1. What is the projected Compound Annual Growth Rate (CAGR) of the Military Maritime Optronics?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Military Maritime Optronics

Military Maritime OptronicsMilitary Maritime Optronics by Type (/> Multispectral, Hyperspectral), by Application (/> Surface Vessels, Submarine), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

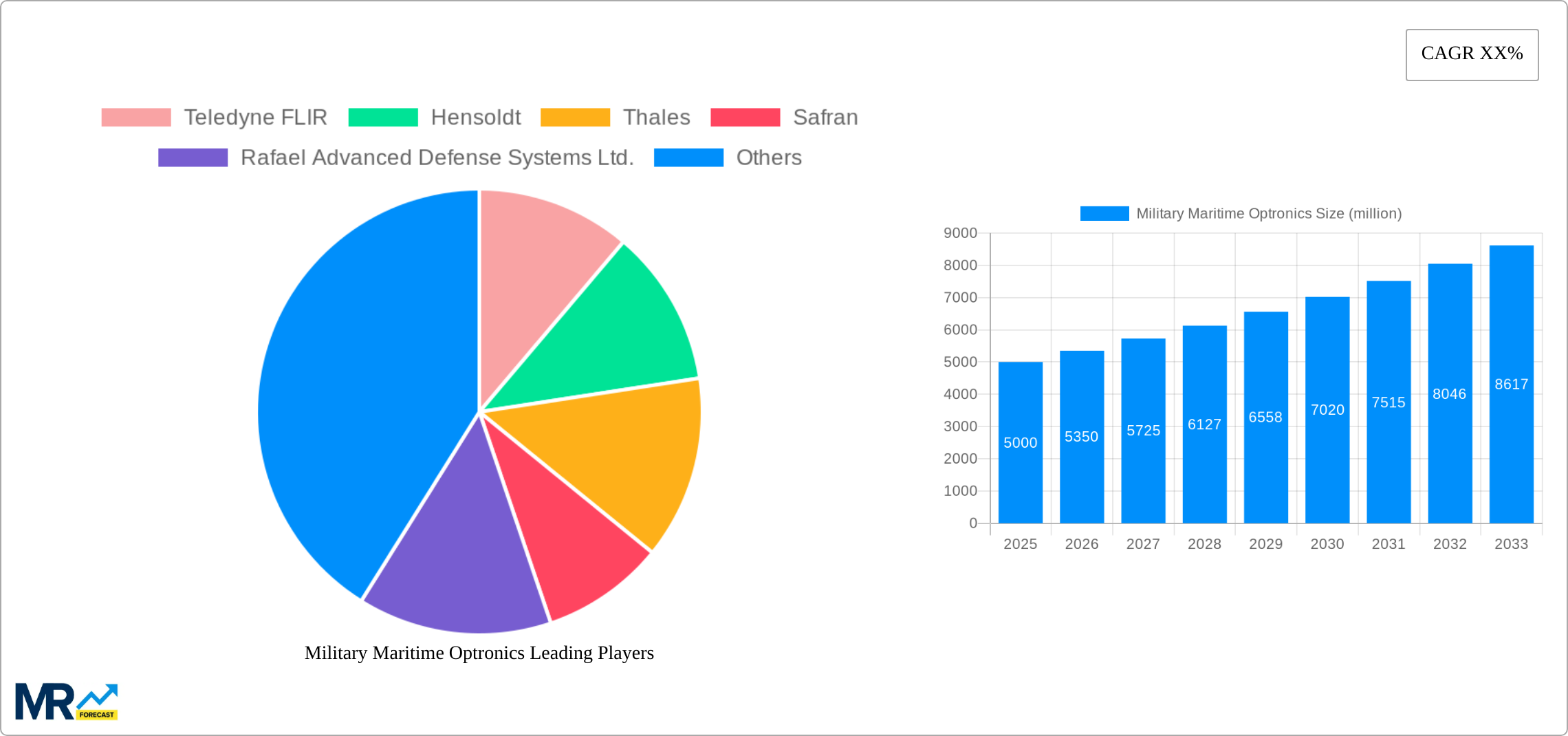

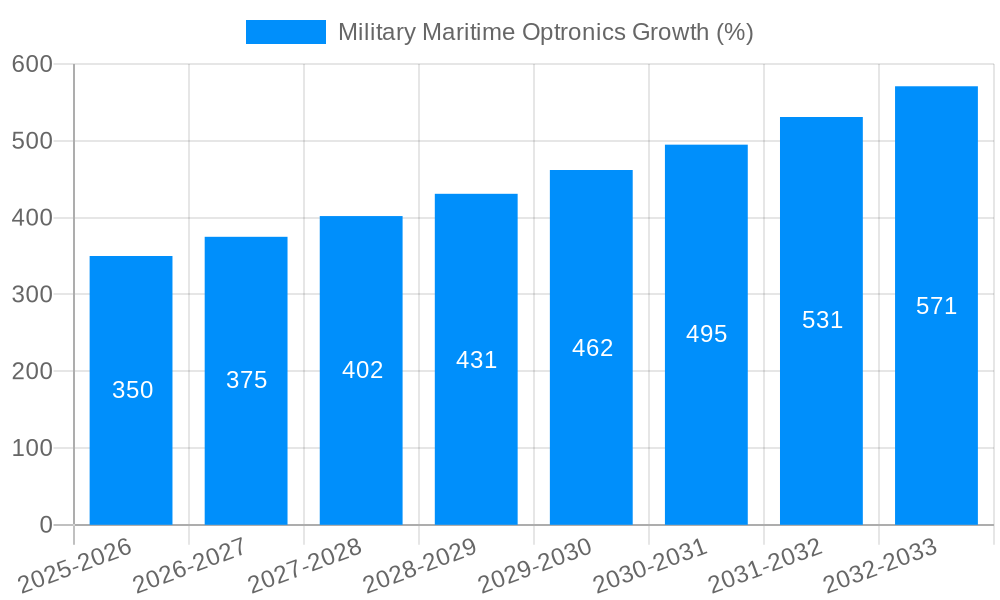

The global military maritime optronics market is experiencing robust growth, driven by increasing defense budgets worldwide and the escalating need for advanced surveillance and targeting systems in naval operations. The market, estimated at $5 billion in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7% from 2025 to 2033, reaching a value exceeding $9 billion by 2033. This expansion is fueled by several key factors, including the growing adoption of unmanned underwater vehicles (UUVs) and autonomous surface vessels, which necessitate sophisticated optronic systems for navigation, target acquisition, and situational awareness. Furthermore, the rising demand for improved night vision capabilities, enhanced image stabilization, and advanced sensor fusion technologies is significantly contributing to market growth. The integration of artificial intelligence (AI) and machine learning (ML) in optronic systems is also a significant trend, enabling automated target recognition and improved decision-making in challenging maritime environments.

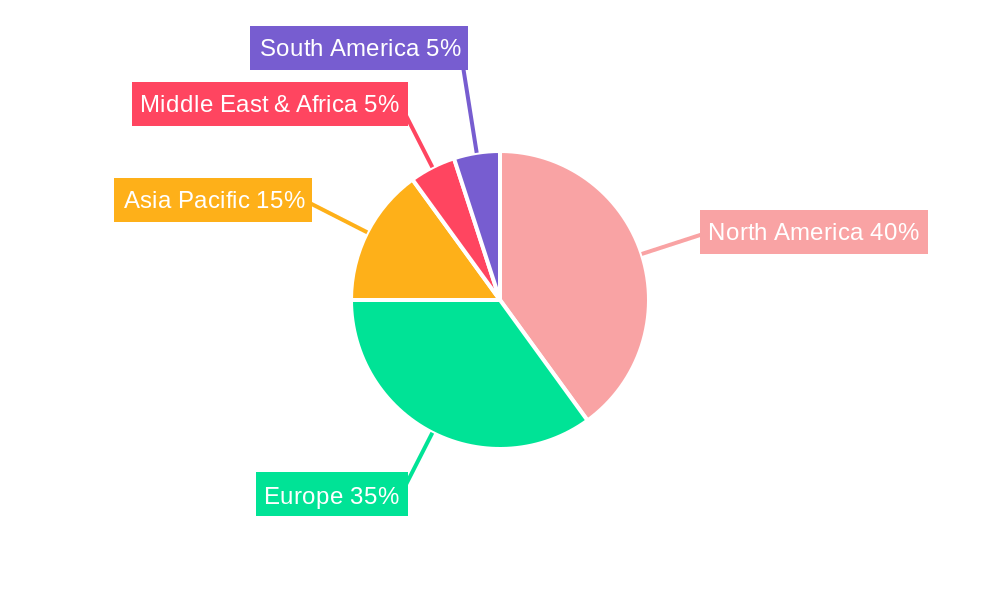

Competition within the market is fierce, with major players such as Teledyne FLIR, Hensoldt, Thales, Safran, and several other prominent defense contractors vying for market share. The market is segmented by technology (multispectral and hyperspectral) and application (surface vessels and submarines). Hyperspectral imaging, offering superior target identification and classification capabilities, is gaining traction, albeit at a higher cost than multispectral systems. The geographic distribution of the market is largely concentrated in North America and Europe, driven by substantial defense expenditures and technologically advanced navies in these regions. However, the Asia-Pacific region is expected to emerge as a significant growth market, fueled by increased military modernization efforts and naval expansion in countries such as China and India. Restraints to growth include the high cost of advanced optronic systems and the complexity involved in integrating these systems into existing naval platforms. Nevertheless, the long-term outlook for the military maritime optronics market remains positive, underpinned by consistent technological advancements and the enduring need for superior maritime surveillance and combat capabilities.

The military maritime optronics market is experiencing robust growth, driven by escalating geopolitical tensions and the increasing need for advanced surveillance and targeting systems across naval fleets globally. The market, valued at $XXX million in 2025, is projected to reach $XXX million by 2033, exhibiting a significant Compound Annual Growth Rate (CAGR) throughout the forecast period (2025-2033). This expansion is fueled by several factors, including the adoption of more sophisticated technologies like multispectral and hyperspectral imaging, a greater emphasis on unmanned systems integration, and the continuous modernization of existing naval platforms. The historical period (2019-2024) showcased substantial growth, laying the groundwork for the even more impressive expansion predicted for the coming decade. Key market insights reveal a strong preference for systems offering enhanced range, resolution, and all-weather operational capabilities. Furthermore, the demand for miniaturization and reduced SWaP (Size, Weight, and Power) is also driving innovation, particularly in the context of integrating optronics into smaller vessels and unmanned underwater vehicles (UUVs). The increasing focus on cybersecurity within military systems is another significant factor affecting the market landscape, influencing the design and implementation of secure and robust optronics solutions. Competition among key players is fierce, with companies continually striving to develop and deliver advanced products that cater to the evolving needs of modern navies. This competition fosters technological advancements and pushes down prices, benefiting end-users in the long run.

Several factors are propelling the growth of the military maritime optronics market. Firstly, the rising demand for enhanced situational awareness is a primary driver. Navies worldwide are seeking superior observation capabilities to detect and track threats effectively, including submarines, surface vessels, and airborne assets, in various environmental conditions. The development and deployment of increasingly sophisticated optronic systems directly address this need. Secondly, technological advancements are significantly contributing to market expansion. The development of high-resolution sensors, advanced image processing algorithms, and improved data fusion techniques are continuously enhancing the performance and capabilities of maritime optronics systems. Thirdly, the growing adoption of unmanned systems is also boosting market growth. Unmanned surface vehicles (USVs) and unmanned underwater vehicles (UUVs) rely heavily on optronics for navigation, target acquisition, and reconnaissance, driving demand for compact, reliable, and robust optronic systems. Finally, government investments in defense modernization programs are playing a crucial role in driving market expansion. Many countries are investing significantly in upgrading their naval fleets and incorporating cutting-edge technologies, including advanced optronics, to enhance their maritime defense capabilities.

Despite the positive growth outlook, several challenges and restraints impact the military maritime optronics market. High initial investment costs for advanced optronic systems can pose a barrier to entry for some nations, particularly smaller ones with limited defense budgets. This is compounded by the continuous need for software and hardware upgrades to maintain operational effectiveness against evolving threats. Furthermore, the harsh maritime environment presents significant challenges to the design and operation of optronic systems. These systems need to be robust enough to withstand extreme weather conditions, saltwater corrosion, and vibrations. Ensuring reliable operation in these challenging conditions often requires the use of specialized, high-cost materials and construction techniques. The complexities of integrating optronic systems with other naval platforms and systems can also present significant engineering and logistical hurdles. Finally, the need to balance performance with size, weight, and power (SWaP) constraints requires continuous innovation and development of advanced miniaturization techniques. These challenges necessitate careful planning, robust testing, and close collaboration between system integrators and end-users.

The North American and European regions are expected to dominate the military maritime optronics market throughout the forecast period. These regions house major defense contractors and possess significant naval capabilities, driving considerable demand for advanced optronic systems. The Asia-Pacific region is also anticipated to experience substantial growth, due to increased military spending and modernization programs in countries like China, India, and Japan.

Dominant Segment: The Multispectral segment is projected to hold a significant market share due to its versatility and cost-effectiveness compared to hyperspectral systems. Multispectral systems can provide crucial information for a wide range of applications, including target identification, surveillance, and navigation. The ability to differentiate various materials and features under diverse lighting conditions makes multispectral systems highly attractive to naval forces. However, the Hyperspectral segment is anticipated to demonstrate strong growth in the coming years, driven by advancements in sensor technology and the need for more detailed spectral analysis in specific scenarios, such as mine detection and environmental monitoring. While currently a smaller segment, its precision and detailed capabilities will propel it to higher market share as applications become more sophisticated.

Dominant Application: The Surface Vessels application segment currently holds the largest market share, given the significant number of surface ships in operation worldwide. These vessels are equipped with various optronic systems for navigation, surveillance, and combat. However, the Submarine application segment is projected to grow at a faster rate in the coming years. Submarines require advanced optronic systems for underwater navigation, target detection, and communication in very challenging conditions, driving demand for sophisticated and high-performance systems capable of operating in low-light and turbid waters.

The paragraph below explains why the multispectral/ surface vessel combination dominates:

The combination of multispectral sensors deployed on surface vessels currently dominates the market due to its cost-effectiveness and wide range of applications. Multispectral systems offer a good balance between information gathering and affordability, making them suitable for integration onto a variety of surface vessels, from smaller patrol boats to large aircraft carriers. The information provided by multispectral imaging is crucial for many naval operations, including navigation, surveillance, target acquisition, and damage assessment, contributing to its wide adoption. While the future looks promising for the hyperspectral segment and submarine applications, the multispectral/ surface vessel combination is expected to remain dominant throughout the forecast period, due to its mature technology, cost-effectiveness, and widespread adoption by naval forces globally.

Several factors are acting as catalysts for growth in the military maritime optronics industry. These include increasing government investments in defense modernization, technological advancements leading to enhanced system performance and reliability, the rising adoption of unmanned systems in naval operations, and growing awareness of the importance of maritime domain awareness. Furthermore, the development of improved software and data analytics capabilities for processing and interpreting the information gathered by optronic systems is also fueling market growth.

This report offers a comprehensive analysis of the military maritime optronics market, providing valuable insights into market trends, drivers, restraints, and future growth opportunities. It includes detailed market sizing and forecasting, segment-level analysis, competitive landscape mapping, and a review of key technological developments. The report's in-depth analysis empowers businesses and stakeholders to make strategic decisions, identify emerging investment opportunities, and navigate the complexities of this rapidly evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Teledyne FLIR, Hensoldt, Thales, Safran, Rafael Advanced Defense Systems Ltd., Elbit Systems, BAE Systems, Leonardo, Safran, Israel Aerospace Industries, Aselsan, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Military Maritime Optronics," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Military Maritime Optronics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.