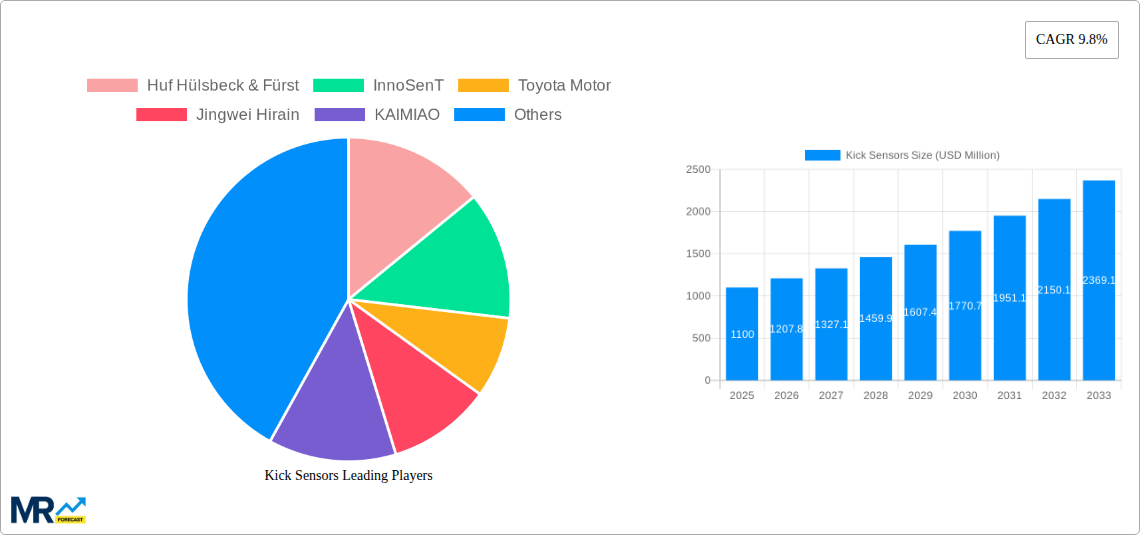

1. What is the projected Compound Annual Growth Rate (CAGR) of the Kick Sensors?

The projected CAGR is approximately 9.8%.

Kick Sensors

Kick SensorsKick Sensors by Type (OEM, Aftermarket, World Kick Sensors Production ), by Application (Passenger Car, Commercial Vehicle, World Kick Sensors Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

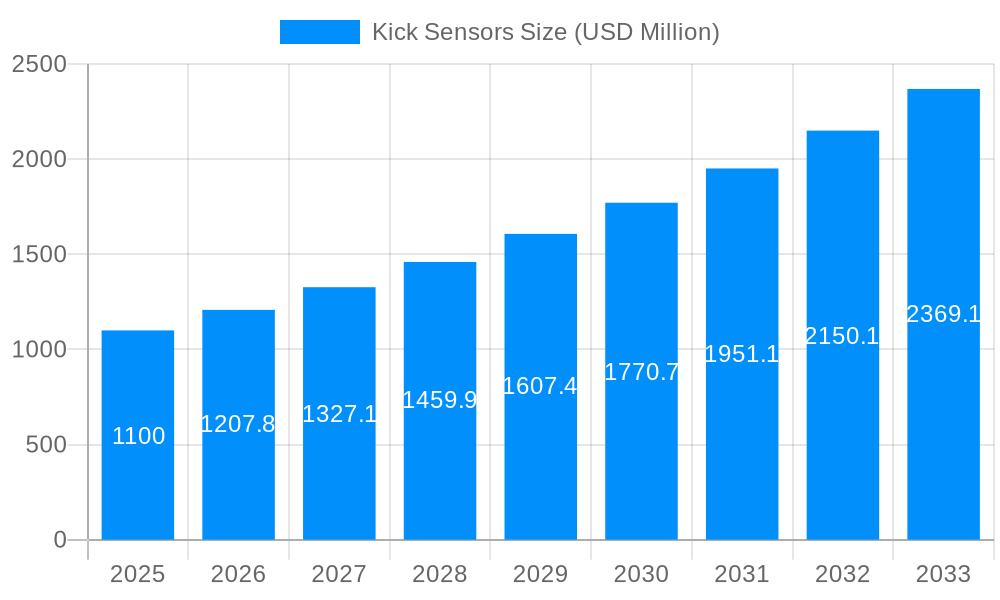

The global Kick Sensors market is poised for substantial expansion, projected to reach approximately $1.1 billion in 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of 9.8% throughout the forecast period. This significant growth is fueled by the increasing integration of advanced driver-assistance systems (ADAS) in vehicles and the rising demand for enhanced vehicle security and convenience features. Kick sensors, which enable hands-free tailgate or trunk operation, are becoming increasingly prevalent in both passenger and commercial vehicles, driven by consumer preference for modern automotive technology. The market's expansion is further bolstered by evolving consumer expectations for seamless and intuitive vehicle interaction, making kick sensor technology a key differentiator for automakers.

The market is segmented into OEM and Aftermarket types, with the OEM segment expected to dominate due to the direct integration of kick sensors during vehicle manufacturing. Key drivers include the growing automotive industry, particularly in emerging economies, and the continuous innovation in sensor technology leading to improved performance and reliability. Restraints such as the initial cost of integration and the complexity of installation in older vehicles are present but are expected to be mitigated by economies of scale and advancements in aftermarket solutions. Leading companies like Huf Hülsbeck & Fürst, InnoSenT, and Toyota Motor are actively investing in research and development, pushing the boundaries of this technology and shaping the competitive landscape. Regional analysis indicates strong growth opportunities across North America, Europe, and Asia Pacific, with China and India emerging as particularly dynamic markets due to their burgeoning automotive sectors and increasing adoption of smart vehicle features.

This report provides an in-depth analysis of the global Kick Sensors market, encompassing its historical performance, current landscape, and future projections. The study spans a comprehensive period from 2019 to 2033, with a base year of 2025 for accurate estimations. We delve into the intricate dynamics shaping this vital automotive component sector, examining production volumes, technological advancements, and the evolving demands of various vehicle segments. The analysis is meticulously structured to offer a clear understanding of market trends, driving forces, challenges, and the strategic positioning of key industry players.

The global Kick Sensors market is poised for substantial expansion, with projections indicating a significant surge in production and adoption over the study period. Throughout the historical period (2019-2024), the market witnessed steady growth, driven by the increasing integration of convenience and safety features in vehicles. The base year of 2025 marks a pivotal point, where the market is expected to achieve a production volume in the billions of units, reflecting its maturing yet rapidly evolving nature. Looking ahead into the forecast period (2025-2033), the market is anticipated to continue its upward trajectory, propelled by advancements in sensor technology, including improved accuracy, miniaturization, and cost-effectiveness. The demand for kick sensors is intrinsically linked to the broader automotive industry, with a notable correlation to the production of passenger cars, which represent the largest application segment. As automakers increasingly focus on enhancing user experience and streamlining vehicle access, the integration of kick sensors for features like hands-free tailgate operation and smart trunk access is becoming a standard expectation rather than a luxury. This trend is further amplified by the growing popularity of SUVs and Crossovers, vehicles often equipped with larger, heavier tailgates that benefit significantly from the convenience offered by kick sensor technology. The aftermarket segment, while smaller than the OEM sector, is also demonstrating robust growth as consumers seek to retrofit their existing vehicles with these modern conveniences. The development of more sophisticated algorithms for sensor interpretation, coupled with advancements in materials science for more durable and weather-resistant sensors, will further underpin market growth. The global average selling price (ASP) of kick sensors is expected to gradually decline due to economies of scale and technological advancements, making them more accessible to a wider range of vehicle models and price points. The competitive landscape is characterized by a mix of established automotive component suppliers and specialized sensor manufacturers, all vying to capture market share through innovation and strategic partnerships. The increasing regulatory focus on vehicle safety and user-friendliness also indirectly supports the growth of kick sensor adoption, as they contribute to a more intuitive and secure vehicle interaction. The market's resilience is also evident in its ability to adapt to evolving vehicle architectures, including the rise of electric vehicles (EVs), where space optimization and seamless integration of features are paramount. The ongoing R&D efforts are focused on developing next-generation kick sensors with enhanced detection capabilities, reduced false positives, and improved energy efficiency, ensuring their continued relevance and indispensability in the automotive sector.

The burgeoning demand for Kick Sensors is primarily driven by a confluence of factors that enhance vehicle functionality and user convenience. The increasing consumer preference for hands-free operations, particularly for cargo access in SUVs and hatchbacks, is a paramount driver. As vehicles become more sophisticated, the expectation for seamless and intuitive interactions with their features has risen significantly. Kick sensors, by enabling effortless opening and closing of tailgates with a simple foot gesture, directly address this demand, offering a superior user experience compared to manual operations. Furthermore, the ongoing drive for automotive innovation and the integration of advanced driver-assistance systems (ADAS) indirectly fuel the kick sensor market. Automakers are continuously seeking to differentiate their offerings by incorporating smart features, and kick sensors are a relatively cost-effective yet high-impact addition. The growing production volume of passenger cars globally, especially in emerging economies, also serves as a substantial propellant for kick sensor adoption. As vehicle ownership increases, so does the market for these convenience-enhancing components. The development of more robust and reliable sensor technologies, coupled with declining manufacturing costs, makes them an increasingly viable option for a wider range of vehicle models, from premium to mass-market segments.

Despite the promising growth trajectory, the Kick Sensors market faces several hurdles that could temper its expansion. One significant restraint is the potential for false positives or negatives, where the sensor may activate inadvertently or fail to detect the intended gesture. This can lead to user frustration and, in some cases, safety concerns, prompting a need for continuous technological refinement and robust validation processes. The cost of integration, while decreasing, can still be a barrier for some entry-level vehicle segments or for the aftermarket, especially when considering the additional electronics and programming required for seamless operation. Moreover, the susceptibility of sensors to environmental factors such as extreme temperatures, moisture, and dirt can impact their performance and longevity, necessitating the use of durable and high-quality components, which in turn can affect overall system cost. The competitive nature of the automotive industry also exerts pressure on pricing, forcing manufacturers to optimize production costs without compromising on quality. The evolving regulatory landscape, while often a driver for safety features, could also introduce new compliance requirements that necessitate further R&D investment. Finally, the ongoing development of alternative hands-free access technologies, such as gesture control systems integrated into the vehicle's interior or exterior body panels, could present future competition, although kick sensors currently offer a specific and well-understood user interface.

The global Kick Sensors market is characterized by a significant dominance of the OEM (Original Equipment Manufacturer) segment and the Passenger Car application, with Asia Pacific emerging as the leading region.

Dominant Segments:

Type: OEM Segment: The OEM segment is the bedrock of the kick sensor market, consistently outperforming the aftermarket. In 2025, the OEM segment is projected to account for well over 80% of the global kick sensor production volume. This dominance is attributable to several key factors. Firstly, automakers are increasingly embedding kick sensors as standard or optional features in new vehicle models to enhance user convenience and differentiate their products in a highly competitive market. The integration of these sensors is often planned from the initial design phase of a vehicle, ensuring seamless integration with the vehicle's electrical systems, body control modules, and software. Companies like Toyota Motor, a major global automaker, are instrumental in driving this demand by incorporating kick sensors across a wide array of their passenger car and commercial vehicle lines. The drive for a premium user experience, particularly in segments like SUVs and luxury vehicles, directly translates to higher OEM demand. The economies of scale achieved through mass production for OEMs also contribute to the segment's strength, making it more cost-effective for manufacturers to integrate these sensors. As the automotive industry continues its push towards electrification and autonomous driving, the demand for sophisticated, user-friendly interfaces, including hands-free access systems, will only intensify, further solidifying the OEM segment's leading position. The forecast period (2025-2033) will see continued OEM dominance, with innovations in sensor technology and integration making them even more compelling for automakers. The production volume in the OEM segment in 2025 is estimated to reach several billion units.

Application: Passenger Car: Passenger cars represent the largest application for kick sensors, driven by their widespread production volumes and the growing demand for convenience features. In 2025, passenger cars are anticipated to consume over 75% of the total kick sensor production. The increasing popularity of SUVs, crossovers, and hatchbacks, which often feature larger tailgates, makes kick sensors an invaluable addition for effortless cargo access. Consumers are increasingly accustomed to and expect these modern conveniences, making them a key factor in purchasing decisions. The global proliferation of passenger vehicles, particularly in emerging markets, directly fuels the demand for kick sensors. Companies like Toyota Motor, as a leading manufacturer of passenger vehicles, play a pivotal role in this segment's growth. The ability to open and close a trunk or tailgate with a simple foot gesture enhances the overall ownership experience, especially for families or individuals with their hands full. The continued evolution of vehicle design and the integration of smart technologies further bolster the position of passenger cars as the primary application for kick sensors. The production volume for passenger cars in 2025 is expected to be in the billions of units.

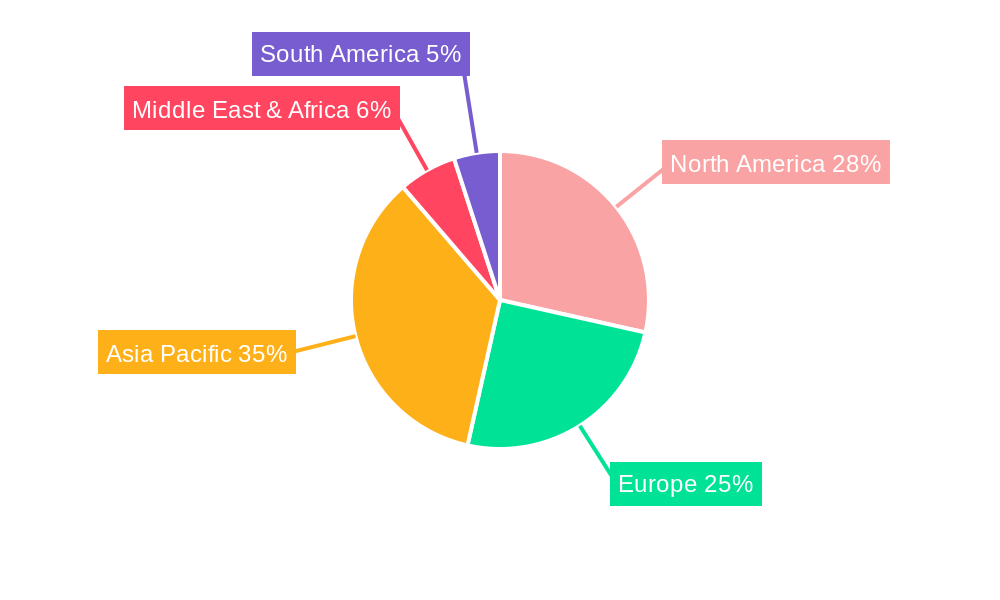

Key Region: Asia Pacific: The Asia Pacific region, encompassing countries like China, Japan, South Korea, and India, is the dominant force in the global kick sensor market. This dominance is largely attributed to the region's position as the world's largest automotive manufacturing hub and a massive consumer market for vehicles. China, in particular, is a colossal producer and consumer of automobiles, with its burgeoning automotive industry driving substantial demand for all automotive components, including kick sensors. The presence of major automotive manufacturers and a rapidly growing middle class with increasing disposable income fuels the adoption of vehicles equipped with advanced features. The significant production volumes of passenger cars and commercial vehicles in this region directly translate into a high demand for kick sensors from OEM manufacturers. Furthermore, the region is home to several key kick sensor manufacturers, fostering a competitive environment that drives innovation and cost-effectiveness. The ongoing technological advancements and the focus on smart mobility solutions within Asia Pacific further reinforce its leadership in the kick sensor market. The projected production volume from this region in 2025 is estimated to contribute significantly to the global billions of units metric.

The growth of the Kick Sensors industry is significantly propelled by the increasing consumer demand for enhanced vehicle convenience and hands-free functionalities. As automakers strive to differentiate their offerings, the integration of smart features like hands-free tailgate access, facilitated by kick sensors, has become a key selling point. The continuous advancements in sensor technology, leading to improved accuracy, miniaturization, and cost-effectiveness, are making kick sensors more accessible for integration into a wider range of vehicle models across all price segments. Furthermore, the expanding global automotive market, particularly in emerging economies, translates into higher vehicle production volumes, thereby creating a larger installed base for kick sensors.

This comprehensive report offers an unparalleled deep dive into the global Kick Sensors market, meticulously detailing its intricate dynamics. Spanning a detailed study period from 2019 to 2033, with a precise base year of 2025, the analysis provides robust historical data, current market valuations, and forward-looking projections. It dissects the market by segments, including OEM and Aftermarket, and applications such as Passenger Cars and Commercial Vehicles, offering granular insights into each. The report thoroughly examines global production volumes, estimated to reach several billion units by 2025, and forecasts its trajectory through 2033. It uncovers the key driving forces and critical growth catalysts shaping the industry, alongside a candid assessment of the challenges and restraints that influence market expansion. Furthermore, it identifies dominant regions and countries poised for significant market share and provides an exhaustive list of leading players and their notable developments. This report is an indispensable resource for stakeholders seeking a strategic advantage in the dynamic kick sensors landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.8%.

Key companies in the market include Huf Hülsbeck & Fürst, InnoSenT, Toyota Motor, Jingwei Hirain, KAIMIAO, Changyi Auto Parts, Hansshow, NAEN Auto Technology, Corepine, Microstep, Whetron Electronics, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Kick Sensors," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Kick Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.