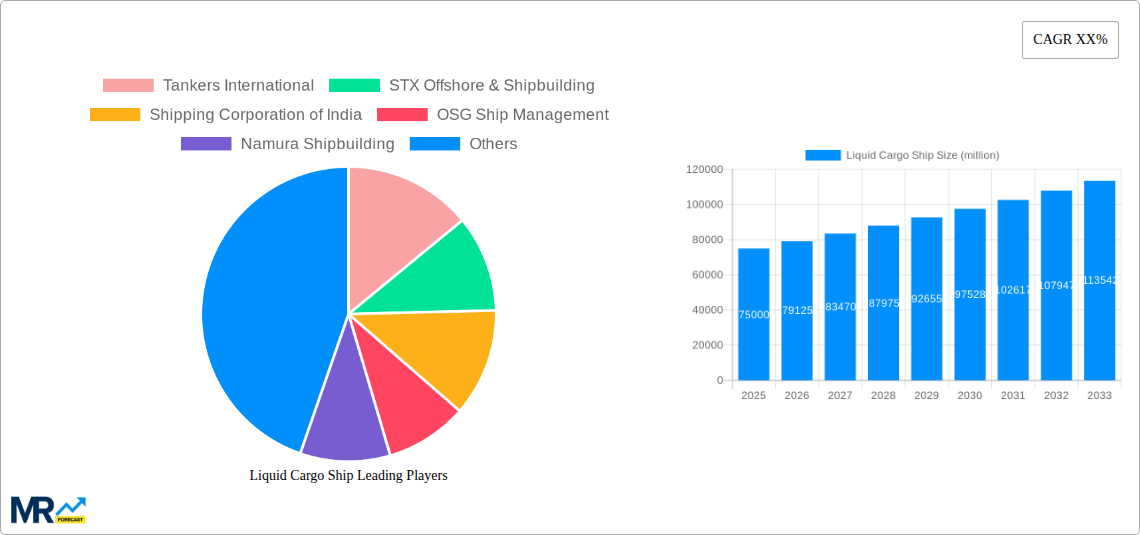

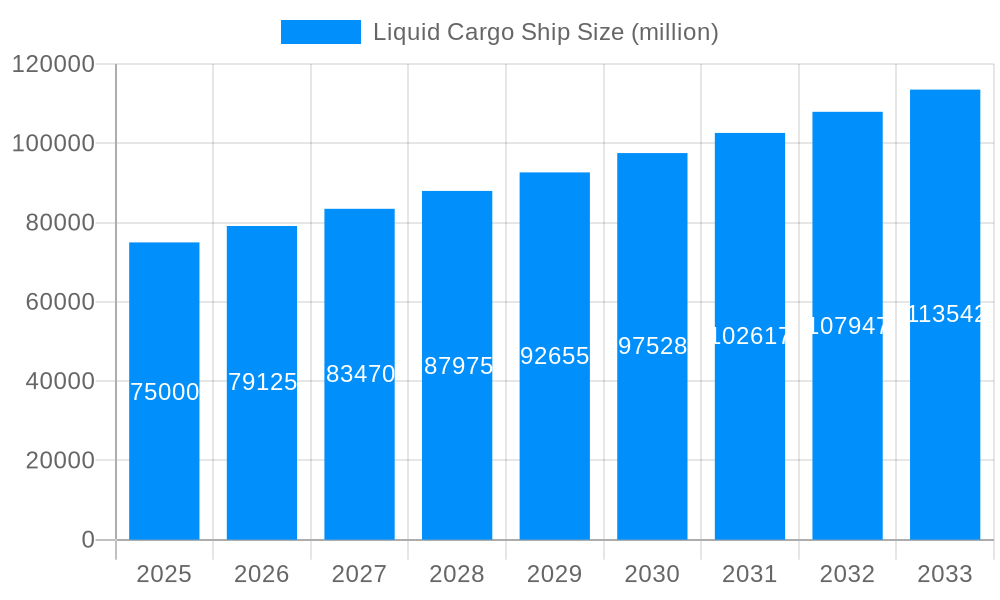

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Cargo Ship?

The projected CAGR is approximately 3.7%.

Liquid Cargo Ship

Liquid Cargo ShipLiquid Cargo Ship by Type (Tanker, Liquefied Gas Ship, Liquid Chemical Gas Tanker, World Liquid Cargo Ship Production ), by Application (Crude Oil and Refined Oil, Liquefied Natural Gas and Liquefied Petroleum Gas, Liquid Chemicals, World Liquid Cargo Ship Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global liquid cargo ship market is projected for robust expansion, driven by escalating energy demands and evolving international trade dynamics. With an estimated market size of $1,000 billion and a projected Compound Annual Growth Rate (CAGR) of 3.7% from 2025 to 2033, significant growth is anticipated. Key growth catalysts include rising consumption of crude oil and refined products, particularly in emerging economies, alongside increasing trade of liquefied natural gas (LNG) and liquefied petroleum gas (LPG), spurred by global decarbonization initiatives and energy security imperatives. The expanding production and trade of liquid chemicals also fuel this upward trend, necessitating a growing and specialized tanker fleet. Advancements in shipbuilding, prioritizing efficiency, safety, and environmental compliance, further bolster this trajectory, ensuring adherence to increasingly stringent regulations.

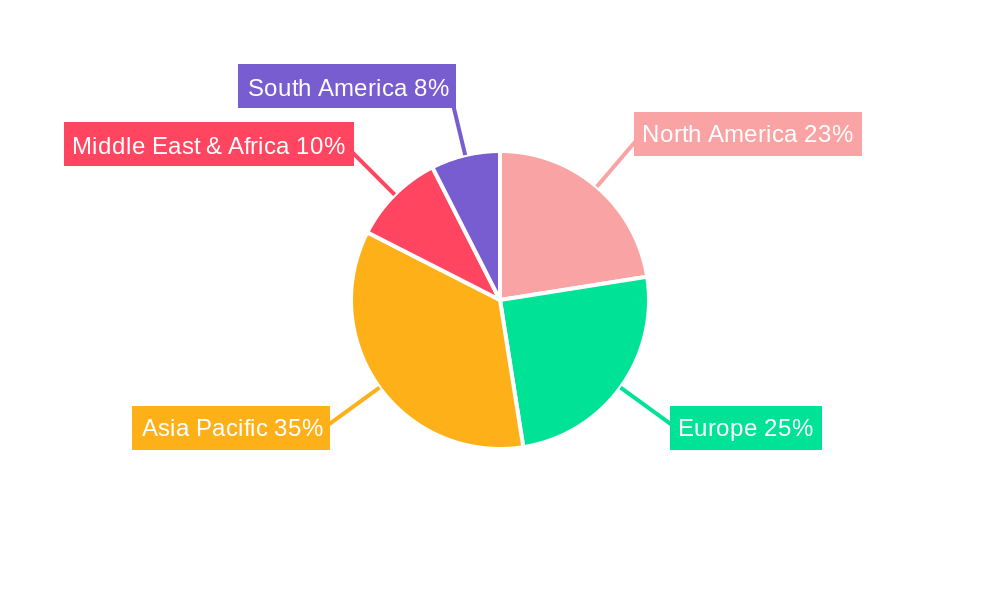

Market segmentation indicates that Tanker vessels will maintain dominance in crude oil and refined oil transportation. However, the Liquefied Gas Ship segment, comprising LNG and LPG carriers, is experiencing the most rapid growth due to the global transition to cleaner energy sources and expanding gas liquefaction and regasification infrastructure. Liquid Chemical Tankers are also rising in importance with the growth and diversification of the chemical industry. Geographically, Asia Pacific, led by China and India, is expected to be the largest and fastest-expanding market, driven by industrial growth and energy needs. North America and Europe will remain substantial markets due to established energy infrastructure and trade volumes. Potential restraints include oil price volatility, geopolitical instability affecting trade routes, and significant capital expenditure for new builds, though the overall market outlook remains strong, supported by essential global trade flows.

The global liquid cargo ship market, a critical artery for international trade, is projected for robust expansion throughout the study period of 2019-2033. The market, valued in the billions of dollars, is witnessing a significant shift in demand driven by evolving energy landscapes and increasing global consumption patterns. The World Liquid Cargo Ship Production segment is particularly dynamic, reflecting advancements in shipbuilding technology and the increasing complexity of the cargoes being transported. Key market insights reveal a sustained demand for Tankers carrying Crude Oil and Refined Oil, particularly as global refining capacities and oil consumption continue to grow, especially in emerging economies. This segment is expected to maintain its dominance, contributing a substantial portion to the overall market value, estimated to reach figures well into the hundreds of millions of dollars annually.

However, the Liquefied Gas Ship segment, encompassing both Liquefied Natural Gas (LNG) and Liquefied Petroleum Gas (LPG), is experiencing even more accelerated growth. This surge is directly correlated with the global transition towards cleaner energy sources. Nations are increasingly investing in LNG infrastructure and imports to reduce reliance on coal and other polluting fuels, thereby driving the need for specialized LNG carriers. Similarly, LPG demand for both industrial and domestic use continues to climb across various continents. The Liquid Chemical Gas Tanker segment, while smaller in volume, is also exhibiting impressive growth, driven by the expanding petrochemical industry and the increasing global trade of specialized chemicals. The sophisticated design and safety features of these vessels are paramount, influencing their market value. The World Liquid Cargo Ship Production is not just about volume but also about technological innovation, with a focus on efficiency, environmental compliance, and advanced cargo handling systems. This trend is reshaping the shipbuilding landscape, with companies like Daewoo Shipbuilding & Marine Engineering and Samsung Heavy Industries at the forefront of developing next-generation vessels. The overall market trajectory indicates a healthy upward trend, supported by predictable demand patterns and ongoing investments in the maritime sector.

The liquid cargo ship market is experiencing a significant upswing, primarily propelled by the inexorable growth in global energy demand and the evolving geopolitical landscape surrounding energy security. The increasing reliance on Liquefied Natural Gas (LNG) as a cleaner alternative to fossil fuels is a paramount driver. Nations worldwide are actively pursuing LNG imports to diversify their energy portfolios and meet stringent environmental regulations, thereby fueling the demand for a larger and more specialized fleet of LNG carriers. This trend is further amplified by significant investments in LNG regasification terminals and liquefaction plants, creating a robust ecosystem for LNG transportation. Alongside LNG, the demand for Liquefied Petroleum Gas (LPG) continues its upward trajectory, driven by its widespread use in both developing and developed economies for residential, commercial, and industrial purposes.

Furthermore, the continuous need for Crude Oil and Refined Oil transportation remains a foundational pillar of the liquid cargo ship market. Despite the global push towards renewable energy, the world's dependence on oil for transportation, industry, and petrochemical production ensures a sustained demand for crude oil tankers. Emerging economies, in particular, are witnessing increased consumption, necessitating greater import volumes and thus, more vessel capacity. The expansion of refining capacities globally also contributes to this demand, as processed fuels need to be transported efficiently. The steady expansion of the petrochemical industry, requiring the transport of various Liquid Chemicals, also adds to the market's momentum, showcasing the diverse and essential role of liquid cargo vessels in the global supply chain.

Despite the robust growth prospects, the liquid cargo ship industry is not without its considerable challenges and restraints. One of the most significant hurdles is the stringent and ever-evolving environmental regulations imposed by international bodies and individual nations. The International Maritime Organization's (IMO) mandates on sulfur emissions (IMO 2020) and the ongoing discussions and implementation plans for decarbonization are forcing shipowners and operators to invest heavily in new technologies, such as scrubbers, alternative fuels, or the retrofitting of existing vessels. This capital expenditure can be substantial, impacting profitability and potentially slowing down fleet expansion for smaller players.

Another major restraint is the cyclical nature of the shipping industry itself, characterized by periods of oversupply and undersupply, which directly influence freight rates and vessel values. Market volatility, influenced by geopolitical events, global economic downturns, and fluctuations in commodity prices, can create uncertainty and deter significant new investments. The sheer capital intensity of building and operating large liquid cargo vessels, with individual new builds costing hundreds of millions of dollars, presents a significant barrier to entry. Furthermore, the availability of skilled labor for operating and maintaining these sophisticated vessels, particularly those designed for hazardous cargoes like LNG and chemicals, can be a constraint. The geopolitical tensions in key shipping lanes and potential disruptions to trade routes also pose a risk, impacting the efficient and cost-effective movement of liquid cargoes.

The global liquid cargo ship market is characterized by distinct regional dominance and segment leadership. From a regional perspective, Asia-Pacific is emerging as a powerhouse, primarily driven by China, South Korea, and Japan, which are not only major consumers of liquid commodities but also leading shipbuilding nations.

Among the segments, the Tanker segment, specifically those carrying Crude Oil and Refined Oil, is expected to continue its significant market share. However, the Liquefied Gas Ship segment, particularly for Liquefied Natural Gas (LNG), is poised for the most substantial growth.

While the Asia-Pacific region and the LNG segment are set for remarkable growth, it is crucial to acknowledge the continued importance of the crude oil and refined oil tanker segment. The interplay between these segments and regions will shape the overall trajectory of the liquid cargo ship market. The World Liquid Cargo Ship Production capabilities of nations like South Korea and China will be pivotal in meeting the burgeoning demand for both types of vessels.

Several key factors are acting as significant growth catalysts for the liquid cargo ship industry. The most prominent is the global energy transition, which is driving unprecedented demand for Liquefied Natural Gas (LNG) as a cleaner alternative to fossil fuels. This necessitates a continuous expansion of the LNG carrier fleet. Furthermore, the sustained global demand for crude oil and refined products, particularly from rapidly developing economies, ensures ongoing requirements for tanker capacity. Advancements in shipbuilding technology, leading to more fuel-efficient and environmentally compliant vessels, also act as a catalyst, encouraging fleet modernization and investment. The expansion of petrochemical industries worldwide further boosts demand for specialized chemical tankers.

This report offers a comprehensive analysis of the global liquid cargo ship market, meticulously examining trends and future projections from 2019 to 2033. It delves into the market's valuation, expected to reach hundreds of millions of dollars annually, highlighting the dominance of Tankers carrying Crude Oil and Refined Oil, while forecasting exceptional growth for Liquefied Gas Ships, particularly LNG Carriers. The report details the driving forces, including the global energy transition and rising energy demands, and addresses the significant challenges such as stringent environmental regulations and market volatility. It identifies key regions like Asia-Pacific and dominant segments like LNG transport, while also profiling leading global players and their strategic moves. This in-depth research provides invaluable insights for stakeholders seeking to navigate and capitalize on the evolving landscape of the liquid cargo shipping industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.7%.

Key companies in the market include Tankers International, STX Offshore & Shipbuilding, Shipping Corporation of India, OSG Ship Management, Namura Shipbuilding, Mitsubishi Heavy Industries, Meyer Werft, Meyer Turku, Maersk Tankers, Kuwait Oil Tankers, Keystone Alaska, Kawasaki Heavy Industries, Hyundai Samho Heavy Industries, Essar Shipping, Damen Shipyard, Daewoo Shipbuilding & Marine Engineering, China State Shipbuilding Corporation, Barkmeijer Stroobos BV, Alaska Tanker, Wartsila, Mitsui O.S.K. Lines, Samsung Heavy Industries, Sirius Shipping, GasLog Ltd, Dynagas Ltd, Royal Dutch Shell Plc, .

The market segments include Type, Application.

The market size is estimated to be USD 1000 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Liquid Cargo Ship," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Liquid Cargo Ship, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.