1. What is the projected Compound Annual Growth Rate (CAGR) of the Manual Sphygmomanometer?

The projected CAGR is approximately 12.91%.

Manual Sphygmomanometer

Manual SphygmomanometerManual Sphygmomanometer by Type (Aneroid Sphygmomanometer, Mercury Sphygmomanometer), by Application (Hospital, Clinic, Physical Examination Center), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

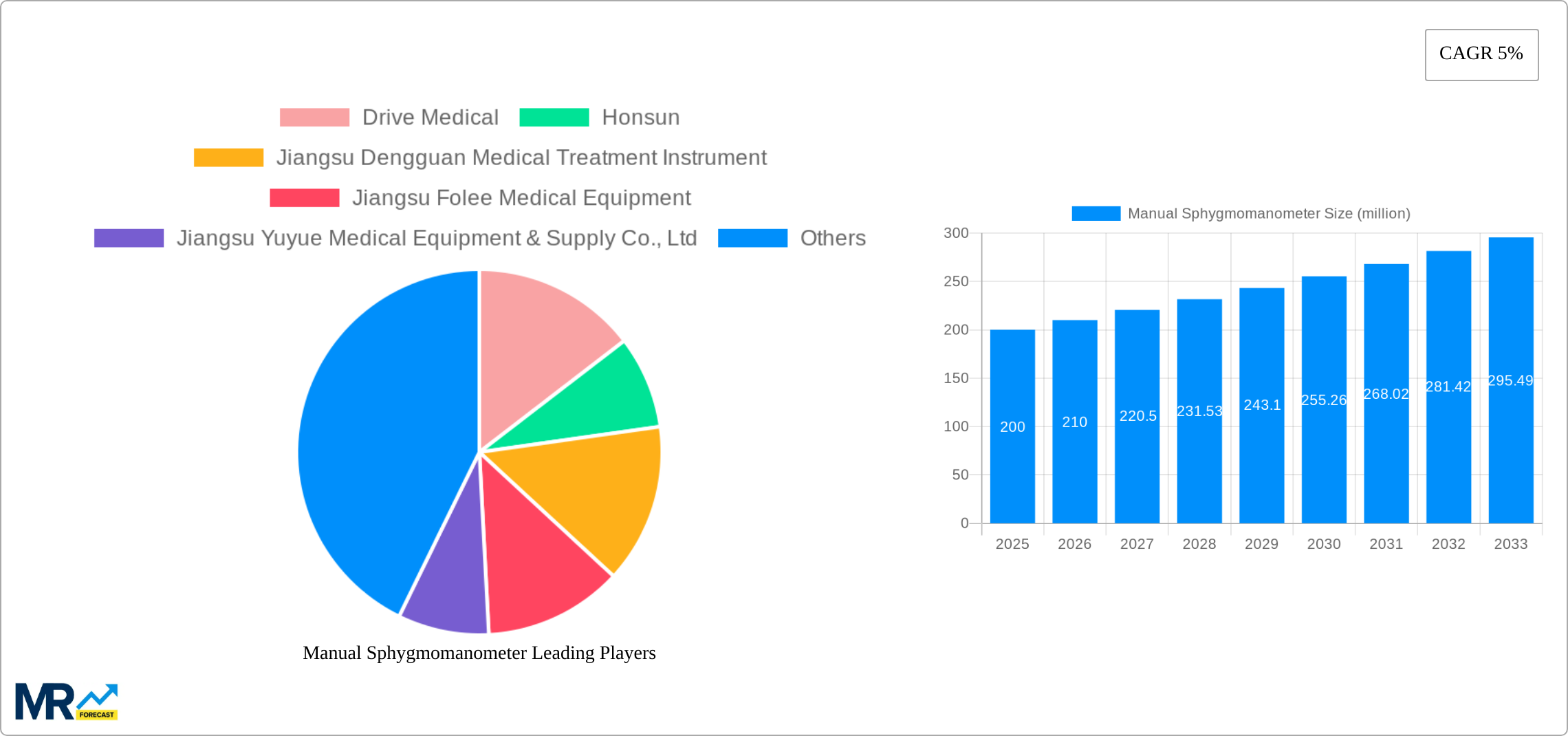

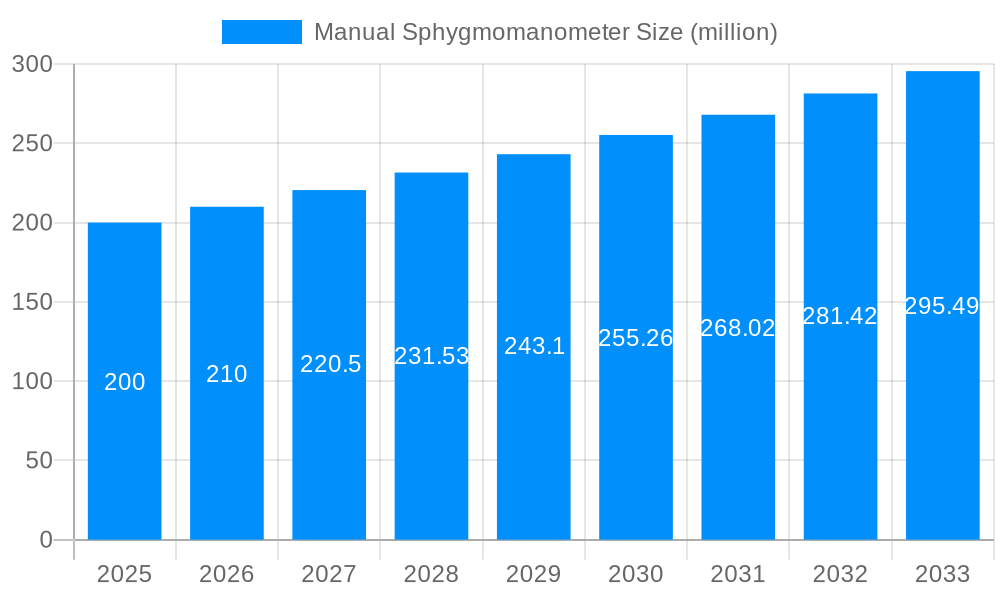

The global manual sphygmomanometer market is poised for significant expansion, driven by the escalating prevalence of hypertension and the sustained demand for economical blood pressure monitoring solutions across clinical and home environments. The market, valued at $10.43 billion in 2025, is projected to achieve a compound annual growth rate (CAGR) of 12.91%, reaching substantial figures by 2033. Key growth catalysts include an aging global population, heightened awareness of cardiovascular health, and the ongoing preference for uncomplicated, dependable, and accessible manual devices, particularly in resource-limited regions. The aneroid sphygmomanometer segment dominates due to its affordability and portability, while mercury sphygmomanometers retain a specialized niche despite declining usage attributed to safety and regulatory considerations. Hospitals and clinics represent the primary application sectors, with notable growth anticipated in home healthcare settings owing to the rise in self-monitoring practices. Leading market participants encompass established medical device manufacturers and agile regional players, who are prioritizing product innovation, enhanced accuracy, and expanded distribution to meet diverse consumer needs. While the burgeoning popularity of automated electronic devices and the potential for manual reading inaccuracies pose challenges, the inherent demand for reliable, cost-effective, and straightforward blood pressure measurement solutions continues to underpin market resilience.

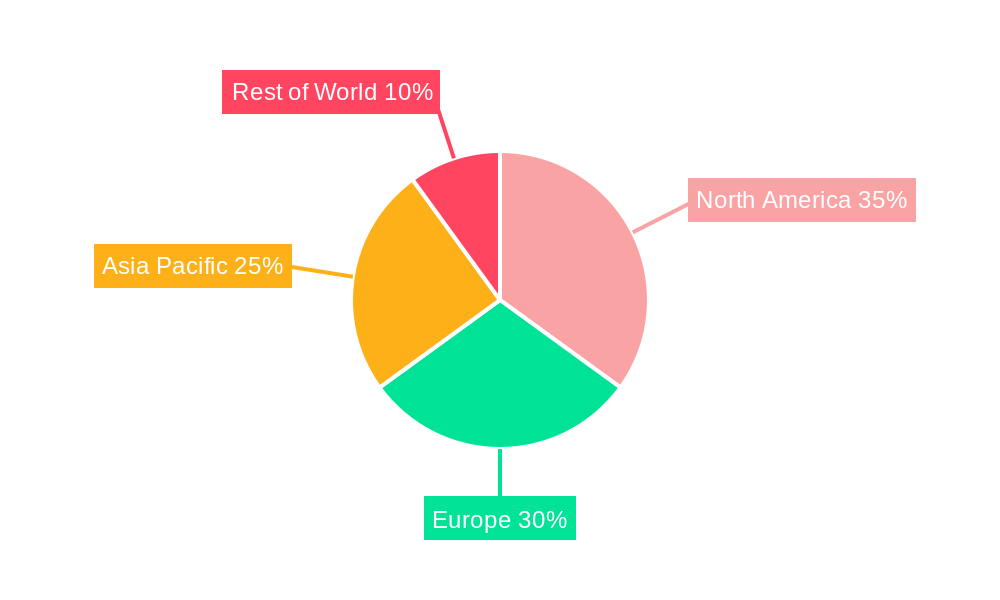

The competitive arena features a blend of international and local enterprises, with strategic focus on specific market segments and geographic territories. Established brands leverage extensive distribution networks and brand equity, while emerging competitors capitalize on technological advancements and efficient manufacturing to capture market share. Regional market dynamics are projected to vary, with North America and Europe maintaining robust positions due to high healthcare spending and cardiovascular disease incidence. Conversely, the Asia-Pacific region is anticipated to exhibit accelerated growth, propelled by rising disposable incomes and improving healthcare infrastructure. Future market evolution will likely be shaped by innovations in manufacturing materials, enhanced user ergonomics, and the integration with digital health platforms for remote patient monitoring and data analytics. The overarching commitment to optimizing patient outcomes and mitigating healthcare expenditures will continue to guide market advancements.

The global manual sphygmomanometer market exhibited steady growth throughout the historical period (2019-2024), reaching an estimated value exceeding 100 million units in 2025. This growth is projected to continue during the forecast period (2025-2033), driven by several factors analyzed in this report. While the market is mature, consistent demand from healthcare settings and a preference for manual devices in certain contexts ensure continued relevance. The base year for this analysis is 2025, providing a solid foundation for projecting future trends. Key market insights reveal a persistent preference for aneroid sphygmomanometers due to their cost-effectiveness and ease of use compared to mercury models, which are facing increasing regulatory restrictions due to environmental concerns. The market is segmented by type (aneroid and mercury) and application (hospitals, clinics, and physical examination centers), with hospitals currently holding the largest market share due to their high volume of patient examinations. However, the growth in the number of clinics and physical examination centers is expected to drive growth in these segments. The report further highlights regional variations, with developing economies experiencing faster growth due to increasing healthcare infrastructure development and rising healthcare awareness. Competitive analysis reveals a fragmented market with a mix of large multinational companies and smaller regional players. The ongoing innovation in design and features, such as improved accuracy and durability, further contributes to market expansion. Despite the emergence of electronic devices, the inherent advantages of manual sphygmomanometers – simplicity, affordability, and portability – maintain a strong position in the market. This report provides a comprehensive overview of the market dynamics, allowing stakeholders to make informed strategic decisions.

Several factors contribute to the continued demand for manual sphygmomanometers. Firstly, the relatively low cost compared to electronic counterparts makes them accessible to a broader range of healthcare providers, particularly in resource-constrained settings. Their simple design and ease of use translate to minimal training requirements for healthcare professionals, lowering operational costs. This is especially significant in areas with limited access to sophisticated medical technology. Secondly, manual devices offer a degree of portability unmatched by their electronic counterparts, crucial for home healthcare, mobile clinics, and emergency situations. Their reliability in off-grid scenarios is also a significant advantage. The absence of electronic components also eliminates concerns about battery life and power outages, making them dependable instruments in various settings. Finally, many healthcare professionals still prefer the tactile feedback provided by a manual sphygmomanometer, enhancing the accuracy of blood pressure measurement and the feel of the pulse. This hands-on experience allows for a more thorough patient assessment, potentially detecting subtle anomalies that electronic devices might miss. This combination of affordability, simplicity, reliability, and tactile feedback underscores the persistent relevance of manual sphygmomanometers in a constantly evolving healthcare landscape.

Despite the enduring demand, the manual sphygmomanometer market faces several challenges. The most significant is the increasing popularity of electronic sphygmomanometers, which offer automated readings, digital display, and data storage capabilities. While more expensive, these features enhance convenience and efficiency. The growing preference for digital health records further contributes to this shift, as electronic devices seamlessly integrate into such systems. Another significant constraint is the potential for human error in manual readings. Inaccurate readings caused by improper technique or subjective interpretation can affect diagnosis and treatment. Furthermore, the gradual phasing out of mercury sphygmomanometers due to environmental regulations presents a challenge for manufacturers and users. Finding suitable and safe alternatives that maintain the affordability and simplicity of mercury devices requires ongoing research and development. Finally, the market is characterized by intense competition, both from established players and new entrants. Maintaining a competitive edge requires constant innovation in design, materials, and features, while simultaneously adhering to strict quality and safety standards. These challenges require manufacturers to adapt and innovate to sustain their market share.

The aneroid sphygmomanometer segment is expected to dominate the market throughout the forecast period. This is due to several factors:

The Hospital application segment will continue to dominate due to the high volume of blood pressure measurements conducted in hospital settings. The large number of patients, regular monitoring requirements, and the diverse range of patients necessitate a high number of devices.

Geographically, developing economies in Asia-Pacific and Africa are projected to witness faster growth rates due to increased healthcare infrastructure development, rising healthcare awareness, and government initiatives to improve healthcare accessibility. Developed markets in North America and Europe will see steady growth, although at a slower pace than developing markets. The larger existing healthcare infrastructure and high adoption of electronic devices may contribute to this slower growth in established regions.

However, the overall market will be influenced by the transition from mercury to aneroid devices, creating fluctuations in different regional markets, depending on regulatory changes and market adoption rates.

Growth in the manual sphygmomanometer industry is fueled by increasing prevalence of hypertension globally, the rising demand for affordable healthcare solutions in developing countries, and the continued preference for manual devices due to their reliability and ease of use in specific clinical settings. The simplicity of these devices and the minimal training requirements for their operation continue to provide a cost-effective solution for many healthcare providers.

This report offers a detailed analysis of the manual sphygmomanometer market, providing valuable insights into market trends, growth drivers, challenges, and key players. It presents a comprehensive understanding of market segmentation, regional dynamics, and future projections, enabling stakeholders to make informed decisions and capitalize on growth opportunities within this evolving market. The report's projections extend to 2033, providing a long-term perspective on market evolution. The data presented is derived from extensive market research and analysis, ensuring accuracy and reliability.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.91% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12.91%.

Key companies in the market include Drive Medical, Honsun, Jiangsu Dengguan Medical Treatment Instrument, Jiangsu Folee Medical Equipment, Jiangsu Yuyue Medical Equipment & Supply Co., Ltd, MDF Instruments, Prestige Medical, Wuxi Medcare Instrument, AME Worldwide, American Diagnostic, Ciga Healthcare, Friedrich Bosch, .

The market segments include Type, Application.

The market size is estimated to be USD 10.43 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Manual Sphygmomanometer," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Manual Sphygmomanometer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.