1. What is the projected Compound Annual Growth Rate (CAGR) of the Military and Aerospace Sensors?

The projected CAGR is approximately 4.9%.

Military and Aerospace Sensors

Military and Aerospace SensorsMilitary and Aerospace Sensors by Type (/> Intelligence and Reconnaissance Systems, Communication and Navigation, Electronic Warfare, Command Control, Others), by Application (/> Land, Airborne, Naval, Space), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

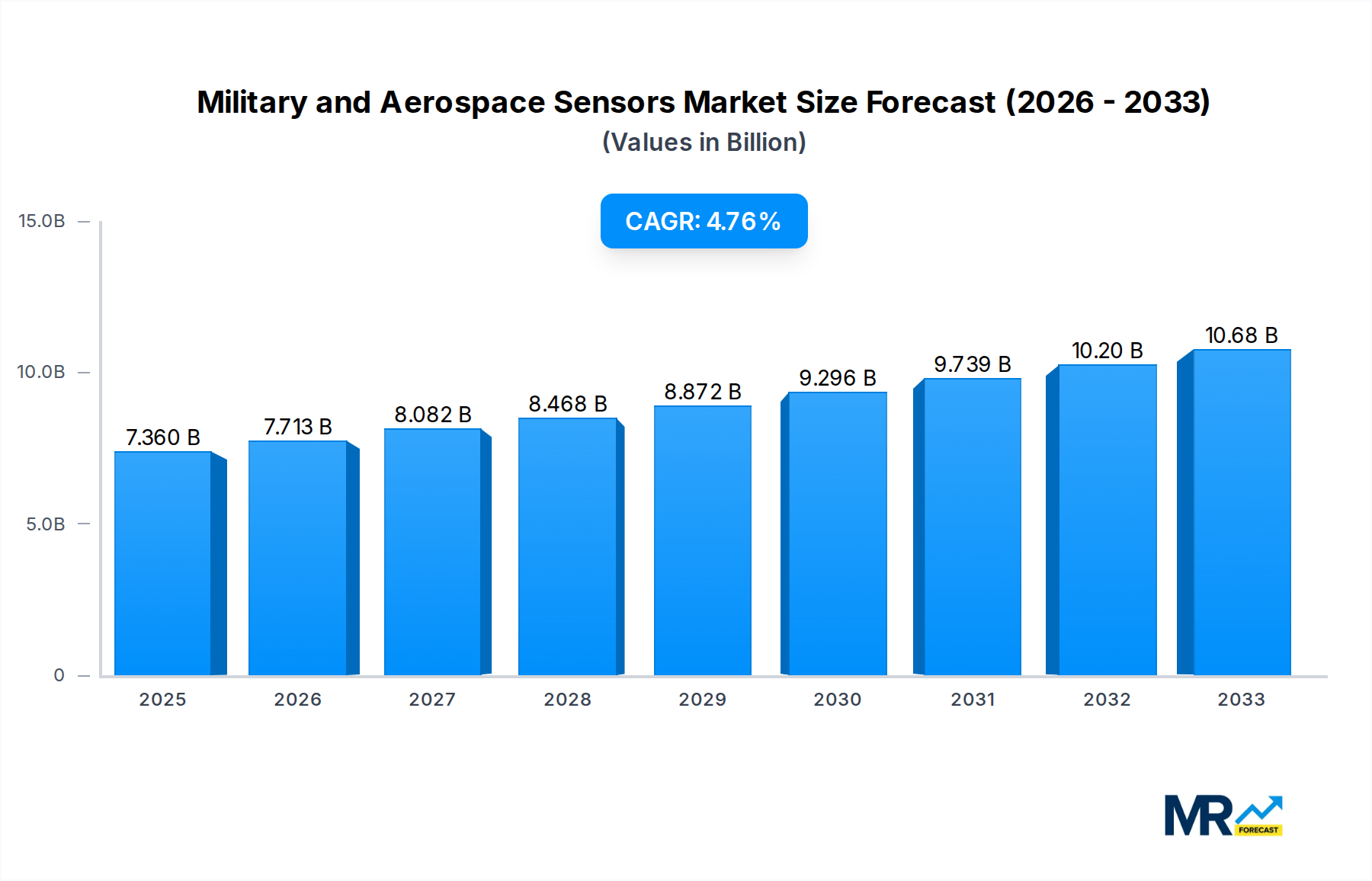

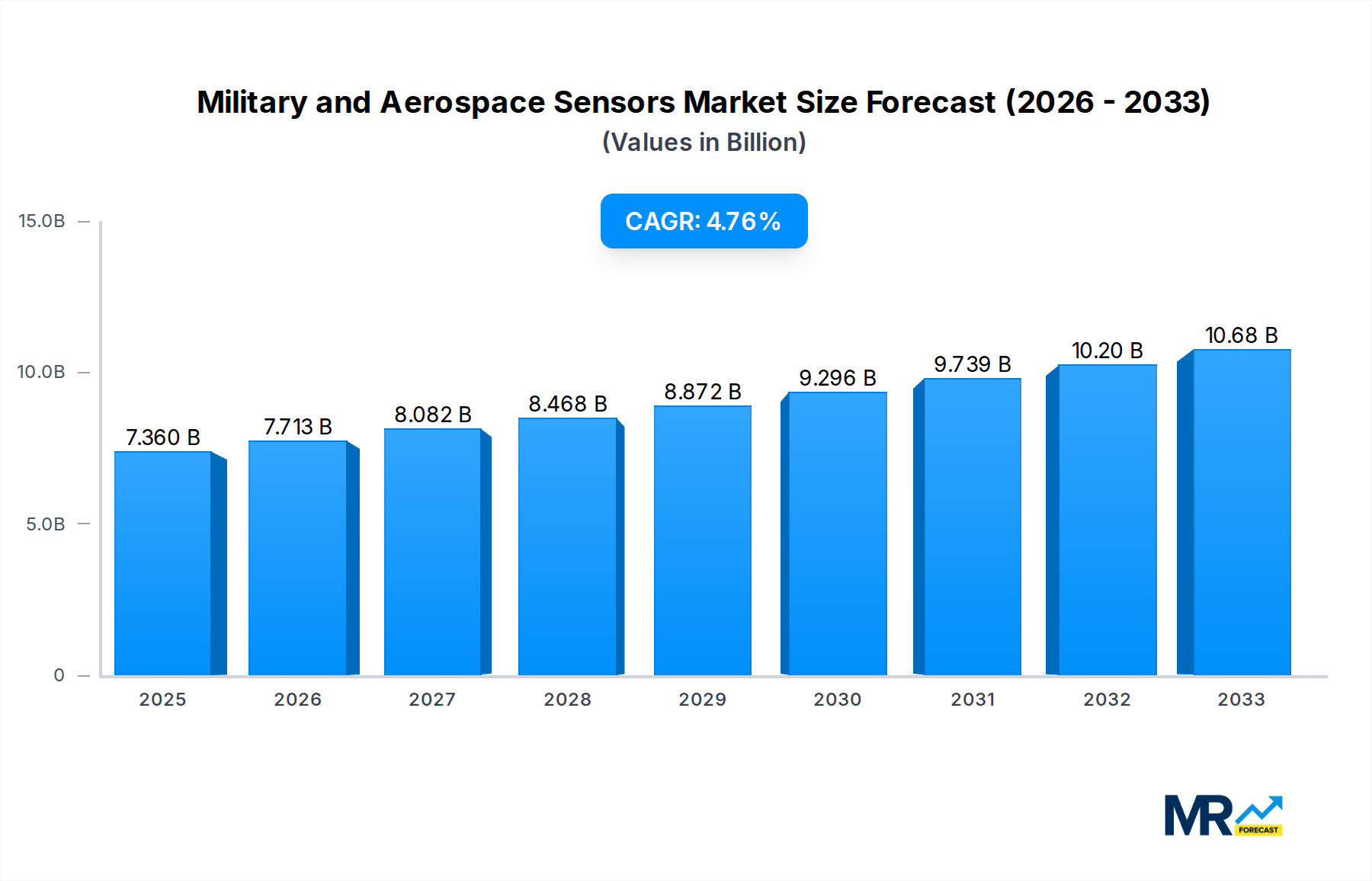

The global Military and Aerospace Sensors market is poised for robust expansion, projected to reach a substantial USD 7.36 billion by 2025. This growth trajectory is underpinned by a Compound Annual Growth Rate (CAGR) of 4.9% throughout the study period, indicating sustained and significant market momentum. The escalating geopolitical tensions worldwide are a primary driver, compelling governments to enhance their defense capabilities and invest heavily in advanced sensor technologies. These sensors are crucial for intelligence gathering, surveillance, reconnaissance, and enabling effective command and control operations across land, airborne, naval, and space domains. Furthermore, the ongoing technological advancements in areas like miniaturization, improved accuracy, and enhanced data processing are fueling the adoption of sophisticated sensor solutions in both new platforms and upgrades of existing systems, thereby stimulating market demand.

The market is characterized by a dynamic landscape with diverse segments catering to specific operational needs. Intelligence and Reconnaissance Systems, Communication and Navigation, Electronic Warfare, and Command Control represent key application areas, each contributing to the overall market value. The continuous evolution of warfare tactics, including the rise of cyber warfare and the need for real-time situational awareness, further accentuates the importance of these sensor technologies. While the market exhibits strong growth, certain restraints such as high development costs for cutting-edge technologies and stringent regulatory compliances can present challenges. However, the persistent emphasis on modernization programs by defense forces globally, coupled with increasing investments in research and development by leading companies like Honeywell, Thales Group, and Lockheed Martin, are expected to outweigh these limitations, ensuring a positive outlook for the Military and Aerospace Sensors market.

Here's a unique report description for Military and Aerospace Sensors, incorporating the provided values, company names, segments, and development years:

This comprehensive report delves into the dynamic Military and Aerospace Sensors market, projecting significant growth and transformation over the Study Period (2019-2033). The market, valued in the billions of USD, is poised for an upward trajectory, with the Base Year (2025) serving as a crucial reference point for understanding current dynamics and future potential. The Forecast Period (2025-2033) will witness an acceleration in adoption and innovation, building upon the trends observed during the Historical Period (2019-2024).

The Military and Aerospace Sensors market is experiencing a paradigm shift, driven by the relentless pursuit of enhanced situational awareness, precision targeting, and secure communications in increasingly complex operational environments. XXX Billion USD represents the estimated market size for 2025, a figure set to burgeon significantly as technological advancements and geopolitical imperatives converge. A key trend is the integration of Artificial Intelligence (AI) and Machine Learning (ML) into sensor platforms, enabling real-time data processing, anomaly detection, and predictive maintenance. This not only improves operational efficiency but also reduces the cognitive load on human operators. The miniaturization and increased sophistication of sensors are also paramount, allowing for deployment on a wider array of platforms, from ubiquitous drones to advanced fighter jets and stealthy naval vessels. Furthermore, the growing emphasis on network-centric warfare necessitates interoperable sensor systems that can seamlessly share information across diverse domains. Cybersecurity of sensor data is also emerging as a critical consideration, with the industry investing heavily in robust encryption and secure transmission protocols to safeguard sensitive intelligence. The demand for multi-spectral and hyper-spectral imaging sensors is also on the rise, offering unparalleled capabilities in target identification and environmental analysis. As the global security landscape continues to evolve, characterized by the rise of asymmetric warfare and the proliferation of advanced threats, the need for cutting-edge sensing technologies will only intensify, further solidifying the growth trajectory of this vital market.

Several potent forces are collectively propelling the Military and Aerospace Sensors market forward. The escalating geopolitical tensions and the modernization of defense arsenals across major nations are primary drivers. Governments worldwide are prioritizing investments in advanced sensor technologies to maintain a technological edge and counter emerging threats. The increasing adoption of unmanned systems, ranging from tactical drones to autonomous aerial vehicles (UAVs) and unmanned naval vessels, creates a substantial demand for specialized sensors for navigation, surveillance, and payload delivery. Furthermore, the growing emphasis on Intelligence, Surveillance, and Reconnaissance (ISR) capabilities, crucial for understanding adversary actions and maintaining battlefield dominance, directly fuels the need for sophisticated optical, electronic, and acoustic sensors. The ongoing digital transformation within the defense sector, characterized by the move towards network-centric operations and the integration of AI/ML, necessitates advanced sensors that can provide high-fidelity, actionable data for automated decision-making and enhanced situational awareness. Finally, the civilian aerospace sector's own advancements, including the development of more efficient aircraft and the expansion of space exploration, also contribute to the market's growth through shared technological innovations and evolving safety and navigation requirements.

Despite the robust growth prospects, the Military and Aerospace Sensors market faces several significant challenges and restraints. The substantial cost associated with research, development, and manufacturing of highly advanced sensors presents a considerable barrier, particularly for smaller nations or defense contractors with limited budgets. The stringent regulatory frameworks and lengthy approval processes inherent in the defense and aerospace industries can also impede the rapid deployment of new technologies. Furthermore, the increasing complexity of sensor systems raises concerns about integration challenges, interoperability issues between different platforms and systems, and the need for highly skilled personnel for operation and maintenance. The evolving nature of threats also necessitates constant innovation, leading to a continuous arms race in sensing capabilities, which can strain resources. Supply chain vulnerabilities, especially for specialized components and rare earth materials, can also disrupt production and increase lead times. Finally, the growing concern over data security and the potential for cyberattacks on sensor networks pose a significant risk, requiring continuous investment in robust cybersecurity measures and data protection strategies to mitigate these threats.

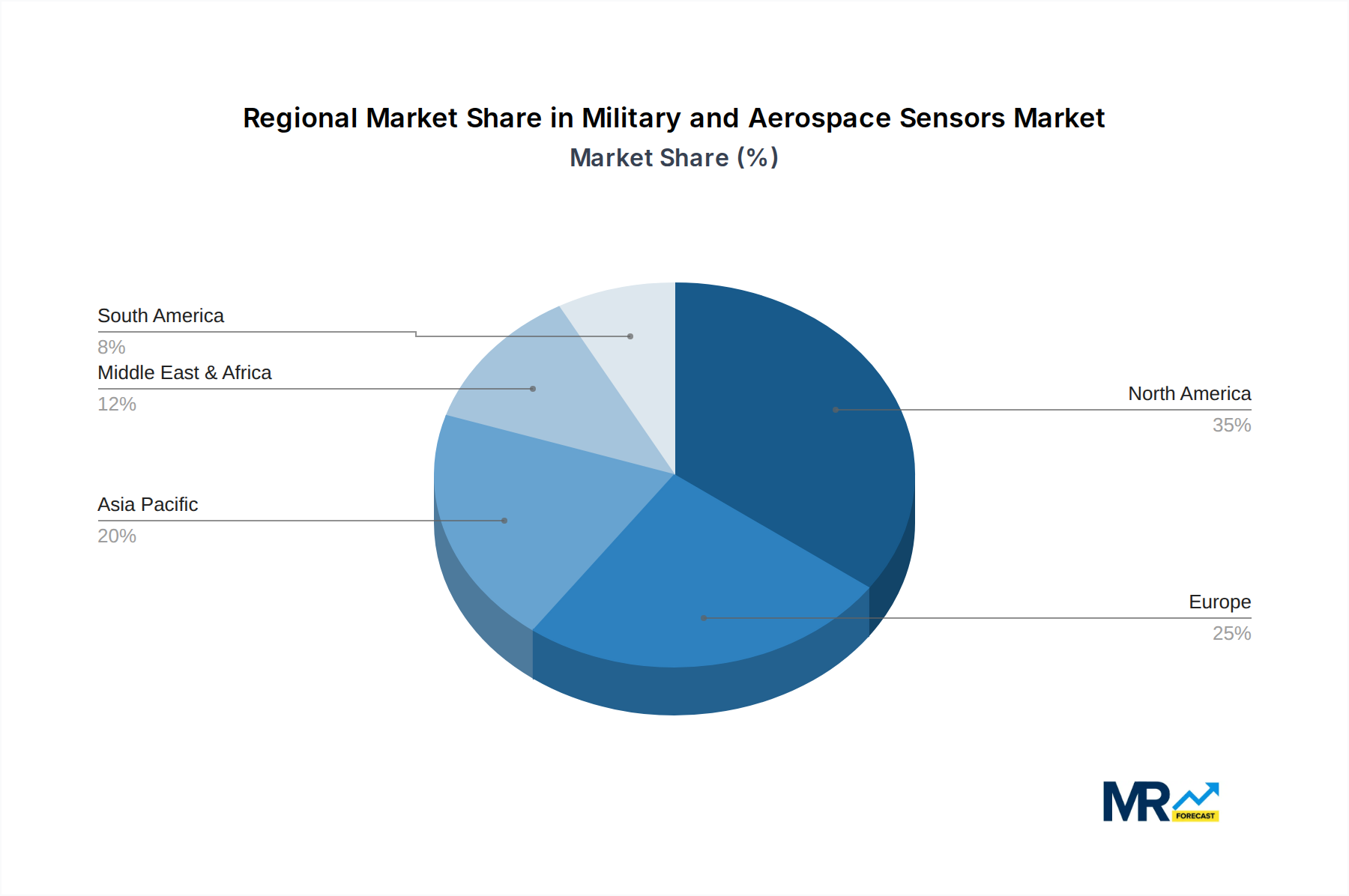

The Military and Aerospace Sensors market is characterized by the dominance of specific regions and segments, driven by defense spending, technological innovation, and geopolitical imperatives.

Dominant Regions/Countries:

Dominant Segments:

The synergy between these dominant regions and segments creates a powerful market dynamic. For instance, the US's focus on advanced ISR capabilities for its airborne platforms directly drives innovation and demand. Similarly, China's push for indigenous defense manufacturing in its rapidly expanding military leverages advancements in airborne sensors and intelligence systems. The strategic importance of airborne ISR in modern conflict and surveillance ensures this application will continue to be a focal point for sensor development and deployment, supported by robust investments from leading global powers.

The Military and Aerospace Sensors industry is fueled by several key growth catalysts. The ongoing global defense modernization efforts and the increasing geopolitical instability are compelling nations to invest in advanced sensing technologies to maintain a strategic advantage. The proliferation of unmanned aerial vehicles (UAVs) and autonomous systems across both military and civilian applications significantly amplifies the demand for sophisticated navigation, imaging, and situational awareness sensors. Furthermore, the imperative to enhance Intelligence, Surveillance, and Reconnaissance (ISR) capabilities, particularly in complex and contested environments, drives innovation in areas like multi-spectral imaging and advanced radar. The digital transformation within defense, emphasizing network-centric operations and AI integration, creates a demand for sensors that can provide actionable, real-time data for enhanced decision-making.

This report provides a thorough examination of the Military and Aerospace Sensors market, offering deep insights into market dynamics, technological advancements, and future projections. It meticulously analyzes the interplay of key driving forces, such as escalating geopolitical tensions and the rapid expansion of unmanned systems, alongside critical challenges like high development costs and regulatory hurdles. The report details the strategic dominance of regions like North America and the Asia-Pacific, alongside the paramount importance of segments like Intelligence and Reconnaissance Systems and the Airborne application. With extensive coverage of leading players and significant developments through 2033, this comprehensive analysis is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving landscape of military and aerospace sensing technologies.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.9%.

Key companies in the market include UTC Aerospace systems, Meggitt PLC, Eaton Corporation, Zodiac Aerospace, Crane Aerospace, Viooa Imaging Technology, Rockwest Solution, Vectornav Technologies LLC., Microflown Anvisa, LLC, Innovative Sensor Technology IST AG, TE Connectivity, Excelitas, Sensata Technologies, Inc, Ametek, Sentech, Honeywell International Inc, Thales Group, Raytheon Company, Lockheed Martin Corporation, Safran Electronics & Defense, BAE Systems PLC.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Military and Aerospace Sensors," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Military and Aerospace Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.