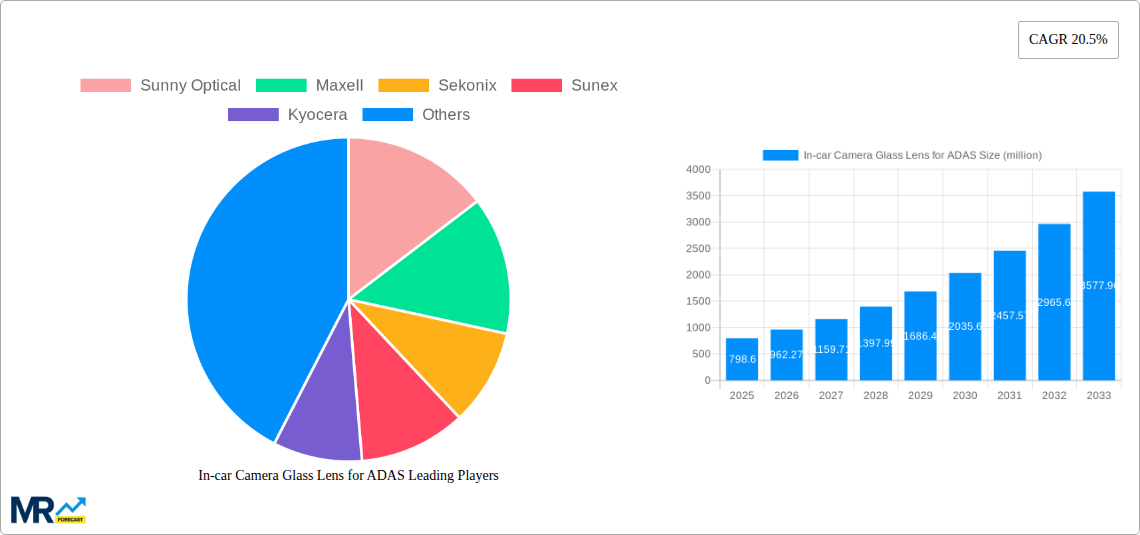

1. What is the projected Compound Annual Growth Rate (CAGR) of the In-car Camera Glass Lens for ADAS?

The projected CAGR is approximately 20.5%.

In-car Camera Glass Lens for ADAS

In-car Camera Glass Lens for ADASIn-car Camera Glass Lens for ADAS by Type (Below 3M, 3M to 5M, Above 5M), by Application (Level 1 Vehicle, Level 2 Vehicle, Level 3-5 Vehicle), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

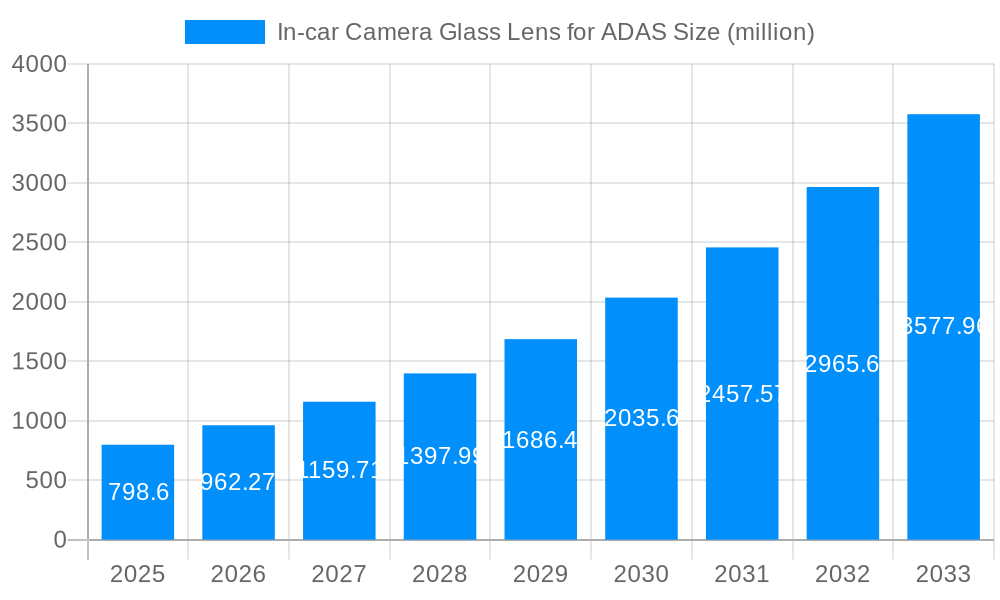

The global In-car Camera Glass Lens market for Advanced Driver-Assistance Systems (ADAS) is experiencing robust growth, projected to reach a substantial USD 798.6 million by 2025. This expansion is fueled by a compelling Compound Annual Growth Rate (CAGR) of 20.5%, indicating a dynamic and rapidly evolving industry. The escalating demand for enhanced vehicle safety features, driven by regulatory mandates and consumer preference for accident prevention technologies, is a primary market driver. As ADAS systems become increasingly sophisticated, the need for high-quality, durable, and optically precise camera glass lenses intensifies. Innovations in lens manufacturing, including advanced coatings for improved light transmission and reduced glare, along with the miniaturization of components to accommodate compact camera modules, are key trends shaping the market. The integration of multiple camera systems for a 360-degree view and the development of specialized lenses for thermal imaging and night vision further contribute to market momentum.

The market is segmented by lens type, with the "Above 5M" category likely to witness significant traction due to the increasing resolution demands of advanced ADAS functionalities like object recognition and lane keeping assist. Similarly, applications in "Level 3-5 Vehicle" segments are expected to be the fastest-growing, reflecting the automotive industry's push towards autonomous driving. Despite the strong growth trajectory, potential restraints could include the high cost of advanced lens manufacturing processes and the complex supply chain dynamics for specialized materials. However, the continuous technological advancements and the proactive adoption of ADAS features by leading automotive manufacturers globally, particularly in regions like Asia Pacific and Europe, are expected to outweigh these challenges. Key players like Sunny Optical, Maxell, and O-film Tech are actively investing in research and development to capture market share in this burgeoning sector.

This comprehensive report delves into the burgeoning market for In-car Camera Glass Lenses for Advanced Driver-Assistance Systems (ADAS), offering a detailed analysis of trends, drivers, challenges, and future growth trajectories. The study encompasses a robust Study Period from 2019 to 2033, with a deep dive into the Historical Period (2019-2024), a precise Base Year analysis for 2025, and an insightful Estimated Year projection for 2025, leading into a meticulous Forecast Period of 2025-2033. The global market valuation is presented in the millions unit, providing a clear financial perspective on this rapidly evolving sector.

The market for In-car Camera Glass Lenses for ADAS is experiencing a significant upswing, driven by an accelerating global adoption of autonomous driving technologies and stringent automotive safety regulations. As vehicles become increasingly sophisticated, the reliance on high-performance camera systems, and consequently, their optical components like glass lenses, is paramount. The trend towards higher resolution cameras, capable of capturing finer details for applications such as object recognition, lane keeping, and pedestrian detection, is directly impacting lens design and material science. This translates to an increased demand for lenses with superior optical clarity, wider fields of view, and enhanced durability to withstand harsh automotive environments, including extreme temperatures and vibrations. The market is witnessing a continuous push for miniaturization, allowing for more discreet and integrated camera placements within the vehicle. Furthermore, advancements in anti-reflective coatings and hydrophobic treatments are becoming standard, improving image quality under diverse lighting and weather conditions. The evolving landscape of ADAS, from basic Level 1 systems to more advanced Level 3-5 autonomous capabilities, is creating a bifurcated demand, with a growing need for specialized lenses tailored to the specific requirements of each autonomy level. The transition from traditional plastic lenses to high-quality glass optics is a defining characteristic, driven by the superior optical performance and scratch resistance glass offers, crucial for the long-term reliability of ADAS. This shift is supported by innovation in glass manufacturing processes, leading to cost-effectiveness and mass-producible solutions. The integration of AI and machine learning in vehicle perception systems further amplifies the need for pristine image data, making the quality of the glass lens a non-negotiable factor. Market participants are actively investing in research and development to offer lenses that not only meet current demands but also anticipate future technological advancements in areas like LiDAR and radar fusion, where clear and accurate visual data remains foundational. The growth in electric vehicles (EVs) also presents a unique opportunity, as their design often incorporates advanced sensor suites, necessitating a corresponding increase in high-quality camera lens integration for ADAS functionalities.

The surge in the In-car Camera Glass Lens for ADAS market is fundamentally propelled by a confluence of powerful forces, primarily centered around enhanced vehicle safety and the relentless pursuit of autonomous driving capabilities. Governments worldwide are progressively mandating advanced safety features in new vehicles, including automatic emergency braking (AEB), lane departure warning (LDW), and adaptive cruise control (ACC), all of which heavily rely on sophisticated camera systems. This regulatory push creates a sustained and growing demand for the optical components that enable these functionalities. Concurrently, consumer awareness and preference for vehicles equipped with these advanced safety and convenience features are on the rise. Buyers are increasingly willing to pay a premium for vehicles that offer a higher degree of safety and a smoother driving experience, thereby incentivizing automakers to integrate more comprehensive ADAS. The technological maturation of AI and sensor fusion algorithms, which are critical for interpreting the data captured by cameras, also plays a pivotal role. As these algorithms become more robust and reliable, the demand for higher quality, higher resolution camera lenses that can provide the necessary detailed and accurate input escalates. Furthermore, the global automotive industry's ambitious roadmap towards full autonomy is a significant long-term driver. The development of Level 3, Level 4, and Level 5 autonomous vehicles necessitates a sophisticated array of sensors, with cameras being a central element. Each advancement in the autonomy ladder demands more capable and precisely engineered camera systems, directly impacting the market for their essential glass lens components. The continuous innovation in lens manufacturing, leading to improved optical performance, increased durability, and cost-effectiveness, also fuels market expansion by making these advanced components more accessible for mass-produced vehicles.

Despite the robust growth, the In-car Camera Glass Lens for ADAS market is not without its hurdles. One significant challenge revolves around the intricate and demanding manufacturing processes involved in producing high-quality, automotive-grade glass lenses. Achieving the required precision, optical uniformity, and defect-free surfaces on a large scale can be technically challenging and capital-intensive. This complexity can lead to higher production costs, which in turn might impact the affordability of ADAS features, particularly for entry-level vehicles. Another restraint stems from the rapid pace of technological evolution in the automotive sector. The constant advancements in sensor technology, processing power, and AI algorithms mean that camera lens requirements are perpetually shifting. Manufacturers of glass lenses must continually invest in research and development to keep pace with these changes, ensuring their products meet the specifications for next-generation ADAS. Failure to adapt quickly could lead to obsolescence. Supply chain disruptions, as witnessed in recent global events, also pose a considerable risk. The automotive industry is highly interconnected, and any interruption in the supply of raw materials, specialized machinery, or even skilled labor for lens production can have a cascading effect on the availability and cost of finished lenses. Furthermore, the rigorous testing and validation procedures mandated by the automotive industry for safety-critical components add another layer of complexity and time to the product development cycle, potentially slowing down market penetration. The increasing demand for miniaturization also presents a design challenge, as fitting complex optical elements into increasingly compact camera modules while maintaining performance requires innovative engineering solutions. Lastly, the cost sensitivity of the automotive market, especially in certain segments and regions, can limit the widespread adoption of premium glass lenses, pushing some manufacturers towards more cost-effective but potentially lower-performing alternatives.

Segments Dominating the Market:

Regional Dominance:

The In-car Camera Glass Lens for ADAS market is experiencing a pronounced dominance in segments that cater to advanced functionalities and higher levels of automation. Within the "Type" segmentation, lenses with Above 5M (Megapixels) resolution are increasingly dictating market trends. This surge is directly attributable to the growing sophistication of ADAS algorithms that require higher detail and clarity for accurate object detection, identification, and tracking. Features like pedestrian detection in challenging lighting conditions, distinguishing between different types of road signs, and enabling robust lane-keeping require a significantly higher pixel count than older ADAS iterations. As automakers push the boundaries of assisted driving, the demand for such high-resolution imaging is becoming standard, making lenses in this category the most sought-after.

In terms of "Application," the market is witnessing substantial growth driven by Level 2 Vehicle and Level 3-5 Vehicle segments. Level 2 systems, which offer features like adaptive cruise control with steering assistance and automatic lane changes, are already widely adopted in mid-range and premium vehicles. This widespread adoption translates into a massive volume demand for the associated camera glass lenses. However, the most significant future growth potential lies within the Level 3-5 Vehicle segment. As autonomous driving capabilities advance towards higher levels, the complexity and number of camera systems per vehicle are expected to skyrocket. These higher autonomy levels will require a denser network of cameras, each equipped with highly specialized and high-performance glass lenses capable of delivering exceptional image quality under a vast range of scenarios, from adverse weather to low-light conditions, and processing incredibly rich data for decision-making.

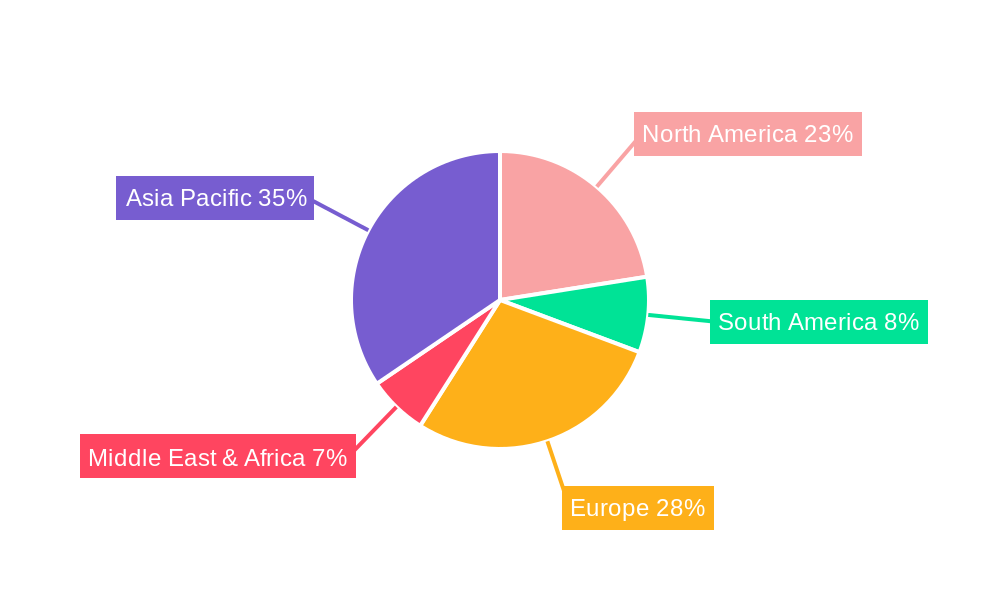

Geographically, the Asia-Pacific region, with China at its forefront, is poised to dominate the In-car Camera Glass Lens for ADAS market. China's aggressive push towards smart mobility, coupled with its massive automotive manufacturing base and significant investments in autonomous driving technology, positions it as a key growth engine. The region is not only a massive consumer of vehicles but also a significant producer of automotive components, fostering a strong ecosystem for lens manufacturers. North America is another crucial region, driven by a strong consumer demand for advanced safety features, the presence of leading automotive manufacturers and technology innovators, and supportive regulatory frameworks that encourage ADAS adoption. The United States, in particular, is at the forefront of autonomous vehicle development and testing. Europe also represents a significant market, characterized by stringent automotive safety regulations (such as Euro NCAP advancements) and a strong commitment to vehicle electrification and advanced driver assistance technologies. The region's emphasis on sustainability and safety creates a fertile ground for the adoption of high-performance ADAS, thereby driving demand for the corresponding camera glass lenses. These regions, with their combined technological prowess, market size, and regulatory incentives, are collectively shaping the future landscape of the In-car Camera Glass Lens for ADAS market.

Several key factors are acting as significant growth catalysts for the In-car Camera Glass Lens for ADAS industry. The escalating global focus on road safety, spurred by governmental regulations and increasing consumer awareness, directly translates to a higher demand for ADAS features. The relentless technological advancements in sensor capabilities and AI algorithms are continuously pushing the need for higher resolution and more precisely engineered camera lenses. Furthermore, the ambitious development trajectories of autonomous driving technologies, from advanced driver assistance to fully autonomous vehicles, are creating a foundational requirement for sophisticated optical solutions. Innovations in lens manufacturing, leading to improved performance, miniaturization, and cost-effectiveness, are also accelerating market adoption.

This report offers an exhaustive examination of the In-car Camera Glass Lens for ADAS market, providing an in-depth understanding of its intricate dynamics. It meticulously analyzes the market size, growth rates, and key trends observed over the Historical Period of 2019-2024, with detailed projections for the Forecast Period of 2025-2033. The report dissects the primary Driving Forces propelling the market, such as stringent safety regulations and the burgeoning demand for autonomous driving. It also sheds light on the inherent Challenges and Restraints, including manufacturing complexities and the rapid pace of technological change. Furthermore, the report identifies and elaborates on the Key Regions or Countries and specific Segments poised for significant market dominance. It highlights the crucial Growth Catalysts and presents a comprehensive overview of the Leading Players and their strategic initiatives. This report is an indispensable resource for stakeholders seeking to navigate and capitalize on the opportunities within the rapidly evolving In-car Camera Glass Lens for ADAS ecosystem.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 20.5%.

Key companies in the market include Sunny Optical, Maxell, Sekonix, Sunex, Kyocera, LCE, Ricoh, O-film Tech, Trace, HongJing, .

The market segments include Type, Application.

The market size is estimated to be USD 798.6 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "In-car Camera Glass Lens for ADAS," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the In-car Camera Glass Lens for ADAS, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.