1. What is the projected Compound Annual Growth Rate (CAGR) of the New Energy Vehicle Charging Facilities?

The projected CAGR is approximately XX%.

New Energy Vehicle Charging Facilities

New Energy Vehicle Charging FacilitiesNew Energy Vehicle Charging Facilities by Type (AC Charging Pile, DC Charging Pile, World New Energy Vehicle Charging Facilities Production ), by Application (Residential Charging, Public Charging, World New Energy Vehicle Charging Facilities Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

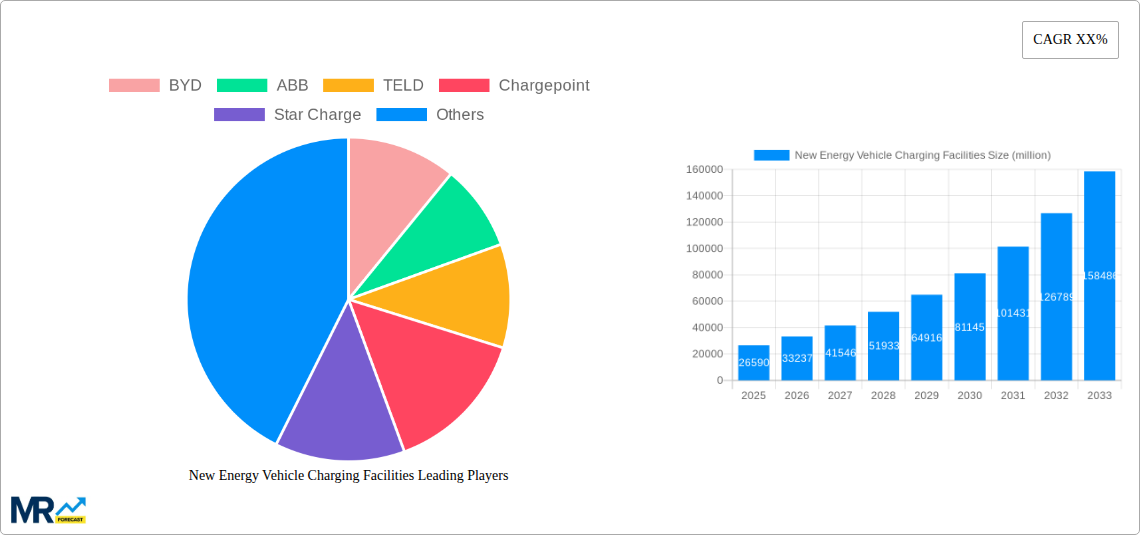

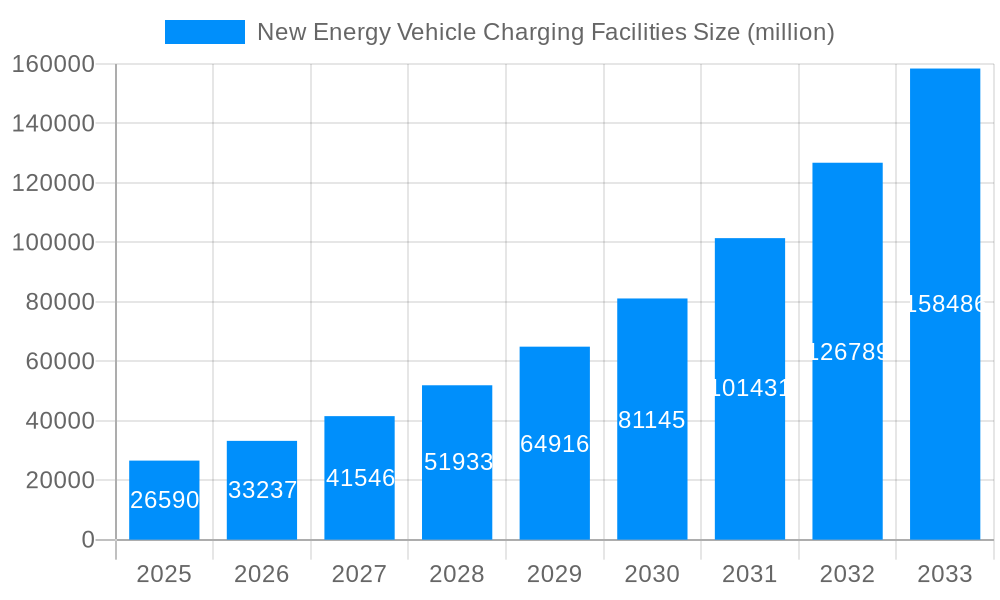

The global New Energy Vehicle (NEV) Charging Facilities market is poised for substantial growth, estimated at \$26.59 billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately 25% through 2033. This robust expansion is primarily driven by the escalating adoption of electric vehicles (EVs) worldwide, fueled by government incentives, increasing environmental consciousness, and advancements in battery technology. The market's trajectory is further bolstered by significant investments in charging infrastructure by both public and private entities, aiming to alleviate range anxiety and facilitate seamless EV ownership. The shift towards sustainable transportation solutions is a paramount force, with regulatory mandates and corporate sustainability goals actively promoting the transition to electric mobility.

The NEV Charging Facilities market is characterized by a dynamic competitive landscape and evolving technological advancements. Key segments include AC Charging Piles and DC Charging Piles, with DC charging expected to gain significant traction due to its faster charging capabilities, catering to public charging needs. Residential charging remains a crucial segment, offering convenience to EV owners. Geographically, Asia Pacific, particularly China, stands as a dominant force, driven by its early and aggressive adoption of EVs and extensive charging network development. North America and Europe are also witnessing rapid infrastructure expansion, supported by favorable government policies and a growing EV market share. The market is segmented into residential and public charging applications, with ongoing innovation focusing on smart charging solutions, grid integration, and faster charging speeds to meet the demands of an expanding EV fleet.

This comprehensive report delves into the dynamic global landscape of New Energy Vehicle (NEV) charging facilities, providing an in-depth analysis of market trends, driving forces, challenges, regional dominance, growth catalysts, leading players, and significant developments. Spanning the Historical Period (2019-2024), Base Year (2025), and extending to a robust Forecast Period (2025-2033), this study offers actionable insights for stakeholders navigating this rapidly evolving sector. The report leverages current market data and projected figures in the million unit to paint a clear picture of the market's trajectory.

The global NEV charging facilities market is experiencing an unprecedented surge, driven by a confluence of accelerating NEV adoption and supportive government policies aimed at decarbonization. XXX, the total global production of NEV charging facilities is projected to reach a monumental 15.6 million units by the end of the forecast period in 2033, up from approximately 3.2 million units in the base year of 2025. This exponential growth signifies a profound shift in the automotive and energy infrastructure landscape. The demand for both AC and DC charging solutions is escalating, with AC charging piles catering to the widespread need for overnight and workplace charging, while DC fast chargers are becoming indispensable for longer journeys and public rapid charging scenarios. The market is witnessing a significant expansion in public charging infrastructure, with governments and private entities investing heavily to alleviate range anxiety and encourage broader NEV uptake. Residential charging, though a mature segment, continues to grow with increased homeownership of NEVs and the development of smart home charging solutions. Furthermore, the integration of charging facilities with smart grids and renewable energy sources is emerging as a key trend, enabling a more sustainable and efficient charging ecosystem. The report meticulously analyzes the interplay of these trends, providing a granular view of their impact on market dynamics and regional growth patterns. The increasing commoditization of charging hardware is also leading to a focus on innovative business models, including charging-as-a-service, subscription models, and integrated payment solutions. The development of ultra-fast charging technologies, capable of replenishing NEV batteries within minutes, is poised to further revolutionize the charging experience and accelerate the transition away from internal combustion engine vehicles. The proliferation of charging networks, coupled with advancements in interoperability and standardization, will be critical in ensuring a seamless and user-friendly charging experience for NEV owners worldwide.

The exponential growth in the NEV charging facilities market is primarily propelled by a trifecta of powerful forces. Firstly, the escalating adoption of New Energy Vehicles globally is the most fundamental driver. As consumer awareness of environmental issues and the long-term cost savings associated with EVs increase, coupled with a wider array of attractive EV models, demand for these vehicles is soaring. This directly translates into a burgeoning need for accessible and efficient charging infrastructure. Secondly, supportive government policies and incentives play a crucial role. Many nations have set ambitious targets for NEV sales and carbon emission reductions, leading to substantial investments in charging infrastructure development through subsidies, tax credits, and regulatory mandates. These policies create a favorable investment climate and accelerate deployment. Thirdly, technological advancements in battery technology and charging infrastructure are making NEVs more practical and convenient. Improved battery ranges reduce range anxiety, while faster charging speeds significantly shorten charging times, mirroring the convenience of traditional refueling. The development of smart charging technologies, enabling grid integration and demand-side management, further enhances the appeal of NEVs and their supporting infrastructure. These driving forces collectively create a powerful momentum that is transforming the automotive and energy sectors.

Despite the robust growth, the NEV charging facilities market is not without its hurdles. One significant challenge is the high upfront cost of infrastructure deployment. Establishing a comprehensive charging network, particularly with DC fast chargers, requires substantial capital investment, which can be a deterrent for some investors and operators. Another restraint is the patchy grid capacity in certain regions. The increased demand for electricity from a large number of charging stations can strain existing power grids, necessitating significant upgrades and investments in grid modernization, which is a time-consuming and costly process. Furthermore, standardization and interoperability issues continue to pose a challenge. The proliferation of different charging connector types, communication protocols, and payment systems can create confusion and inconvenience for NEV users, hindering seamless charging experiences across various networks. Lastly, permitting and regulatory complexities can slow down the deployment of charging facilities. Obtaining necessary permits and navigating diverse local regulations can be a bureaucratic maze, leading to delays and increased project costs. Addressing these challenges is crucial for unlocking the full potential of the NEV charging ecosystem.

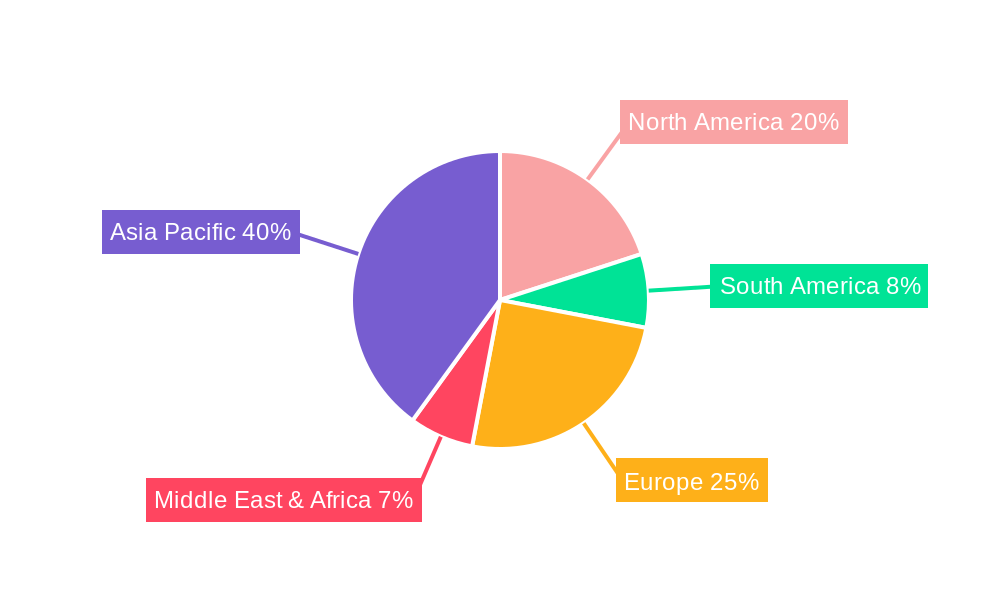

The Asia-Pacific region, particularly China, is poised to dominate the global New Energy Vehicle Charging Facilities market, driven by aggressive government mandates, a massive NEV manufacturing base, and a rapidly expanding consumer market for electric vehicles. China's strategic focus on developing a comprehensive charging infrastructure, aiming to support its ambitious NEV adoption targets, has resulted in significant investments and rapid deployment. By 2025, China is expected to account for over 60% of the global NEV charging facilities production, with an estimated output of 9.36 million units. This dominance is further amplified by the country's leading NEV manufacturers like BYD, which are not only producing vehicles but also heavily investing in their own charging solutions and networks. The sheer scale of NEV sales in China necessitates a proportional scaling of charging infrastructure, making it the undeniable leader.

Within the segments, DC Charging Piles are expected to witness the most substantial growth and dominance, especially in the context of public charging. The demand for rapid charging solutions to address range anxiety and facilitate long-distance travel is a primary catalyst for the proliferation of DC charging. By 2025, the global production of DC Charging Piles is estimated to reach 4.1 million units, representing a significant portion of the total NEV charging facilities production. This segment is crucial for enabling the widespread adoption of NEVs for daily commuting and commercial applications. The increasing development of fast-charging corridors and the integration of DC chargers at public locations like shopping malls, service stations, and transportation hubs underscore their importance. The technological advancements in higher-power DC charging, capable of delivering hundreds of kilowatts, are further accelerating the adoption of this segment, promising significantly reduced charging times that are becoming increasingly competitive with refueling internal combustion engine vehicles. The global rollout of DC fast-charging networks is a key indicator of its anticipated market dominance.

Another segment demonstrating significant market share and growth is Public Charging. The strategic imperative to build out widespread public charging infrastructure, accessible to all NEV users regardless of their home charging capabilities, is a global trend. Governments and private entities are heavily investing in expanding public charging networks to alleviate range anxiety and promote NEV adoption. By 2025, the global market for Public Charging facilities is projected to be a substantial contributor, with an estimated 5.8 million units of charging facilities dedicated to public use. This segment encompasses a variety of charging speeds and types, from Level 2 AC chargers in parking lots to high-power DC fast chargers along highways. The growing trend of integrated mobility services, where charging is a seamless part of the overall transportation experience, further bolsters the significance of the public charging segment. The development of user-friendly payment systems and network interoperability are critical factors driving the expansion and dominance of public charging solutions.

The NEV charging facilities industry is experiencing robust growth fueled by several key catalysts. The increasing government subsidies and policy support for both NEV adoption and charging infrastructure development is a primary growth engine. Furthermore, declining battery costs and improving EV range are making NEVs more attractive to consumers, thereby increasing the demand for charging solutions. The expansion of charging networks and the rise of innovative business models, such as charging-as-a-service, are also creating new opportunities and accelerating market penetration.

This report offers a comprehensive analysis of the New Energy Vehicle Charging Facilities market, meticulously examining the interplay of technological advancements, market dynamics, and regulatory landscapes. The study provides a detailed breakdown of the market by Type (AC Charging Pile, DC Charging Pile) and Application (Residential Charging, Public Charging), alongside an in-depth analysis of World New Energy Vehicle Charging Facilities Production. Industry developments, including strategic partnerships, technological breakthroughs, and regulatory shifts, are thoroughly investigated. The report's robust methodology and extensive data collection ensure a reliable and insightful overview, equipping stakeholders with the knowledge to navigate this complex and rapidly expanding sector effectively.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include BYD, ABB, TELD, Chargepoint, Star Charge, Wallbox, EVBox, Webasto, Xuji Group, SK Signet, Pod Point, Leviton, CirControl, Daeyoung Chaevi, EVSIS, IES Synergy, Siemens, Clipper Creek, Auto Electric Power Plant, DBT-CEV, .

The market segments include Type, Application.

The market size is estimated to be USD 26590 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "New Energy Vehicle Charging Facilities," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the New Energy Vehicle Charging Facilities, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.