1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Metal Detectors?

The projected CAGR is approximately 3.0%.

Industrial Metal Detectors

Industrial Metal DetectorsIndustrial Metal Detectors by Type (Metal Detector with Conveyor, Rectangular Aperture Metal Detector, Gravity Fall Metal Detector, Pipeline Liquid, Paste and Slurry Metal Detector), by Application (Food Industry, Pharmaceutical Industry, Textiles Industry, Mining and Plastic Industry, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Industrial Metal Detectors market is poised for steady expansion, projected to reach a valuation of approximately $779 million by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 3.0% through the forecast period ending in 2033. This growth is underpinned by the increasing demand for stringent quality control and product safety across a diverse range of industries. The core function of metal detectors – to identify and remove metallic contaminants from production lines – remains paramount. Key drivers for this market include the escalating stringency of regulatory standards, particularly in the food and pharmaceutical sectors, where even microscopic metal fragments can pose significant health risks and lead to costly recalls. Furthermore, advancements in detection technology, offering enhanced sensitivity, faster processing speeds, and improved integration capabilities with existing manufacturing systems, are propelling market adoption. The growing emphasis on automation and Industry 4.0 principles within manufacturing environments also contributes to the uptake of sophisticated metal detection systems, which are vital for ensuring uninterrupted and efficient production processes.

The market is segmented into various detector types, including Metal Detector with Conveyor, Rectangular Aperture Metal Detector, Gravity Fall Metal Detector, and Pipeline Liquid, Paste and Slurry Metal Detector, catering to specific application needs. The Food Industry represents a dominant segment due to the inherent risks of metallic contamination in processed foods, followed closely by the Pharmaceutical Industry, where product purity is non-negotiable. The Textiles and Mining and Plastic Industries also present substantial growth opportunities as they adopt more rigorous quality assurance measures. Geographically, the Asia Pacific region, led by China and India, is expected to witness robust growth owing to rapid industrialization and a burgeoning manufacturing base. North America and Europe remain significant markets, driven by established industries with high quality standards and ongoing technological innovation. Restraints such as the initial capital investment for advanced systems and the need for skilled personnel for operation and maintenance are being gradually mitigated by the long-term benefits of reduced product spoilage, enhanced brand reputation, and compliance with global safety regulations.

Here is a comprehensive report description for Industrial Metal Detectors, incorporating the provided information and adhering to your formatting requests:

This report delves into the dynamic global market for Industrial Metal Detectors, providing an in-depth analysis of its historical performance, current landscape, and future trajectory. The study spans a comprehensive period from 2019 to 2033, with a dedicated focus on the base year of 2025, estimated figures for the same year, and detailed projections for the forecast period of 2025-2033. It builds upon an extensive historical analysis from 2019-2024. The market is valued in millions of units, offering a granular perspective on unit sales and adoption rates across various industrial sectors.

The global industrial metal detector market is currently experiencing a robust and upward trend, driven by an escalating emphasis on product safety, quality control, and regulatory compliance across a myriad of industries. Over the Study Period (2019-2033), and particularly within the Forecast Period (2025-2033), the market is projected to witness significant expansion. A key insight is the increasing integration of advanced sensor technologies and artificial intelligence (AI) into metal detection systems, enabling higher sensitivity, better differentiation between ferrous and non-ferrous metals, and improved detection of even minute metallic contaminants. The Base Year (2025) reflects a mature yet rapidly evolving market, where established players are investing heavily in R&D to offer more sophisticated and user-friendly solutions. The Estimated Year (2025) further solidifies this trajectory, indicating consistent growth in unit sales. The Historical Period (2019-2024) laid the groundwork for this expansion, characterized by a growing awareness of the financial and reputational damage associated with product recalls due to metallic contamination. Furthermore, the rise of smart manufacturing and Industry 4.0 initiatives is fostering the adoption of interconnected metal detection systems that can seamlessly integrate with other production line machinery for real-time data analysis and process optimization. This trend is particularly pronounced in sectors like food and pharmaceuticals, where consumer health and safety are paramount. The increasing complexity of manufacturing processes and the use of diverse materials also contribute to the demand for versatile and adaptable metal detection solutions. The market is also seeing a surge in demand for customized solutions tailored to specific application requirements, ranging from the detection of microscopic metal fragments in pharmaceuticals to larger metallic debris in mining operations. This adaptability ensures that metal detectors remain an indispensable tool for maintaining the integrity and quality of manufactured goods.

The industrial metal detectors market is being propelled by a confluence of powerful factors that underscore the critical role these systems play in modern manufacturing. Foremost among these is the unwavering global commitment to stringent food safety regulations. Governments and international bodies are continuously reinforcing standards to protect consumers from potentially harmful metallic contaminants, making effective metal detection a non-negotiable aspect of food processing. Similarly, the pharmaceutical industry faces equally rigorous regulatory scrutiny, demanding the highest levels of purity and preventing any foreign metallic intrusion into drugs and medical devices. This regulatory imperative directly translates into sustained demand for advanced metal detection solutions. Beyond compliance, the economic rationale for investing in industrial metal detectors is compelling. Early detection of metallic contaminants significantly mitigates the risk of costly product recalls, thereby safeguarding brand reputation and preventing substantial financial losses. The cost of a recall often far outweighs the investment in sophisticated detection technology. Furthermore, the increasing automation and complexity of manufacturing processes across sectors like plastics and textiles create new opportunities and challenges for contamination control, necessitating reliable metal detection systems. The growth of e-commerce and the associated rise in product traceability demands further reinforce the need for robust quality control measures, including effective metal detection.

Despite its promising growth trajectory, the industrial metal detectors market is not without its hurdles. One significant challenge lies in the initial capital investment required for advanced metal detection systems. While the long-term benefits are substantial, the upfront cost can be a deterrent for smaller businesses or those operating in price-sensitive markets. This is particularly true for sophisticated systems featuring multi-frequency detection or advanced signal processing capabilities. Another restraint is the complexity of installation and calibration, especially for highly specialized applications. Ensuring optimal performance often requires skilled technicians and a deep understanding of the specific production environment, which can be a barrier to widespread adoption. The diverse range of metallic contaminants and their varying physical properties (e.g., size, shape, magnetic properties) also present a technical challenge. Developing detectors that can reliably identify all types of metallic impurities without generating excessive false positives requires continuous technological innovation. Furthermore, competition from alternative detection methods, such as X-ray inspection systems, while often complementary, can present a perceived challenge in certain niche applications, although metal detectors generally offer a more cost-effective solution for metallic contamination. Lastly, the dynamic nature of manufacturing processes and the introduction of new materials can necessitate frequent recalibration or upgrades to existing metal detection equipment, adding to ongoing operational costs.

The Food Industry stands as a dominant segment within the global industrial metal detectors market, and consequently, regions with a strong and burgeoning food processing sector are poised for significant market leadership.

Dominant Segment: Food Industry The Food Industry's preeminence is driven by several interconnected factors. Firstly, it is subject to the most stringent global food safety regulations, with constant oversight from bodies like the FDA (Food and Drug Administration) in the US, EFSA (European Food Safety Authority) in Europe, and similar organizations worldwide. These regulations mandate the detection and removal of metallic contaminants, which can range from small fragments of machinery to pieces of packaging, posing direct health risks to consumers. The sheer volume of food production globally, coupled with the perishable nature of many products, further amplifies the need for reliable and continuous metal detection to prevent contamination throughout the supply chain – from raw ingredient processing to final packaging. The high rate of product recalls in the food sector due to metallic foreign objects, which can result in immense financial losses and severe reputational damage, acts as a powerful motivator for food manufacturers to invest in advanced metal detection technology. The market for Metal Detector with Conveyor systems is particularly significant within the food industry, as these are seamlessly integrated into existing production lines for automated inspection of packaged goods. Additionally, Rectangular Aperture Metal Detectors are crucial for inspecting bulk ingredients or packaged items moving on belts. The increasing demand for convenience foods, processed snacks, and ready-to-eat meals, all of which undergo extensive processing, further fuels the adoption of metal detectors.

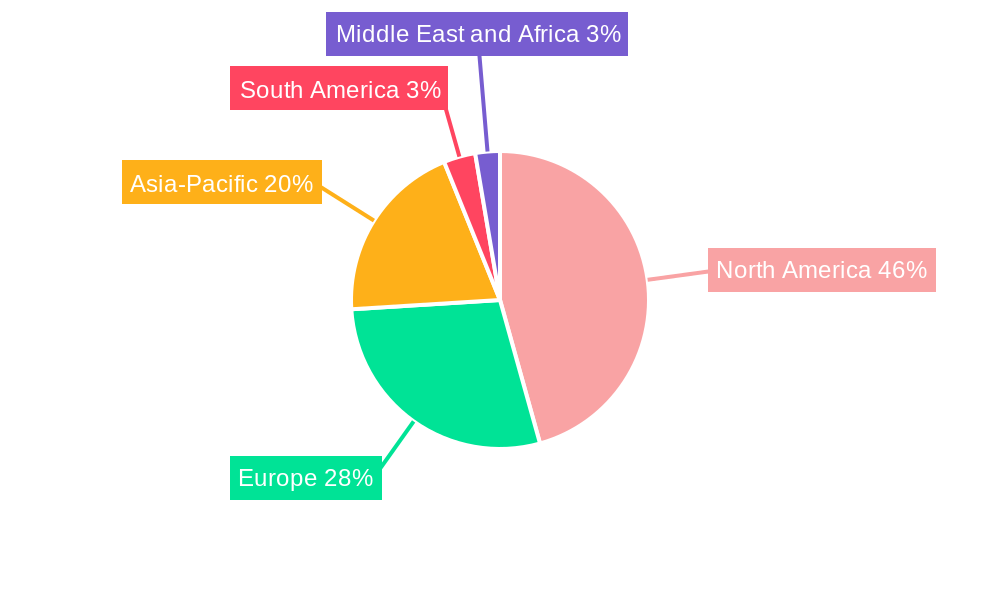

Dominant Region/Country: North America North America, particularly the United States, is a leading force in the industrial metal detectors market, largely due to the robust presence of a highly developed and technologically advanced food processing industry. The stringent regulatory framework enforced by agencies like the FDA, combined with a strong consumer demand for safe and high-quality food products, necessitates the widespread adoption of sophisticated metal detection systems. The presence of major global food manufacturers and a well-established supply chain further contributes to the market's strength. Beyond the food sector, North America also boasts significant adoption in the pharmaceutical industry, driven by similar regulatory pressures and a focus on patient safety. The mining and plastics industries in countries like Canada and the US also contribute to the demand, albeit to a lesser extent than food and pharmaceuticals, for quality control and equipment protection. The strong emphasis on automation and Industry 4.0 principles within the manufacturing landscape of North America also encourages the integration of advanced metal detection technologies.

Emerging Dominant Segment: Pharmaceutical Industry While the Food Industry currently holds the top spot, the Pharmaceutical Industry is rapidly emerging as a critical and high-growth segment for industrial metal detectors. The absolute necessity for purity and the extreme sensitivity to any metallic contamination in medicines and medical devices mean that pharmaceutical manufacturers are among the most diligent adopters of advanced detection technology. Any metallic particle, no matter how small, can have catastrophic consequences for patient health, leading to severe regulatory penalties and irreparable damage to a pharmaceutical company's reputation. Consequently, the demand for highly sensitive and reliable metal detection systems, such as those designed for Pipeline Liquid, Paste and Slurry Metal Detectors used in the production of liquid medications or injectables, is on the rise. Rectangular Aperture Metal Detectors are also vital for inspecting packaged drugs and vials. The increasing global demand for pharmaceuticals, coupled with the growing complexity of drug manufacturing processes and the development of novel drug delivery systems, will continue to drive significant investment in this segment over the forecast period.

Several key factors are acting as significant growth catalysts for the industrial metal detectors industry. The continuous tightening of global regulatory standards for product safety, especially in the food and pharmaceutical sectors, remains a primary driver. Furthermore, advancements in sensor technology, leading to more sensitive, accurate, and versatile metal detection systems, are broadening their applicability. The increasing adoption of automation and Industry 4.0 principles in manufacturing operations is also a significant catalyst, as businesses seek to integrate intelligent inspection systems into their production lines for enhanced efficiency and quality control. The growing awareness among manufacturers of the substantial financial and reputational risks associated with product contamination is also pushing them to invest in preventative measures, including robust metal detection solutions.

This report offers a comprehensive and multi-faceted view of the global industrial metal detectors market. It meticulously analyzes the market dynamics from 2019 to 2033, providing deep insights into the Historical Period (2019-2024), Base Year (2025), and a detailed Forecast Period (2025-2033). The analysis encompasses unit sales projections in millions of units, offering a granular understanding of market volume. We dissect the market by Type (e.g., Metal Detector with Conveyor, Gravity Fall Metal Detector), Application (e.g., Food Industry, Pharmaceutical Industry), and explore the impact of Industry Developments. Furthermore, the report identifies and elaborates on the key Driving Forces, Challenges, and Growth Catalysts shaping the market's evolution. A dedicated section highlights the dominant Regions and Segments, providing strategic insights into areas of significant market activity and potential. Finally, an exhaustive list of Leading Players and a timeline of Significant Developments offer a complete panorama of the industrial metal detectors landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.0% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.0%.

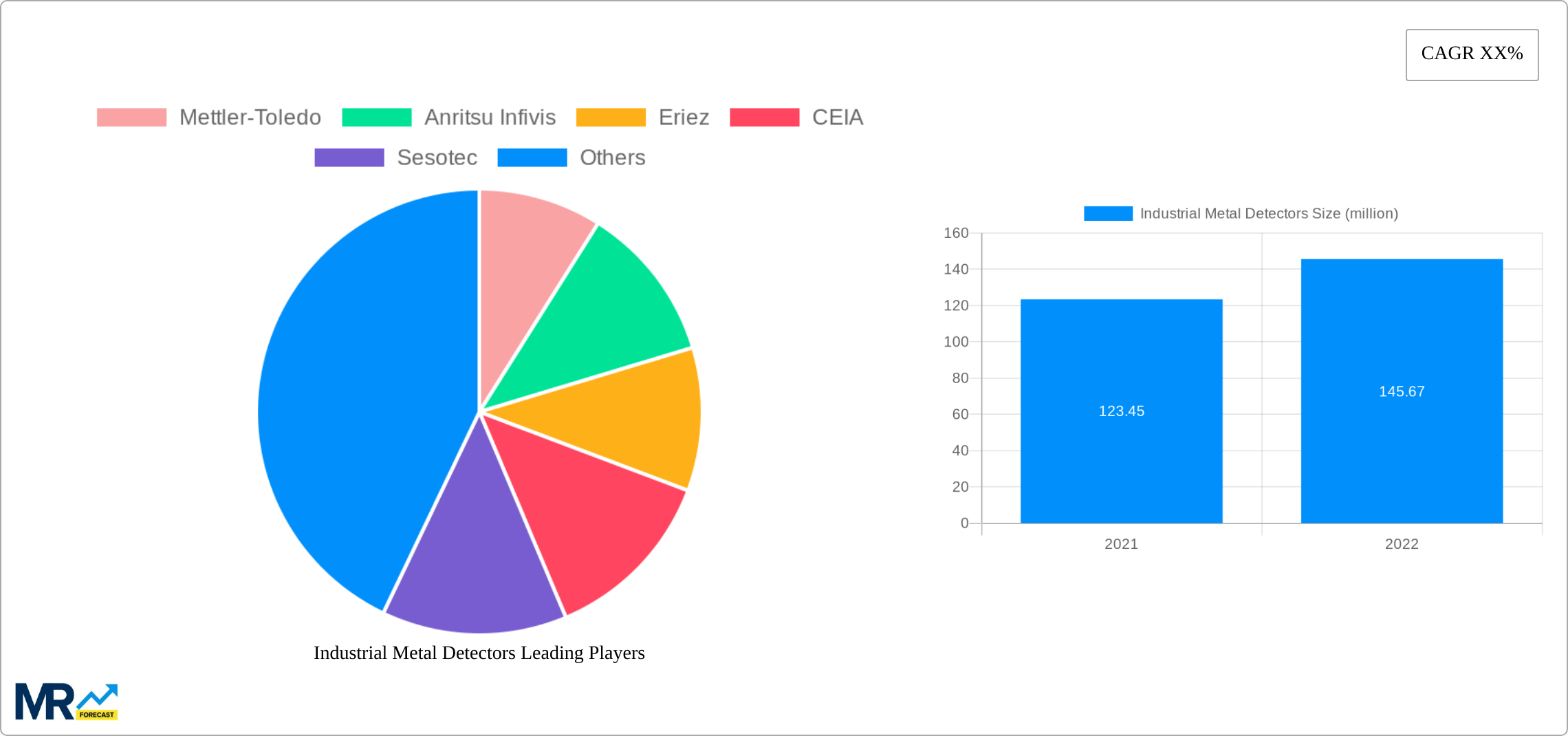

Key companies in the market include Mettler-Toledo, Anritsu Infivis, Eriez, CEIA, Sesotec, Minebea Intec, Nissin Electronics, Multivac Group, Loma Systems, Thermo Fisher, Bizerba, Ishida, WIPOTEC-OCS, Mesutronic, Fortress Technology, Nikka Densok, Shanghai Techik, Gaojing, Easyweigh, Qingdao Baijing, COSO, JUZHENG Electronic and Technology, Dongguan Shanan, Dongguan Lianxin.

The market segments include Type, Application.

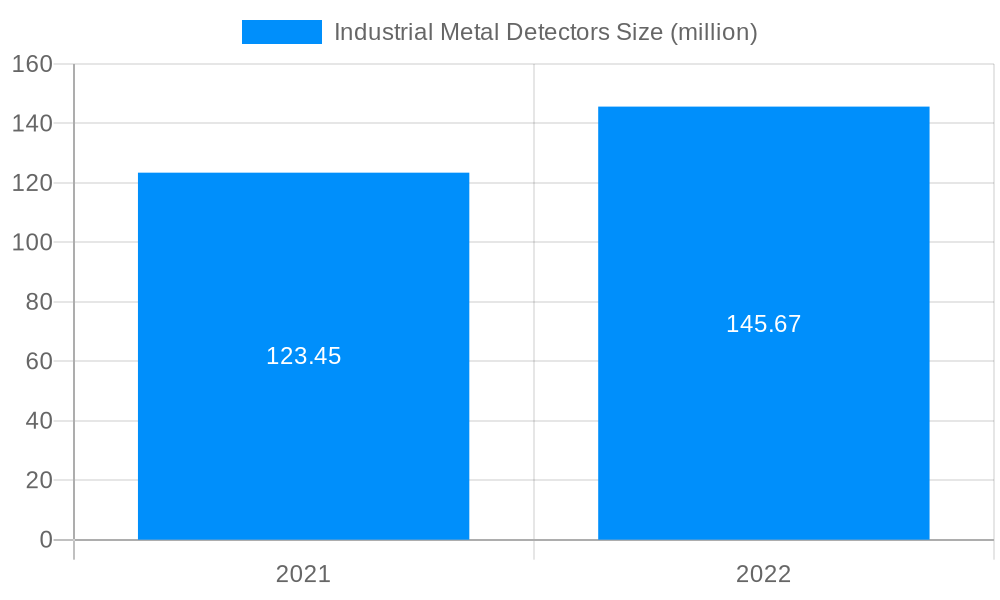

The market size is estimated to be USD 779 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Industrial Metal Detectors," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Industrial Metal Detectors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.