1. What is the projected Compound Annual Growth Rate (CAGR) of the Lithium-Ion Battery Recycling Production Lines?

The projected CAGR is approximately 14.6%.

Lithium-Ion Battery Recycling Production Lines

Lithium-Ion Battery Recycling Production LinesLithium-Ion Battery Recycling Production Lines by Type (Capacity:<500 Kg/h, Capacity:500-1000 Kg/h, Capacity:1000-2000 Kg/h, World Lithium-Ion Battery Recycling Production Lines Production ), by Application (Electronic Products, Power Battery, Chemicals, Others, World Lithium-Ion Battery Recycling Production Lines Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

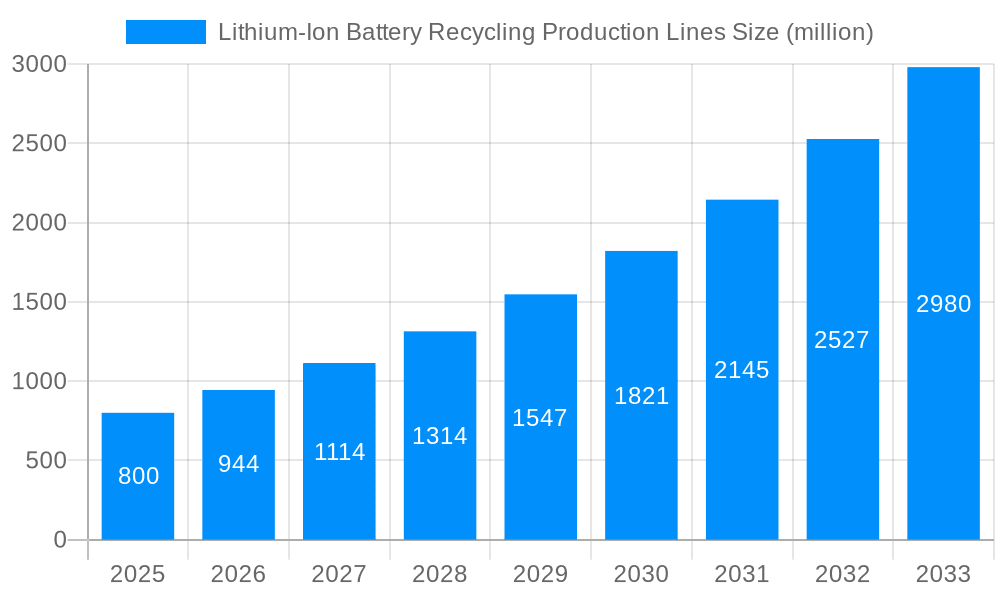

The global market for Lithium-Ion Battery Recycling Production Lines is poised for substantial expansion, projected to reach an estimated USD 800 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 18% anticipated from 2025 to 2033. This robust growth is primarily fueled by the escalating demand for electric vehicles (EVs) and the increasing adoption of renewable energy storage systems, both of which generate a significant volume of end-of-life lithium-ion batteries requiring responsible recycling. Stringent environmental regulations and government incentives worldwide are further accelerating the development and deployment of advanced recycling technologies. The market is witnessing a surge in investments towards establishing efficient and scalable production lines capable of handling diverse battery chemistries and capacities. Key players are focusing on technological innovation to improve recovery rates of valuable materials like cobalt, nickel, and lithium, thereby enhancing the economic viability of battery recycling and contributing to a circular economy.

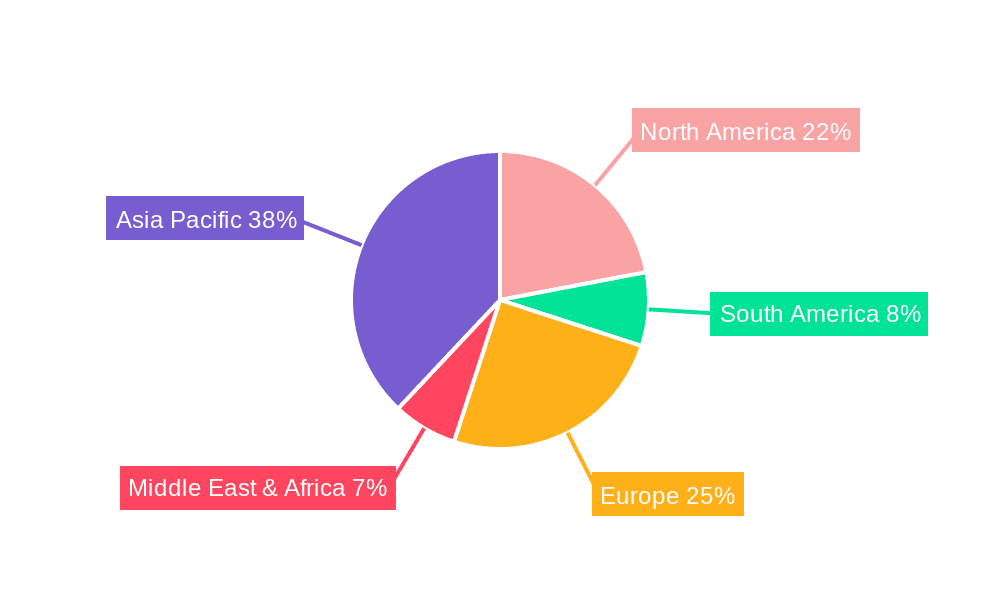

The market is segmented across various battery capacities, with lines designed for handling capacities between 500-1000 Kg/h and 1000-2000 Kg/h expected to dominate due to the increasing size of EV battery packs. Application-wise, the power battery segment is the primary driver, followed by electronic products. Geographically, Asia Pacific, particularly China, is leading the market due to its expansive EV manufacturing base and supportive government policies. North America and Europe are also exhibiting strong growth, driven by similar trends and a growing commitment to sustainability. However, challenges such as the complexity of battery disassembling, safety concerns associated with handling damaged batteries, and the fluctuating prices of recovered materials can pose restraints. Nevertheless, ongoing research and development into more efficient and cost-effective recycling processes, alongside strategic collaborations between battery manufacturers, recyclers, and technology providers, are expected to overcome these hurdles and solidify the market's upward trajectory.

The global landscape of Lithium-Ion Battery (LIB) recycling production lines is undergoing a profound transformation, driven by an escalating demand for sustainable resource management and the burgeoning electric vehicle (EV) market. This report delves into the intricate trends shaping this vital industry from the historical period of 2019-2024, through the estimated base year of 2025, and projecting forward to 2033. A critical insight is the accelerating shift towards high-capacity production lines, particularly those in the 1000-2000 Kg/h range, which are becoming increasingly crucial for handling the sheer volume of retired power batteries. These advanced lines are no longer niche; they represent the future of efficient and economical LIB recycling. The market's trajectory also points towards a significant concentration on power battery applications, as the number of EVs on the road continues to surge, creating a substantial influx of end-of-life battery packs. This demand is directly fueling investments in sophisticated recycling technologies that can safely and effectively extract valuable materials like lithium, cobalt, nickel, and manganese. Furthermore, a growing emphasis on circular economy principles is prompting a move away from simple shredding to more integrated processes that include pre-treatment, mechanical separation, and hydrometallurgical or pyrometallurgical refining. Companies are recognizing that the future value lies not just in disposal, but in the recovery and reintegration of these critical raw materials back into the battery supply chain.

The technological evolution of LIB recycling production lines is marked by several key trends:

The exponential growth of the electric vehicle (EV) market is the undeniable primary driver for the surge in demand for Lithium-Ion Battery (LIB) recycling production lines. As millions of EVs transition from their operational lifespan, a colossal volume of spent batteries will require responsible and efficient end-of-life management. This impending wave of battery waste, coupled with the increasing scarcity and geopolitical sensitivities surrounding key raw materials like lithium, cobalt, and nickel, is creating a compelling economic and environmental imperative for robust recycling infrastructure. Governments worldwide are implementing stricter regulations and offering incentives to encourage battery recycling, further accelerating investment in this sector. The concept of a circular economy, aiming to minimize waste and maximize resource utilization, is no longer a theoretical ideal but a practical necessity, with LIB recycling at its core. This shift in mindset, from linear consumption to circular resource management, is fundamentally altering how industries view and invest in battery end-of-life solutions, making recycling production lines a strategic priority for numerous stakeholders.

Key factors propelling the growth include:

Despite the robust growth trajectory, the Lithium-Ion Battery (LIB) recycling production lines sector faces significant hurdles that could impede its full potential. A paramount challenge lies in the variability and complexity of battery chemistries and designs. The rapid evolution of battery technology means that recycling facilities must constantly adapt to different materials, cell formats, and safety features, which complicates the development of standardized, one-size-fits-all recycling lines. Furthermore, the high initial capital investment required for state-of-the-art recycling plants, encompassing advanced shredding, separation, and refining equipment, can be a substantial barrier for new entrants and smaller operators. Logistics and collection infrastructure for spent batteries also present a considerable challenge; efficiently gathering, transporting, and safely storing batteries from diverse sources across vast geographical areas requires significant coordination and investment. Safety concerns during the dismantling and processing of potentially hazardous LIBs, due to their stored energy and flammable electrolytes, necessitate stringent safety protocols and specialized equipment, adding to operational costs and complexity. Finally, economic viability remains a persistent concern, as the fluctuating prices of recovered materials and the cost of the recycling process itself can make it difficult to compete with the cost of virgin materials, especially when market prices for critical minerals are low.

Key challenges and restraints include:

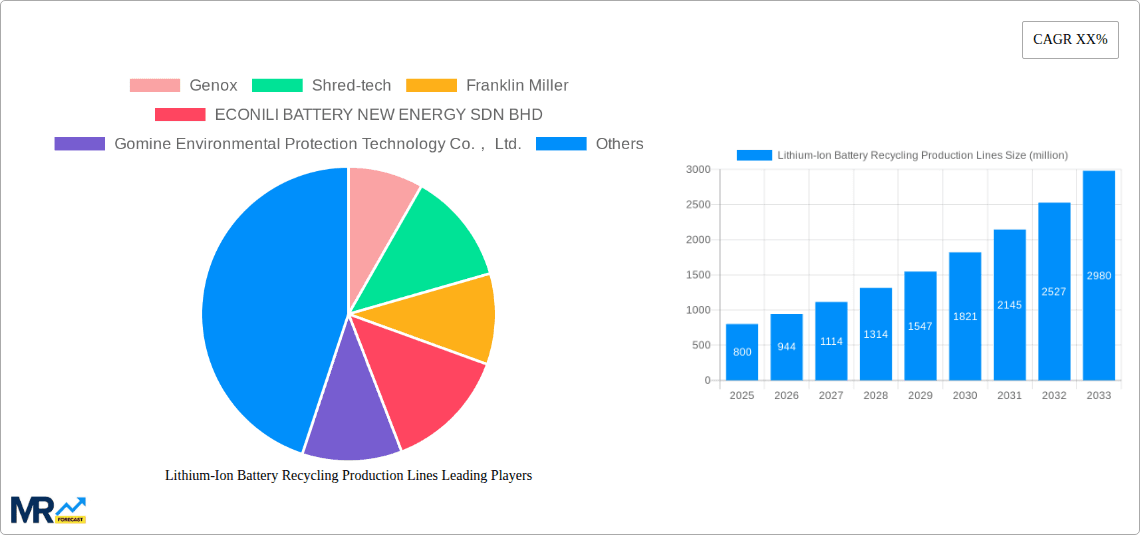

The dominance in the global Lithium-Ion Battery (LIB) recycling production lines market is poised to be significantly influenced by a confluence of factors, leading to distinct regional and segmental strengths. Asia Pacific, particularly China, is expected to emerge as a dominant force. This supremacy stems from several interconnected elements: China's unparalleled position as the world's largest producer and consumer of electric vehicles, creating a vast and growing pool of end-of-life batteries. Coupled with this is the Chinese government's proactive industrial policy, which has heavily supported the development of a comprehensive LIB recycling ecosystem, including substantial investments in advanced recycling technologies and production lines. Leading companies within China, such as Gongyi Xingmao Machinery Co., Ltd., Henan Renewable Energy Technology Co.,Ltd, and Xiamen TMAX Battery Equipments Ltd., have been instrumental in developing and deploying a wide range of recycling equipment and integrated production lines. These companies cater to various capacity segments, from smaller <500 Kg/h lines for specialized applications to large-scale 1000-2000 Kg/h facilities crucial for processing the immense volume of power batteries.

Within the segmentation of production lines, the 1000-2000 Kg/h capacity segment is projected to witness the most significant growth and dominance. This is directly attributable to the overwhelming need to process the massive influx of retired power batteries from EVs. The sheer volume necessitates highly efficient, high-throughput recycling operations. Companies like Genox, Shred-tech, and Franklin Miller are actively innovating in this segment, offering robust and scalable solutions that can handle the demands of industrial-scale battery recycling. These advanced lines are equipped with sophisticated pre-treatment capabilities, high-capacity shredders, and integrated separation systems designed to maximize material recovery and minimize processing time. The application focus within this dominant segment is undeniably on Power Battery recycling. As EVs continue to proliferate, the recycling of their high-capacity power units will be the primary driver for the deployment of these larger production lines. While electronic products also contribute to battery waste, the scale and volume generated by the power battery sector far outweigh it.

In addition to the Asia Pacific region, Europe is also demonstrating strong growth, driven by stringent environmental regulations, a commitment to circular economy principles, and ambitious EV adoption targets. Countries like Germany, France, and the Netherlands are actively investing in and developing advanced LIB recycling capabilities. Companies such as XRIDO and Vanest Machinery Co.,Ltd are contributing to the European market with their innovative solutions. North America, particularly the United States, is also a significant and growing market, fueled by increasing EV sales and governmental initiatives aimed at establishing a domestic battery supply chain, which includes recycling. Companies like ECONILI BATTERY NEW ENERGY SDN BHD and Gomine Environmental Protection Technology Co., Ltd. are playing roles in these emerging markets, though the established infrastructure and scale in China currently place it in a leading position. The continued innovation by companies like Suny Group, Kerui Machinery, Weborn Technology, and Zhengzhou Dingshuo Machinery Manufacturing Co., Ltd. across various segments will further shape the competitive landscape and the overall dominance of specific regions and segments in the coming years.

The expansion of the Lithium-Ion Battery (LIB) recycling production lines industry is significantly catalyzed by government mandates and incentives, such as Extended Producer Responsibility (EPR) schemes and favorable subsidies, which make recycling economically more attractive and operationally feasible. The rapid advancement of recycling technologies, leading to improved material recovery rates and reduced processing costs, is another key growth driver. Furthermore, the growing global commitment to achieving net-zero emissions and fostering a circular economy creates a strong demand for sustainable resource management, positioning LIB recycling as a critical component of this transition. The increasing investment from both public and private sectors, recognizing the strategic importance of a secure and domestically sourced supply of critical battery metals, is also fueling rapid growth and innovation in production line development.

1000-2000 Kg/h capacity production lines in China to meet the growing demand for power battery recycling.This comprehensive report offers an in-depth analysis of the global Lithium-Ion Battery (LIB) recycling production lines market, meticulously examining trends from 2019 to 2033. It provides granular insights into market drivers, including the surging demand from the electric vehicle sector and increasing environmental consciousness, alongside critical challenges such as technical complexities and economic viability. The report details leading companies and their contributions, significant technological advancements, and regional market dynamics, with a particular focus on the dominance of Asia Pacific, especially China, and the burgeoning 1000-2000 Kg/h capacity segment catering primarily to power battery applications. With detailed segmentation by capacity, application, and technology, this report is an indispensable resource for stakeholders seeking to understand the current landscape and future trajectory of this vital industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.6% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 14.6%.

Key companies in the market include Genox, Shred-tech, Franklin Miller, ECONILI BATTERY NEW ENERGY SDN BHD, Gomine Environmental Protection Technology Co., Ltd., Suny Group, Gongyi Xingmao Machinery Co., Ltd., Henan Renewable Energy Technology Co.,Ltd, Xiamen TMAX Battery Equipments Ltd., XRIDO, Vanest Machinery Co.,Ltd, Zhengzhou Dingshuo Machinery Manufacturing Co., Ltd., Kerui Machinery, Weborn Technology.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Lithium-Ion Battery Recycling Production Lines," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Lithium-Ion Battery Recycling Production Lines, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.