1. What is the projected Compound Annual Growth Rate (CAGR) of the Mechanical Water Meter?

The projected CAGR is approximately 4.4%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Mechanical Water Meter

Mechanical Water MeterMechanical Water Meter by Type (Volumetric Water Meter, Dry Water Meter, Waterman Water Meter, Others), by Application (Household, Commercial/Industrial, Public Utilities), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

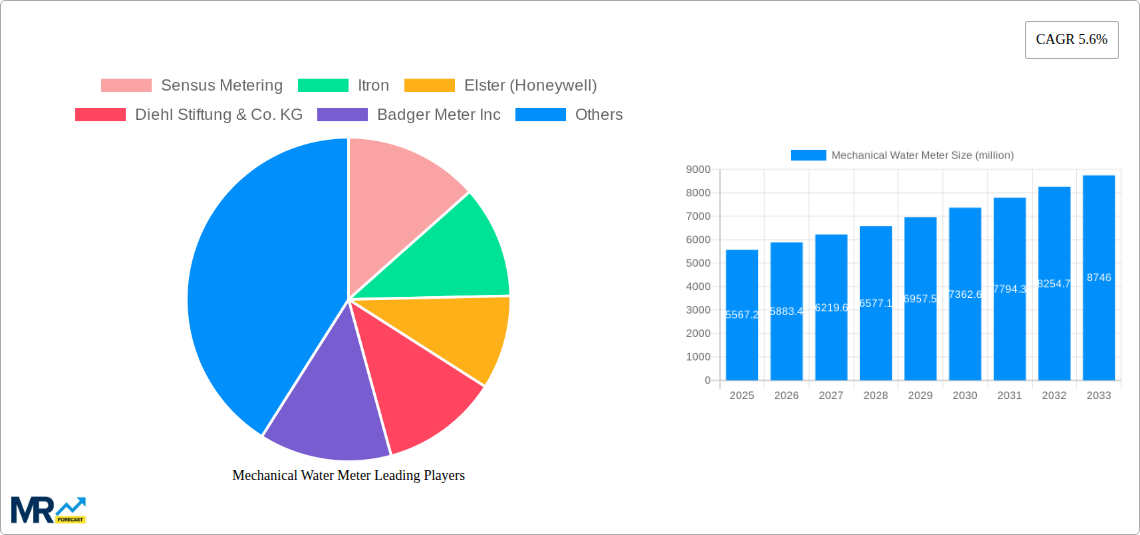

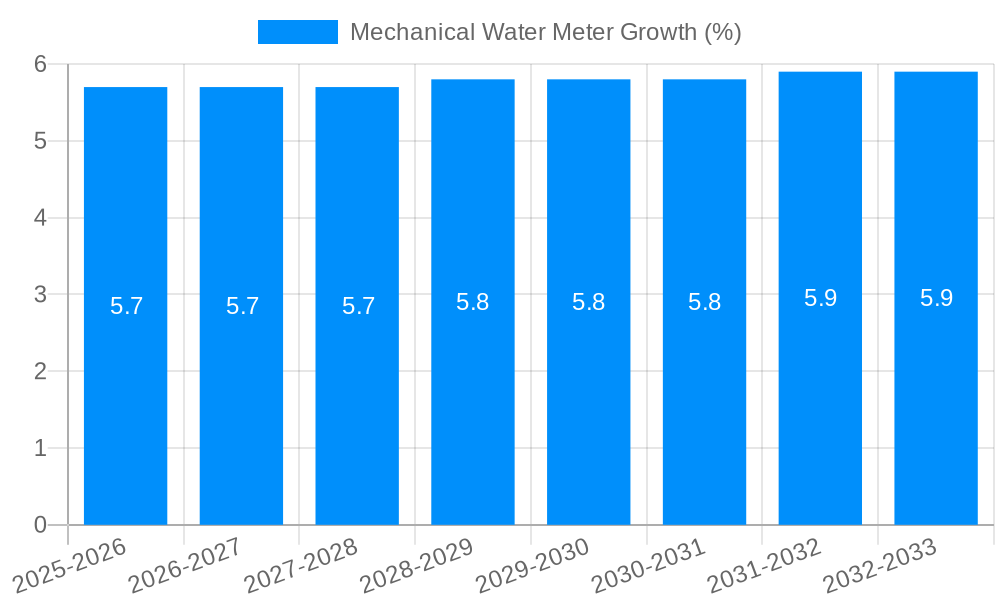

The global mechanical water meter market, valued at $4117.9 million in 2025, is projected to experience steady growth, driven by increasing urbanization and the need for efficient water resource management. A compound annual growth rate (CAGR) of 4.4% from 2025 to 2033 indicates a substantial market expansion. This growth is fueled by several key factors. Firstly, the rising global population necessitates improved water infrastructure and accurate metering solutions to manage consumption effectively. Secondly, government regulations and initiatives promoting water conservation are driving the adoption of advanced metering infrastructure (AMI) which often includes mechanical meters, especially in developing economies where affordability is crucial. The market also sees strong demand from the residential sector, complemented by robust growth from industrial and commercial applications. However, the market faces challenges such as the increasing popularity of smart water meters and technological advancements, which present a potential threat to mechanical meter dominance in the long term. Competitive landscape analysis suggests that established players like Itron, Sensus, and Badger Meter hold significant market share, while regional players are also contributing significantly, especially in developing markets in Asia. The market's future trajectory will depend on the balance between the cost-effectiveness of mechanical meters and the advanced capabilities of newer technologies.

The competitive landscape is marked by the presence of both established global players and regional manufacturers. Companies like Sensus Metering, Itron, and Badger Meter have established market leadership through their technological advancements and global reach. However, regional players, particularly from China, are gaining traction, driven by their cost-competitive products and localization strategies. The market dynamics indicate an ongoing shift towards more sophisticated metering solutions, potentially impacting the demand for basic mechanical meters. Nevertheless, the continued need for affordable and reliable water metering solutions, particularly in developing nations, ensures that the mechanical water meter market will remain a significant segment within the broader water metering industry for the foreseeable future. Future growth will heavily depend on regional infrastructure development, government policies promoting water conservation, and the continuing affordability of mechanical meters compared to their technologically advanced counterparts.

The global mechanical water meter market exhibited robust growth during the historical period (2019-2024), exceeding 100 million units in annual sales by 2024. This growth is primarily driven by increasing urbanization and population growth, particularly in developing economies where infrastructure development is a major focus. However, the market is experiencing a gradual shift towards smart water metering systems. While mechanical meters remain dominant in many regions due to their lower initial cost, their limitations in terms of accuracy, data collection, and leak detection are driving a transition towards more advanced technologies. The estimated market size for 2025 is projected to be around 110 million units, indicating continued but decelerating growth compared to previous years. This slower growth reflects the increasing adoption of smart meters, which offer superior capabilities. The forecast period (2025-2033) anticipates continued growth, albeit at a more moderate pace, with a projected market size exceeding 150 million units by 2033. This projection considers factors like continued infrastructure development, especially in emerging markets, but also acknowledges the ongoing market share shift towards electronic and smart metering solutions. The report provides a comprehensive analysis of this dynamic market, factoring in regional variations and the competitive landscape. The key to understanding the future trajectory of mechanical water meters lies in appreciating the balance between their cost-effectiveness in specific applications and the growing need for advanced water management solutions. This nuanced perspective is crucial for accurate forecasting and informed strategic decision-making within the water utility industry.

The continued prevalence of mechanical water meters despite the rise of smart meters is driven by several factors. Their lower upfront cost remains a significant advantage, making them economically viable for many water utilities, especially in regions with limited budgets. Simplicity in design and installation contributes to their widespread adoption, particularly in areas with less developed infrastructure or where specialized technical expertise is lacking. While less sophisticated than smart meters, mechanical meters offer reliable basic functionality; they accurately measure water consumption and require minimal maintenance for several years of consistent performance. Furthermore, a well-established supply chain and a large number of manufacturers ensure the ready availability of mechanical meters, creating a stable and competitive market. This established supply network keeps costs manageable and ensures quick access to replacement parts. Finally, the familiarity and ease of understanding of mechanical meters, particularly among older generations of water utility staff, helps maintain their continued use.

The mechanical water meter market faces significant challenges, primarily stemming from technological advancements in smart water metering and evolving industry needs. The limitations of mechanical meters in data collection represent a key drawback; unlike smart meters that provide real-time data on consumption patterns, leaks, and system efficiency, mechanical meters require manual readings, creating inefficiencies and delays. The lack of advanced features like leak detection contributes to higher water loss rates, negatively impacting water resource management. Furthermore, the accuracy of mechanical meters can degrade over time due to wear and tear, potentially leading to billing inaccuracies and disputes with consumers. Increasing regulatory pressures and the demand for improved water conservation necessitate the adoption of more advanced metering infrastructure. The growing emphasis on data-driven decision-making in water resource management further favors the adoption of smart meters capable of providing granular, real-time data. Finally, the growing popularity of advanced metering systems creates significant competitive pressure for traditional mechanical water meters.

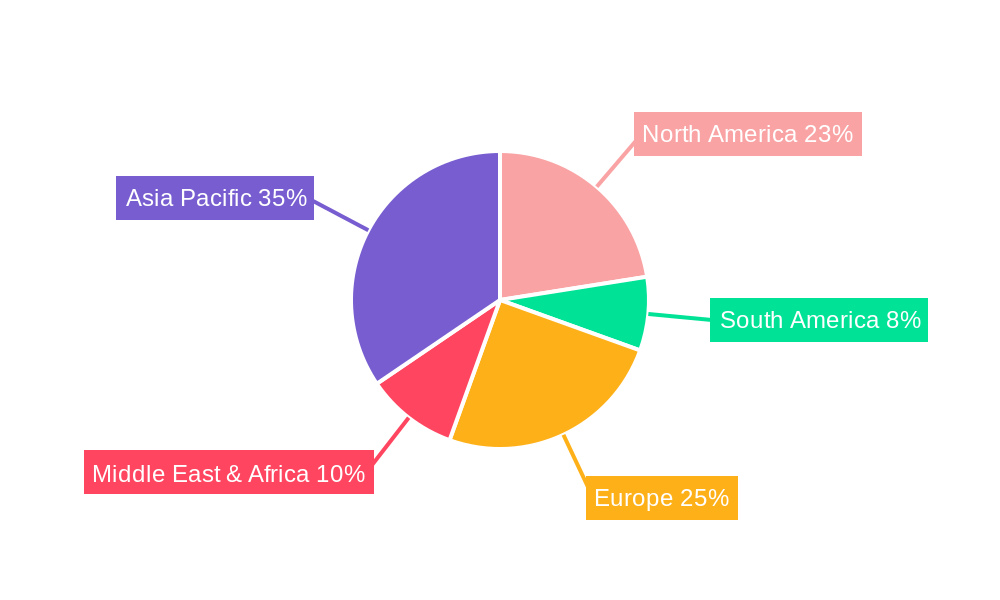

Developing Economies: Regions like Asia-Pacific (excluding Japan), Africa, and parts of Latin America are predicted to drive significant growth in the mechanical water meter market during the forecast period. The ongoing infrastructure development in these areas creates a high demand for water meters, with mechanical meters representing a cost-effective solution for many projects. The sheer volume of new installations in these developing markets will significantly contribute to overall market growth figures, even with the global shift towards smart metering.

Residential Segment: The residential sector typically accounts for a substantial portion of mechanical water meter installations. The relatively low cost of these meters makes them the preferred choice for individual households, especially in regions where infrastructure limitations or affordability considerations dictate the selection of simpler metering technologies. This strong presence in residential applications contributes significantly to the overall market size and will continue to do so even as the commercial and industrial sectors gradually shift toward smart metering solutions.

Specific Countries: Within these regions, rapid urbanization and population growth in countries like India, China, and several nations in sub-Saharan Africa will contribute disproportionately to the demand for mechanical water meters. These countries often prioritize affordable and readily deployable solutions due to resource limitations and the immense scale of infrastructure projects.

The paragraph below elaborates on this further: The continued dominance of the mechanical water meter in developing economies is a complex interplay of cost, accessibility, and infrastructure readiness. The initial investment required for smart meter infrastructure, including the necessary communication networks and data management systems, often presents a significant hurdle for these regions. Thus, the lower cost and simpler installation procedures of mechanical meters create a clear advantage, ensuring their continued relevance in providing basic water metering capabilities in a substantial portion of the global market. However, it’s crucial to acknowledge that even in these regions, the transition towards smart meters is inevitable, driven by long-term cost savings associated with reduced water loss and improved efficiency.

Continued investment in infrastructure development, particularly in developing economies, is a major catalyst for the growth of the mechanical water meter market. These investments often focus on extending water supply networks to underserved populations, necessitating the installation of millions of new meters. Government initiatives and funding programs aimed at improving water management and reducing water loss further bolster the demand for accurate, reliable, and affordable water meters, with mechanical meters often fulfilling this requirement cost-effectively.

This report provides a detailed analysis of the global mechanical water meter market, offering valuable insights into market trends, growth drivers, challenges, and key players. It includes historical data, current estimations, and future forecasts, providing a comprehensive overview for stakeholders in the water utility industry, investors, and manufacturers. The report's focus on regional variations and segment-specific analyses allows for informed decision-making based on a detailed understanding of market dynamics.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.4% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.4%.

Key companies in the market include Sensus Metering, Itron, Elster (Honeywell), Diehl Stiftung & Co. KG, Badger Meter Inc, Ningbo Water Meter, Zenner International GmbH & Co. KG, Kamstrup Water Metering, Neptune Technology Group (Roper Industries), Shanchuan Group, Donghai Group, Mueller Water Products, LianLi Water Meter, SUNTRONT Technology, Hunan Changde Water Meter Manufacture, Shenzhen Huaxu, Beijing Huiyi, Chongqing Smart Water Meter Group, Lianyungang Water Meter, China Minsen Metet, Integrated Electronic Systems Lab, B METERS s.r.l., Hangzhou Jingda Electronic, .

The market segments include Type, Application.

The market size is estimated to be USD 4117.9 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Mechanical Water Meter," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Mechanical Water Meter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.