1. What is the projected Compound Annual Growth Rate (CAGR) of the Military Aerospace Simulation and Training?

The projected CAGR is approximately XX%.

Military Aerospace Simulation and Training

Military Aerospace Simulation and TrainingMilitary Aerospace Simulation and Training by Type (Full Flight Simulator, Flight Training Device, Computer Based Training, World Military Aerospace Simulation and Training Production ), by Application (Fixed-wing Aircraft, Rotary-wing Aircraft, World Military Aerospace Simulation and Training Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

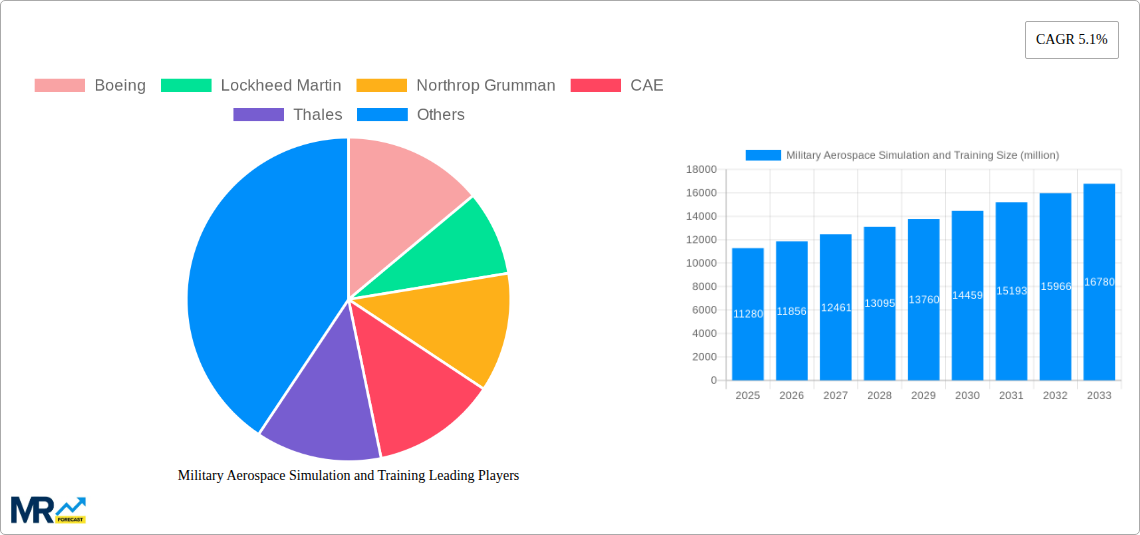

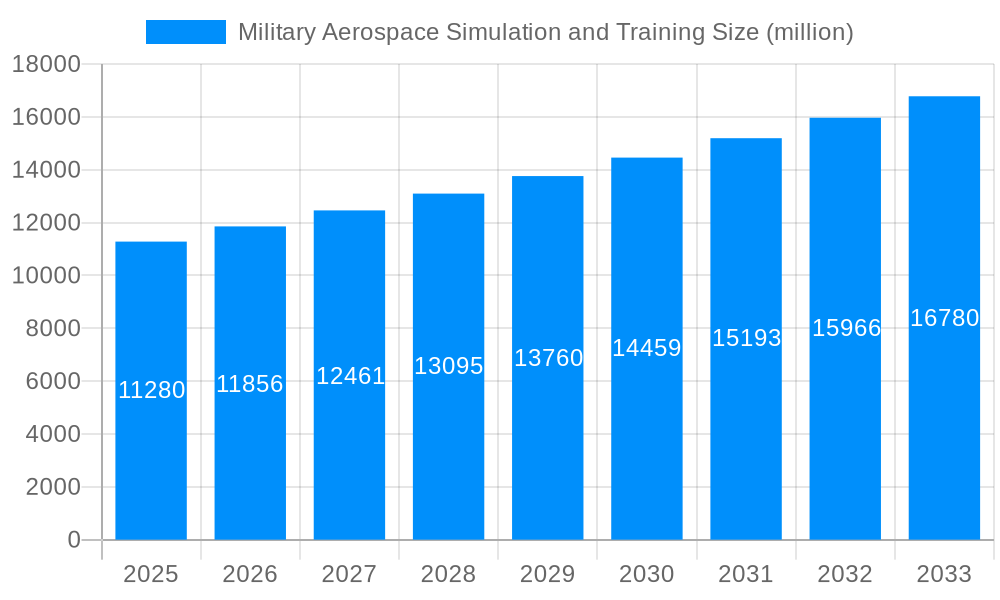

The global military aerospace simulation and training market, valued at approximately $15.94 billion in 2025, is poised for significant growth over the next decade. This expansion is driven by several key factors. Firstly, increasing defense budgets worldwide, particularly in regions experiencing geopolitical instability, are fueling demand for advanced training solutions. Secondly, the growing complexity of modern military aircraft and weapons systems necessitates sophisticated simulation technologies to ensure effective pilot and crew training. Technological advancements, such as the integration of artificial intelligence (AI) and virtual reality (VR) into simulators, are further enhancing training effectiveness and realism, contributing to market growth. Furthermore, the shift towards more cost-effective and efficient training methodologies is favoring simulation over live-flight training, a key trend driving market expansion. Segments like full-flight simulators and computer-based training are experiencing rapid growth due to their versatility and scalability. The Asia-Pacific region is expected to witness substantial growth driven by increasing defense spending and modernization initiatives in countries like China and India.

However, market growth is not without its challenges. High initial investment costs associated with procuring and maintaining advanced simulators can act as a restraint, particularly for smaller nations with limited defense budgets. Additionally, the need for regular software and hardware updates to keep pace with technological advancements can represent a significant ongoing expense. Despite these restraints, the long-term prospects for the military aerospace simulation and training market remain strong, fueled by the continuous demand for highly skilled personnel within the military aerospace sector and the ongoing development of increasingly sophisticated training technologies. Major players such as Boeing, Lockheed Martin, and CAE are actively shaping market dynamics through innovation and strategic partnerships. Competitive landscape is characterized by technological advancements, strategic mergers and acquisitions, and regional market expansion plans.

The global military aerospace simulation and training market is experiencing robust growth, driven by escalating defense budgets worldwide and the increasing need for advanced training solutions. The market, valued at USD XXX million in 2025, is projected to reach USD XXX million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of X% during the forecast period (2025-2033). This expansion is fueled by a shift towards more realistic and immersive training environments, incorporating technologies like virtual reality (VR), augmented reality (AR), and artificial intelligence (AI). The historical period (2019-2024) witnessed significant advancements in simulation technology, particularly in the development of high-fidelity full-flight simulators and sophisticated training software. This trend is set to continue, with a growing emphasis on cost-effective training solutions such as computer-based training (CBT) and flight training devices (FTDs). The increasing complexity of modern military aircraft and weapons systems necessitates advanced simulation capabilities to ensure effective pilot and crew training. This includes the integration of live, virtual, and constructive (LVC) training environments for multi-domain operations, reflecting the evolving nature of modern warfare. Furthermore, the growing adoption of cloud-based training platforms allows for greater accessibility and scalability, reducing training costs and improving training efficiency. The market is witnessing a substantial increase in the demand for training programs tailored to specific mission scenarios, further contributing to its growth. Competition among major players is intense, resulting in continuous innovation and the development of increasingly sophisticated simulation systems.

Several factors are driving the expansion of the military aerospace simulation and training market. The escalating geopolitical tensions and the need for maintaining combat readiness are paramount drivers. Governments across the globe are investing heavily in modernizing their defense forces, and a core component of this modernization is improving pilot and crew training. The transition to fifth-generation and beyond aircraft, along with the proliferation of sophisticated weapon systems, necessitates advanced training programs to ensure proficient handling of increasingly complex technologies. The high cost of real-world flight training makes simulation an attractive and cost-effective alternative, particularly for repetitive training exercises. Furthermore, simulation allows for risk-free training in high-stakes scenarios, mitigating the risk of accidents and injuries during live flight training. The integration of advanced technologies like VR, AR, and AI allows for more realistic and immersive training, enhancing learning outcomes and improving pilot proficiency. The growing adoption of LVC training, integrating live, virtual, and constructive elements, further enhances realism and allows for collaboration across multiple platforms and geographical locations. This facilitates effective joint training exercises and improves interoperability within allied forces.

Despite the strong growth potential, several challenges and restraints could hinder market expansion. The high initial investment cost associated with developing and implementing advanced simulation systems is a significant hurdle, particularly for smaller nations with limited defense budgets. The need for continuous updates and maintenance to keep up with technological advancements also presents a challenge. The complexity of integrating different simulation systems and ensuring interoperability across various platforms can pose significant logistical and technical hurdles. Maintaining the realism and accuracy of simulation models to reflect the dynamic nature of military operations is crucial, and achieving this requires ongoing research and development. Furthermore, there is an ongoing need to bridge the gap between simulated training and real-world scenarios. Finding qualified personnel to develop, implement, and maintain these sophisticated systems is also a critical challenge. The cybersecurity risks associated with sophisticated simulation systems necessitate robust security measures, adding to the overall cost and complexity.

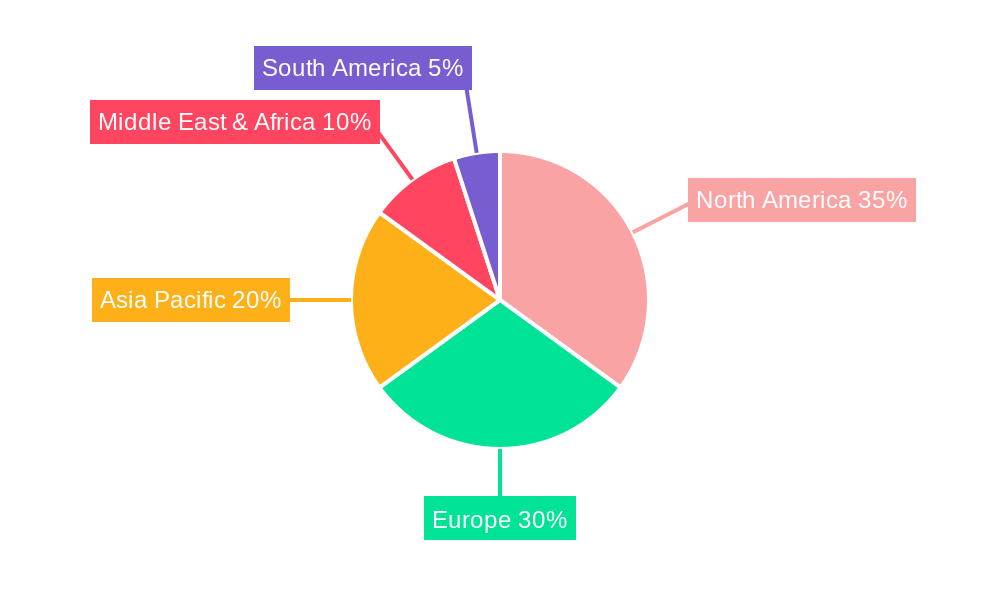

The North American region (United States and Canada) is anticipated to dominate the military aerospace simulation and training market throughout the forecast period. This is attributed to significant defense spending, the presence of major simulation technology developers and manufacturers such as Boeing, Lockheed Martin, and CAE, and the advanced technological capabilities of the region's armed forces.

Within segments, the Full Flight Simulator (FFS) segment is projected to hold the largest market share. The high fidelity and realistic environment offered by FFSs are crucial for advanced pilot training, particularly for complex aircraft like fighter jets and transport aircraft.

The Fixed-wing Aircraft application segment is also expected to dominate due to the large number of fixed-wing aircraft operated by military forces worldwide, necessitating extensive training programs.

The integration of advanced technologies, including AI, VR, AR, and cloud computing, is significantly accelerating the growth of the industry. These advancements enhance training realism, making it more effective and engaging. The increasing demand for cost-effective, scalable, and accessible training solutions also fuels market growth. Furthermore, the global focus on improving military readiness and interoperability, coupled with rising defense budgets, creates a robust environment for expansion.

This report provides a comprehensive analysis of the military aerospace simulation and training market, covering market size, growth trends, key players, and technological advancements. It offers valuable insights into the driving forces, challenges, and opportunities within this dynamic sector, enabling informed decision-making for stakeholders across the industry. The report's detailed segmentation analysis provides a granular understanding of market dynamics across different types of simulators, aircraft applications, and geographic regions. The forecast period extends to 2033, providing a long-term perspective on market evolution.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Boeing, Lockheed Martin, Northrop Grumman, CAE, Thales, FlightSafety, CSTS Dinamika, Kratos, L-3 Communications, Rockwell Collins, Textron, BAE Systems, Rheinmetall, Bluesky, Moreget, .

The market segments include Type, Application.

The market size is estimated to be USD 15940 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Military Aerospace Simulation and Training," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Military Aerospace Simulation and Training, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.