1. What is the projected Compound Annual Growth Rate (CAGR) of the IV Connector Without Needle?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

IV Connector Without Needle

IV Connector Without NeedleIV Connector Without Needle by Type (Positive Fluid Displacement, Negative Fluid Displacement, Neutral Displacement, World IV Connector Without Needle Production ), by Application (Infusion, Transfusion of Blood, Blood Collection, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

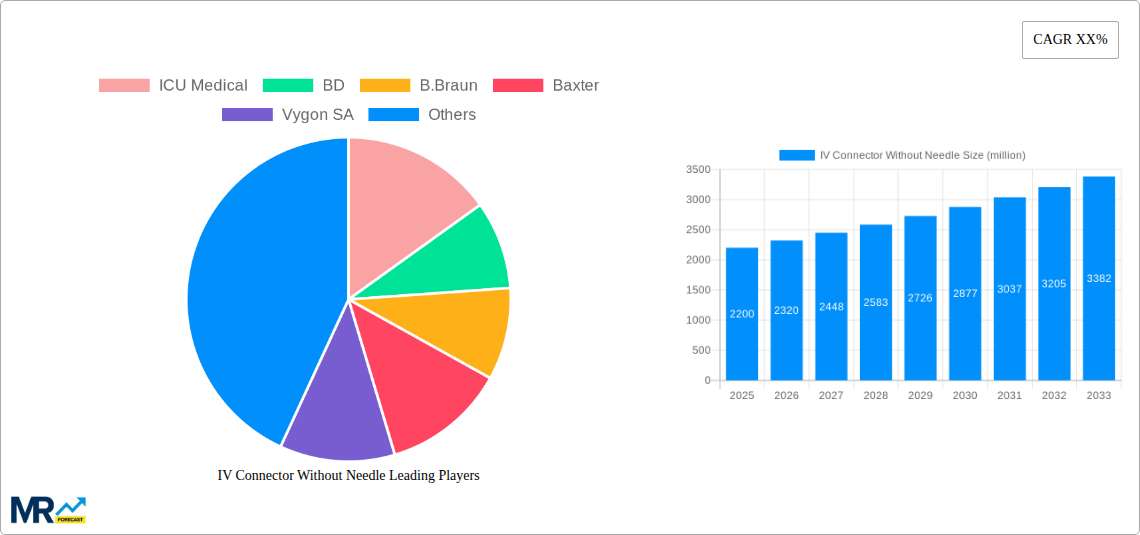

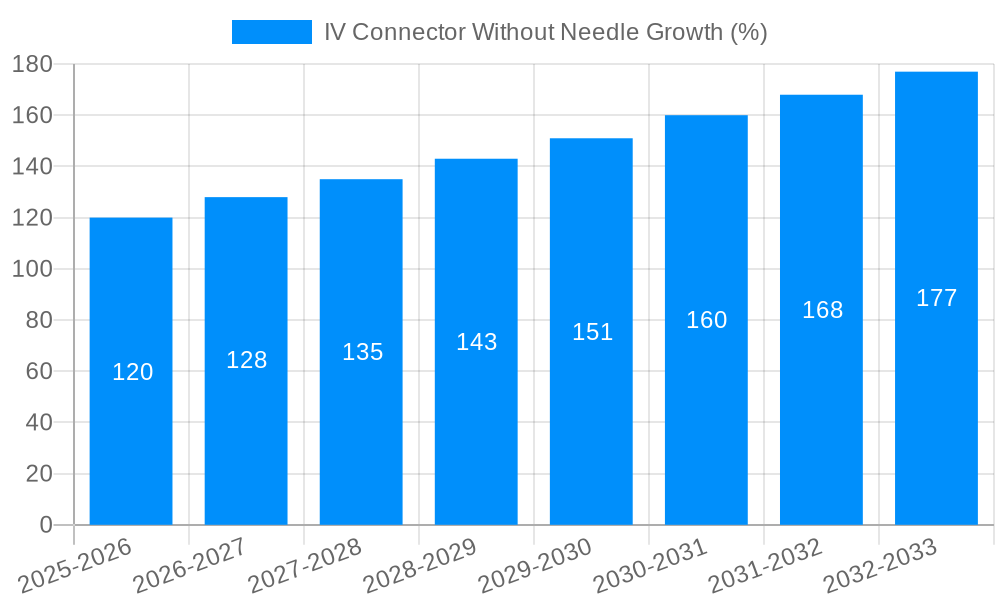

The IV Connector Without Needle market is experiencing robust growth, driven by the increasing prevalence of chronic diseases requiring intravenous therapy, a rising geriatric population susceptible to infections, and the growing preference for safer, less invasive medical devices. The market, estimated at $1.5 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 7% from 2025 to 2033, reaching approximately $2.8 billion by 2033. This growth is fueled by technological advancements leading to improved connector designs with enhanced safety features like needle-free access, minimizing the risk of needle-stick injuries for healthcare professionals and patients. The infusion therapy segment dominates the application landscape, owing to its widespread use in hospitals and clinics for administering fluids, medications, and nutrition. Positive fluid displacement technology currently holds the largest market share among the different types of connectors, but negative displacement technologies are gaining traction due to their potential for improved safety and reduced risk of contamination. Competition in this market is intense, with key players including ICU Medical, BD, B. Braun, Baxter, Vygon SA, Medtronic, and others focusing on product innovation, strategic partnerships, and geographic expansion to secure market share. Regional growth is expected to be particularly strong in developing economies of Asia Pacific and the Middle East & Africa, driven by increasing healthcare infrastructure investments and rising healthcare expenditure.

The restraints to market growth include stringent regulatory approvals, high initial investment costs for advanced technologies, and potential pricing pressures due to the increasing number of market entrants. However, the long-term outlook remains positive, particularly with the continuing focus on improving patient safety and the ongoing development of innovative needle-free connector technologies designed to reduce infection rates and improve the efficiency of intravenous therapy. The market segmentation by type (positive, negative, and neutral displacement) and application (infusion, transfusion, blood collection, other) allows for a targeted approach by manufacturers to meet the specific needs of different healthcare settings and procedures. Further market penetration will rely on effective marketing strategies targeting both healthcare professionals and patients, highlighting the benefits of needle-free connectors in terms of safety, convenience, and cost-effectiveness.

The global IV connector without needle market is experiencing robust growth, projected to reach multi-million unit sales by 2033. Driven by advancements in medical technology and an increasing demand for safer and more efficient intravenous therapies, this market segment is witnessing significant expansion across various applications and geographical regions. The historical period (2019-2024) showed steady growth, laying the foundation for the impressive forecast period (2025-2033). Our base year of 2025 provides a crucial benchmark for understanding the current market dynamics and projecting future trends. Key market insights reveal a strong preference for needle-free connectors due to their reduced risk of needlestick injuries, improved patient safety, and ease of use for healthcare professionals. The market is characterized by increasing adoption in hospitals and clinics worldwide, particularly in developed nations with robust healthcare infrastructures. The rising prevalence of chronic diseases requiring long-term intravenous therapy further fuels this growth. Innovation in connector designs, including advancements in materials and functionalities, also contributes significantly to market expansion. Competition among key players is driving down costs and improving product quality, making needle-free IV connectors more accessible and affordable. Furthermore, regulatory approvals and stringent safety standards are promoting the adoption of these devices, creating a positive growth trajectory for the foreseeable future. The estimated year 2025 shows a marked increase in market value compared to previous years, signaling the continued upward trend. The market is also witnessing increased investment in research and development, driving the development of new and improved products.

Several factors are propelling the growth of the IV connector without needle market. The foremost driver is the significant reduction in the risk of needlestick injuries. Healthcare professionals are exposed to numerous needle-related risks daily, leading to infections and other complications. Needle-free connectors mitigate these risks substantially, improving workplace safety and reducing healthcare costs associated with needle-related injuries and infections. Additionally, patient safety is significantly enhanced; needle-free systems minimize the risk of accidental needle sticks during procedures or post-procedure handling. The increasing prevalence of chronic diseases requiring frequent intravenous therapy, such as cancer and diabetes, is a major driver. These conditions necessitate frequent IV access, making needle-free connectors a more convenient and safer alternative. The rising demand for minimally invasive procedures further fuels the market's growth. Needle-free connectors are seamlessly integrated into minimally invasive procedures, improving patient outcomes and recovery times. Furthermore, technological advancements leading to improved designs, more durable materials, and enhanced functionalities are attracting healthcare providers to adopt these connectors. Finally, the increasing awareness among healthcare professionals and patients regarding the benefits of needle-free systems contributes to the market's expansion.

Despite its significant growth potential, the IV connector without needle market faces several challenges. The high initial cost of these devices compared to traditional needle-based connectors can be a barrier to adoption, particularly in resource-constrained settings. Furthermore, the perceived complexity of using some needle-free connectors can deter healthcare professionals from adopting them readily. Although safer, some needle-free connectors may require specific training, posing a challenge for their widespread implementation. Another factor is the potential for complications, although rare, associated with needle-free connectors, such as leaks or malfunctions. Rigorous quality control and adherence to stringent manufacturing standards are essential to address this issue. Finally, regulatory approvals and compliance with varying international standards can be complex and time-consuming for manufacturers, impacting market entry and expansion. Addressing these challenges through improved design, cost reduction strategies, and robust training programs is crucial for driving market growth further.

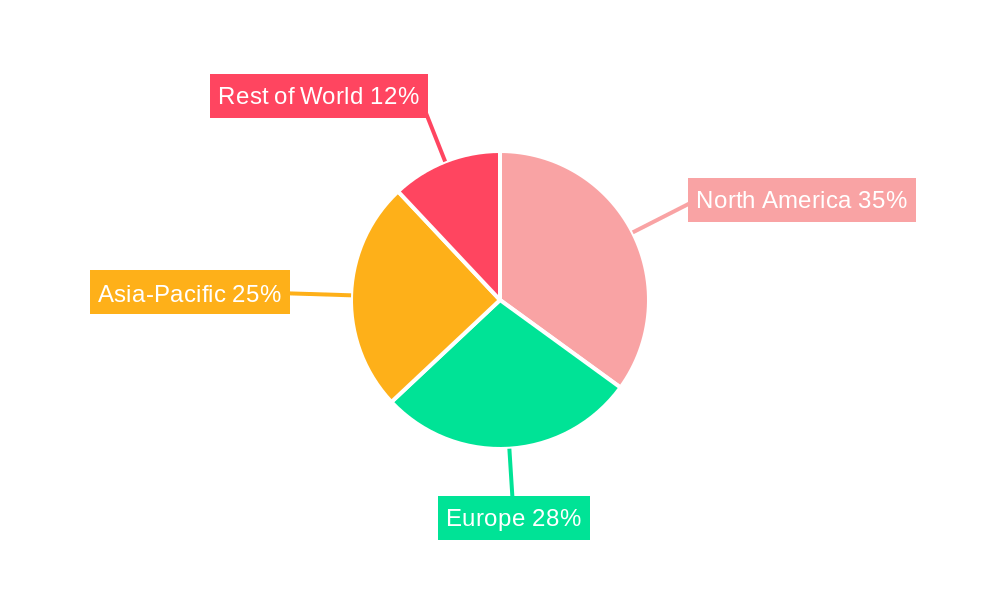

The North American market is expected to dominate the IV connector without needle market throughout the forecast period (2025-2033). This is driven by high healthcare expenditure, advanced medical infrastructure, and stringent safety regulations promoting the adoption of safer medical devices. Europe is expected to follow closely, exhibiting strong growth due to a similar landscape of well-established healthcare systems and a rising focus on patient safety.

Segment Domination: The Positive Fluid Displacement segment is projected to hold the largest market share due to its reliability, ease of use, and proven effectiveness in various applications. Positive displacement ensures accurate and consistent fluid delivery, making it a preferred choice for critical intravenous therapies.

Regional Breakdown:

Further Analysis of Positive Fluid Displacement: This segment's dominance is linked to its precision and the reduced risk of complications associated with other types of displacement. Its suitability for various applications, including infusion and blood transfusion, further enhances its market share. The consistent and reliable fluid delivery mechanism offered by positive fluid displacement systems makes them highly sought after by hospitals and clinics seeking improved patient outcomes and reduced medical errors. The segment's continued growth is expected to be influenced by technological advancements that improve the efficiency and safety of these devices.

The IV connector without needle industry is experiencing robust growth due to several key factors. Increased awareness of needlestick injuries and their associated risks, coupled with rising demand for safer medical practices, are driving widespread adoption. Technological advancements leading to more efficient and user-friendly needle-free systems also contribute significantly. Stringent regulatory approvals and safety standards are further promoting the market expansion, building consumer and healthcare provider confidence in these innovative devices.

This report provides a comprehensive overview of the IV connector without needle market, analyzing historical trends, current market dynamics, and future growth projections. It offers detailed insights into market segmentation by type (positive, negative, neutral displacement), application (infusion, transfusion, blood collection, other), and geography. The report identifies key market drivers, challenges, and opportunities, as well as profiles leading players and their strategic initiatives. This detailed analysis equips stakeholders with valuable information for informed decision-making in this rapidly expanding sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include ICU Medical, BD, B.Braun, Baxter, Vygon SA, Medtronic, Nexus Medical, Baihe Medical, Specath, RyMed Technologies.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "IV Connector Without Needle," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the IV Connector Without Needle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.