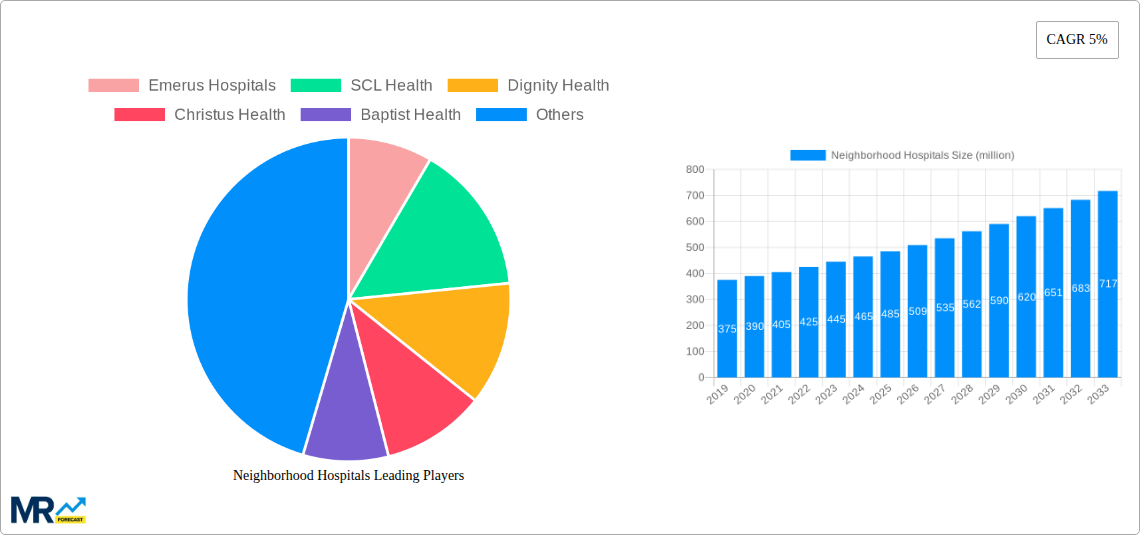

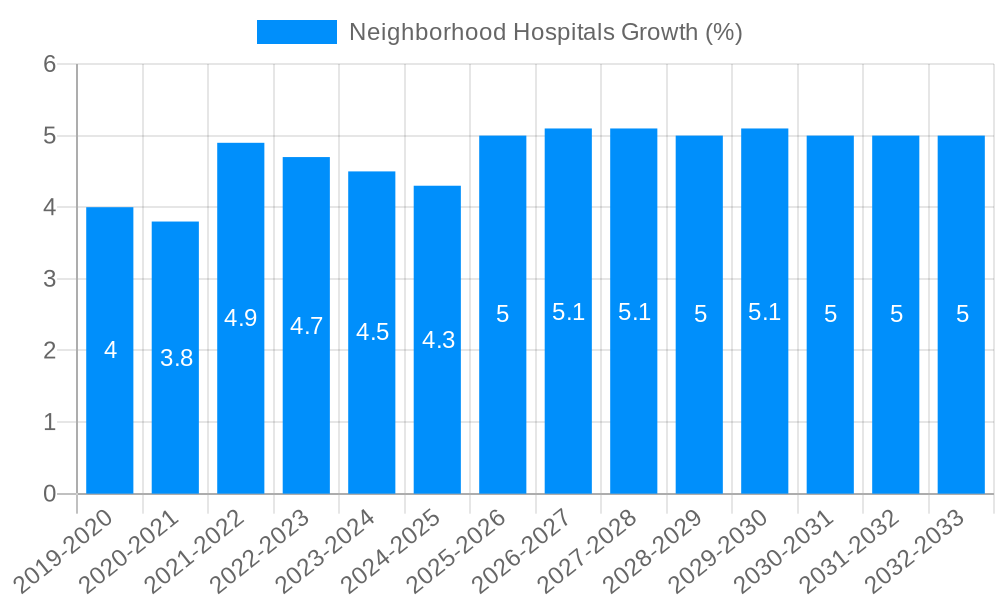

1. What is the projected Compound Annual Growth Rate (CAGR) of the Neighborhood Hospitals?

The projected CAGR is approximately 5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Neighborhood Hospitals

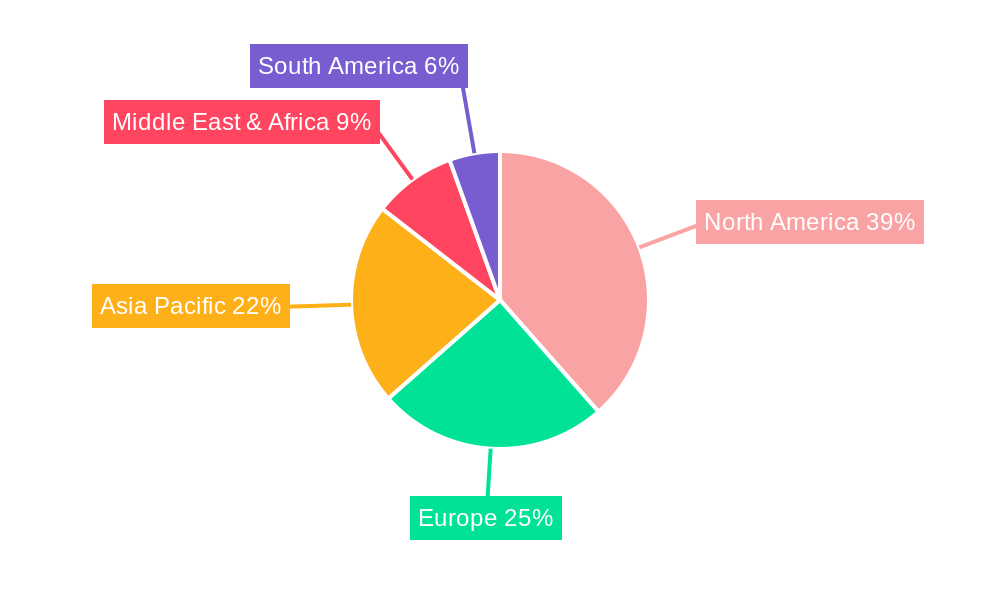

Neighborhood HospitalsNeighborhood Hospitals by Type (/> Tier 1 cities, Tier 2 cities, Tier 3 cities), by Application (/> Primary care, Dietary guidance, Gynaecological services, Non-emergency outpatient surgery, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The Neighborhood Hospitals market is poised for significant expansion, projected to reach an estimated $485 million by 2025. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of 5%, indicating sustained demand and strategic development within the sector. A primary driver for this expansion is the increasing patient preference for accessible, community-based healthcare services that offer a more personalized and convenient alternative to large, distant medical centers. The demand for primary care and dietary guidance is particularly strong, reflecting a growing emphasis on preventative health and wellness. Furthermore, the market is witnessing a surge in the utilization of neighborhood hospitals for non-emergency outpatient surgeries and gynecological services, driven by improved infrastructure and the availability of specialized medical professionals within these smaller, more localized facilities. This trend underscores a shift towards decentralized healthcare delivery models that prioritize patient convenience and reduced wait times.

The market is characterized by distinct segmentation based on city tiers, with Tier 1 cities leading in adoption due to higher population density and greater disposable income. However, Tier 2 and Tier 3 cities are emerging as significant growth areas, driven by government initiatives aimed at improving healthcare access in underserved regions and the establishment of new facilities by key players such as Emerus Hospitals, SCL Health, and Dignity Health. These companies are actively investing in expanding their footprint, recognizing the untapped potential in suburban and rural areas. While the market benefits from strong drivers, potential restraints include regulatory hurdles in certain regions and the initial capital investment required for establishing and equipping these facilities. Despite these challenges, the overarching trend towards localized, patient-centric care, coupled with technological advancements in medical equipment and telemedicine integration, is expected to propel the Neighborhood Hospitals market to new heights throughout the forecast period of 2025-2033.

The neighborhood hospital market is experiencing a transformative shift, driven by an evolving healthcare landscape and a growing demand for localized, accessible, and cost-effective medical services. XXX This market is projected to witness robust expansion, with estimates suggesting a valuation that could reach several tens of millions of dollars by the end of the forecast period in 2033. The base year of 2025 sets the stage for this growth, with a projected market size also in the tens of millions of dollars. During the study period from 2019 to 2033, encompassing both the historical period of 2019-2024 and the forecast period of 2025-2033, key trends have emerged.

One of the most prominent trends is the increasing integration of these facilities into community life, moving away from the traditional large, centralized hospital model. Neighborhood hospitals, often smaller in scale, are strategically located to serve specific geographical areas, reducing travel time and improving patient convenience. This trend is further amplified by the growing preference for outpatient services, particularly for non-emergency procedures, which these smaller facilities are well-equipped to handle. The focus is shifting towards preventative care and early intervention, with neighborhood hospitals playing a crucial role in providing accessible primary care, dietary guidance, and specialized services like gynaecological care. The market is also seeing a rise in hybrid models, where neighborhood hospitals offer a blend of inpatient and outpatient services, catering to a wider spectrum of patient needs. Technology adoption, including telehealth and remote patient monitoring, is also a significant driver, enhancing the reach and efficiency of these localized healthcare hubs. Furthermore, the evolving payer landscape and the emphasis on value-based care are pushing healthcare providers to adopt more efficient and patient-centric models, which neighborhood hospitals are ideally positioned to fulfill. The overall market sentiment points towards continued investment and expansion in this sector, as stakeholders recognize the intrinsic value of bringing healthcare closer to where people live and work.

Several powerful forces are propelling the growth and adoption of neighborhood hospitals. Foremost among these is the increasing patient preference for convenience and accessibility. With busy lives and the desire for immediate care, the proximity offered by neighborhood hospitals is a significant draw. This trend is further reinforced by the growing emphasis on outpatient care and same-day surgeries, areas where neighborhood hospitals excel in providing efficient and personalized services. The demographic shift towards an aging population also plays a crucial role, as elderly individuals often require more frequent, localized medical attention and find it challenging to travel to distant large hospitals. Moreover, the rising healthcare costs associated with large, traditional hospitals are pushing both patients and payers towards more cost-effective alternatives, a niche that neighborhood hospitals are effectively filling. Their leaner operational models and focused service offerings often translate into lower overall costs without compromising on quality for specific types of care. The ongoing advancements in medical technology, including minimally invasive surgical techniques and diagnostic tools, also enable smaller facilities to offer a wider range of services, making them more comprehensive care centers. Finally, a growing awareness and proactive approach to health and wellness among the general population is fueling the demand for accessible primary care and preventative services, which are core offerings of many neighborhood hospitals.

Despite the promising outlook, the neighborhood hospital sector faces certain challenges and restraints that could temper its growth trajectory. A primary concern is the potential for limited service offerings compared to large, comprehensive medical centers. While designed for specific needs, some patients may require specialized equipment or a broader range of subspecialty care that a neighborhood hospital cannot provide, necessitating referrals to larger institutions. This can lead to a fragmented patient experience and potential delays in care. Another significant hurdle is regulatory and reimbursement complexities. Navigating the intricate web of healthcare regulations and securing favorable reimbursement rates from insurance providers can be challenging for smaller, independent facilities. This can impact their financial viability and ability to invest in expansion or advanced technologies. Staffing shortages, particularly for highly specialized medical professionals, also pose a threat. Attracting and retaining skilled physicians and nurses in localized areas can be more difficult than in established metropolitan hospital systems. Furthermore, initial capital investment for establishing and equipping a neighborhood hospital can be substantial, potentially deterring smaller operators or those with limited access to funding. The perception of quality and trust also needs to be actively cultivated. Patients may inherently associate larger hospitals with higher standards of care, and neighborhood hospitals will need to consistently demonstrate their commitment to quality and patient safety to build and maintain public confidence. Finally, competition from existing healthcare providers, including established physician practices and urgent care centers, can create a crowded market and necessitate clear differentiation strategies.

The dominance within the neighborhood hospitals market is not confined to a single region or segment; rather, it's a dynamic interplay of geographical accessibility and the specialization of services offered. However, the United States, particularly its suburban and exurban areas, is poised to emerge as a dominant region due to a confluence of factors.

Tier 2 and Tier 3 Cities as Dominant Segments:

Primary Care and Non-Emergency Outpatient Surgery as Dominant Application Segments:

In essence, the combination of underserved populations in Tier 2 and Tier 3 cities and the strong demand for Primary Care and Non-Emergency Outpatient Surgery creates a powerful synergy that will propel these segments and regions to the forefront of the neighborhood hospital market's growth. The strategic placement in these areas, coupled with a focus on services that address immediate community needs, ensures sustained relevance and market penetration.

The neighborhood hospitals industry is fueled by potent growth catalysts that promise sustained expansion. A primary driver is the escalating demand for convenient and accessible healthcare, pushing services closer to patients. The increasing prevalence of chronic diseases and an aging demographic necessitate localized, ongoing care. Furthermore, the growing preference for outpatient procedures and same-day surgeries aligns perfectly with the operational models of these facilities. The emphasis on value-based care and the pursuit of cost-effective healthcare solutions also position neighborhood hospitals favorably, offering a more economical alternative to large medical centers for specific needs. Technological advancements, including telemedicine and remote patient monitoring, further enhance their reach and efficiency, enabling them to provide broader and more integrated care.

This comprehensive report delves into the dynamic neighborhood hospitals market, providing in-depth analysis and forecasts from 2019 to 2033. It meticulously examines market trends, driving forces, and challenges that shape this evolving sector. The report offers granular insights into key regions and dominant segments, including the strategic importance of Tier 2 and Tier 3 cities and the crucial roles of Primary Care and Non-Emergency Outpatient Surgery. Furthermore, it identifies significant growth catalysts and profiles the leading players, offering a holistic view of the industry landscape. The valuation projections, with a base year of 2025, aim to equip stakeholders with critical data for strategic decision-making and investment opportunities.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5%.

Key companies in the market include Emerus Hospitals, SCL Health, Dignity Health, Christus Health, Baptist Health, Baylor Scott&White Health, The Franciscan Alliance, The Hospitals of Providence, Integris Health, Saint Luke's Health System, St. Vincent Health, Allegheny Health Network, Memorial Hermann, Saint Alphonsus, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Neighborhood Hospitals," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Neighborhood Hospitals, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.