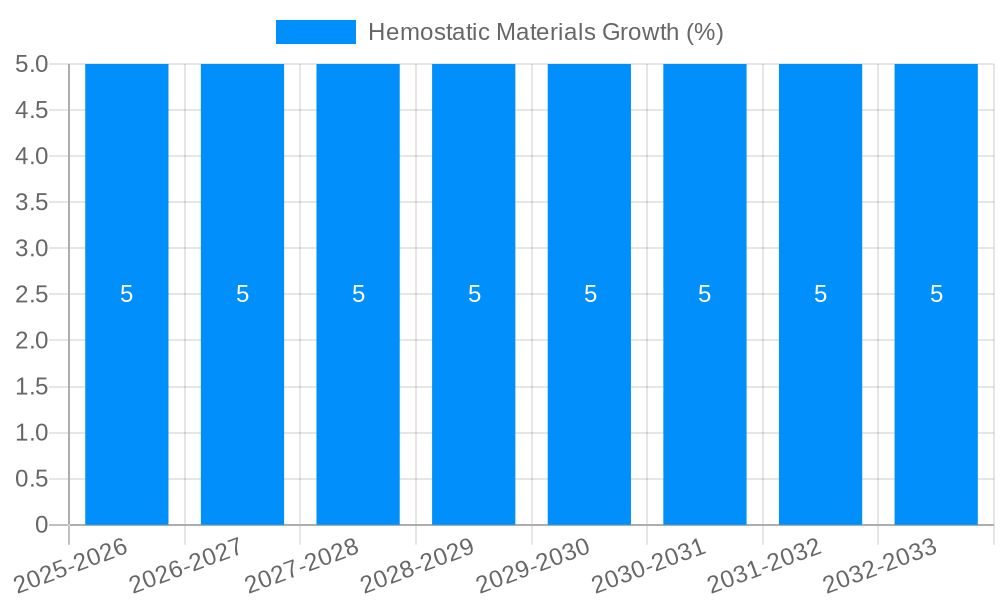

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hemostatic Materials?

The projected CAGR is approximately 5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Hemostatic Materials

Hemostatic MaterialsHemostatic Materials by Application (Hospital, Clinics, Beauty Salon), by Type (Mechanical Hemostatic Agent, Adhesive Hemostatic Agent), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Hemostatic Materials market is poised for robust expansion, projected to reach an estimated USD 1.5 billion in 2025 and exhibit a Compound Annual Growth Rate (CAGR) of approximately 5% through 2033. This significant growth is underpinned by a confluence of favorable market drivers and evolving healthcare practices. The increasing prevalence of surgical procedures, both elective and emergency, across various medical specialties, directly fuels the demand for effective hemostatic solutions to control bleeding and improve patient outcomes. Advancements in material science have led to the development of more sophisticated and efficient hemostatic agents, enhancing their efficacy and broadening their applicability. Furthermore, the growing awareness among healthcare professionals and institutions regarding the benefits of employing hemostatic materials in reducing operative time, minimizing blood loss, and accelerating post-operative recovery is a pivotal driver. The expanding healthcare infrastructure, particularly in emerging economies, coupled with rising disposable incomes, is also contributing to greater accessibility and adoption of these critical medical products.

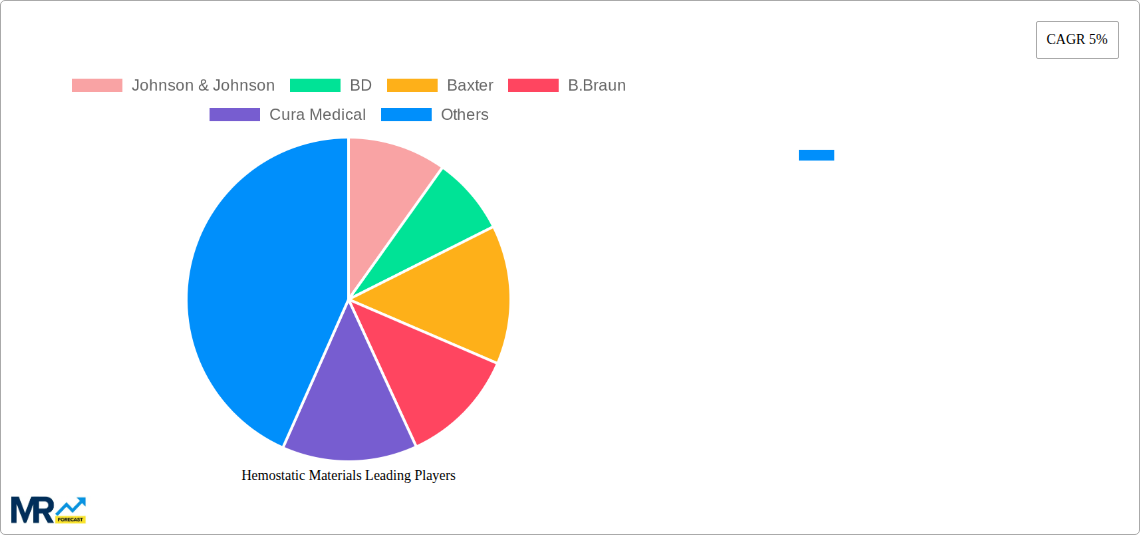

The market segmentation offers a clear view of where demand is concentrated and where future opportunities lie. The application segment highlights the significant role of hospitals and clinics as primary end-users, owing to the high volume of surgical interventions performed in these settings. The burgeoning aesthetic and cosmetic surgery sector, encompassing beauty salons, also presents a notable growth avenue, as minimally invasive procedures requiring precise bleeding control gain popularity. In terms of product type, both Mechanical Hemostatic Agents and Adhesive Hemostatic Agents command substantial market shares, with ongoing innovation in each category. Mechanical agents offer a physical barrier to bleeding, while adhesive agents provide a sealing function, catering to diverse surgical needs. Key players like Johnson & Johnson, BD, and Baxter are at the forefront of innovation and market penetration, continually introducing new products and expanding their geographical reach. The competitive landscape is dynamic, with a mix of established global giants and emerging regional manufacturers contributing to market growth and diversification. The study period of 2019-2033, with a focus on the forecast period of 2025-2033, indicates a sustained positive trajectory for the Hemostatic Materials market.

Here's a unique report description on Hemostatic Materials, incorporating your specified elements:

This in-depth analysis delves into the dynamic Hemostatic Materials market, forecasting its trajectory from 2019-2033, with a keen focus on the Base Year: 2025. The report provides a granular examination of the market's evolution through the Historical Period: 2019-2024 and projects its growth during the Forecast Period: 2025-2033. Our research illuminates the intricate interplay of technological advancements, evolving clinical needs, and expanding application frontiers. We project the global Hemostatic Materials market to reach a staggering valuation of over $15,000 million by 2033, indicating substantial growth from its estimated $7,500 million in 2025. The report offers strategic insights for stakeholders navigating this critical segment of the healthcare industry, highlighting key opportunities and potential pitfalls.

The Hemostatic Materials market is poised for robust expansion, driven by an escalating demand for advanced solutions that offer superior efficacy and improved patient outcomes. XXX, we observe a discernible shift towards bioabsorbable and biologically derived hemostats, moving away from traditional, non-degradable materials. This trend is fueled by a growing awareness of post-operative complications associated with foreign body presence. The Hospital segment, expected to constitute over 60% of the market share by 2033, will continue to be the primary driver, owing to increasing surgical volumes and the adoption of sophisticated hemostatic agents in complex procedures. The penetration of advanced hemostatic agents in specialized surgical fields, such as cardiovascular, orthopedic, and neurosurgery, is a significant trend, where precise bleeding control is paramount. Furthermore, the burgeoning field of minimally invasive surgery (MIS) is creating a demand for hemostatic materials that are adaptable to narrow surgical corridors and facilitate rapid clot formation. We anticipate the market to witness an increased focus on novel delivery systems, such as sprays and injectable formulations, enhancing ease of use and targeted application. The global market is projected to cross the $15,000 million mark by 2033, reflecting a compound annual growth rate (CAGR) of approximately 7.5% from its estimated $7,500 million in 2025. The competitive landscape is characterized by continuous innovation, with companies investing heavily in research and development to introduce next-generation hemostatic products. This includes the exploration of materials with enhanced antimicrobial properties and growth factor integration to promote tissue regeneration. The market's growth is further bolstered by increasing healthcare expenditure in developing economies and a rising prevalence of chronic diseases necessitating surgical interventions.

The hemostatic materials market's upward trajectory is propelled by a confluence of powerful drivers. A primary catalyst is the escalating global incidence of surgical procedures, encompassing both elective and emergency interventions. As populations age and the prevalence of chronic conditions like cardiovascular disease and cancer rises, the demand for surgical solutions, and consequently for effective hemostatic agents, continues to surge. This expanding surgical volume directly translates into a larger addressable market. Furthermore, significant advancements in medical technology have led to the development of more sophisticated and efficacious hemostatic agents. Innovations such as bio-engineered collagen, gelatin-based foams, and polysaccharide-derived materials offer improved biocompatibility, faster clotting times, and reduced immunogenic responses compared to older generation products. The increasing adoption of minimally invasive surgical techniques, while reducing patient trauma, often presents unique hemostasis challenges requiring specialized agents, thus fostering innovation and market growth. Moreover, a growing emphasis on patient safety and a reduction in post-operative complications, such as excessive bleeding and infection, are driving healthcare providers to invest in premium hemostatic solutions. This push for improved clinical outcomes directly fuels the demand for advanced hemostatic materials. The global market is estimated to grow from $7,500 million in 2025 to over $15,000 million by 2033.

Despite the promising growth outlook, the hemostatic materials market is not without its hurdles. One significant challenge is the high cost associated with advanced hemostatic agents. The research, development, and manufacturing processes for novel bio-based and engineered hemostats are often complex and resource-intensive, leading to premium pricing that can limit accessibility, particularly in resource-constrained healthcare settings. This cost factor can be a major restraint, especially in emerging markets. Another critical challenge is the regulatory landscape. Obtaining approvals for new hemostatic materials can be a lengthy and stringent process, involving extensive clinical trials to demonstrate safety and efficacy. Delays in regulatory approvals can impede market entry for innovative products and slow down the pace of innovation. Furthermore, the availability of cost-effective alternatives, such as traditional surgical techniques for bleeding control, can pose a competitive threat. While not always as effective or efficient as advanced agents, their lower price point can make them a preferred choice in certain scenarios. The market also faces challenges related to limited awareness and adoption of newer hemostatic technologies in some regions or among certain medical professionals, necessitating ongoing education and training initiatives. The overall market growth, though robust, is tempered by these factors, with projections indicating a strong but manageable expansion from its estimated $7,500 million in 2025 to over $15,000 million by 2033.

The global Hemostatic Materials market is characterized by distinct regional dominance and segment leadership, painting a comprehensive picture of its current landscape and future potential.

Dominant Segments:

Application: Hospital: This segment is projected to be the undisputed leader, capturing an estimated 65% of the market share by 2033. Hospitals, with their comprehensive surgical infrastructure and higher patient volumes, are the primary consumers of hemostatic materials. The sheer number of complex surgical procedures performed in hospital settings, ranging from cardiovascular and orthopedic surgeries to trauma and general surgery, necessitates a consistent and substantial supply of effective hemostatic agents. The increasing adoption of advanced surgical techniques, including robotic-assisted and laparoscopic surgeries, further amplifies the demand for specialized hemostatic products that can operate within confined surgical spaces. Furthermore, hospitals are often at the forefront of adopting new technologies and materials, driven by a focus on patient safety, reduced blood loss, and shorter recovery times, all of which are key selling points for advanced hemostatic solutions. The market within the hospital segment is estimated to grow from approximately $5,000 million in 2025 to over $9,750 million by 2033.

Type: Mechanical Hemostatic Agent: This category is expected to retain a dominant position, accounting for approximately 55% of the total market revenue by 2033. Mechanical hemostats, such as absorbable gelatin sponges, oxidized regenerated cellulose, and collagen-based products, have a long-standing track record of efficacy and broad applicability across various surgical specialties. Their well-established performance profiles and relatively lower cost compared to some advanced biological agents contribute to their widespread adoption. These agents work by providing a physical matrix for clot formation, absorbing excess fluid, and supporting platelet aggregation, making them indispensable tools for managing oozing and diffuse bleeding. The continuous innovation within this segment, focusing on improved absorbency, tensile strength, and integration with drug delivery capabilities, ensures their sustained relevance. The market for mechanical hemostats is projected to grow from around $4,200 million in 2025 to over $8,250 million by 2033.

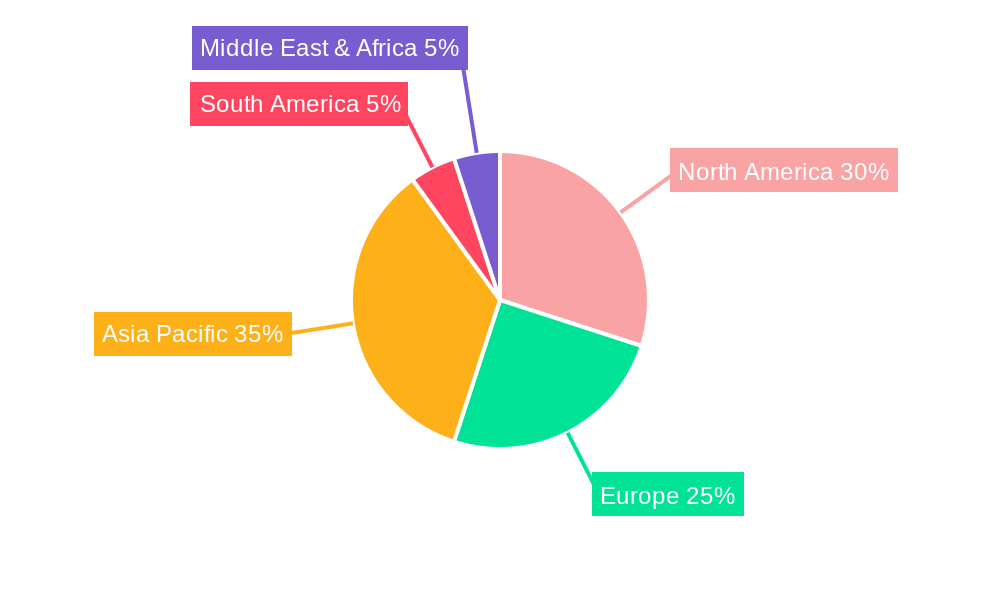

Key Region to Dominate the Market:

North America: This region is anticipated to maintain its leadership in the Hemostatic Materials market, driven by a robust healthcare infrastructure, high disposable incomes, and a strong emphasis on technological innovation. The presence of leading medical device manufacturers and research institutions, coupled with a high volume of complex surgical procedures, particularly in the United States, positions North America as a key market. The region's advanced healthcare reimbursement policies also facilitate the adoption of high-value hemostatic solutions. The market in North America is estimated to grow from approximately $2,800 million in 2025 to over $5,800 million by 2033. The region's proactive approach to adopting new medical technologies and its significant investment in R&D for hemostatic materials further solidify its dominant position.

Europe: Following closely behind North America, Europe represents another significant market. The region benefits from a well-established healthcare system, an aging population, and a growing demand for advanced medical treatments. Stringent quality standards and a focus on patient outcomes drive the adoption of innovative hemostatic materials. Countries like Germany, the UK, and France are major contributors to market growth. The European market is projected to expand from around $2,000 million in 2025 to over $4,000 million by 2033.

The interplay of these dominant segments and regions, coupled with the overall market expansion projected to exceed $15,000 million by 2033, underscores the critical importance of understanding these dynamics for strategic market positioning.

Several key factors are acting as significant growth catalysts for the hemostatic materials industry. The increasing prevalence of chronic diseases and the resultant rise in surgical procedures globally are primary drivers. Advancements in bio-engineering and material science are continuously leading to the development of more effective, biocompatible, and easily deployable hemostatic agents. The growing adoption of minimally invasive surgical techniques, which often require specialized bleeding control solutions, further fuels innovation and market expansion. Moreover, a heightened focus on patient safety and the reduction of post-operative complications are compelling healthcare providers to invest in advanced hemostatic materials.

This comprehensive report delves into the intricate Hemostatic Materials market, providing a detailed forecast from 2019-2033, with 2025 serving as the Base Year and Estimated Year. It meticulously analyzes the Historical Period: 2019-2024 and outlines projections for the Forecast Period: 2025-2033. The market is expected to witness substantial growth, soaring from an estimated $7,500 million in 2025 to surpass $15,000 million by 2033. This detailed analysis offers invaluable strategic intelligence for stakeholders, illuminating market dynamics, key growth drivers, potential challenges, and emerging opportunities within this vital sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5%.

Key companies in the market include Johnson & Johnson, BD, Baxter, B.Braun, Cura Medical, GELITA MEDICAL, Curasan AG, Meril Life Sciences, Zhonghui Shengxi, Beijing Datsing Bio-tech, Guizhou Jin Jiu Biotech, Beijing Taikesiman, Foryou Medical, Saikesaisi Holdings Group, Biotemed, YEK, HanBang, Trauer, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Hemostatic Materials," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Hemostatic Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.