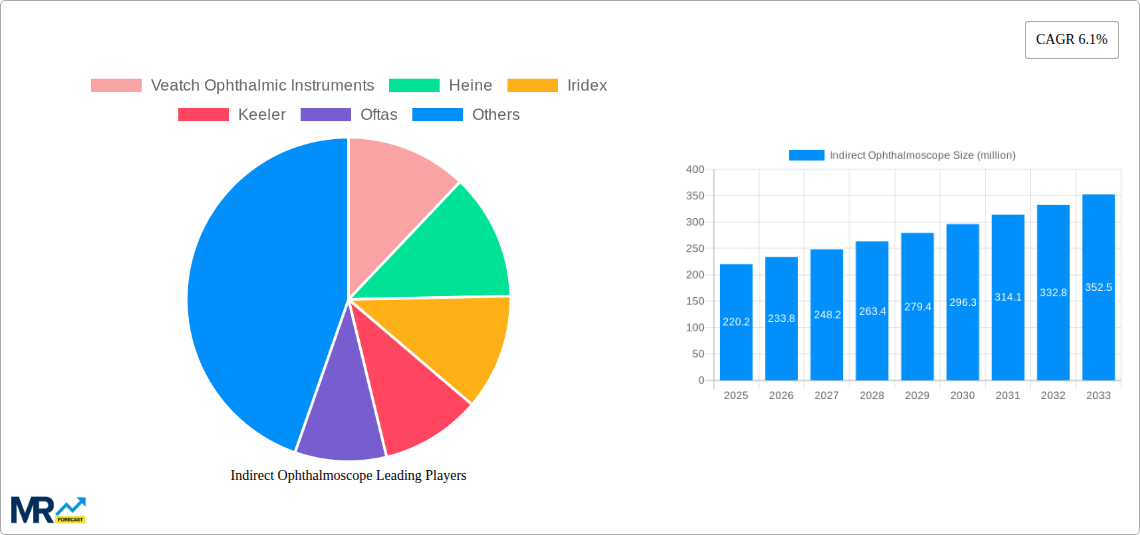

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indirect Ophthalmoscope?

The projected CAGR is approximately 6.1%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Indirect Ophthalmoscope

Indirect OphthalmoscopeIndirect Ophthalmoscope by Type (Diabetic Retinopathy, Peripheral Neovascularization, Pediatric Retinal Repairs, Lattice Degeneration), by Application (Clinic, Hospital, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

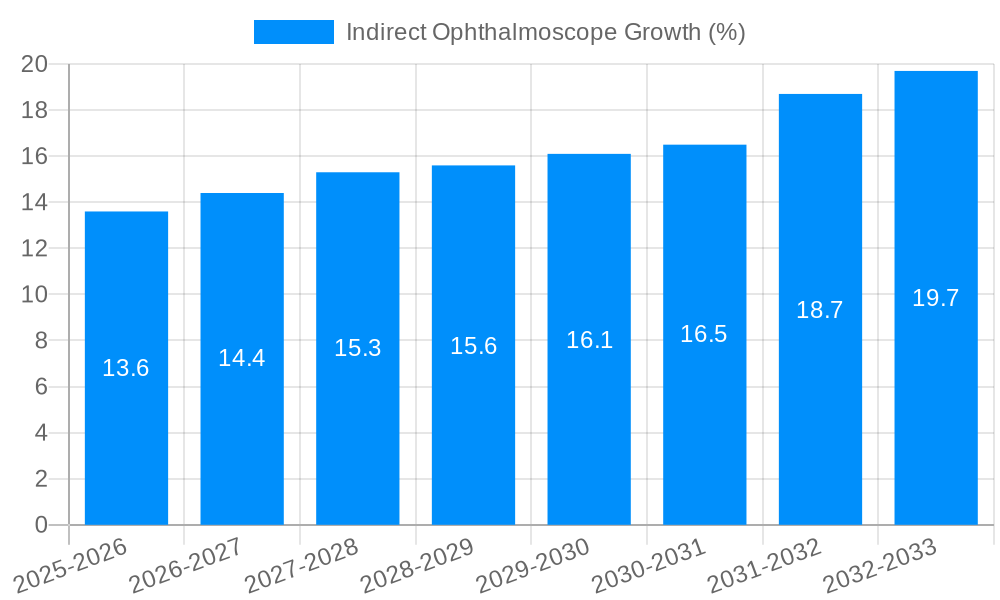

The indirect ophthalmoscope market, valued at $220.2 million in 2025, is projected to experience robust growth, driven by a rising prevalence of eye diseases globally and increasing demand for advanced diagnostic tools. The market's Compound Annual Growth Rate (CAGR) of 6.1% from 2025 to 2033 signifies a steady expansion, fueled by technological advancements leading to improved image quality and portability of indirect ophthalmoscopes. Factors like the growing geriatric population, a higher incidence of diabetic retinopathy and macular degeneration, and increasing awareness regarding eye health contribute significantly to market growth. Furthermore, the integration of digital imaging capabilities and improved user-friendliness are enhancing the appeal of indirect ophthalmoscopes among ophthalmologists and optometrists. The market is segmented by product type (e.g., handheld, stand-mounted), end-user (hospitals, clinics, research institutions), and geography. Competitive dynamics are shaped by established players like Heine, Welch Allyn, and Nidek, continuously striving for innovation and market share expansion through product diversification and strategic partnerships.

However, certain challenges persist. High initial investment costs for advanced indirect ophthalmoscopes, especially digital models, could limit their accessibility in resource-constrained settings. Additionally, the ongoing development and adoption of alternative diagnostic technologies, such as optical coherence tomography (OCT), might influence the growth trajectory. Nevertheless, the overall market outlook for indirect ophthalmoscopes remains positive, driven by unmet needs in eye care and continuous technological innovation in ophthalmic imaging. The competitive landscape is likely to remain active, with existing players investing in R&D and new entrants exploring market opportunities. Growth is anticipated to be particularly strong in developing economies with growing healthcare infrastructure and rising disposable incomes.

The global indirect ophthalmoscope market, valued at approximately $XXX million in 2025, is poised for significant growth throughout the forecast period (2025-2033). Analysis of the historical period (2019-2024) reveals a steady increase in demand, driven primarily by the rising prevalence of ophthalmic diseases and the increasing adoption of advanced diagnostic techniques. The market's trajectory is further shaped by technological advancements resulting in improved image quality, portability, and integration with digital imaging systems. This trend towards digitalization allows for better data storage, sharing, and analysis, enhancing diagnostic accuracy and facilitating telemedicine applications. The increasing number of ophthalmologists and optometrists globally also contributes to the market's growth. However, the high cost of advanced indirect ophthalmoscopes and the availability of alternative diagnostic methods present some challenges. The competitive landscape is dynamic, with established players like Heine and Welch Allyn competing alongside newer entrants focusing on innovative features and cost-effective solutions. The market is segmented by product type (e.g., binocular, monocular), end-user (hospitals, clinics), and geography. Future growth will likely be fueled by expanding healthcare infrastructure in developing countries, increasing awareness of eye health, and the continuous innovation within the indirect ophthalmoscope technology. The market is expected to reach $YYY million by 2033, representing a substantial compound annual growth rate (CAGR). This growth reflects a convergence of factors, solidifying the indirect ophthalmoscope's vital role in modern ophthalmic practice.

Several factors are propelling the growth of the indirect ophthalmoscope market. The escalating global prevalence of age-related macular degeneration, glaucoma, cataracts, and diabetic retinopathy is a primary driver. Early and accurate diagnosis of these conditions is crucial for effective management, and the indirect ophthalmoscope remains a cornerstone of ophthalmic examination. The increasing adoption of minimally invasive surgical techniques in ophthalmology also contributes to market expansion, as detailed pre-operative assessments often necessitate the use of an indirect ophthalmoscope. Furthermore, technological improvements resulting in higher-resolution imaging, improved illumination, and enhanced portability are significantly impacting market demand. The integration of digital imaging capabilities allows for seamless documentation, storage, and sharing of retinal images, enhancing collaboration among healthcare professionals and facilitating remote consultations. Lastly, the rising disposable incomes in emerging economies are increasing healthcare spending, further boosting demand for advanced diagnostic tools like indirect ophthalmoscopes.

Despite the positive growth trajectory, several challenges hinder the market's full potential. The high initial investment cost of advanced indirect ophthalmoscopes, especially those with integrated digital imaging capabilities, can be a barrier for smaller clinics and healthcare facilities in developing regions. The availability of alternative diagnostic tools, such as optical coherence tomography (OCT) and fundus photography, presents competition. While these techniques offer more detailed imaging, they are often more expensive and not universally accessible. Moreover, the need for skilled professionals proficient in using indirect ophthalmoscopes can limit the wider adoption of the technology. Furthermore, regulatory hurdles and varying reimbursement policies across different healthcare systems can also pose significant challenges. The competitive landscape is intense, requiring manufacturers to continuously innovate and offer cost-effective solutions to maintain their market share.

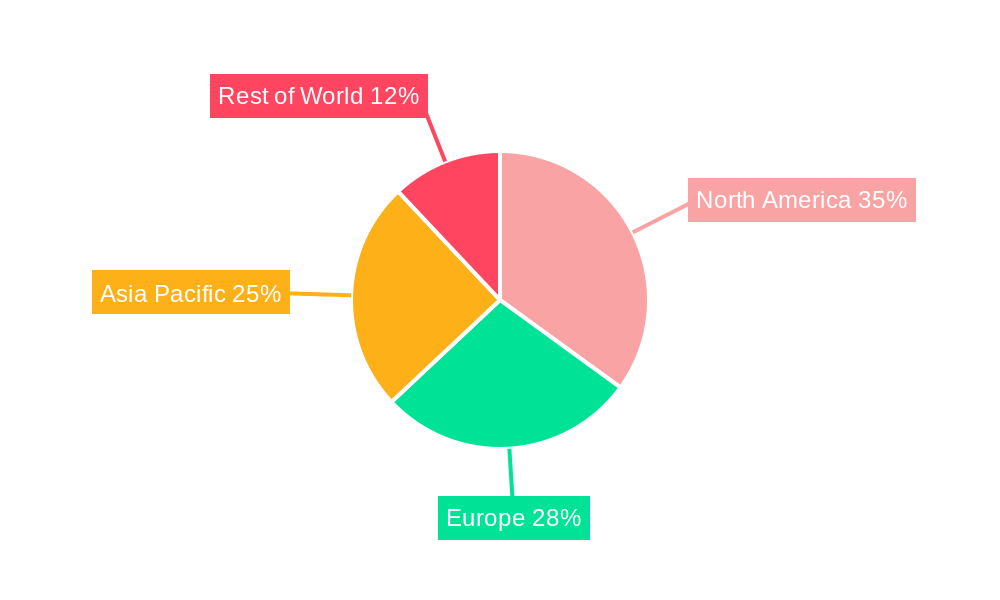

The indirect ophthalmoscope market exhibits significant regional variations.

North America: This region is expected to maintain a dominant market share throughout the forecast period, driven by robust healthcare infrastructure, high prevalence of ophthalmic diseases, and the early adoption of advanced technologies. The presence of major market players and high healthcare expenditure contribute to this dominance.

Europe: Europe is another significant market, with growth fueled by aging populations and increasing awareness of eye health. Stringent regulatory frameworks influence technological advancements and market penetration.

Asia-Pacific: This region is witnessing remarkable growth, propelled by expanding healthcare infrastructure, rising disposable incomes, and a burgeoning middle class. However, challenges related to affordability and healthcare access persist.

Segments: The segment of binocular indirect ophthalmoscopes is projected to hold a larger market share compared to monocular devices due to their enhanced image quality and broader clinical applications. Hospitals and large ophthalmology clinics represent a significant end-user segment, owing to higher volumes of patients and advanced diagnostic needs.

In summary, while North America and Europe currently dominate, the Asia-Pacific region offers significant growth potential in the coming years. The binocular segment leads the product market, catering to the increased demand for enhanced diagnostic capabilities.

The indirect ophthalmoscope market is experiencing growth due to the convergence of factors, including the rising prevalence of ophthalmic diseases necessitating early detection and diagnosis, technological advancements offering improved image quality and portability, and increased investment in healthcare infrastructure globally. These factors collectively create a fertile ground for market expansion.

This report provides a comprehensive overview of the indirect ophthalmoscope market, examining key trends, drivers, challenges, and regional variations. It features detailed analysis of leading players, segment-wise market breakdowns, and projections for market growth throughout the forecast period (2025-2033). The report is an invaluable resource for industry stakeholders seeking actionable insights into this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.1% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.1%.

Key companies in the market include Veatch Ophthalmic Instruments, Heine, Iridex, Keeler, Oftas, Ziemer Ophthalmic Systems AG, Welch Allyn Insight, Lvpei, Nidek Co. Inc, Neitz, Ellex Medical Lasers Ltd, .

The market segments include Type, Application.

The market size is estimated to be USD 220.2 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Indirect Ophthalmoscope," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Indirect Ophthalmoscope, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.