1. What is the projected Compound Annual Growth Rate (CAGR) of the Marine Ballast Water Filter Elements?

The projected CAGR is approximately 4.5%.

Marine Ballast Water Filter Elements

Marine Ballast Water Filter ElementsMarine Ballast Water Filter Elements by Type (Horizontal, Vertical), by Application (Shipyards, Shipping Companies, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

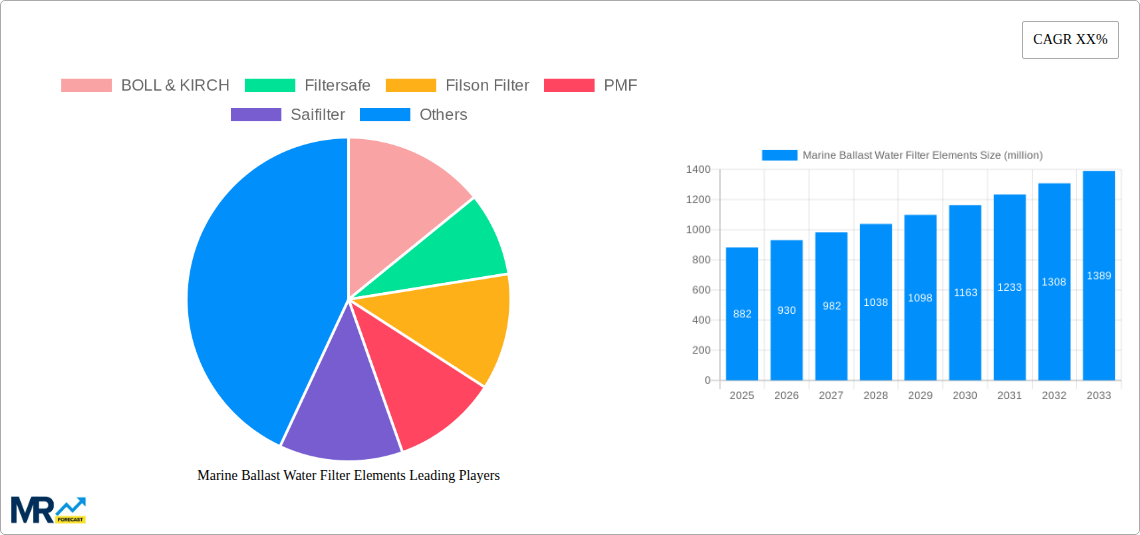

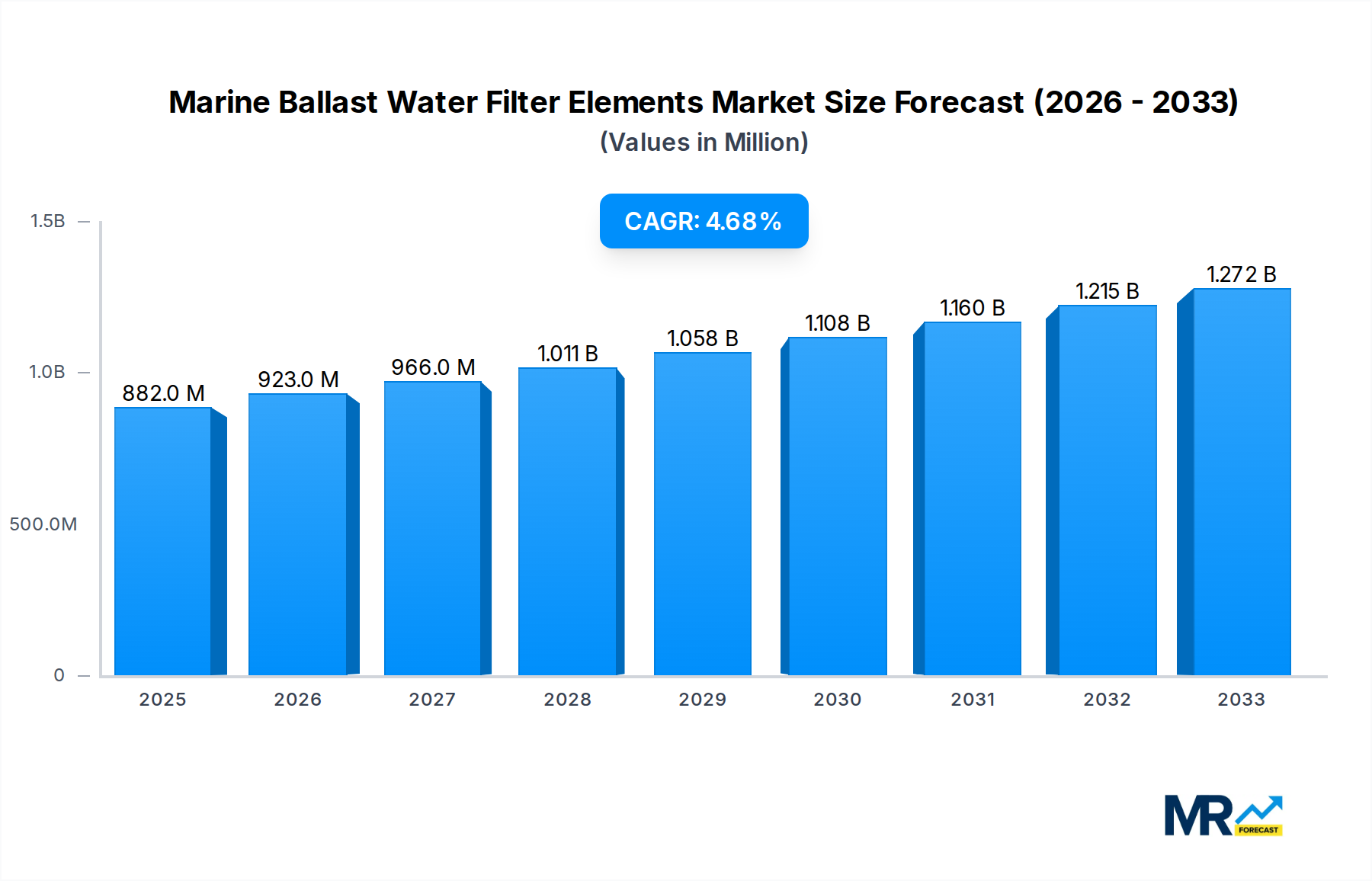

The global Marine Ballast Water Filter Elements market is poised for robust expansion, projected to reach an estimated \$882 million by 2025. This growth trajectory is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 4.5% anticipated over the forecast period of 2025-2033. The primary impetus for this surge is the escalating global shipping trade, which necessitates stringent ballast water management to prevent the introduction of invasive aquatic species. Regulatory mandates from international bodies like the International Maritime Organization (IMO), particularly the Ballast Water Management (BWM) Convention, are compelling shipping companies to invest in advanced filtration systems. Furthermore, the increasing demand for efficient and reliable filter elements that can withstand harsh marine environments and ensure compliance with evolving environmental standards is a significant driver. Technological advancements leading to more durable, cost-effective, and high-performance filter elements are also contributing to market vitality.

The market is segmented by type into Horizontal and Vertical filter elements, with applications predominantly found in Shipyards and Shipping Companies. The growing number of new vessel constructions and retrofitting projects to meet ballast water treatment requirements are creating substantial opportunities for market players. While the market presents a promising outlook, certain restraints could influence its pace. These include the initial high cost of advanced filtration systems for some vessel owners, particularly smaller operators, and the ongoing complexity and variability of regional regulations. However, the long-term benefits of compliance, including avoiding port entry denials and environmental penalties, are expected to outweigh these initial challenges. Leading companies such as BOLL & KIRCH, Filtersafe, and Filson Filter are actively innovating and expanding their product portfolios to capture a significant share of this expanding market.

The global marine ballast water filter elements market is poised for substantial expansion, projected to reach a market value of over $1,500 million by 2033, exhibiting a compelling compound annual growth rate (CAGR) of approximately 8.5% during the forecast period of 2025-2033. This upward trajectory is underpinned by an increasing awareness of the environmental ramifications associated with the discharge of untreated ballast water, which can lead to the introduction of invasive aquatic species and disrupt delicate marine ecosystems. International maritime regulations, spearheaded by the International Maritime Organization (IMO) through the Ballast Water Management Convention (BWMC), are a pivotal driving force, compelling shipping companies worldwide to invest in effective ballast water treatment systems. These systems invariably rely on advanced filter elements to remove a significant proportion of plankton, sediment, and other particulate matter before discharge.

The study period, spanning from 2019 to 2033, with a base year of 2025 and an estimated year also of 2025, highlights a dynamic market landscape. The historical period from 2019 to 2024 witnessed the initial adoption and refinement of ballast water treatment technologies, driven by the phased implementation of the BWMC. As we move into the forecast period, the market is expected to mature, with a greater emphasis on cost-effectiveness, efficiency, and the development of more sustainable filter technologies. The demand for robust and high-performance filter elements is expected to surge as new vessels are constructed and existing fleets undergo retrofitting to comply with stringent environmental standards. Industry developments will likely focus on enhancing filtration efficiency, reducing the frequency of element replacement, and minimizing the environmental footprint of the filtration process itself. The market's growth is not merely a response to regulation but also a testament to the shipping industry's growing commitment to environmental stewardship and sustainable operational practices.

The marine ballast water filter elements market is experiencing robust growth, primarily propelled by the stringent regulatory framework established by international bodies like the IMO. The Ballast Water Management Convention (BWMC) mandates that all ships engaged in international voyages must manage their ballast water to remove or kill harmful aquatic organisms and pathogens before they are discharged into new environments. This convention, along with similar regional and national legislations, has created an indispensable demand for effective ballast water treatment systems, at the core of which lie high-performance filter elements. The continuous increase in global maritime trade, leading to a larger fleet of vessels, further amplifies this demand. Moreover, there's a growing recognition within the shipping industry of its environmental responsibility, prompting proactive investments in sustainable technologies that minimize ecological impact. This includes upgrading existing ballast water treatment systems with more efficient filter elements or opting for advanced systems from the outset for new builds.

Beyond regulatory compliance and fleet expansion, advancements in filtration technology are also acting as significant drivers. Manufacturers are continually innovating to produce filter elements that offer superior filtration efficiency, longer service life, and reduced maintenance requirements. This not only enhances the effectiveness of ballast water treatment but also contributes to operational cost savings for shipping companies. The development of more durable and environmentally friendly materials for filter elements, along with a focus on ease of replacement and disposal, are further contributing to market expansion. The economic benefits of preventing the introduction of invasive species, which can cause substantial ecological and economic damage to local marine environments, are also subtly but surely influencing investment decisions.

Despite the promising growth trajectory, the marine ballast water filter elements market is not without its challenges and restraints. One of the most significant hurdles is the high initial cost of ballast water treatment systems, which often include sophisticated filter elements. For many smaller shipping companies or those operating on tighter margins, the capital investment required for retrofitting existing vessels or installing new systems can be a substantial deterrent. This financial burden can slow down the adoption rate, particularly in developing regions or for older fleets. Furthermore, the complexity of installation and integration of these systems into existing vessel infrastructure can be a logistical and technical challenge, requiring specialized expertise and potentially leading to extended dry-docking periods, which translate to significant operational downtime and costs.

Another critical restraint is the variability in water conditions and the presence of diverse marine organisms. Filter elements need to be robust enough to handle a wide range of particle sizes, densities, and concentrations, from fine silts to larger plankton. Developing filter technologies that can consistently and effectively filter all types of ballast water, regardless of geographical origin, remains an ongoing challenge. The maintenance and replacement frequency of filter elements can also be a concern. While advancements are being made, some systems still require frequent cleaning or replacement of elements, adding to operational expenses and logistical complexities, especially for vessels operating in remote locations. Lastly, ensuring the long-term reliability and performance of filter elements in the harsh marine environment, which includes corrosive saltwater, vibrations, and extreme temperatures, requires continuous research and development.

The Horizontal segment within the marine ballast water filter elements market is projected to exhibit significant dominance, driven by its inherent versatility and widespread applicability across a broad spectrum of maritime vessels. Horizontal filter elements are favored for their ease of integration into various ballast water treatment system designs, offering greater flexibility in system layout and maintenance. Their prevalent use in mid-sized to large cargo ships, tankers, and container vessels, which constitute a substantial portion of the global fleet, contributes significantly to their market leadership. The inherent design allows for efficient flow distribution and sediment collection, crucial for handling the large volumes of ballast water processed by these vessels. As shipping companies prioritize operational efficiency and system reliability, the demand for horizontal filter elements is expected to remain robust. This segment benefits from established manufacturing processes and a well-developed supply chain, ensuring consistent availability and competitive pricing, further solidifying its dominant position. The ease of maintenance and replacement associated with horizontal filter elements also appeals to ship owners seeking to minimize downtime and operational disruptions.

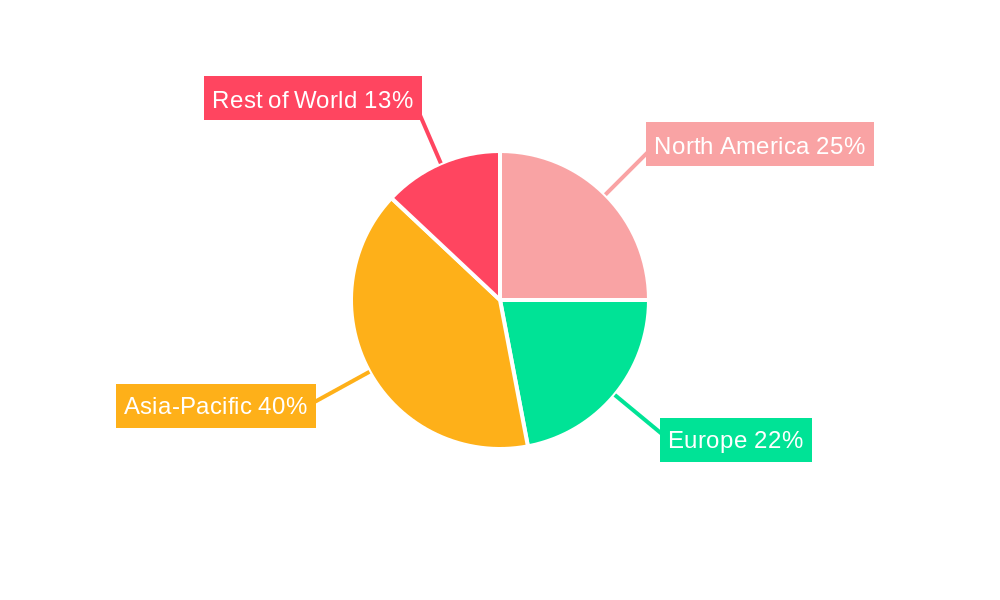

In terms of regional dominance, Asia Pacific is anticipated to lead the marine ballast water filter elements market. This leadership is primarily attributed to the region's status as a global hub for shipbuilding and maritime activities. Countries like China, South Korea, and Japan are responsible for a significant percentage of global new vessel construction, inherently driving the demand for ballast water treatment systems and their associated filter elements. Furthermore, the extensive shipping networks and the sheer volume of maritime trade originating from and passing through the Asia Pacific region necessitate stringent ballast water management practices. Regulatory enforcement in this region is becoming increasingly rigorous, compelling shipyards and shipping companies to adopt advanced filtration technologies. The presence of leading filter element manufacturers and suppliers within the region also contributes to its market dominance by ensuring ready availability and technical support. The burgeoning economies and increasing environmental awareness in many Asia Pacific nations are further fueling investments in sustainable maritime solutions, including sophisticated ballast water filtration. The ongoing retrofitting of older vessels to comply with international regulations, coupled with the construction of new, environmentally compliant vessels, ensures a sustained demand for filter elements in this dynamic region.

The marine ballast water filter elements industry is propelled by several key growth catalysts. The unwavering enforcement and ongoing evolution of international maritime regulations, particularly the IMO's Ballast Water Management Convention, serve as a primary catalyst, compelling a vast majority of the global fleet to adopt compliant treatment systems that rely heavily on filter elements. The continuous growth in global maritime trade, leading to an expanding fleet size, directly translates to an increased demand for these essential components. Furthermore, technological advancements in filtration media and design are enhancing the efficiency, durability, and cost-effectiveness of filter elements, making them more attractive to shipping companies.

This comprehensive report on Marine Ballast Water Filter Elements offers an in-depth analysis of the market's dynamics from 2019 to 2033, with a specific focus on the base and estimated year of 2025 and the forecast period of 2025-2033. It delves into the key market trends, exploring the projected market valuation exceeding $1,500 million by 2033, driven by stringent environmental regulations and the expansion of the global shipping fleet. The report meticulously examines the driving forces, such as the IMO's Ballast Water Management Convention, and the challenges, including high initial costs and operational complexities, that shape the market landscape. Furthermore, it provides a detailed segmentation analysis, highlighting the anticipated dominance of the Horizontal segment and the Asia Pacific region in terms of market share and growth potential. The report also identifies critical growth catalysts and lists leading industry players, offering a holistic view of the competitive environment. It concludes with significant developments and provides an outlook for the future of the marine ballast water filter elements sector, ensuring stakeholders are equipped with actionable insights for strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.5%.

Key companies in the market include BOLL & KIRCH, Filtersafe, Filson Filter, PMF, Saifilter, Boedon, Bluslot Filter, Zhehan Filter Equipment, Hebei Sinter Filter Technic, Xinxiang Tiancheng Aviation Purification Equipment, Xinxiang Guohai, HENAN ZHONGLV NEW MATERIAL TECHNOLOGY.

The market segments include Type, Application.

The market size is estimated to be USD 882 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Marine Ballast Water Filter Elements," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Marine Ballast Water Filter Elements, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.