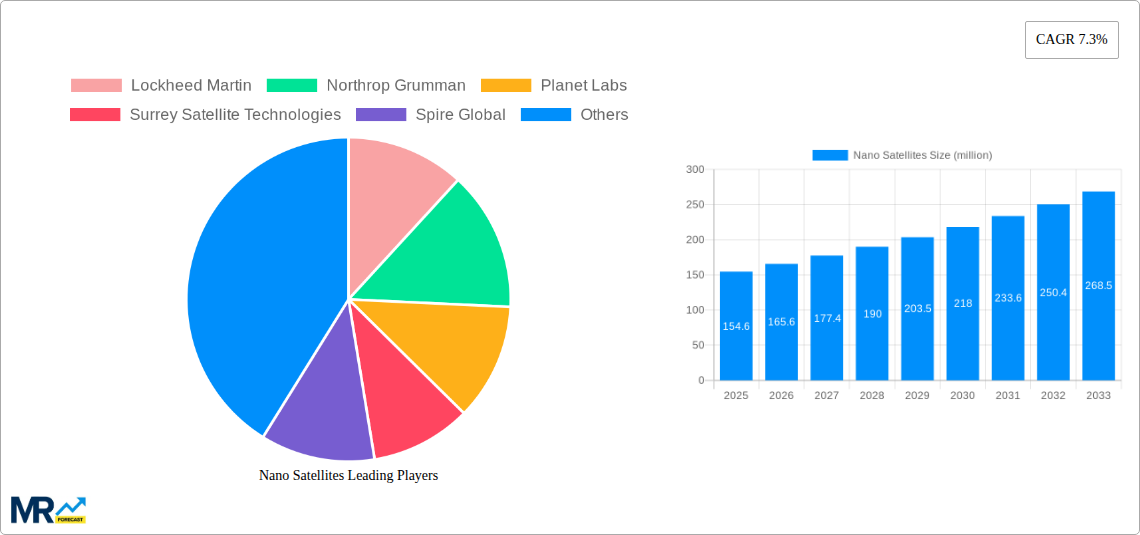

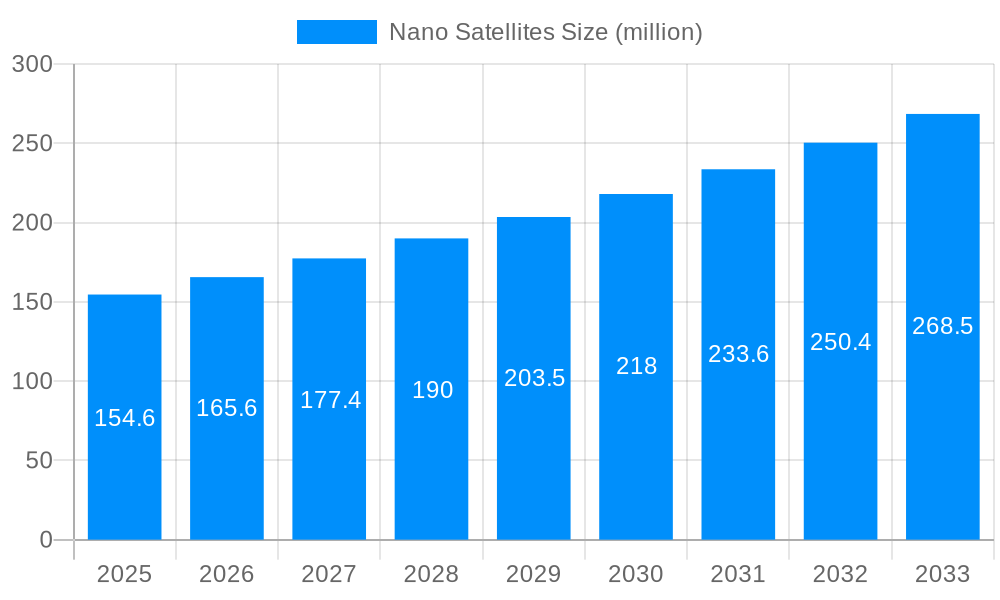

1. What is the projected Compound Annual Growth Rate (CAGR) of the Nano Satellites?

The projected CAGR is approximately 7.3%.

Nano Satellites

Nano SatellitesNano Satellites by Type (Communications Satellite, Positioning Satellite, Others), by Application (Government Departments, Army, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global nanosatellite market is experiencing robust expansion, projected to reach an estimated USD 154.6 million by 2025. This significant growth is fueled by a compelling Compound Annual Growth Rate (CAGR) of 7.3%, indicating sustained and healthy market development through 2033. The surge in demand is primarily driven by the increasing adoption of nanosatellites in critical applications such as communications and positioning, where their cost-effectiveness, rapid deployment, and miniaturization offer distinct advantages over traditional, larger satellites. Emerging trends like the proliferation of small satellite constellations for Earth observation, global internet connectivity, and advanced scientific research are further propelling market expansion. The decreasing launch costs and advancements in miniaturization technologies are making space access more democratized, encouraging a wider array of governmental agencies and private entities to leverage nanosatellite capabilities for data collection, surveillance, and innovative service delivery.

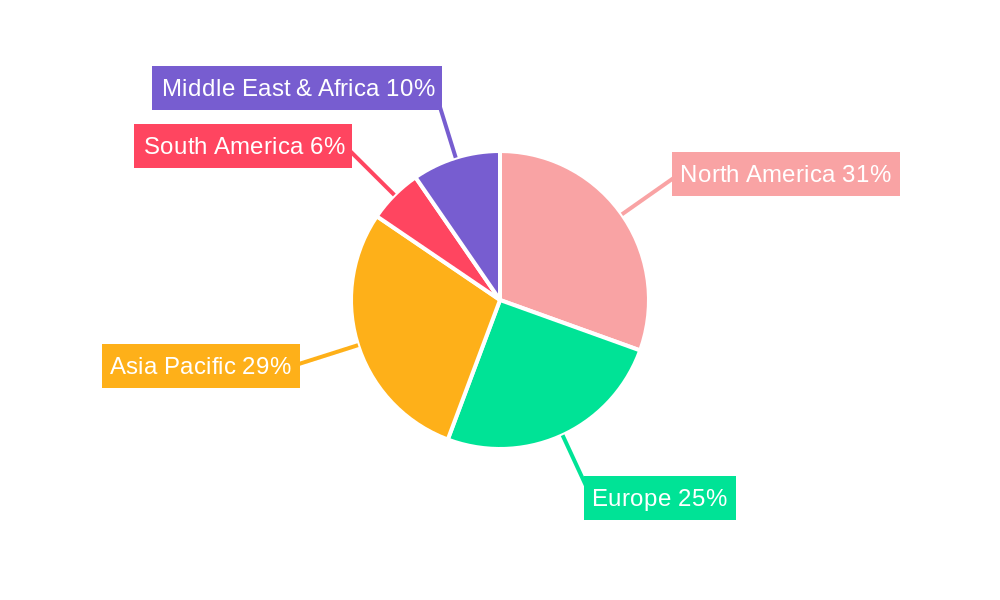

The market's trajectory is also influenced by the expanding applications across government departments and defense sectors, which are increasingly utilizing nanosatellites for national security, intelligence gathering, and disaster management. While the market is dominated by established aerospace giants like Lockheed Martin and Northrop Grumman, a vibrant ecosystem of specialized nanosatellite companies, including Planet Labs and Surrey Satellite Technologies, is emerging, fostering innovation and competition. Key restraints, such as regulatory hurdles and the inherent limitations in payload capacity and lifespan compared to larger satellites, are being actively addressed through technological advancements and evolving policy frameworks. The Asia Pacific region, particularly China and India, is anticipated to be a significant growth engine due to increasing investments in space programs and a burgeoning demand for satellite-based services.

XXX The nano-satellite market is on an unparalleled ascent, driven by a convergence of technological advancements, shrinking development costs, and an expanding array of applications. During the historical period of 2019-2024, the sector witnessed substantial growth, fueled by the increasing deployment of CubeSats and miniaturized satellite platforms. This trend is projected to accelerate significantly through the study period of 2019-2033, with the base year of 2025 serving as a crucial inflection point for projected market valuations. By the estimated year of 2025, the global nano-satellite market is expected to command a valuation in the tens of millions, with forecasts for the forecast period of 2025-2033 indicating a compound annual growth rate that will push this figure into the hundreds of millions. Key market insights reveal a burgeoning demand for earth observation and telecommunications services, with nano-satellites offering a cost-effective and agile solution compared to their larger counterparts. The accessibility and reduced launch costs associated with these small satellites have democratized space, enabling a wider range of entities, from academic institutions to nascent commercial ventures, to participate in space-based activities. This shift is not merely about cost reduction; it is about enhanced flexibility, rapid deployment capabilities, and the ability to create constellations that offer global coverage and high revisit rates. The miniaturization of components, coupled with advancements in propulsion systems and communication technologies, has been instrumental in unlocking new possibilities for nano-satellite constellations. Furthermore, the increasing adoption by government departments and military organizations for intelligence, surveillance, and reconnaissance (ISR) missions underscores the strategic importance of this segment. The market is also seeing innovation in the "Others" category, encompassing scientific research, in-orbit manufacturing, and even space debris removal initiatives. This dynamic ecosystem is characterized by rapid iteration and a constant drive to push the boundaries of what is possible with compact and intelligent space systems.

The relentless progress of the nano-satellite market is underpinned by several potent driving forces. Foremost among these is the dramatic reduction in development and manufacturing costs. Advances in commercial off-the-shelf (COTS) components, coupled with standardized design platforms like CubeSats, have significantly lowered the financial barrier to entry. This has democratized access to space, allowing startups and research institutions to launch missions that were previously the exclusive domain of large government agencies and established aerospace corporations. Secondly, the burgeoning demand for high-resolution Earth observation data for applications ranging from precision agriculture and environmental monitoring to urban planning and disaster management is a major catalyst. Nano-satellite constellations can provide unprecedented revisit rates, offering near real-time imagery and insights crucial for timely decision-making. The need for robust and cost-effective communication solutions, especially for the Internet of Things (IoT) and remote connectivity, is also driving adoption. Nano-satellites can provide global coverage, bridging the digital divide and enabling new services in underserved regions. Furthermore, the increasing emphasis on national security and defense for reconnaissance, surveillance, and tactical communication is leading governments to invest heavily in nano-satellite capabilities. Their agility, rapid deployability, and ability to form resilient, distributed networks make them attractive assets for military operations. Finally, the growth of the NewSpace ecosystem, characterized by private sector innovation and investment, has fostered a competitive environment that accelerates technological development and drives down costs, further fueling the nano-satellite revolution.

Despite the remarkable growth trajectory, the nano-satellite sector faces several significant challenges and restraints that could temper its expansion. A primary concern is the increasing issue of space debris. The proliferation of small satellites, especially in large constellations, raises the risk of collisions, potentially creating cascading debris events that could render valuable orbits unusable. Effective debris mitigation strategies and regulations are crucial but are still evolving. Another challenge lies in the limited payload capacity and power constraints inherent to small satellites. While miniaturization has advanced significantly, the ability to carry complex scientific instruments or sophisticated communication payloads remains restricted, limiting the scope of certain highly demanding applications. The operational lifespan of nano-satellites can also be a concern. Due to their smaller size and potentially less robust design, they may have a shorter operational life compared to traditional satellites, necessitating more frequent replacements and contributing to the overall cost of sustained missions. Regulatory hurdles and licensing complexities, particularly for international operations and spectrum allocation, can also pose a significant impediment. Navigating these bureaucratic processes can be time-consuming and resource-intensive, especially for smaller companies. Furthermore, the intense competition in the market, while driving innovation, also leads to price erosion, potentially impacting the profitability and sustainability of some nano-satellite ventures. Finally, the development of robust ground infrastructure for managing large constellations, including data processing and command and control systems, requires substantial investment and expertise.

The nano-satellite market's dominance is currently bifurcated across key regions and specific segments, demonstrating a dynamic interplay of technological advancement, government adoption, and commercial opportunity.

Dominant Regions/Countries:

Dominant Segments:

The interplay between these regions and segments creates a robust market. For instance, the US government's demand for advanced ISR capabilities (Army application) drives innovation in communication and positioning nano-satellites. Similarly, Europe's focus on climate monitoring (Government Departments application) fuels the development of sophisticated Earth observation nano-satellites, often falling under the "Communications Satellite" type due to their data downlink requirements. The Asia-Pacific region's rapid economic development and desire for improved connectivity are directly stimulating the growth of the communications satellite segment for both commercial and governmental use.

The nano-satellite industry is experiencing robust growth, primarily propelled by the decreasing cost of launch services, which has made space more accessible than ever before. The proliferation of standardized platforms like CubeSats has dramatically reduced development expenses and timelines. Furthermore, the insatiable demand for real-time Earth observation data, coupled with the burgeoning Internet of Things (IoT) market requiring global connectivity, provides substantial market pull. Increasing government investment in defense, intelligence, and scientific research also acts as a significant growth catalyst, driving the adoption of agile and cost-effective nano-satellite solutions for a multitude of applications.

This report provides an exhaustive analysis of the nano-satellite market, delving into its intricate trends and future projections. We cover the historical period of 2019-2024, utilizing 2025 as the base and estimated year for immediate market insights. The forecast period extends from 2025-2033, offering a comprehensive view of growth trajectories. Key segments like Communications Satellites, Positioning Satellites, and Others are analyzed, alongside crucial application areas such as Government Departments and the Army. The report highlights the driving forces behind the market's expansion, the challenges and restraints that need to be addressed, and identifies the key regions and countries poised for dominance. It also elucidates the growth catalysts that will shape the industry's future and provides a detailed overview of the leading players and significant developments witnessed in the sector. This comprehensive coverage aims to equip stakeholders with the knowledge necessary to navigate and capitalize on the evolving nano-satellite landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.3%.

Key companies in the market include Lockheed Martin, Northrop Grumman, Planet Labs, Surrey Satellite Technologies, Spire Global, Dauria Aerospace, Tyvak, CubeSat, NANOSATELLITE COMPANIES, AEC-Able Engineering, AeroAstro L.L.C., Aeroflex, Aerojet, Airbus Defence and Space, Aitech, Alenia Spazio, APCO Technologies, Ardé, ATK, Austrian Aerospace, Boeing Space Systems, CAEN Aerospace, Raytheon, .

The market segments include Type, Application.

The market size is estimated to be USD 154.6 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Nano Satellites," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Nano Satellites, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.