1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Bone Screw?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Medical Bone Screw

Medical Bone ScrewMedical Bone Screw by Type (Self-Tapping Screws (Cancellous Bone Screws), Non-self-Tapping Screws (Cortical Bone Screws)), by Application (Aldult, Child), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

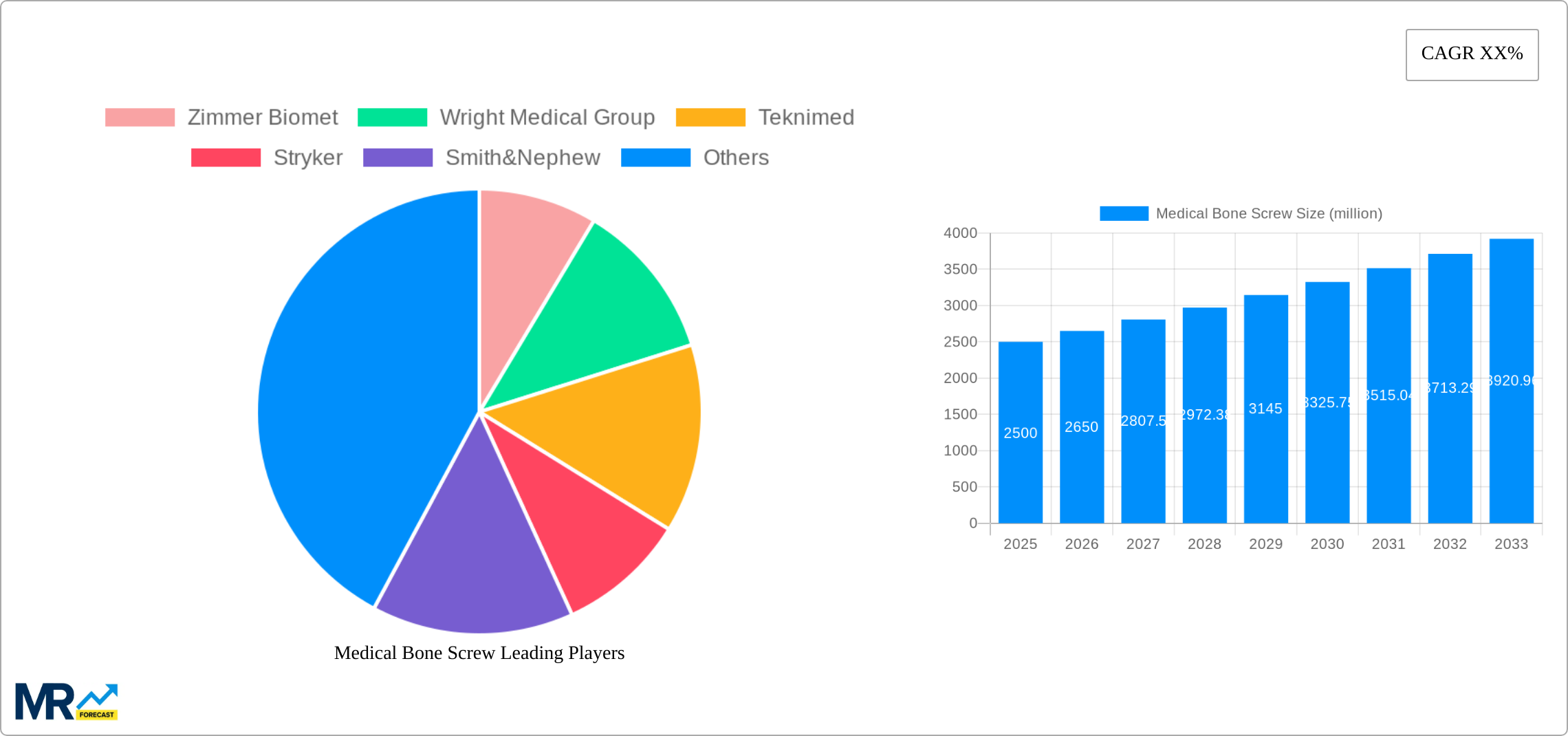

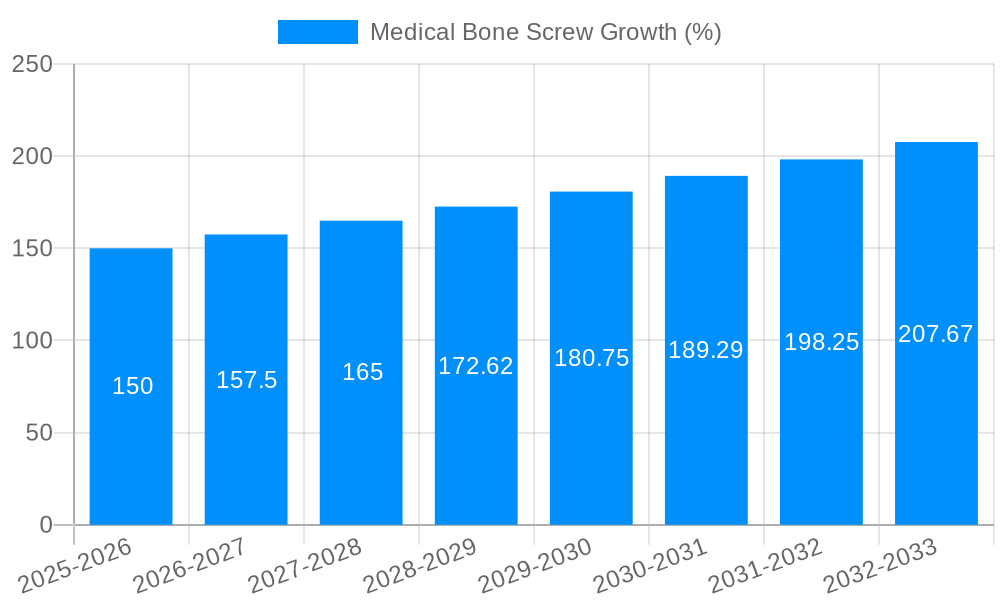

The global medical bone screw market is experiencing robust growth, driven by the rising prevalence of orthopedic injuries and surgeries, an aging global population susceptible to bone fractures and osteoporosis, and advancements in minimally invasive surgical techniques. The market is segmented by screw type (self-tapping and non-self-tapping) and application (adult and pediatric). Self-tapping screws, particularly cancellous bone screws, dominate due to their ease of use and suitability for various bone densities. However, non-self-tapping cortical bone screws are increasingly utilized in high-stress areas requiring greater fixation strength. The pediatric segment is showing significant growth potential, fueled by increasing awareness of pediatric orthopedic conditions and improved treatment options. Key players like Zimmer Biomet, Stryker, and Medtronic are driving innovation through the development of biocompatible materials, improved screw designs, and advanced surgical instrumentation, enhancing market competitiveness. Geographic expansion, particularly in emerging markets of Asia-Pacific and the Middle East & Africa, presents substantial growth opportunities, as healthcare infrastructure improves and affordability increases. Restraints include the high cost of implants, stringent regulatory approvals, and potential complications associated with surgical procedures.

The market's compound annual growth rate (CAGR) is projected to be around 5-7% during the forecast period (2025-2033), resulting in a substantial market expansion. North America currently holds the largest market share, driven by high healthcare expenditure and technological advancements. However, Europe and the Asia-Pacific regions are expected to witness significant growth owing to rising orthopedic procedures and an increasing number of trauma cases. The competitive landscape is characterized by both large multinational corporations and smaller specialized companies. The ongoing focus on developing innovative biomaterials, improving surgical techniques, and expanding distribution networks will continue to shape the future of the medical bone screw market.

The global medical bone screw market is experiencing robust growth, projected to reach multi-million unit sales by 2033. Driven by an aging global population, rising incidence of traumatic injuries, and advancements in surgical techniques, the market demonstrates consistent expansion across various segments. The historical period (2019-2024) witnessed a steady increase in demand, establishing a strong base for future growth. The estimated year (2025) showcases a significant market size, indicating a sustained upward trajectory. This growth is further fueled by increasing adoption of minimally invasive surgical procedures, which necessitates the use of smaller and more specialized bone screws. The forecast period (2025-2033) anticipates continued expansion, with significant contributions from both developed and developing economies. Technological innovations, including the development of biocompatible and biodegradable materials, are also shaping market trends. Competition among key players like Zimmer Biomet, Stryker, and Medtronic is intensifying, leading to innovations in screw design, material science, and surgical instruments. This competitive landscape fosters a dynamic market characterized by continuous improvement in product offerings and expanding market penetration. The market is segmented by screw type (self-tapping and non-self-tapping), application (adult and pediatric), and material composition, allowing for targeted market analysis and identification of growth opportunities. Specific regional variations in market growth exist, driven by healthcare infrastructure development, economic factors, and regional prevalence of orthopedic conditions. Overall, the market demonstrates a positive outlook with considerable potential for continued expansion throughout the forecast period.

Several factors are contributing to the significant growth of the medical bone screw market. The escalating global geriatric population is a primary driver, as older individuals are more prone to osteoporosis and fractures requiring surgical intervention. Simultaneously, rising incidences of traumatic injuries from accidents and sports activities necessitate a substantial number of bone screw implantations annually. Advancements in surgical techniques, particularly minimally invasive surgery (MIS), are contributing to increased demand. MIS procedures often rely on smaller, more precise bone screws, driving innovation and market expansion in this area. Technological advancements are constantly improving bone screw materials and designs. The development of biocompatible and biodegradable materials reduces the risk of complications and improves patient outcomes, making these devices increasingly attractive for surgical applications. Furthermore, the expanding healthcare infrastructure, particularly in developing countries, contributes to market growth by increasing access to specialized orthopedic procedures. The rise in sports-related injuries among younger demographics further boosts market demand for pediatric bone screws, a segment demonstrating significant growth potential. Finally, increased awareness of orthopedic conditions and improved healthcare reimbursement policies are facilitating greater market access and adoption of bone screws. These factors collectively contribute to the impressive projected growth of the medical bone screw market.

Despite the significant growth potential, the medical bone screw market faces several challenges. The stringent regulatory requirements for medical devices, including rigorous testing and approval processes, pose a significant barrier to market entry for new players and can delay product launches. High manufacturing costs and the complexities of the supply chain can negatively impact profitability. Competition among established players, such as Zimmer Biomet and Stryker, is intense, leading to price pressures and a need for continuous innovation. The potential for complications associated with bone screw implantation, such as infection, screw breakage, or loosening, can impact patient outcomes and influence market perception. Variations in healthcare reimbursement policies across different regions also create uncertainty in market forecasting. Furthermore, the need for highly specialized surgical skills for bone screw implantation can limit access to these procedures in areas with limited surgical expertise. Finally, economic downturns or fluctuations in healthcare spending can potentially impact market growth, influencing purchasing decisions from hospitals and healthcare providers. Addressing these challenges is crucial for maintaining sustainable growth in the medical bone screw market.

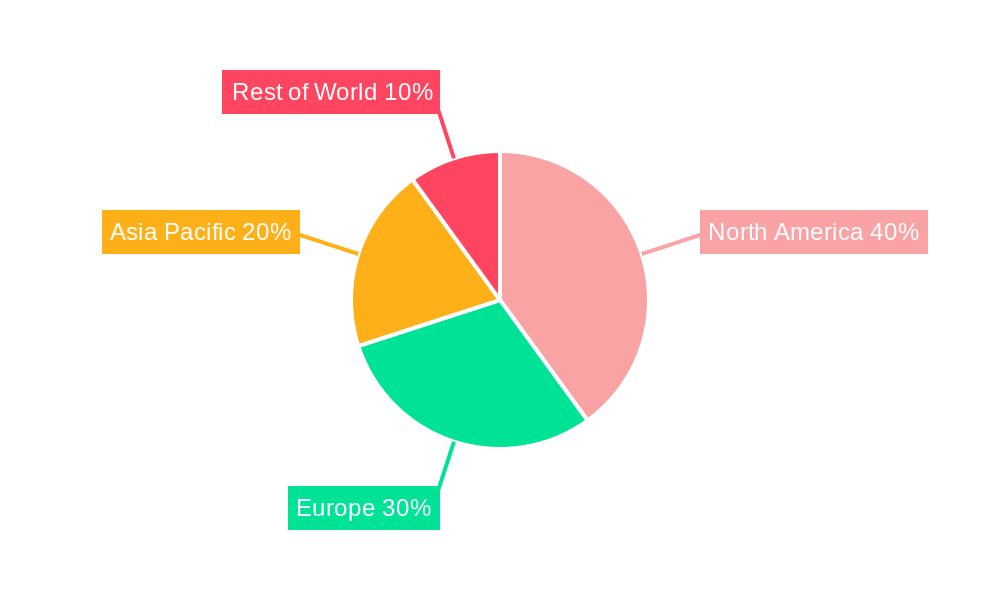

The medical bone screw market exhibits significant regional variations in growth rates and market penetration. North America and Europe currently hold the largest market shares, driven by factors such as advanced healthcare infrastructure, high healthcare spending, and a substantial aging population. However, Asia-Pacific is projected to experience substantial growth during the forecast period, driven by rising healthcare expenditures and an expanding middle class. Specific countries, such as the United States and Germany, demonstrate significant market dominance, characterized by a large patient pool and well-established orthopedic surgical practices.

Adult Application Segment: This segment is expected to maintain its dominance throughout the forecast period, driven by the high prevalence of age-related bone conditions and trauma. Increased incidence of fractures and osteoporosis in aging populations will directly translate into increased demand for bone screws in adult patients.

Self-Tapping Screws (Cancellous Bone Screws) Segment: This segment is likely to dominate due to the ease and speed of implantation, making them highly suitable for various surgical applications. Their versatility in handling cancellous bone, which is spongy and less dense than cortical bone, makes them more widely applicable.

The paragraph below explains the reason behind the above point: The adult segment's dominance stems from the higher incidence of bone fractures and related conditions in this age group. Moreover, self-tapping screws offer the advantage of simpler and faster insertion, making them preferable for surgeons in many scenarios. The higher adoption rate of self-tapping screws compared to their non-self-tapping counterparts further contributes to the dominance of this segment. The combination of these factors positions the adult application and self-tapping screw segments as the leading drivers of growth in the global medical bone screw market. The continued aging of populations worldwide and advances in minimally invasive surgical techniques will further cement this dominance in the coming years.

Several factors are accelerating the growth of the medical bone screw market. Technological advancements, such as the development of biocompatible and biodegradable materials, are improving patient outcomes and reducing complications. Minimally invasive surgical techniques are driving increased adoption of smaller and more precise bone screws. The increasing prevalence of orthopedic conditions and the rising geriatric population are generating significant demand. Finally, expansion of healthcare infrastructure in developing economies is opening up new market opportunities.

This report provides a thorough analysis of the medical bone screw market, covering key trends, driving forces, challenges, and growth opportunities. It offers detailed insights into market segmentation, regional variations, and competitive landscape. This comprehensive analysis enables informed decision-making for stakeholders involved in this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Zimmer Biomet, Wright Medical Group, Teknimed, Stryker, Smith&Nephew, Siora Surgicals, SinoBiom, Sharmaortho, Sandvik Coromant, OsteoMed, OrthoPediatrics, Orthofix Holdings, Medtronic, Johnson & Johnson (DePuy Synthes), Integra LifeSciences, Inion, GPC Medical, Bioretec Oy, BioPro Implants, Arthrex, Acumed, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Medical Bone Screw," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Medical Bone Screw, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.