1. What is the projected Compound Annual Growth Rate (CAGR) of the Hip Surgery Device?

The projected CAGR is approximately 5.04%.

Hip Surgery Device

Hip Surgery DeviceHip Surgery Device by Type (/> Total Hip Replacement, Partial Hip Replacement, Hip Resurfacing), by Application (/> Hospital, ASCs), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

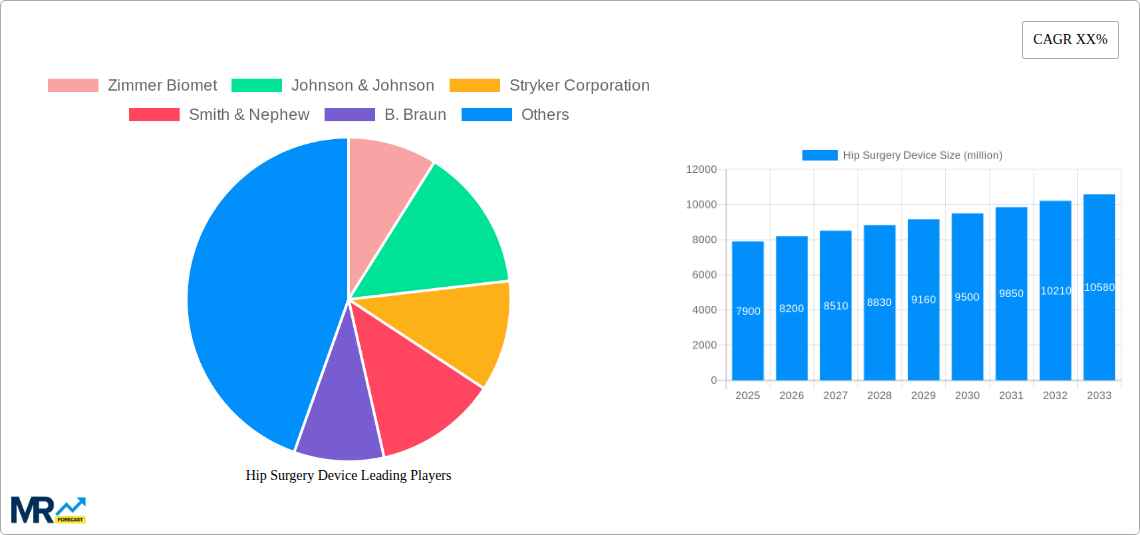

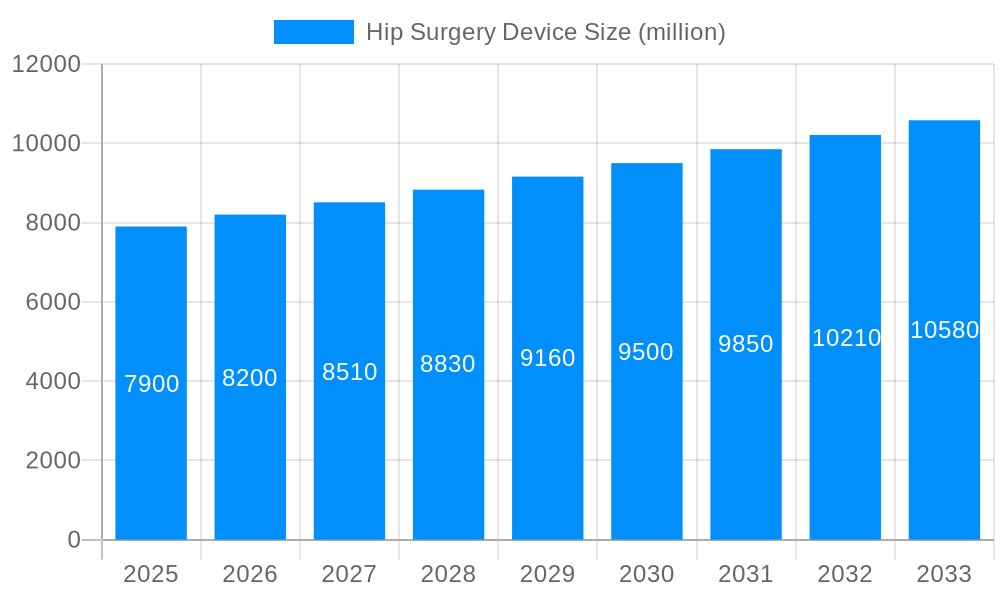

The global Hip Surgery Device market is poised for substantial growth, projected to reach approximately USD 7.9 billion in 2025 with a Compound Annual Growth Rate (CAGR) of 3.9%. This expansion is driven by an aging global population, leading to a higher incidence of hip-related conditions such as osteoarthritis and fractures. Advancements in surgical techniques and the development of innovative implant materials offering improved longevity and patient outcomes are also key contributors. Minimally invasive procedures are gaining traction, reducing recovery times and hospital stays, further stimulating market demand. The increasing prevalence of obesity, a significant risk factor for hip joint degeneration, also underpins the market's upward trajectory. Furthermore, a growing awareness among patients and healthcare providers about the benefits of hip replacement surgeries for restoring mobility and improving quality of life is fueling market penetration.

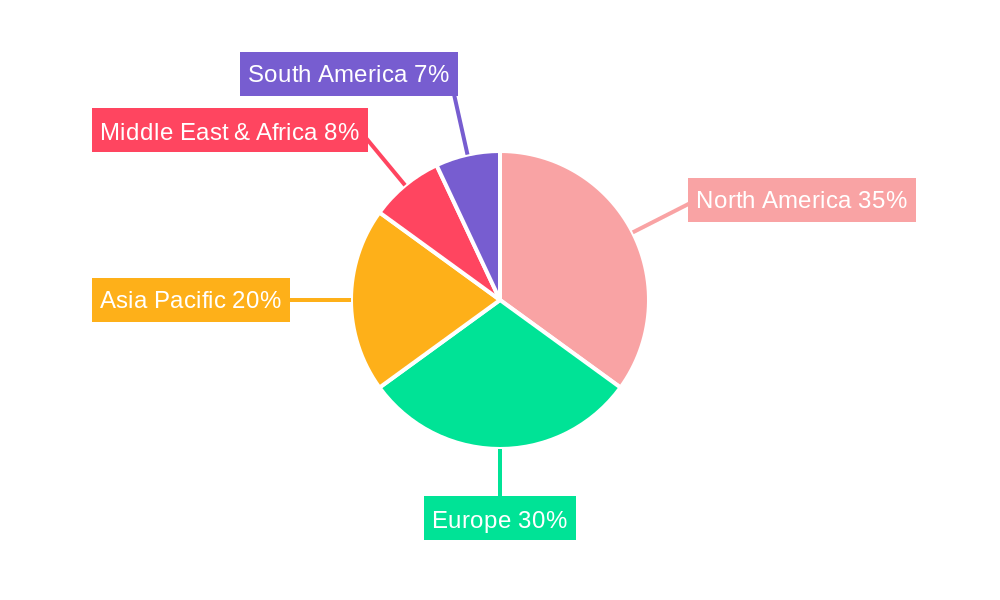

The market is segmented by device type, with Total Hip Replacement holding the largest share due to its widespread application in treating severe hip joint damage. Partial Hip Replacement and Hip Resurfacing are also significant segments, offering tailored solutions for specific patient needs. Hospitals remain the primary end-use segment, leveraging advanced infrastructure for complex surgical procedures. However, Ambulatory Surgery Centers (ASCs) are emerging as a rapidly growing segment, driven by their cost-effectiveness and focus on outpatient procedures, particularly for less complex cases. Geographically, North America and Europe currently dominate the market, owing to developed healthcare infrastructures and high patient spending capacity. The Asia Pacific region, however, is expected to witness the fastest growth, propelled by rising healthcare expenditure, increasing medical tourism, and a growing middle class with greater access to advanced medical treatments.

This report delves into the dynamic global Hip Surgery Device market, a sector poised for significant expansion. Valued in the billions of dollars, the market is projected to witness robust growth fueled by an aging global population, increasing prevalence of hip-related ailments, and advancements in surgical technologies. Our comprehensive analysis spans the Study Period: 2019-2033, with the Base Year: 2025 and Estimated Year: 2025, providing a granular view of the market dynamics during the Historical Period: 2019-2024 and projecting trends throughout the Forecast Period: 2025-2033.

XXX is a pivotal moment for the hip surgery device market, characterized by a confluence of technological innovation, evolving patient demographics, and shifting healthcare delivery models. The market, already a multi-billion dollar behemoth, is projected to experience accelerated growth in the coming years. A primary driver is the persistent and increasing incidence of hip osteoarthritis and other degenerative conditions, largely attributed to the global aging population. As individuals live longer, the wear and tear on their hip joints naturally escalates, creating a sustained demand for reconstructive and replacement procedures. Furthermore, the rising prevalence of obesity and sedentary lifestyles in younger demographics are contributing to a growing number of younger patients requiring hip interventions, thus expanding the addressable market beyond the traditionally older patient cohort.

Technological advancements are revolutionizing hip surgery. Minimally invasive surgical techniques are gaining traction, leading to smaller incisions, reduced pain, faster recovery times, and lower infection rates. This has spurred the development of sophisticated instrumentation, robotic-assisted surgery platforms, and advanced implant materials such as highly cross-linked polyethylene and ceramic-on-ceramic bearings, which offer enhanced durability and longevity. The focus is increasingly shifting towards patient-specific solutions, with advancements in 3D printing and personalized implant design enabling tailored surgical approaches. Moreover, the integration of digital technologies, including AI-powered pre-operative planning and intra-operative navigation, is enhancing surgical precision and improving patient outcomes. The economic landscape is also evolving, with a notable shift towards Ambulatory Surgery Centers (ASCs) for certain hip procedures. This trend is driven by cost-effectiveness, shorter patient stays, and greater patient convenience, presenting a significant growth avenue for device manufacturers catering to this segment. The interplay between these technological, demographic, and economic factors is creating a complex yet highly promising market for hip surgery devices, paving the way for sustained revenue streams in the billions.

The global hip surgery device market is experiencing a powerful surge, driven by a confluence of factors that are fundamentally reshaping its trajectory. Foremost among these is the undeniable demographic shift towards an aging global population. As life expectancy continues to increase across the globe, the cumulative wear and tear on hip joints due to osteoarthritis and other degenerative conditions becomes more pronounced. This naturally leads to a greater demand for hip replacement and resurfacing procedures, a trend that is expected to intensify in the coming years, translating into billions in market value. Beyond the aging population, a growing awareness of hip health and the availability of advanced treatment options are empowering individuals to seek surgical interventions earlier. Furthermore, the increasing prevalence of obesity, a significant risk factor for hip joint damage, is contributing to a higher incidence of hip pathology, even in younger demographics, thereby expanding the patient pool.

The relentless march of technological innovation is another colossal force propelling this market forward. The development and refinement of minimally invasive surgical techniques have dramatically improved patient recovery times, reduced post-operative pain, and lowered the risk of complications. This, in turn, has fostered greater patient acceptance and has spurred the development of specialized instruments and implants designed for these less invasive approaches. Robotic-assisted surgery is emerging as a transformative technology, offering enhanced precision, control, and repeatability during complex procedures, thereby improving outcomes and attracting significant investment. Moreover, advancements in implant materials, such as advanced ceramics and highly durable polymers, are leading to longer-lasting implants, a critical factor for patients seeking enduring relief from hip pain. The continuous innovation in implant design, including patient-specific solutions, further solidifies the market's growth potential. The increasing focus on improving patient quality of life and restoring mobility is a constant underlying driver for the entire hip surgery device ecosystem.

Despite the promising growth trajectory, the hip surgery device market is not without its significant hurdles and constraints that warrant careful consideration. A primary challenge revolves around the escalating healthcare costs associated with hip replacement surgeries. The sophisticated nature of advanced implants, coupled with the surgical expertise required, contributes to substantial expenses. This financial burden can limit access for a segment of the population, particularly in developing economies, thereby capping market penetration. Reimbursement policies and regulatory scrutiny from healthcare authorities worldwide also present a complex landscape for manufacturers. Stringent approval processes for new devices and ongoing evaluations of existing ones can lead to delays in market entry and increased compliance costs.

The issue of implant longevity and the potential for revision surgeries remains a persistent concern. While advancements have been made, loosening of implants, wear debris generation, and infection are still factors that can necessitate follow-up procedures, adding to patient discomfort and healthcare expenditure. This can indirectly impact market growth by creating patient apprehension and influencing surgeon preferences for established, albeit less advanced, technologies. Furthermore, the increasing number of younger patients undergoing hip replacement raises questions about the long-term durability of implants over an extended lifespan, potentially leading to a higher demand for revision surgeries later in life. The competitive landscape is also intensely challenging, with established players constantly vying for market share, requiring significant investment in research and development, marketing, and sales to maintain a competitive edge. Finally, the skilled workforce required for complex hip surgeries, including experienced orthopedic surgeons and surgical teams, can be a limiting factor in certain regions, hindering the widespread adoption of advanced surgical techniques and devices.

The global Hip Surgery Device market is characterized by significant regional variations and a clear dominance within specific product segments and application settings. North America is poised to continue its reign as a dominant force, driven by a highly developed healthcare infrastructure, a significant aging population, high disposable incomes, and a strong emphasis on technological adoption. The United States, in particular, represents a substantial portion of the global market due to a high incidence of hip osteoarthritis, a proactive approach to managing chronic pain, and robust reimbursement policies that facilitate access to advanced surgical procedures. The presence of major market players and extensive research and development activities further solidify North America's leading position.

Europe closely follows, with countries like Germany, the United Kingdom, and France exhibiting strong market performance. Similar to North America, an aging demographic, increasing patient awareness, and advancements in orthopedic surgery are key drivers. However, variations in reimbursement structures and regulatory landscapes across European nations can present a more fragmented market compared to North America. Asia Pacific is emerging as a rapidly growing region, fueled by a burgeoning middle class, increasing healthcare expenditure, and a growing awareness of hip health. Countries like China and India, with their massive populations and improving healthcare access, represent significant untapped potential.

In terms of segments, Total Hip Replacement (THR) consistently accounts for the largest market share. This is primarily due to the high prevalence of severe osteoarthritis and hip fractures, which are most effectively treated with a complete replacement of the damaged hip joint. The market for THR is characterized by a mature product offering and continuous innovation in implant materials and design to improve longevity and patient outcomes. Partial Hip Replacement also holds a significant, albeit smaller, market share, typically indicated for hip fractures where only the femoral head is replaced. While less common than THR, its demand is steady and influenced by trauma cases.

The Hip Resurfacing segment, though smaller, is gaining traction due to its potential to preserve more bone stock and offer a more natural range of motion, particularly appealing to younger, active patients. However, its adoption is influenced by surgeon expertise and specific patient selection criteria.

The Hospital segment is the predominant application setting for hip surgery devices, as these facilities are equipped with the necessary infrastructure, surgical expertise, and comprehensive patient care capabilities for complex orthopedic procedures. However, the Ambulatory Surgery Centers (ASCs) segment is experiencing a notable surge in growth. The increasing shift of elective hip surgeries to ASCs is driven by their cost-effectiveness, faster patient turnover, and enhanced patient convenience. This trend is prompting device manufacturers to develop specific product lines and strategies tailored to the needs of ASCs. The combination of these dominant regions and segments creates a multi-faceted market landscape with substantial opportunities for stakeholders.

Several key factors are acting as potent growth catalysts for the hip surgery device industry. The accelerating global aging population is a primary driver, directly correlating with the rising incidence of hip osteoarthritis and fractures. Simultaneously, increasing patient awareness regarding treatment options and a desire for improved quality of life are empowering individuals to seek timely surgical interventions. Technological advancements, particularly in minimally invasive techniques, robotic surgery, and advanced implant materials, are enhancing surgical outcomes, reducing recovery times, and driving demand for more sophisticated devices. The growing prevalence of obesity and sedentary lifestyles also contributes to a higher incidence of hip joint damage, expanding the patient pool.

This report offers a comprehensive analysis of the hip surgery device market, providing in-depth insights into its intricate workings. It meticulously examines market size, segmentation by type and application, and future projections. The report highlights the key drivers, challenges, and opportunities shaping the industry, offering a strategic roadmap for stakeholders. Coverage extends to leading market players, their product portfolios, and recent strategic initiatives. Furthermore, it delves into regional market dynamics, identifying growth hotspots and areas of potential disruption. The inclusion of historical data from 2019-2024 and detailed forecasts up to 2033, with a focus on the 2025 base year, ensures a robust understanding of market trends and future potential. This report serves as an indispensable resource for investors, manufacturers, healthcare providers, and policymakers seeking to navigate and capitalize on the evolving landscape of the hip surgery device sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.04% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.04%.

Key companies in the market include Zimmer Biomet, Johnson & Johnson, Stryker Corporation, Smith & Nephew, B. Braun, Wright Medical Group, Corin Group, Exactech, DJO Global, Waldemar Link, Mindray.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Hip Surgery Device," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Hip Surgery Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.