1. What is the projected Compound Annual Growth Rate (CAGR) of the Manual Doctor Chair?

The projected CAGR is approximately 7.9%.

Manual Doctor Chair

Manual Doctor ChairManual Doctor Chair by Type (Electric, Manual), by Application (Hospital, Clinic, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

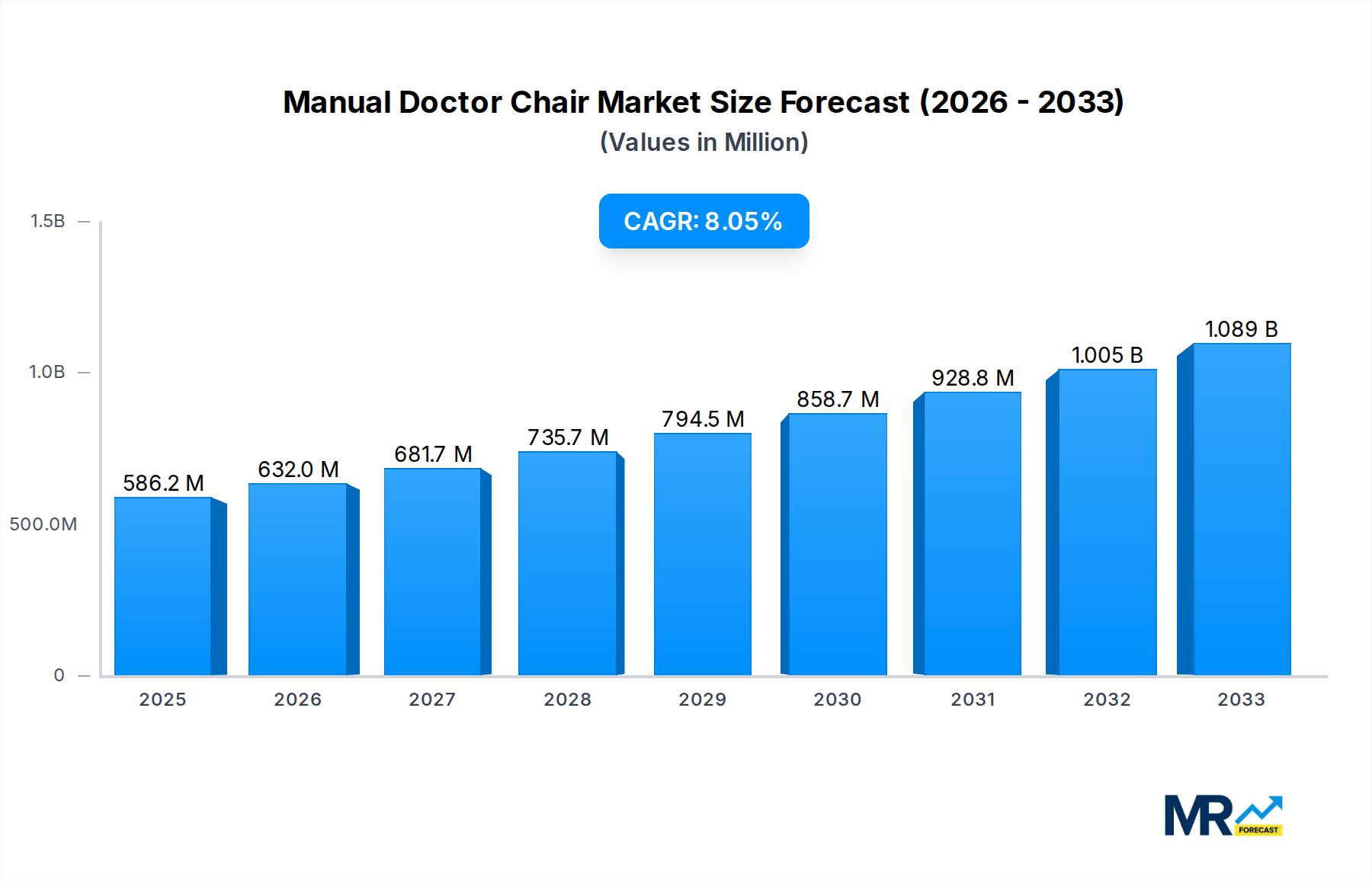

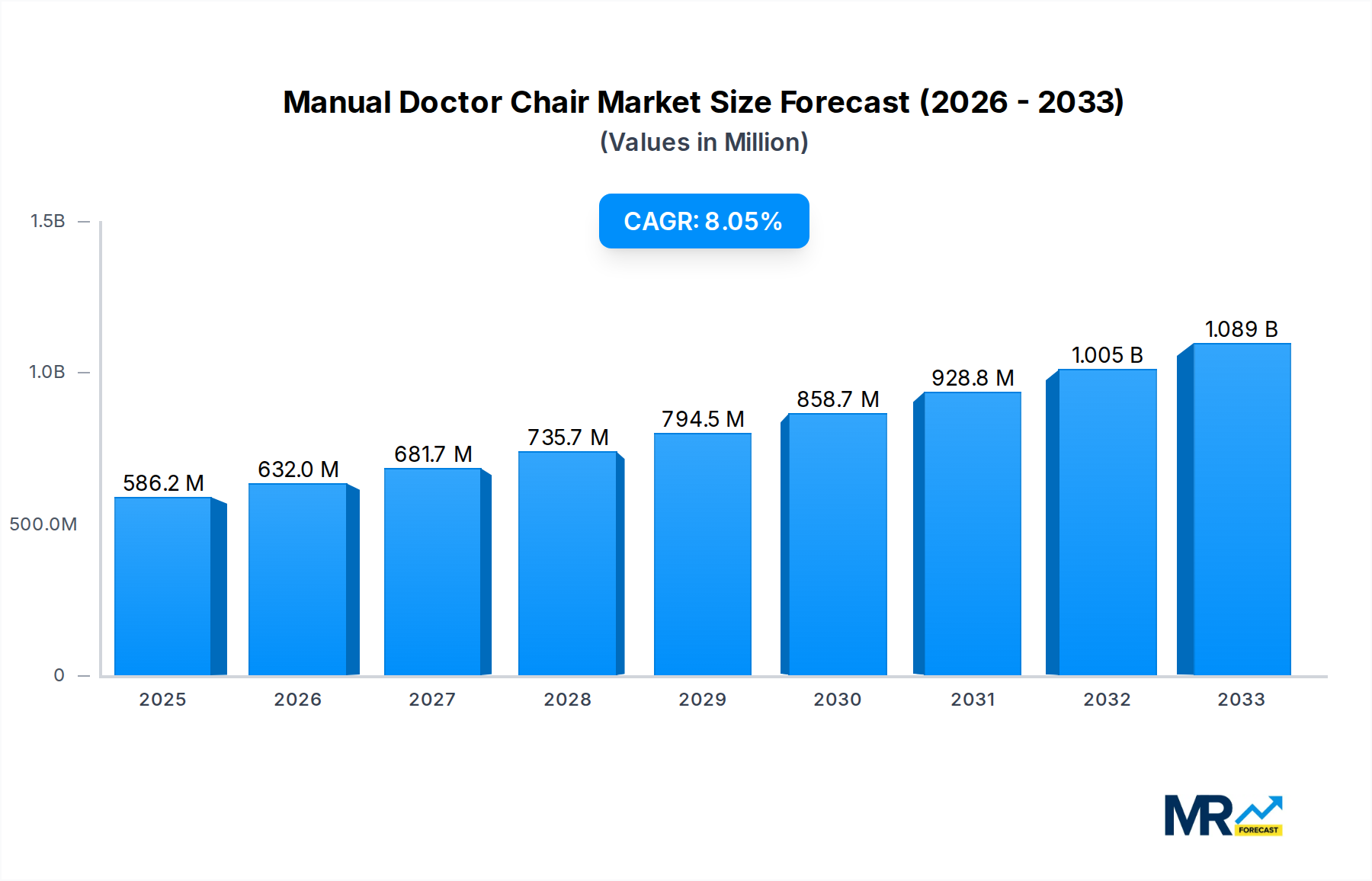

The global Manual Doctor Chair market is poised for robust expansion, projected to reach a significant valuation of USD 586.2 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 7.9% anticipated throughout the forecast period of 2025-2033. This sustained growth is primarily fueled by the increasing demand for efficient and cost-effective healthcare solutions, particularly in burgeoning economies and established healthcare facilities prioritizing patient comfort and practitioner ergonomics. The inherent simplicity and reliability of manual doctor chairs, coupled with their lower initial investment compared to electric counterparts, make them an attractive choice for a wide spectrum of medical settings, from large hospitals to smaller specialized clinics. Furthermore, ongoing advancements in design, incorporating enhanced adjustability and specialized functionalities, are continually improving the user experience and broadening the appeal of these essential medical instruments.

The market landscape for manual doctor chairs is characterized by a dynamic interplay of growth drivers and emerging trends. Key drivers include the expanding global healthcare infrastructure, a growing geriatric population requiring specialized care, and the continuous development of new medical facilities. The increasing prevalence of chronic diseases also necessitates more frequent and comfortable access to medical examinations, thereby stimulating demand. Trends such as the integration of antimicrobial materials for improved hygiene and the development of lightweight, portable designs for enhanced maneuverability are shaping product innovation. While the market demonstrates strong upward momentum, potential restraints such as the increasing adoption of advanced electric chairs in premium segments and stringent regulatory compliances in certain regions could present challenges. However, the fundamental utility and affordability of manual doctor chairs are expected to ensure their continued relevance and sustained market penetration.

This comprehensive report provides an in-depth analysis of the global Manual Doctor Chair market, offering a detailed examination of its trends, drivers, challenges, and future trajectory. The study encompasses a significant historical period from 2019 to 2024, with a detailed base year analysis for 2025 and an extensive forecast period extending from 2025 to 2033. The report leverages millions of units as its primary metric for market sizing and projections, providing a robust quantitative perspective.

The manual doctor chair market, while seemingly a niche segment, has demonstrated a remarkable resilience and continued relevance throughout the study period of 2019-2033. Despite the increasing adoption of electric and automated medical equipment, the inherent simplicity, cost-effectiveness, and reliability of manual doctor chairs continue to solidify their position in healthcare facilities globally. The market has witnessed a steady evolution, driven by a persistent demand for ergonomic designs that prioritize both patient comfort and practitioner efficiency. Early in the historical period (2019-2024), the focus was primarily on basic functionality and durability. However, as the market matured, manufacturers began incorporating more sophisticated design elements, such as adjustable height mechanisms, customizable backrests, and integrated storage solutions, all achievable within the manual framework. The base year of 2025 marks a point where a significant portion of the existing installed base is in need of upgrades or replacements, signaling a sustained demand. Moreover, the forecast period (2025-2033) is expected to see a continued emphasis on lightweight yet robust materials, contributing to easier maneuverability and reduced maintenance requirements. The integration of advanced upholstery materials, offering enhanced hygiene and patient comfort, is also a key trend. The market is not solely driven by replacement cycles; new healthcare infrastructure development, particularly in emerging economies, is a significant contributor. These regions often prioritize cost-effective solutions, making manual doctor chairs a logical choice for initial outfitting. Furthermore, specialized applications within clinics and smaller medical practices, where the advanced features of electric chairs might be considered overkill, continue to rely heavily on manual alternatives. The trend towards patient-centric care also subtly influences the market, with manufacturers striving to create chairs that facilitate better patient interaction and examination. The enduring appeal of manual doctor chairs lies in their proven track record, minimal operational complexity, and a lower initial investment, factors that are critically important in budget-conscious healthcare environments. The ability to offer a reliable and functional solution without the dependency on power sources also makes them indispensable in certain settings, ensuring uninterrupted service during power outages. This inherent dependability, coupled with ongoing design refinements, positions the manual doctor chair market for continued, albeit perhaps incremental, growth throughout the forecast horizon.

The sustained demand and projected growth for manual doctor chairs are propelled by a confluence of critical factors that underscore their enduring value in the healthcare ecosystem. Foremost among these is cost-effectiveness. In an era where healthcare providers are under immense pressure to manage budgets efficiently, manual doctor chairs present a significantly lower initial investment compared to their electric counterparts. This affordability makes them an attractive option for hospitals, clinics, and private practices, especially those in budget-constrained regions or those seeking to equip multiple examination rooms without substantial capital outlay. The simplicity of operation and maintenance also plays a pivotal role. Manual chairs require no electrical power, thus eliminating the associated energy costs and reducing the complexity of installation and upkeep. This translates into fewer potential points of failure, lower repair expenses, and less downtime, all of which are crucial for maintaining operational efficiency in a busy medical setting. Furthermore, the robustness and durability of well-manufactured manual chairs are highly valued. Their mechanical nature often makes them more resilient to the wear and tear of daily use in a demanding clinical environment. This longevity contributes to a lower total cost of ownership over time. The portability and ease of maneuverability offered by many manual doctor chair designs are also significant drivers. Lighter weight and the absence of power cords allow healthcare professionals to easily reposition chairs within examination rooms or move them between different areas as needed, enhancing workflow flexibility. Finally, the continued development and innovation in ergonomic design within the manual segment ensure that these chairs meet contemporary standards for patient comfort and practitioner support. Manufacturers are consistently refining mechanisms for height adjustment, backrest recline, and seat positioning, ensuring that manual chairs remain functional and comfortable for a wide range of medical procedures and patient needs.

Despite the inherent strengths, the manual doctor chair market is not without its significant challenges and restraints that could temper its growth trajectory throughout the study period of 2019-2033. The most prominent restraint is the increasing preference for automation and advanced features. As healthcare technology advances, there is a growing expectation from both practitioners and patients for more sophisticated and feature-rich equipment. Electric doctor chairs, with their precise, motorized adjustments, offer a level of ease and precision that manual chairs struggle to replicate. This can lead to perceived limitations in functionality, especially in specialized medical fields where intricate positioning is crucial. The limited adjustability and ergonomic compromises of some basic manual models can also be a drawback. While manufacturers are improving designs, certain manual chairs may still lack the fine-tuning capabilities necessary for optimal patient comfort and practitioner ergonomics during prolonged procedures. This can lead to practitioner fatigue and potentially impact the quality of patient care. Another significant challenge is the perception of being outdated. In a market increasingly driven by innovation and technological advancement, manual doctor chairs can sometimes be perceived as less modern or professional, particularly in high-end clinics or advanced medical institutions. This perception, while not always reflective of actual performance, can influence purchasing decisions. Furthermore, the growing emphasis on patient experience and comfort might also favor electric chairs that offer smoother and more effortless adjustments, contributing to a more positive patient perception. The labor costs associated with manual adjustments can also be a subtle restraint. While the chair itself is cheaper, the time and effort a practitioner expends on manual adjustments, especially in repetitive examination scenarios, could be considered a less efficient use of valuable clinical time. Finally, stringent regulatory requirements and evolving safety standards in the medical device industry can add to the cost and complexity of developing and certifying even manual chairs, potentially limiting the pace of innovation and increasing the barrier to entry for new players.

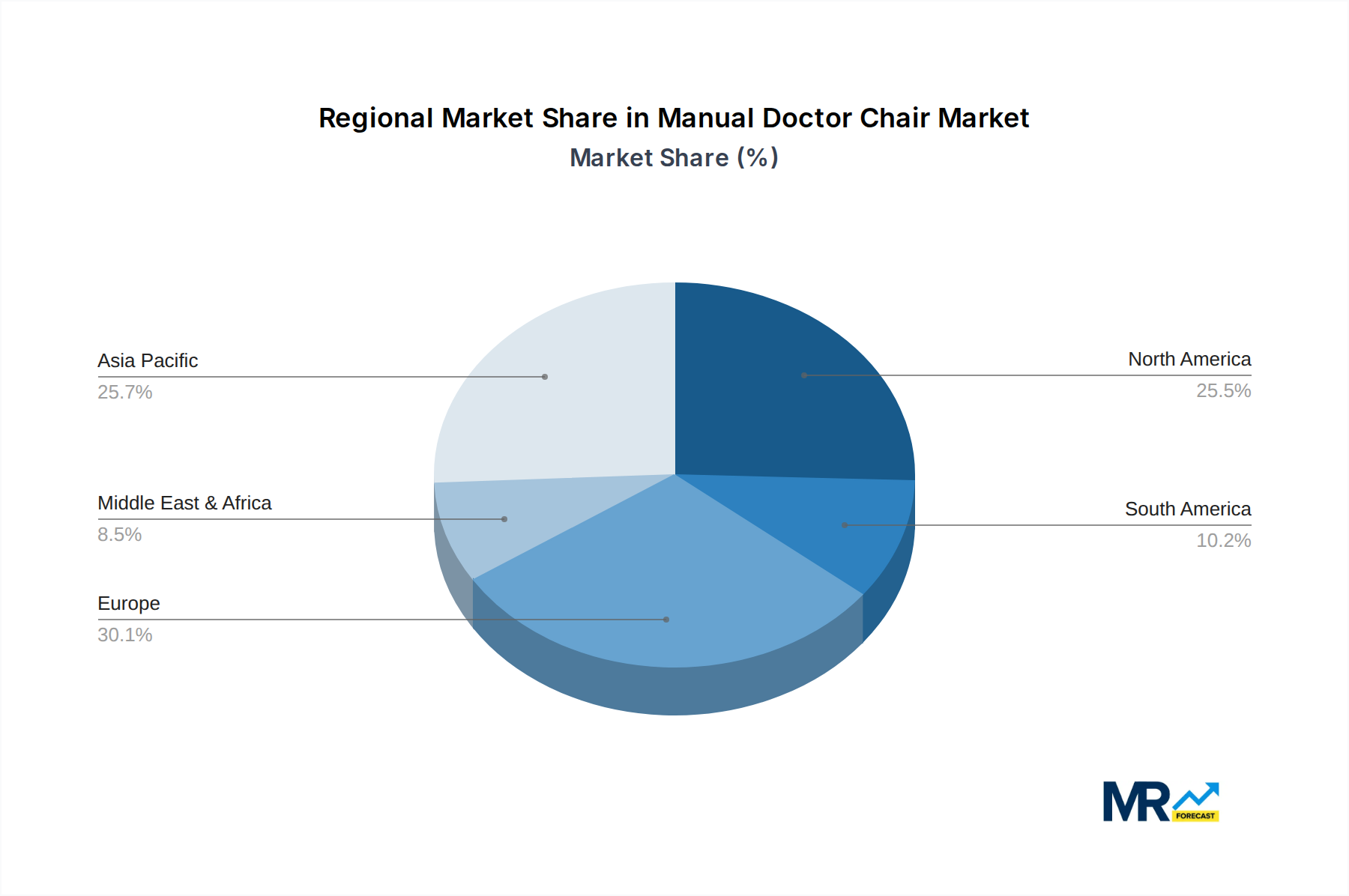

The Manual Doctor Chair market is poised for significant dominance by the Clinic segment, particularly within the Asia Pacific region. This dominance is driven by a multifaceted interplay of economic factors, healthcare infrastructure development, and the specific needs of emerging markets.

Dominant Segment: Clinic

Dominant Region/Country: Asia Pacific

While other regions like North America and Europe will continue to represent significant markets, their demand might be more tilted towards higher-end, electric models in certain segments. However, the sheer volume of clinic establishments and the ongoing healthcare expansion in the Asia Pacific, combined with the inherent advantages of manual doctor chairs in terms of cost and simplicity, will unequivocally position this region and the clinic segment as the dominant force in the global manual doctor chair market throughout the forecast period.

Several factors are acting as growth catalysts for the manual doctor chair industry, ensuring its continued relevance and expansion. The increasing emphasis on cost containment within healthcare systems globally is a primary driver, making the affordable nature of manual chairs a highly attractive proposition. Furthermore, the robust growth in emerging economies, characterized by expanding healthcare infrastructure and a rising demand for medical services, presents a significant opportunity. As these nations develop their healthcare networks, budget-friendly solutions like manual doctor chairs become essential for widespread adoption. The simplicity of operation and maintenance, requiring no electrical power, also serves as a key catalyst, particularly in regions with less developed power grids or during power outages. Finally, ongoing innovations in ergonomic design, focusing on improved comfort and adjustability within the manual framework, are helping to keep manual chairs competitive and appealing to healthcare professionals.

This report offers a holistic understanding of the manual doctor chair market, delving beyond simple market size figures to provide actionable insights. It meticulously analyzes the historical trends from 2019-2024, the current market landscape in the base year of 2025, and projects the future trajectory through an extensive forecast period of 2025-2033. Key segments like Type (Electric, Manual) and Application (Hospital, Clinic, Others) are examined in detail, with a particular focus on identifying and elaborating on the dominance of specific segments and regions. Industry developments, key drivers, and significant challenges are thoroughly explored, providing a nuanced view of the market dynamics. The report also includes a comprehensive list of leading players and significant recent developments, offering a strategic perspective for stakeholders aiming to navigate and capitalize on opportunities within this evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.9%.

Key companies in the market include ATMOS MedizinTechnik, JOSON-CARE ENTERPRISE, Narang Medical, Medifa GmbH & Co. KG., Capron Podologie, Foshan Medco Medical eequipment, Gardhen Bilance, IntraSpace, MRIMED, Tangshan UMG Medical Instrument, Medik Medical, .

The market segments include Type, Application.

The market size is estimated to be USD 586.2 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Manual Doctor Chair," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Manual Doctor Chair, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.