1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Dosimetry Equipment?

The projected CAGR is approximately 6.8%.

Medical Dosimetry Equipment

Medical Dosimetry EquipmentMedical Dosimetry Equipment by Type (TLD, OSL, RPL, Active Type, World Medical Dosimetry Equipment Production ), by Application (Clinic, Hospital, Scientific Research, Others, World Medical Dosimetry Equipment Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

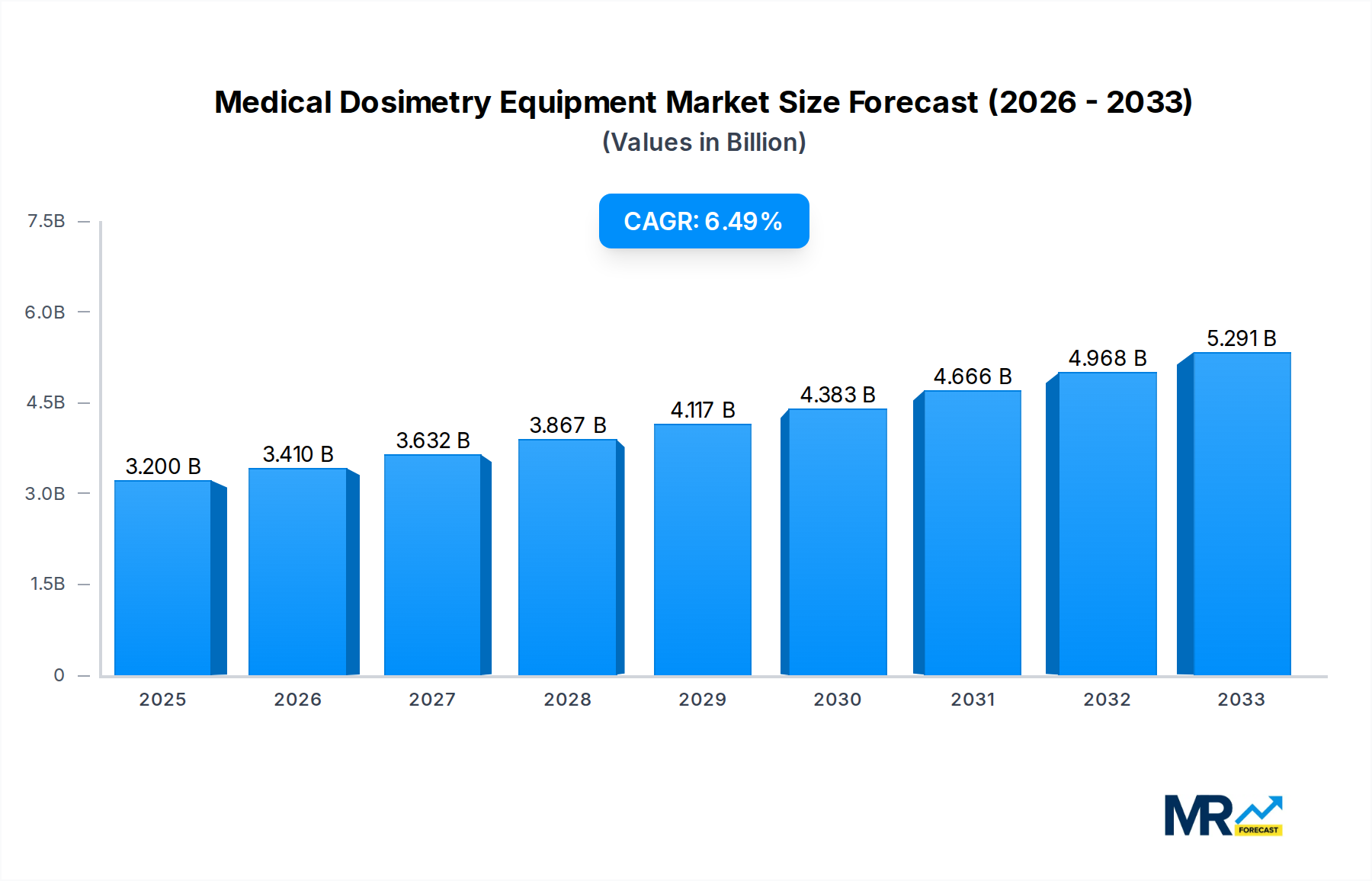

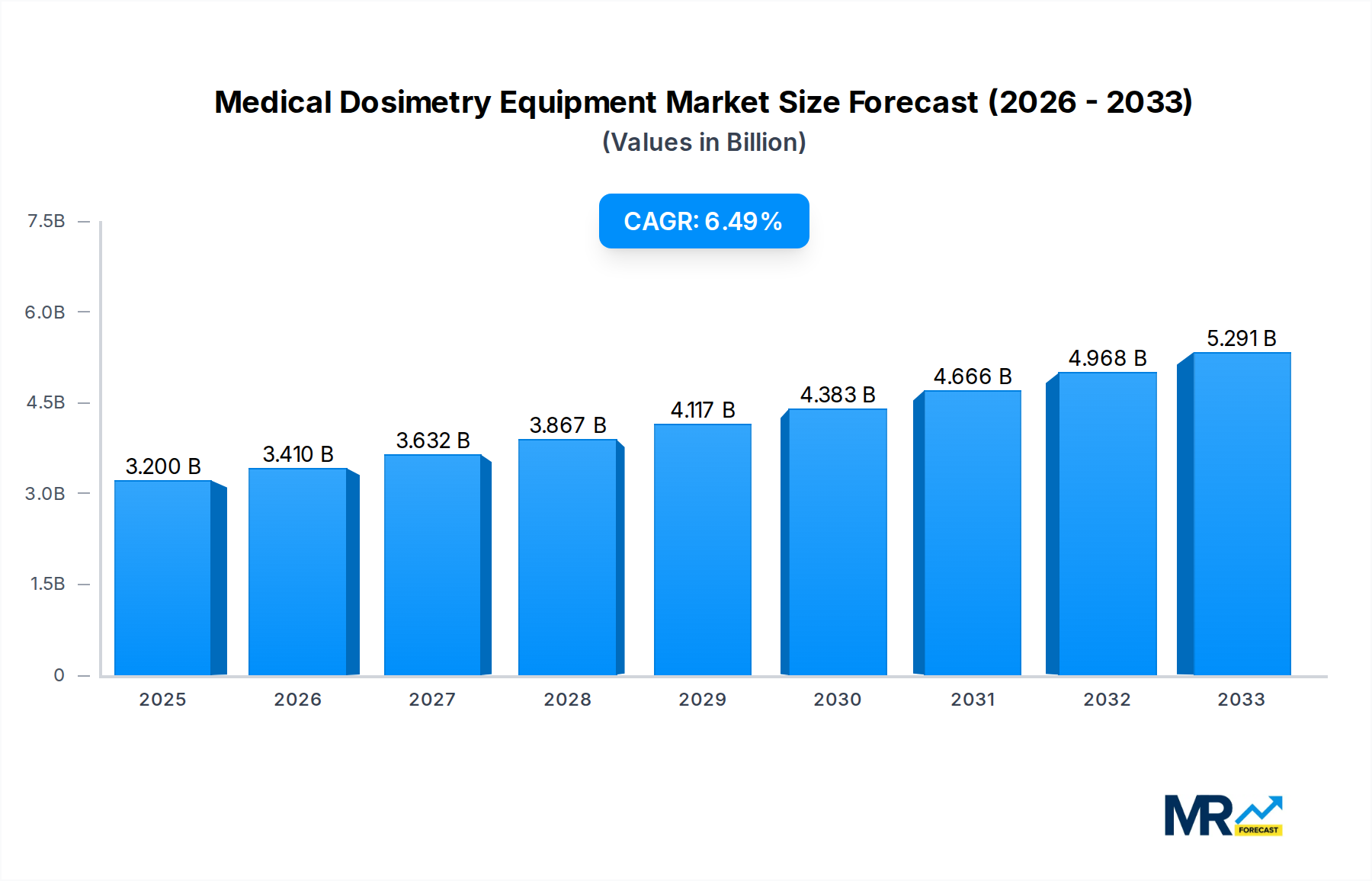

The global Medical Dosimetry Equipment market is poised for substantial growth, projected to reach an estimated USD 3.2 billion in 2025 and expand at a robust Compound Annual Growth Rate (CAGR) of 6.8% through 2033. This upward trajectory is primarily driven by the increasing incidence of cancer globally, necessitating advanced radiation therapy and diagnostic procedures. The growing demand for precise radiation dose measurement and management in oncology treatments is a critical factor fueling market expansion. Furthermore, technological advancements in dosimetry equipment, including the development of more accurate, portable, and user-friendly devices, are significantly contributing to market penetration across various healthcare settings. The rise in healthcare expenditure, coupled with government initiatives to improve cancer care infrastructure and patient outcomes, further underpins this positive market outlook.

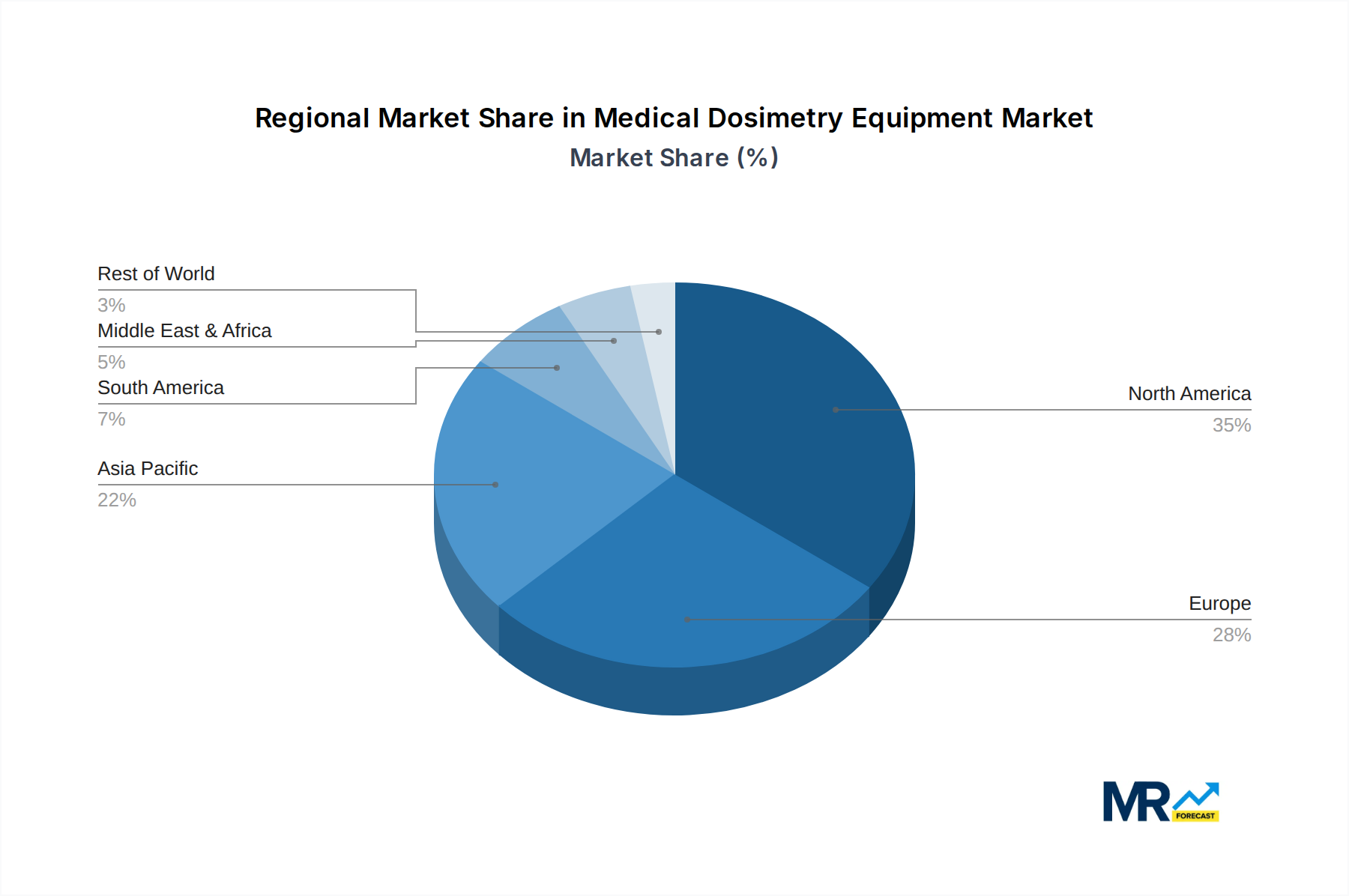

The market is segmented across different types of dosimetry equipment, including TLD, OSL, RPL, and Active Type, catering to diverse applications within clinics, hospitals, and scientific research facilities. The "World Medical Dosimetry Equipment Production" is a key indicator of this global demand. Geographically, North America currently leads the market, attributed to its advanced healthcare infrastructure, high adoption of new technologies, and significant investments in cancer research. However, the Asia Pacific region is expected to witness the fastest growth, driven by rapid advancements in healthcare, a burgeoning patient population, and increasing awareness about the importance of accurate dosimetry in radiation therapy. Restraints such as the high cost of sophisticated equipment and the need for skilled personnel to operate them may pose challenges, but the overarching trend points towards sustained and strong market expansion driven by an unwavering commitment to improving cancer treatment efficacy and patient safety.

This comprehensive report delves into the global medical dosimetry equipment market, providing an in-depth analysis of its trajectory from the historical period of 2019-2024 through to the projected forecast period of 2025-2033, with a base and estimated year of 2025. The market, projected to reach significant figures in the billions, is characterized by evolving technological advancements and increasing demand for precise radiation monitoring in healthcare and research settings. The report offers invaluable insights for stakeholders looking to understand current trends, driving forces, potential challenges, and future growth opportunities within this critical sector.

The global medical dosimetry equipment market is on a robust growth trajectory, fueled by an escalating demand for sophisticated radiation measurement and monitoring solutions across diverse healthcare applications. During the study period of 2019-2033, and particularly around the estimated year of 2025, the market is expected to witness a substantial expansion, with production values likely to surpass $7 billion globally. This growth is intricately linked to the increasing prevalence of cancer diagnoses and the subsequent rise in the utilization of radiation therapy, a cornerstone treatment modality. As radiotherapy techniques become more advanced, employing higher doses and more precise targeting, the need for accurate and reliable dosimetry equipment to monitor patient exposure and ensure treatment efficacy becomes paramount. Furthermore, the growing emphasis on occupational safety for healthcare professionals working with ionizing radiation in facilities like hospitals and clinics is a significant driver. Regulations are becoming more stringent, pushing for the adoption of advanced dosimetry systems that provide real-time monitoring and comprehensive data logging.

The market is also experiencing a pronounced shift towards more advanced and sophisticated types of dosimetry, moving beyond traditional methods. While Thermoluminescent Dosimetry (TLD) and Optically Stimulated Luminescence (OSL) dosimetry continue to hold significant market share due to their established reliability and cost-effectiveness, there is a discernible trend towards Active Type dosimeters. These devices offer real-time readings, enhanced portability, and often integrate with digital platforms for seamless data management and analysis, which are crucial for modern clinical workflows and research endeavors. The increasing adoption of Picture Archiving and Communication Systems (PACS) and Electronic Health Records (EHRs) within healthcare institutions is also indirectly fueling the demand for integrated dosimetry solutions that can seamlessly feed data into these systems. This integration enhances traceability, simplifies record-keeping, and supports more robust quality assurance protocols in radiation oncology.

Beyond clinical applications, the domain of scientific research, particularly in fields involving radiation biology, nuclear medicine, and environmental monitoring, is also contributing to market expansion. Researchers require highly sensitive and accurate dosimeters for experimental designs and validation. The exploration of new radiopharmaceuticals and advanced imaging techniques necessitates precise dosimetry for both efficacy and safety assessments. Moreover, the increasing awareness and regulatory focus on radiation protection in non-clinical settings, such as industrial radiography and nuclear power plants, although not the primary focus of this report, also contribute to the overall demand for dosimetry technologies, creating a broader ecosystem of innovation that can eventually translate into medical applications. The global production of medical dosimetry equipment, expected to reach a significant valuation by 2025, underscores the critical role these devices play in ensuring patient safety, optimizing treatment outcomes, and advancing scientific understanding of radiation's impact.

Several potent forces are synergistically propelling the global medical dosimetry equipment market forward, ensuring its continued expansion and technological evolution throughout the study period of 2019-2033, with a particular focus around the base year of 2025. Foremost among these is the increasing global incidence of cancer. As cancer rates rise, so does the demand for radiation therapy, the primary treatment modality for a significant portion of these diagnoses. This directly translates into a greater need for accurate and reliable medical dosimetry equipment to meticulously plan, deliver, and monitor radiation treatments, ensuring optimal efficacy while minimizing collateral damage to healthy tissues. The pursuit of personalized medicine and advanced treatment techniques like Intensity-Modulated Radiation Therapy (IMRT) and Volumetric Modulated Arc Therapy (VMAT) necessitates highly sophisticated dosimetry systems capable of measuring complex dose distributions with exceptional precision.

Another significant driver is the escalating focus on patient safety and radiation protection. Regulatory bodies worldwide are imposing stricter guidelines and standards for radiation exposure monitoring in healthcare settings. This heightened regulatory scrutiny compels hospitals and clinics to invest in advanced dosimetry solutions that provide real-time data, comprehensive traceability, and robust quality assurance capabilities. The well-being of healthcare professionals who work with ionizing radiation is also a critical concern, leading to increased demand for personal dosimeters that accurately track occupational exposure. Furthermore, the advancements in medical imaging and diagnostic technologies that utilize radiation, such as PET-CT scans and SPECT imaging, are also contributing to the market's growth. These technologies require precise dosimetry for accurate interpretation and effective patient management.

The growing integration of digital technologies and data management in healthcare is also playing a pivotal role. The trend towards Electronic Health Records (EHRs) and Picture Archiving and Communication Systems (PACS) encourages the adoption of dosimetry equipment that can seamlessly integrate with these digital platforms. This integration streamlines workflows, enhances data accessibility, and facilitates more efficient analysis and reporting of radiation doses. Finally, continuous innovation in dosimetry technology itself, including the development of more sensitive, portable, and cost-effective solutions, acts as a continuous catalyst. Researchers and manufacturers are constantly striving to improve the accuracy, speed, and usability of dosimetry devices, making them more accessible and adaptable to a wider range of clinical and research applications.

Despite the robust growth prospects, the medical dosimetry equipment market faces several notable challenges and restraints that can temper its expansion and influence market dynamics throughout the study period of 2019-2033, with the estimated year of 2025 serving as a key point of analysis. One of the primary impediments is the high initial cost of advanced dosimetry equipment. Sophisticated systems, particularly those incorporating real-time monitoring and digital integration capabilities, represent a significant capital investment for healthcare institutions, especially smaller clinics or those in developing regions where budgetary constraints are more pronounced. This cost factor can slow down the adoption rate of the latest technologies, leading to a disparity in access to cutting-edge dosimetry solutions.

Another significant challenge is the need for specialized training and expertise. Operating and interpreting data from advanced dosimetry equipment requires skilled personnel. Healthcare facilities often face difficulties in recruiting and retaining qualified medical dosimetrists and radiation physicists. The lack of adequate training programs or the cost associated with such training can hinder the effective utilization of the equipment, thereby limiting its overall impact. Furthermore, the complexity of regulatory compliance can also pose a challenge. Navigating the intricate web of national and international regulations pertaining to radiation safety and dosimetry equipment can be time-consuming and resource-intensive for manufacturers and end-users alike. Keeping pace with evolving standards and ensuring adherence can be a constant struggle.

The slow adoption rate of new technologies in established healthcare systems can also act as a restraint. The healthcare sector is often characterized by a cautious approach to adopting new technologies due to concerns about reliability, validation, and integration with existing infrastructure. This can create a lag between technological advancements and their widespread implementation in clinical practice. Moreover, interoperability issues between different dosimetry devices and existing hospital information systems can present a significant hurdle. For seamless data integration and efficient workflow management, dosimetry equipment needs to communicate effectively with other IT systems, and a lack of standardized protocols can impede this process. Finally, reimbursement policies for dosimetry services and equipment can also influence market growth. Inadequate or inconsistent reimbursement rates may discourage healthcare providers from investing in the most advanced and potentially more expensive dosimetry solutions.

Throughout the study period of 2019-2033, with a focus around the estimated year of 2025, the global medical dosimetry equipment market is poised for significant growth, with certain regions and specific segments expected to lead this expansion. The North America region, particularly the United States, is anticipated to maintain its dominant position in the medical dosimetry equipment market. This dominance is underpinned by several factors including the presence of a well-established healthcare infrastructure, a high prevalence of cancer and advanced treatment modalities, and substantial investment in research and development. The region boasts a strong ecosystem of leading healthcare providers and research institutions that are early adopters of cutting-edge medical technologies, including advanced dosimetry systems. Furthermore, stringent regulatory frameworks in the US concerning radiation safety and patient care incentivize the adoption of sophisticated dosimetry solutions. The high disposable income and robust healthcare spending further facilitate the procurement of expensive, high-end equipment.

In parallel with regional dominance, the Active Type segment within the medical dosimetry equipment market is projected to witness the most rapid and significant growth, ultimately becoming a key driver of market expansion. Active dosimeters, such as electronic personal dosimeters (EPDs) and real-time dosimeters, offer distinct advantages over passive technologies like TLD and OSL. Their ability to provide immediate, real-time dose readings is invaluable for dynamic treatment planning, immediate occupational exposure monitoring, and rapid verification of radiation delivery. This real-time feedback loop significantly enhances patient safety and operational efficiency in radiation therapy departments and nuclear medicine facilities. The increasing sophistication of software integration, enabling remote monitoring, data logging, and predictive analysis of radiation exposure, further elevates the appeal of active dosimetry solutions.

Within the application landscape, the Hospital segment is expected to continue its reign as the largest and most influential market. Hospitals are the primary centers for cancer treatment, diagnostic imaging utilizing radiation, and interventional procedures involving radiation. The sheer volume of procedures performed, coupled with the comprehensive radiation safety protocols implemented in hospital settings, necessitates a constant demand for a wide array of medical dosimetry equipment. This includes equipment for patient treatment verification, occupational health monitoring for staff, and quality assurance checks on radiation-generating equipment. The presence of specialized departments like radiation oncology, radiology, and nuclear medicine within hospitals ensures a sustained and substantial requirement for both passive and active dosimetry solutions.

Furthermore, the Scientific Research segment is also demonstrating robust growth, albeit from a smaller base. As researchers delve deeper into understanding the biological effects of radiation, developing novel radiopharmaceuticals, and exploring new radiation delivery techniques, the demand for highly precise and specialized dosimetry equipment escalates. This includes applications in radiobiology laboratories, where accurate dose assessment is critical for experimental outcomes, and in the development and validation of new radiation therapies and imaging agents. The continuous drive for innovation in this segment fuels the development of next-generation dosimetry technologies that can address increasingly complex research questions. Therefore, while North America leads regionally and Hospitals dominate in application, the technological advancement within the Active Type segment, supported by the burgeoning Scientific Research applications, points towards a future where dynamic and integrated dosimetry solutions will be at the forefront of market growth.

The medical dosimetry equipment industry is experiencing significant growth catalysts that are shaping its future trajectory. A primary catalyst is the increasing global burden of cancer, driving the demand for more advanced and accurate radiation therapy, which in turn necessitates sophisticated dosimetry for treatment planning and delivery. Concurrently, stricter regulations and growing awareness surrounding radiation safety are compelling healthcare facilities to invest in reliable monitoring equipment to protect both patients and healthcare professionals.

Technological advancements, particularly in digital integration and real-time monitoring capabilities, are proving to be major catalysts. The development of portable, user-friendly, and data-rich dosimetry systems enhances their adoption in clinical and research settings. Furthermore, the expanding applications of nuclear medicine and diagnostic imaging that utilize radiation contribute to the overall market expansion by increasing the need for precise dose measurement and control.

This report offers an unparalleled depth of analysis for the medical dosimetry equipment market, encompassing a thorough examination of market dynamics from 2019 to 2033. It dissects the intricate interplay of technological advancements, regulatory landscapes, and evolving clinical needs that shape this vital sector. The report provides granular insights into market segmentation by type (TLD, OSL, RPL, Active Type), application (Clinic, Hospital, Scientific Research, Others), and geographical regions. With a projected market value in the billions, stakeholders will find actionable intelligence regarding current trends, future projections around the estimated year of 2025, and the key drivers propelling growth. Furthermore, it critically assesses the challenges and restraints, alongside identifying potent growth catalysts and the strategic initiatives of leading global players. This comprehensive coverage ensures a well-rounded understanding essential for strategic decision-making and identifying untapped opportunities within the burgeoning medical dosimetry equipment industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.8%.

Key companies in the market include Landauer, Fluke Corporation, Chiyoda Technol Corporation, Mirion Technologies, Thermo Fisher Scientific, Nagase Landauer, Fuji Electric, Hitachi Aloka, Bertin Instruments, Tracerco, ATOMTEX, Panasonic, Polimaster, Ludlum Measurements, XZ LAB, Arrow-Tech, Renri, Renri, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Medical Dosimetry Equipment," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Medical Dosimetry Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.