic view of the industry landscape. With a focus on specific product Types such as Electric Resistance Welding Steel Pipe, Submerged Arc Welding Steel Pipe, Seamless Steel Pipe, and Polyethylene & Composite, alongside crucial Applications like Oil Delivery and Natural Gas Delivery, this report aims to equip businesses with actionable intelligence for strategic decision-making.

XXX The global Oil & Gas Pipeline market is currently experiencing a dynamic shift, driven by evolving energy demands and an increasing emphasis on efficiency and sustainability. A significant trend observed is the continuous expansion and upgrading of existing pipeline infrastructure, particularly in emerging economies where energy consumption is on the rise. This expansion is not merely about increasing capacity but also about enhancing the safety and integrity of these critical transportation networks. The adoption of advanced materials and technologies is a prominent trend, aimed at reducing leakage risks, improving corrosion resistance, and extending the operational lifespan of pipelines. For instance, the increasing use of composite materials and advanced coatings signifies a move towards lighter, more durable, and environmentally friendlier pipeline solutions.

Furthermore, the report highlights a growing trend towards the transportation of natural gas, fueled by its position as a cleaner fossil fuel compared to oil. This is leading to significant investments in natural gas pipeline projects, especially for connecting remote gas fields to processing facilities and end-user markets. The integration of smart pipeline technologies, including real-time monitoring systems, artificial intelligence for predictive maintenance, and automated leak detection, is another key trend. These technologies are crucial for improving operational efficiency, minimizing downtime, and ensuring compliance with stringent safety and environmental regulations. The report also indicates a growing focus on subsea pipeline construction and maintenance, as exploration and production activities move into deeper waters. This trend necessitates the development and deployment of specialized equipment and expertise.

In terms of market segmentation, the demand for Submerged Arc Welding (SAW) Steel Pipe and Seamless Steel Pipe remains robust due to their superior strength and durability, making them ideal for high-pressure applications in both oil and gas transportation. However, the Polyethylene & Composite segment is witnessing accelerated growth, particularly for lower-pressure applications and distribution networks, owing to its cost-effectiveness, ease of installation, and resistance to corrosion. The market is also observing a growing emphasis on the repurposing of existing oil pipelines for the transportation of other commodities, including hydrogen and CO2, as part of the broader energy transition efforts. This strategic adaptation showcases the inherent flexibility of pipeline infrastructure and its potential role in a decarbonized future. The increasing regulatory scrutiny and public awareness regarding pipeline safety and environmental impact are also shaping market trends, pushing for stricter adherence to industry standards and the adoption of best practices throughout the entire pipeline lifecycle.

The Oil & Gas Pipeline market is experiencing robust growth propelled by several interconnected driving forces. Foremost among these is the persistent and growing global demand for energy, particularly from developing economies in Asia and Africa, which are undergoing rapid industrialization and urbanization. This increased energy consumption necessitates the expansion and modernization of existing pipeline networks to ensure a steady and reliable supply of crude oil and natural gas. Furthermore, the ongoing transition to cleaner energy sources, while a long-term shift, still relies heavily on natural gas as a bridge fuel. Consequently, significant investments are being channeled into building new natural gas pipelines to connect expanding production sites with burgeoning consumer markets, thereby reinforcing the strategic importance of gas delivery infrastructure.

The substantial reserves of oil and gas discovered in previously inaccessible or remote regions also act as a significant driver. The development of these resources often requires extensive pipeline networks to transport the extracted commodities to processing plants and export terminals. Technological advancements in pipeline construction, material science, and leak detection systems are also contributing to market expansion. These innovations enable the construction of pipelines in more challenging terrains and deeper waters, while also enhancing safety, efficiency, and environmental protection, thereby reducing operational risks and costs. Additionally, government policies and regulatory frameworks that encourage energy infrastructure development and ensure energy security play a crucial role in driving investments in the oil and gas pipeline sector. The strategic imperative of maintaining energy independence and diversifying supply routes further fuels the demand for robust pipeline systems.

Despite the strong growth drivers, the Oil & Gas Pipeline sector faces several significant challenges and restraints that can impede its progress. One of the most prominent challenges is the increasing environmental scrutiny and regulatory hurdles. Public opposition to new pipeline projects, often fueled by concerns about environmental impact, potential spills, and climate change, can lead to lengthy approval processes, legal battles, and project cancellations. This growing opposition translates into higher compliance costs and a greater risk of project delays, impacting investment decisions. The volatility in crude oil and natural gas prices also presents a considerable restraint. Significant fluctuations in commodity prices can affect the profitability of exploration and production activities, which in turn influences the investment decisions for new pipeline infrastructure. Low commodity prices can lead to the deferral or cancellation of pipeline projects, particularly those that are not deemed essential for immediate supply.

The aging infrastructure in many established oil and gas producing regions poses another significant challenge. Maintaining, repairing, and upgrading existing pipelines to meet current safety and environmental standards requires substantial capital investment and can be a complex undertaking. The risk of leaks and failures in older pipelines can lead to environmental damage and operational disruptions, necessitating continuous monitoring and remedial actions. Furthermore, geopolitical instability and security concerns in certain regions can disrupt supply chains and pose risks to pipeline operations, leading to increased insurance costs and the need for robust security measures. The high upfront capital investment required for constructing new pipelines, coupled with long payback periods, also acts as a restraint, especially for smaller companies or in markets with uncertain demand projections. The development of alternative energy sources and increasing adoption of renewable energy technologies, while a long-term trend, could potentially reduce the long-term demand for fossil fuels, thereby impacting future investments in oil and gas pipeline infrastructure.

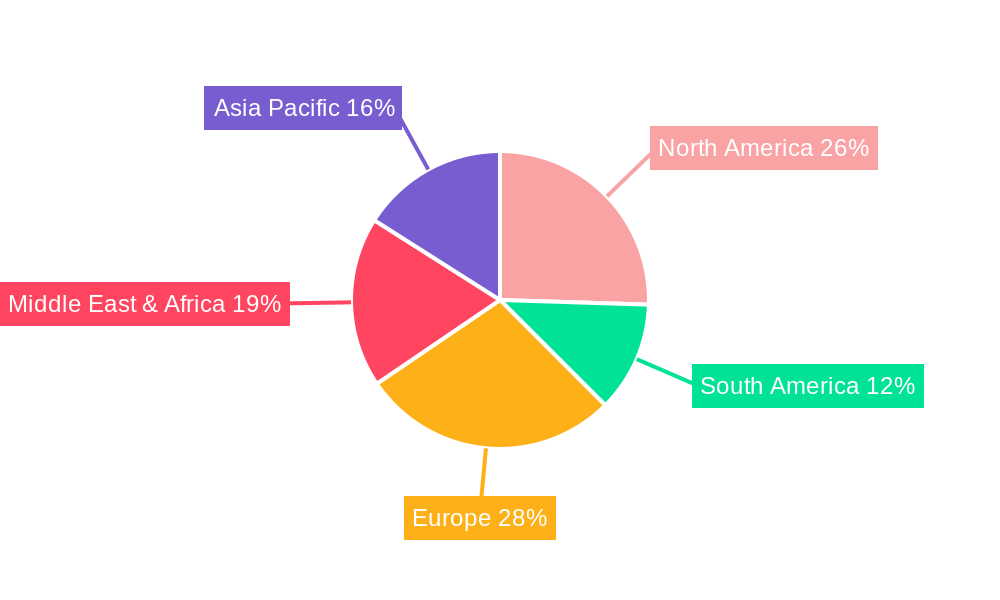

The global Oil & Gas Pipeline market is characterized by a dynamic interplay of regional development and segment specialization. While multiple regions contribute significantly, Asia Pacific is projected to be a dominant force in the market, driven by its insatiable and growing energy demand, coupled with substantial investments in infrastructure development. Countries like China and India, with their rapidly expanding economies and large populations, are at the forefront of this growth. China, in particular, has been actively investing in a vast network of oil and gas pipelines to secure its energy supply, connect domestic production with import terminals, and facilitate the distribution of energy resources across its vast territory. The country's ambitious energy infrastructure plans, including the development of long-distance cross-country pipelines and offshore infrastructure, are set to drive significant demand for various pipeline segments.

India's energy landscape is also undergoing a transformation, with increasing focus on expanding its natural gas grid and oil transportation networks to meet the rising demand from industrial, commercial, and residential sectors. The government's initiatives to promote the use of natural gas as a cleaner fuel are leading to substantial investments in pipeline projects. Other countries in the Southeast Asian region, such as Indonesia and Vietnam, are also contributing to market growth through their ongoing oil and gas exploration and production activities, requiring the construction of associated pipeline infrastructure.

In terms of dominant segments, Natural Gas Delivery is expected to witness the most significant growth and dominance. The global shift towards cleaner energy sources has positioned natural gas as a crucial bridge fuel, leading to a surge in demand for natural gas pipelines. This includes the development of large-scale transmission pipelines to transport gas from production basins to consumption centers, as well as extensive distribution networks to reach end-users. The increasing adoption of Liquefied Natural Gas (LNG) and the subsequent need for regasification terminals and associated pipeline infrastructure further bolster the growth of the natural gas delivery segment.

Within the pipeline Type classification, Submerged Arc Welding (SAW) Steel Pipe is anticipated to continue its dominance, especially for large-diameter, high-pressure applications in long-haul transmission pipelines for both oil and natural gas. The inherent strength, reliability, and cost-effectiveness of SAW pipes make them the preferred choice for critical infrastructure projects. However, Seamless Steel Pipe will also maintain a strong position, particularly for high-pressure and critical applications where superior mechanical properties and integrity are paramount. The Polyethylene & Composite segment is expected to experience rapid growth, especially in distribution networks and for applications requiring corrosion resistance and ease of installation. The increasing focus on reducing leakage and enhancing the safety of lower-pressure distribution systems will further fuel the adoption of these materials. The development of advanced composite materials with improved strength-to-weight ratios and chemical resistance will expand their application scope.

The Oil & Gas Pipeline industry is propelled by several key growth catalysts. The escalating global demand for energy, particularly from developing nations, necessitates continuous expansion and modernization of pipeline networks. The strategic importance of natural gas as a cleaner transition fuel is a significant driver, leading to substantial investments in gas pipelines. Technological advancements in materials science, welding techniques, and monitoring systems are enabling safer, more efficient, and cost-effective pipeline construction and operation. Government initiatives aimed at enhancing energy security and developing domestic energy resources also play a crucial role in catalyzing market growth. Furthermore, the increasing focus on the transportation of unconventional resources and the growing exploration activities in challenging environments, such as deep offshore, are creating new avenues for pipeline development.

This report provides an all-encompassing view of the Oil & Gas Pipeline market, meticulously detailing market dynamics, segmentation, and future trajectories. It offers a granular analysis of product types, including Electric Resistance Welding Steel Pipe, Submerged Arc Welding Steel Pipe, Seamless Steel Pipe, and Polyethylene & Composite, alongside critical applications such as Oil Delivery and Natural Gas Delivery. The report's comprehensive coverage extends to identifying key market drivers, challenges, and significant growth catalysts that are shaping the industry's landscape. Furthermore, it furnishes valuable insights into regional market dominance and the strategic moves of leading global players, ensuring stakeholders are equipped with the necessary intelligence for informed decision-making and strategic planning in this vital sector of the global energy infrastructure.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.7%.

Key companies in the market include Gazprom, British Petroleum p.l.c., China National Petroleum Corporation, Kinder Morgan Inc., Chevron Corporation, Royal Dutch Shell p.l.c, ConocoPhillips, Eni S.p.A, Tenaris S.A., Europipe, TMK, Chelpipe, National Oilwell Varco, Welspun Corp Ltd., Maharashtra Seamless Ltd., EVRAZ North America, General Electric, TechnipFMC, Saipem S.p.A, Subsea 7 S.A., .

The market segments include Type, Application.

The market size is estimated to be USD 37360 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Oil & Gas Pipeline," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Oil & Gas Pipeline, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.