1. What is the projected Compound Annual Growth Rate (CAGR) of the Marine Valves and Actuators?

The projected CAGR is approximately XX%.

Marine Valves and Actuators

Marine Valves and ActuatorsMarine Valves and Actuators by Type (Marine Valves, Marine Actuators), by Application (Passenger Ships, Fishing Boats, Pleasure Boats, Goods Transport Ships, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

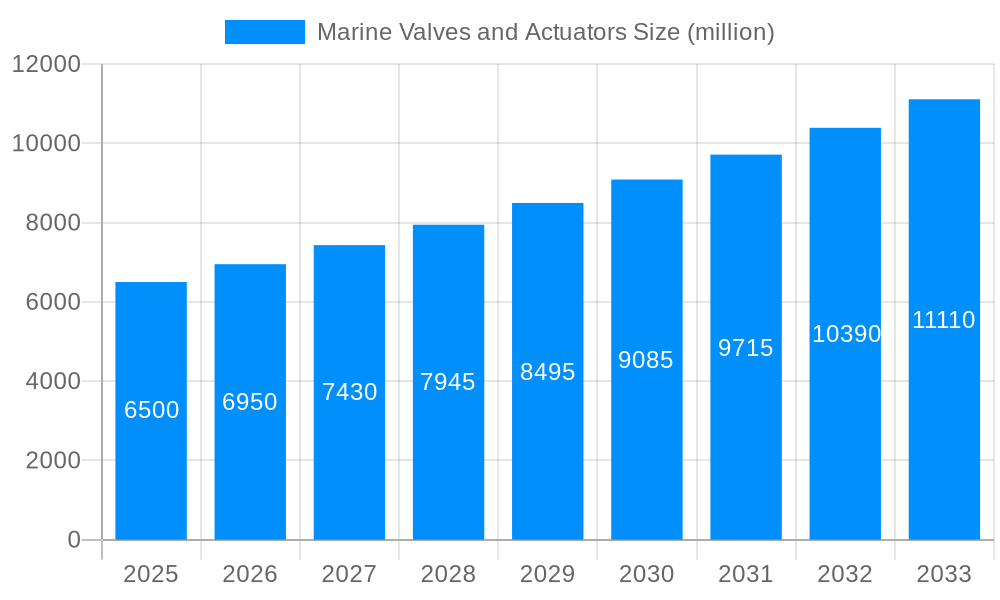

The global Marine Valves and Actuators market is projected to experience robust growth, estimated at a substantial market size of USD 6,500 million by 2025, with a projected Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period of 2025-2033. This expansion is primarily propelled by the escalating demand for new vessel construction across various maritime sectors, including cargo shipping, passenger ferries, and offshore exploration. The increasing emphasis on enhanced operational efficiency, safety regulations, and the adoption of smart technologies in marine environments are further fueling the market. The integration of advanced actuators for precise control and the growing need for corrosion-resistant and durable valves in harsh marine conditions are key drivers. The market is witnessing a significant shift towards automated and intelligent valve systems, driven by the necessity to optimize fuel consumption and minimize environmental impact through stringent emission controls.

The market segmentation reveals a dynamic landscape, with Marine Valves holding a dominant share due to their widespread application in controlling fluid and gas flow in diverse marine systems. Within applications, Goods Transport Ships represent the largest segment, followed by Passenger Ships, reflecting the global trade volume and the expansion of cruise and ferry services. Emerging trends include the development of sustainable and eco-friendly valve solutions, smart valves with integrated sensors for real-time monitoring and predictive maintenance, and the increasing adoption of electric actuators over hydraulic or pneumatic alternatives for improved energy efficiency and reduced environmental footprint. However, the market faces certain restraints, such as the high initial cost of advanced marine valve and actuator systems and the complex regulatory landscape associated with maritime safety and environmental compliance, which can hinder widespread adoption, particularly for smaller vessel operators.

Here's a unique report description on Marine Valves and Actuators, incorporating your specified elements:

This comprehensive report delves into the dynamic global market for marine valves and actuators, offering a nuanced analysis of trends, drivers, challenges, and growth opportunities. Spanning a study period from 2019 to 2033, with a base year of 2025 and a detailed forecast period of 2025-2033, the report provides invaluable insights for industry stakeholders. Leveraging historical data from 2019-2024, we chart the market's trajectory, projecting future performance based on robust methodologies and expert analysis. The market is poised for significant expansion, with a projected valuation reaching an estimated $X,XXX million in 2025 and expected to grow to $Y,YYY million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of Z.ZZ%.

XXX The global marine valves and actuators market is undergoing a significant transformation, driven by a confluence of technological advancements, evolving regulatory landscapes, and the persistent demand for enhanced operational efficiency and safety across diverse maritime applications. A key trend observed is the increasing adoption of smart and connected valve systems. These intelligent actuators, often integrated with IoT capabilities, enable real-time monitoring, predictive maintenance, and remote control, thereby minimizing downtime and optimizing fluid management on vessels. This shift towards digitalization is particularly pronounced in the Goods Transport Ships segment, where the sheer volume of operations and the need for precise cargo handling necessitate advanced control solutions. Furthermore, the industry is witnessing a surge in demand for actuators with higher levels of automation and precision, moving beyond basic on/off functionality to sophisticated proportional and fail-safe mechanisms. The emphasis on energy efficiency and environmental compliance is also shaping valve and actuator design, with manufacturers focusing on solutions that reduce leakage, minimize energy consumption, and comply with stringent emissions regulations. The Passenger Ships sector, in particular, is investing heavily in these advanced systems to enhance passenger comfort and meet international environmental standards. The market is also experiencing a growing preference for specialized materials and coatings that offer superior corrosion resistance and longevity in harsh marine environments, a critical consideration for all vessel types, from Fishing Boats to large cargo carriers. The increasing complexity of modern vessels, with their intricate piping networks and sophisticated control systems, further fuels the demand for customized and integrated valve and actuator solutions, moving away from one-size-fits-all approaches. The overarching trend is a move towards more intelligent, efficient, and sustainable fluid control systems that can withstand the rigors of the maritime environment while contributing to operational excellence and environmental stewardship.

The expansion of the global marine valves and actuators market is propelled by several interconnected forces. The robust growth in global trade, particularly in seaborne cargo, directly translates into increased demand for new construction of Goods Transport Ships, consequently driving the need for essential components like valves and actuators. This burgeoning shipping industry necessitates reliable and efficient fluid handling systems to ensure the smooth operation of engines, ballast systems, cargo handling, and other critical functions. Concurrently, increasing investments in shipbuilding and the retrofitting of older vessels with advanced technologies are significant growth catalysts. Many existing fleets are being upgraded to comply with stricter environmental regulations and to improve operational efficiency, which often involves replacing conventional valve and actuator systems with more sophisticated, automated, and energy-efficient alternatives. The growing emphasis on maritime safety and security also plays a crucial role. The implementation of stringent international safety standards and certifications necessitates the use of high-quality, reliable valves and actuators that can perform under extreme conditions and prevent potential hazards like leaks or system failures. Furthermore, the expanding offshore oil and gas exploration and production activities, although facing some market volatility, continue to create a sustained demand for specialized marine valves and actuators designed for demanding offshore environments, impacting segments like Others which can encompass specialized support vessels. The continuous innovation in materials science and actuator technology, leading to more durable, compact, and cost-effective solutions, also plays a vital role in driving market adoption across all segments, including Pleasure Boats and Fishing Boats.

Despite the promising growth trajectory, the marine valves and actuators market faces several inherent challenges and restraints that could impede its full potential. One of the most significant hurdles is the inherent cyclicality of the maritime industry. Fluctuations in global trade, geopolitical instability, and economic downturns can directly impact shipbuilding orders and vessel maintenance budgets, leading to periods of reduced demand for marine valves and actuators. The stringent regulatory environment, while a driver for advanced solutions, also presents a challenge. Compliance with evolving international maritime regulations, such as those related to emissions and ballast water management, requires significant investment in research and development for manufacturers and in retrofitting or new builds for ship owners. This can be particularly burdensome for smaller players or those operating in less developed maritime economies. Another constraint is the high initial cost associated with advanced, automated, and smart valve and actuator systems. While these systems offer long-term operational benefits, their upfront investment can be a deterrent, especially for segments like Fishing Boats or smaller Pleasure Boats with limited capital. Furthermore, the availability of skilled labor for installation, maintenance, and repair of these increasingly sophisticated systems is a growing concern. The complexity of modern marine engineering demands specialized expertise, and a shortage of qualified technicians can lead to delays and increased operational costs. Supply chain disruptions, as witnessed in recent global events, can also pose a significant challenge, impacting the timely delivery of components and raw materials, thereby affecting production schedules and market responsiveness. The competitive landscape, characterized by the presence of established global players and emerging regional manufacturers, can also lead to price pressures and margin erosion, particularly for standard product offerings.

The Goods Transport Ships segment is anticipated to emerge as a dominant force in the global marine valves and actuators market, driven by its sheer volume and critical role in international commerce. This segment encompasses a vast array of vessels, including container ships, bulk carriers, tankers, and roll-on/roll-off (Ro-Ro) ships, all of which require a substantial number of valves and actuators for various functions. The continuous demand for transporting goods across oceans necessitates constant fleet expansion and regular maintenance, ensuring a steady and significant market for these components. The increasing focus on larger, more efficient vessels and the integration of advanced cargo handling technologies within this segment further amplify the need for sophisticated valve and actuator solutions.

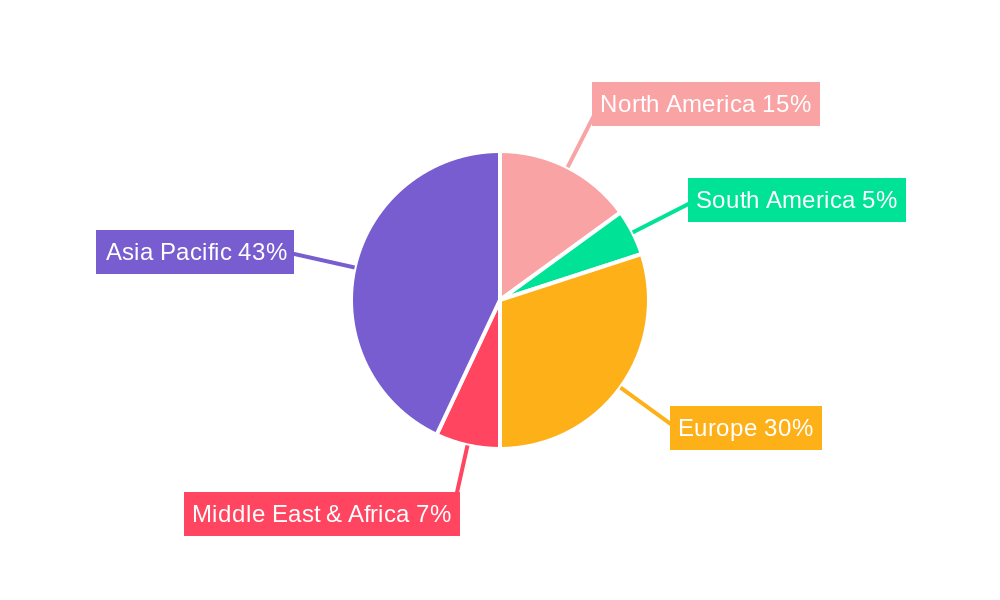

In terms of regional dominance, Asia Pacific is projected to lead the market and exhibit the highest growth. This leadership is primarily attributed to the region's status as a global shipbuilding hub, with countries like China, South Korea, and Japan accounting for a significant portion of global new vessel construction. The burgeoning economies within Asia Pacific also contribute to increased maritime trade, driving demand for both new builds and retrofitting of existing fleets.

Dominant Segment: Goods Transport Ships

Dominant Region: Asia Pacific

The synergy between the substantial demand from the Goods Transport Ships segment and the manufacturing prowess of the Asia Pacific region positions them as the primary drivers of the global marine valves and actuators market. The continuous investment in new vessel construction, coupled with stringent operational and environmental requirements, will ensure the sustained growth and dominance of these key areas.

Several key factors are acting as powerful catalysts for growth within the marine valves and actuators industry. The ongoing global economic recovery and the subsequent rebound in international trade are directly stimulating new shipbuilding orders, particularly for goods transport vessels, thereby increasing the fundamental demand for valves and actuators. Furthermore, the increasing focus on decarbonization and environmental sustainability within the shipping sector is a significant growth driver. This includes the adoption of cleaner fuels, which necessitates the development and deployment of specialized valves and actuators capable of handling these new substances, as well as retrofitting existing fleets to meet stricter emissions standards. Technological advancements, such as the integration of IoT and AI into actuators for enhanced monitoring and predictive maintenance, are creating new market opportunities and driving higher-value sales. The growing complexity of modern vessels also demands more sophisticated and integrated fluid control solutions, pushing innovation and product development.

This report offers an exhaustive examination of the marine valves and actuators market, providing a 360-degree view of its landscape. Beyond market sizing and forecasting, it dissects key trends, intricate drivers, and persistent challenges. The analysis extends to an in-depth exploration of dominant segments and regions, identifying specific areas poised for substantial growth. Furthermore, the report illuminates crucial industry developments, technological innovations, and the strategic initiatives of leading market players. With its comprehensive coverage, this report aims to equip stakeholders with the critical intelligence needed to navigate the complexities of the marine valves and actuators sector, identify lucrative opportunities, and formulate effective business strategies for sustained success in this evolving industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

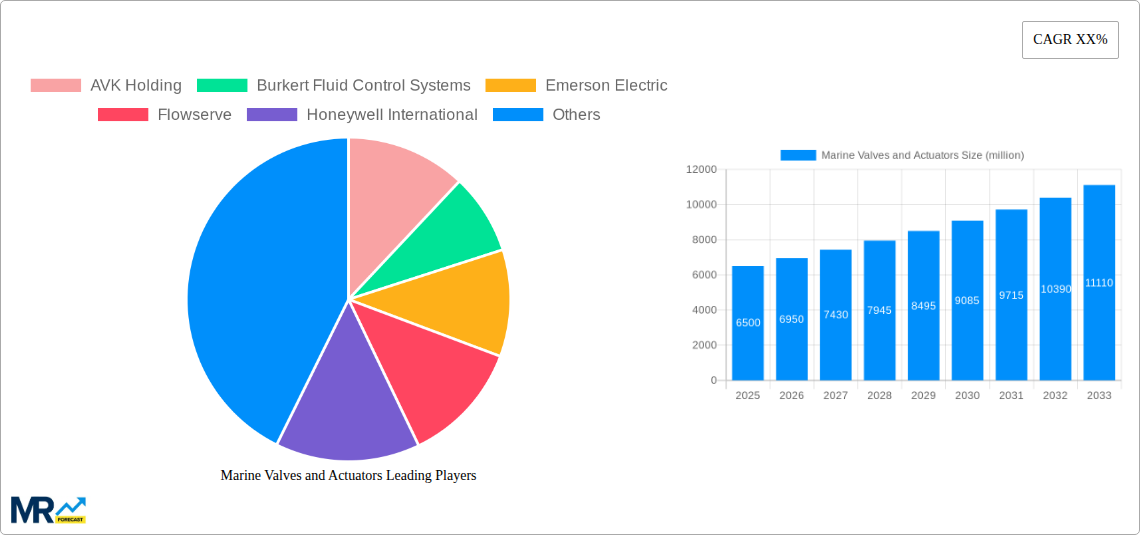

Key companies in the market include AVK Holding, Burkert Fluid Control Systems, Emerson Electric, Flowserve, Honeywell International, KITZ, Rotork, Schlumberger Limited, Tyco International, Watts Water Technologies, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Marine Valves and Actuators," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Marine Valves and Actuators, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.