1. What is the projected Compound Annual Growth Rate (CAGR) of the Mining and Metallurgical Waste Management?

The projected CAGR is approximately 6.63%.

Mining and Metallurgical Waste Management

Mining and Metallurgical Waste ManagementMining and Metallurgical Waste Management by Type (Mining, Metallurgy), by Application (Metal, Non-Metallic), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

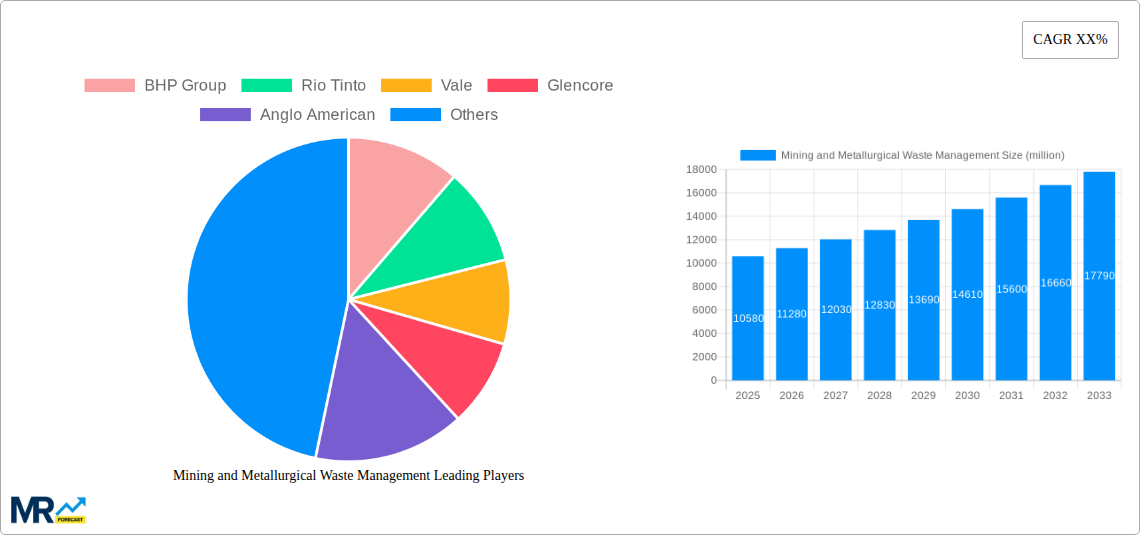

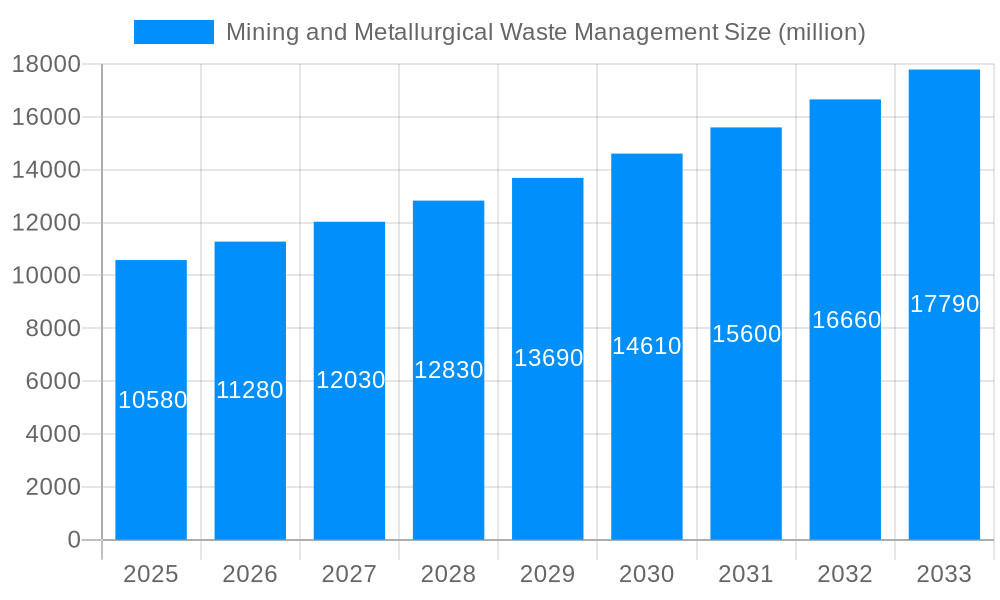

The global Mining and Metallurgical Waste Management market is poised for robust expansion, projected to reach a substantial USD 10.58 billion by 2025. This growth is driven by an estimated Compound Annual Growth Rate (CAGR) of 6.63%, indicating a dynamic and evolving industry landscape. The increasing global demand for metals and non-metallic minerals, coupled with stringent environmental regulations mandating responsible waste disposal and resource recovery, are primary catalysts for this market's upward trajectory. Companies are investing in advanced technologies for waste treatment, recycling, and repurposing, transforming what was once considered waste into valuable secondary resources. This shift towards a circular economy in the mining sector is not only environmentally imperative but also economically beneficial, creating new revenue streams and reducing operational costs. Furthermore, the growing awareness among stakeholders regarding the environmental impact of mining operations fuels the adoption of sustainable waste management practices.

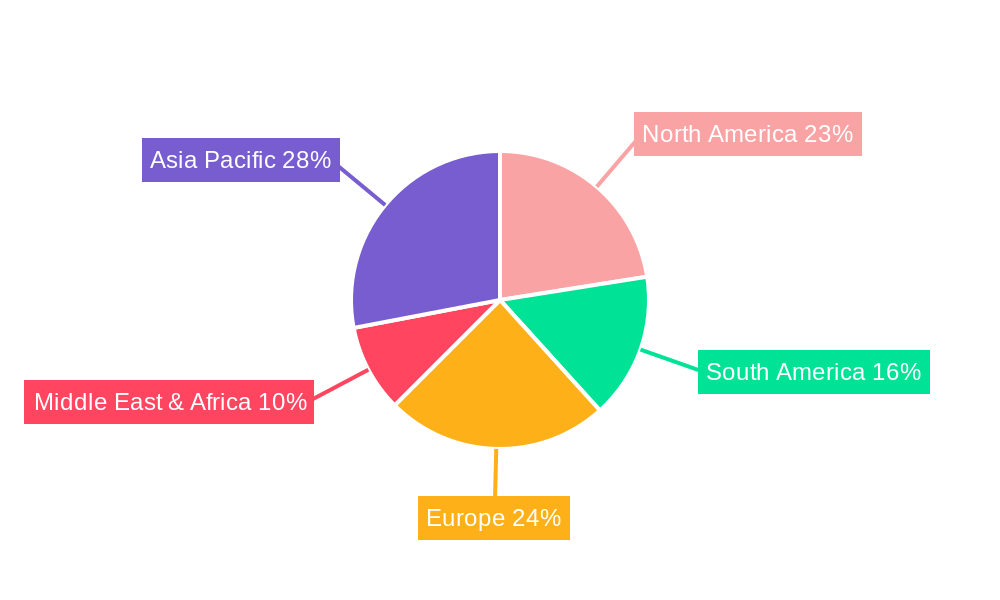

The market is segmented into two primary types: Mining Waste Management and Metallurgical Waste Management, catering to distinct needs within the broader industry. Applications are predominantly focused on Metal and Non-Metallic segments, reflecting the diverse range of materials processed. Key players such as BHP Group, Rio Tinto, Vale, Glencore, and Anglo American are at the forefront of developing and implementing innovative waste management solutions, alongside specialized environmental service providers like Veolia Environnement and SUEZ. Geographically, Asia Pacific, particularly China and India, is expected to emerge as a significant growth engine due to its vast mining operations and increasing focus on environmental compliance. North America and Europe are also substantial markets, driven by advanced technological adoption and stringent regulatory frameworks. The forecast period, extending from 2025 to 2033, anticipates continued innovation and strategic investments, further solidifying the importance of sustainable waste management practices in the mining and metallurgical industries.

Here's a unique report description on Mining and Metallurgical Waste Management, incorporating your specified elements:

The global mining and metallurgical waste management market is experiencing a significant transformation, moving beyond traditional disposal methods towards innovative, sustainable solutions. This shift is driven by increasing environmental regulations, growing corporate social responsibility, and the economic imperative to recover valuable resources from waste streams. During the Study Period of 2019-2033, with a Base Year of 2025, the market is projected to witness substantial growth, fueled by advancements in processing technologies and a heightened awareness of the environmental impact of mining activities. The historical performance from 2019-2024 indicates a steady, albeit sometimes fragmented, increase in investment in waste management solutions. However, the Estimated Year of 2025 marks a critical juncture where the market is poised for more accelerated expansion. The forecast period of 2025-2033 anticipates a robust CAGR as companies increasingly adopt circular economy principles. A key market insight is the burgeoning trend of waste valorization, where formerly discarded materials are being re-processed to extract residual metals and minerals, transforming waste liabilities into potential revenue streams. This is particularly evident in the Metal application segment, where the recovery of precious metals, base metals like copper and zinc, and rare earth elements from tailings and slag is becoming economically viable. Furthermore, the demand for advanced containment and treatment solutions for hazardous waste is projected to rise significantly, driven by stricter environmental protection laws. The integration of Artificial Intelligence (AI) and Machine Learning (ML) for optimizing waste processing and monitoring environmental impact is also a defining trend, promising greater efficiency and reduced operational costs. Companies are investing billions in research and development to create more cost-effective and environmentally sound waste management techniques. For instance, advancements in bioremediation and phytoremediation are opening new avenues for treating contaminated mine sites, further contributing to the positive market trajectory. The projected market size, estimated to be in the billions, reflects this growing importance and the significant capital being deployed to address the complex challenges of mining and metallurgical waste. The overall sentiment is one of increasing maturity and sophistication in how the industry approaches waste, moving towards a paradigm of resource recovery and minimized environmental footprint.

Several powerful forces are actively propelling the growth and innovation within the mining and metallurgical waste management sector. Foremost among these is the escalating global pressure from governments and regulatory bodies to implement stringent environmental standards. These regulations are increasingly penalizing improper waste disposal and mandating the adoption of best practices for waste reduction, treatment, and recycling. This creates a direct imperative for mining and metallurgical operations to invest in robust waste management systems. Secondly, the burgeoning concept of the circular economy is fundamentally reshaping industry priorities. Companies are recognizing the immense untapped value locked within their waste streams, leading to a paradigm shift from viewing waste as a disposal problem to a resource opportunity. This includes the recovery of valuable metals, minerals, and even energy from tailings, slag, and wastewater. Thirdly, the increasing global demand for minerals and metals, driven by megatrends like electrification, renewable energy, and urbanization, is indirectly boosting the waste management market. As mining operations intensify to meet this demand, the volume of waste generated also increases, necessitating more effective management strategies. Furthermore, corporate social responsibility (CSR) and stakeholder expectations are playing a crucial role. Investors, consumers, and local communities are demanding greater transparency and accountability from mining companies regarding their environmental performance. This reputational aspect incentivizes proactive and sustainable waste management practices. Finally, technological advancements in waste processing, separation, and analytical techniques are making it more feasible and cost-effective to manage and even derive value from mining and metallurgical waste, creating a positive feedback loop for market expansion.

Despite the promising growth trajectory, the mining and metallurgical waste management sector is not without its significant hurdles and restraints. A primary challenge lies in the sheer volume and complexity of the waste generated. Mining operations, especially those dealing with low-grade ores, produce vast quantities of tailings and overburden, making their management and disposal an enormous logistical and financial undertaking. The inherent hazardous nature of some metallurgical waste, containing heavy metals and other toxic substances, poses significant environmental risks and necessitates highly specialized and often expensive containment and treatment solutions. High capital investment and operational costs associated with advanced waste management technologies, such as advanced dewatering, chemical treatment, and resource recovery systems, can be a significant barrier, particularly for smaller mining entities or those operating in economically challenging regions. The lack of standardized regulations and enforcement across different jurisdictions can create an uneven playing field and hinder the widespread adoption of best practices. In some regions, inadequate regulatory frameworks or weak enforcement may disincentivize proactive waste management. Technological limitations and the need for continuous innovation also present challenges. While advancements are being made, effective and economically viable solutions for all types of mining waste are still under development. Finding cost-effective methods to extract valuable components from complex waste matrices remains an ongoing research focus. Furthermore, socio-political factors and public perception can act as restraints. Opposition from local communities to waste disposal sites or perceived environmental risks can lead to project delays or outright rejection, impacting the implementation of necessary waste management infrastructure.

The mining and metallurgical waste management market is poised for significant dominance by specific regions and segments, driven by a confluence of resource availability, regulatory frameworks, and industrial activity.

Dominant Segments:

Dominant Regions/Countries:

The synergy between the dominant segments and regions creates a dynamic market where the application of advanced technologies in metal recovery and metallurgical waste processing, within the regulatory and resource-rich environments of countries like Australia, China, and North America, will define the leading edge of the mining and metallurgical waste management industry for the foreseeable future.

Several key factors are acting as powerful catalysts for growth within the mining and metallurgical waste management industry. The increasing scarcity and declining grades of easily accessible mineral deposits are compelling companies to explore more efficient methods for extracting value from waste streams. Furthermore, advances in sensor technology, automation, and data analytics are enabling more precise identification and separation of valuable materials within waste, making resource recovery more economically viable. The growing emphasis on ESG (Environmental, Social, and Governance) principles by investors and stakeholders is also a significant catalyst, pushing companies to adopt more sustainable waste management practices to enhance their corporate reputation and secure funding. Finally, government incentives and supportive policies aimed at promoting a circular economy and reducing environmental pollution are further stimulating investment and innovation in this sector.

This comprehensive report offers an in-depth analysis of the global mining and metallurgical waste management market, meticulously dissecting trends, drivers, challenges, and opportunities. The report provides an authoritative overview of the market landscape throughout the Study Period of 2019-2033, with a keen focus on the Base Year of 2025 and the robust Forecast Period of 2025-2033. It delves into the economic implications, projecting market sizes in the billions and highlighting the substantial investments being made by industry giants. The report further enumerates leading players and significant recent developments, offering strategic insights for stakeholders seeking to navigate this dynamic sector. It examines key regions and segments, such as the Metal application and Metallurgy type, that are poised for significant growth, and analyzes the underlying forces propelling this expansion while also acknowledging the critical restraints that must be addressed for sustained progress.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.63% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.63%.

Key companies in the market include BHP Group, Rio Tinto, Vale, Glencore, Anglo American, Antofagasta, China Shenhua Energy., Veolia Environnement, SUEZ, Metso, MMC Norilsk Nickel, Teck, Cleanaway Waste Management, Newmont Corporation, Tetra Tech.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Mining and Metallurgical Waste Management," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Mining and Metallurgical Waste Management, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.