1. What is the projected Compound Annual Growth Rate (CAGR) of the Heavy-Duty Automotive Aftermarket?

The projected CAGR is approximately 15.99%.

Heavy-Duty Automotive Aftermarket

Heavy-Duty Automotive AftermarketHeavy-Duty Automotive Aftermarket by Type (Class 4 to Class 6, Class 7 and Class 8), by Application (DIY, OE Seller, DIFM), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

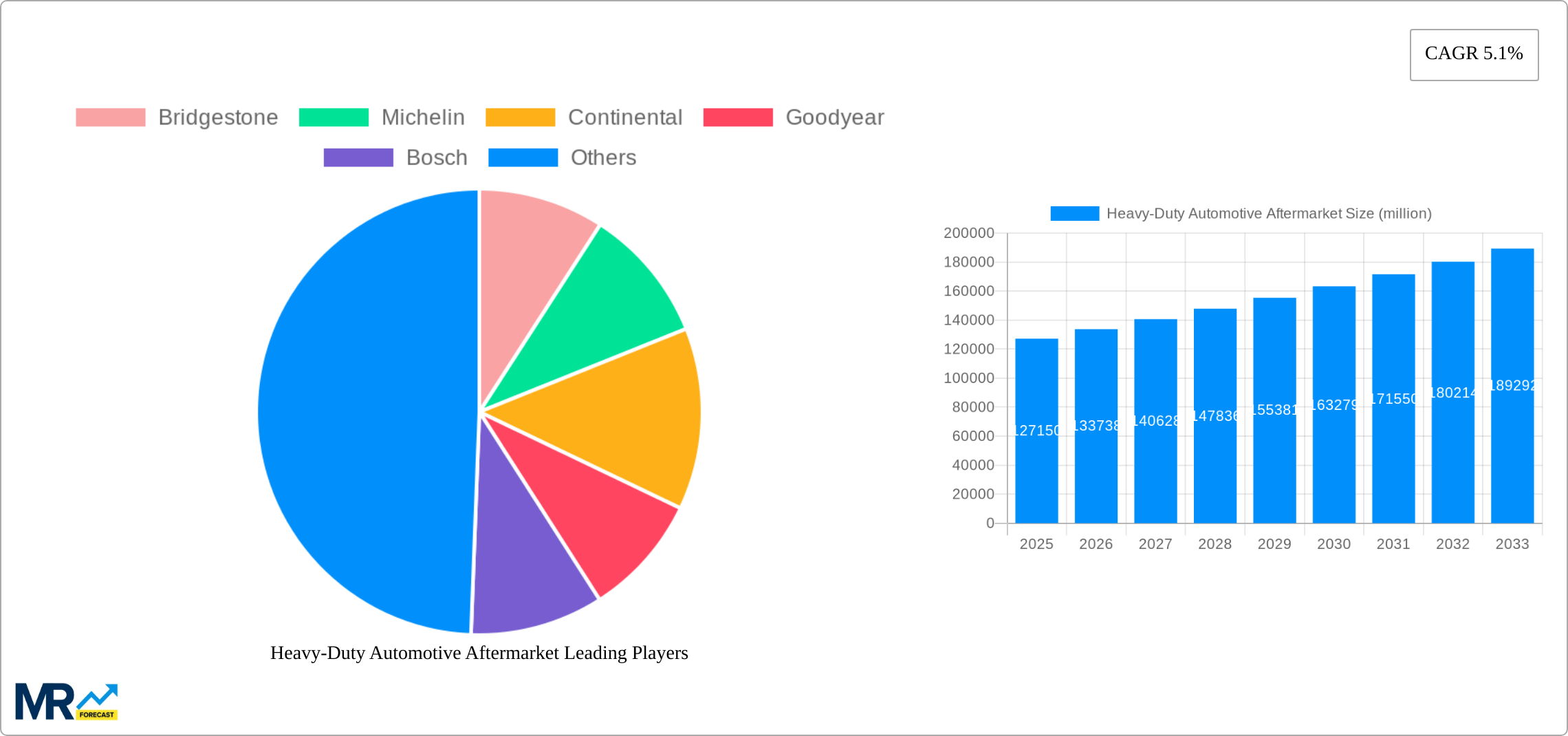

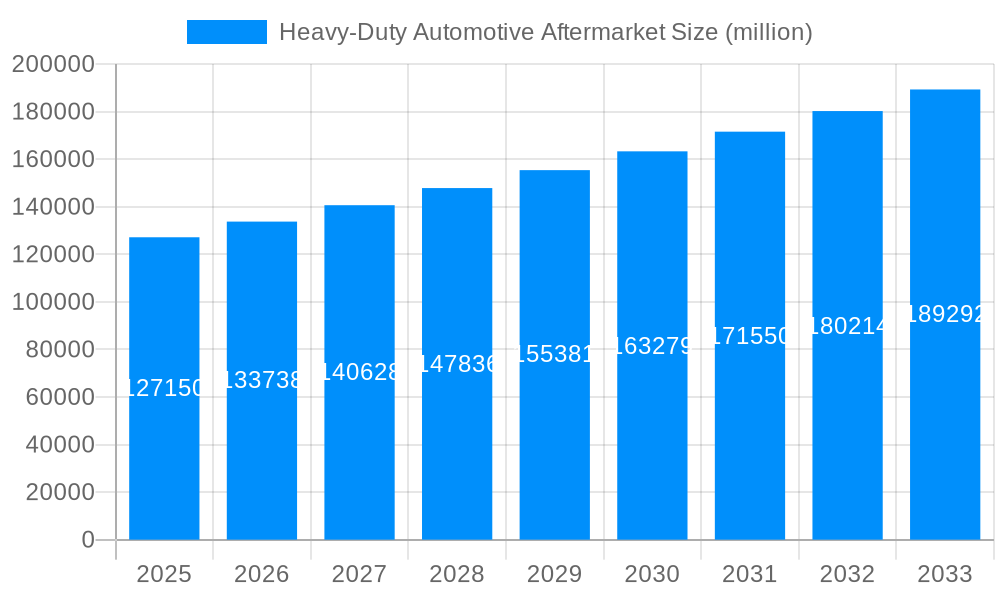

The heavy-duty automotive aftermarket, serving Class 4-8 vehicles, is forecasted to reach a market size of $13.33 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 15.99% from 2025 to 2033. This significant expansion is driven by several key factors: an aging vehicle fleet requiring increased maintenance and repairs, technological advancements enhancing fleet management and vehicle longevity, and stringent emission regulations necessitating compliance upgrades and servicing. The market is segmented by vehicle class (Class 4-6, Class 7 & 8) and by service channel (DIY, OE, and DIFM). While the DIY segment shows steady growth, the DIFM segment is particularly valuable due to the complexity of heavy-duty vehicle systems. Key market participants include Bridgestone, Michelin, Continental, Goodyear, and Bosch, who leverage strong brand recognition and extensive distribution. North America and Europe currently lead the market, with the Asia-Pacific region anticipating substantial growth due to infrastructure development and increased freight transport.

The competitive environment features established and emerging players employing strategies such as partnerships and acquisitions. While promising, the aftermarket faces challenges including fluctuating fuel prices, economic volatility, and potential technological disruptions. Nevertheless, the long-term outlook is positive, supported by increasing vehicle miles traveled, fleet expansion, and the continuous demand for parts and services across commercial trucking, construction, and mining sectors, underscoring the resilience of this market given the extended lifespans of heavy-duty vehicles.

The heavy-duty automotive aftermarket, encompassing parts and services for Class 4-8 vehicles, is experiencing robust growth, projected to reach several million units by 2033. The market's expansion is fueled by a confluence of factors, including the aging heavy-duty vehicle fleet, increasing freight transportation demands, and the growing adoption of advanced driver-assistance systems (ADAS) and telematics. The rising complexity of modern heavy-duty trucks necessitates more frequent maintenance and repairs, thereby boosting the demand for aftermarket parts and services. Furthermore, the increasing focus on vehicle uptime and operational efficiency is driving fleet owners to prioritize preventive maintenance and quick repair solutions. This trend is particularly pronounced in the Class 8 segment, which accounts for a significant portion of the market due to its prevalence in long-haul trucking and logistics. The DIY segment, while smaller than professional repair channels, is witnessing growth driven by the availability of online resources and readily accessible parts for simpler maintenance tasks. The rise of e-commerce platforms further facilitates this trend, allowing for convenient purchasing of parts and accessories. The estimated market value in 2025 is expected to be in the several billion-dollar range, reflecting the significant investment and opportunity within this sector. Competition is fierce among major players like Bridgestone, Michelin, and Bosch, pushing innovation and efficiency within the supply chain. The forecast period (2025-2033) anticipates continued market expansion driven by technological advancements and the unwavering demand for reliable heavy-duty vehicle operation.

Several key factors contribute to the growth of the heavy-duty automotive aftermarket. The aging heavy-duty truck fleet necessitates increased maintenance and repairs, significantly impacting demand for replacement parts and services. Stringent emission regulations are also a driver, leading to the adoption of advanced emission control systems and increasing the need for specialized maintenance and repairs. The rise of telematics and connected vehicles provides valuable data on vehicle performance, enabling predictive maintenance and reducing downtime. This proactive approach minimizes unexpected breakdowns and drives demand for preventative maintenance services. The increasing demand for faster repair turnaround times is pushing workshops and service providers to invest in advanced tools and technologies, increasing market growth. Furthermore, the expansion of the e-commerce sector has made purchasing aftermarket parts more convenient for both individual owners and large fleet operators, further stimulating market growth. The continuous development of new technologies and materials in the automotive industry means parts wear out differently from those in previous generations, creating a ripple effect on the aftermarket. Lastly, government regulations around vehicle safety and maintenance also fuel the need for regular checks and replacements.

Despite the significant growth potential, the heavy-duty automotive aftermarket faces several challenges. The high initial cost of heavy-duty vehicles and parts can be a barrier to entry for smaller players and independent repair shops. Furthermore, the complexity of modern heavy-duty trucks requires specialized skills and training for technicians, leading to a potential shortage of skilled labor. Fluctuating fuel prices and economic downturns can significantly impact freight transportation demand, thereby affecting aftermarket demand. The increasing adoption of electric and alternative fuel vehicles presents both opportunities and challenges, as it requires the aftermarket to adapt to new technologies and repair procedures. Counterfeit parts pose a significant threat to the industry, compromising vehicle safety and reliability. Supply chain disruptions, particularly evident in recent years, can cause delays and increased costs, affecting both manufacturers and consumers. Finally, intense competition among established players and the emergence of new entrants puts pressure on pricing and profit margins.

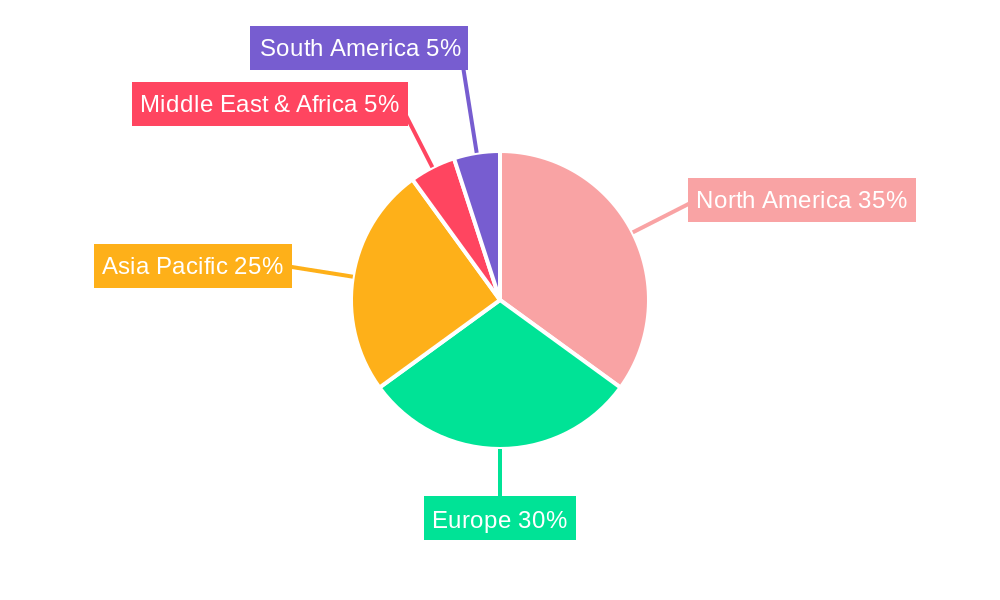

The North American market, particularly the United States and Canada, is expected to dominate the heavy-duty automotive aftermarket due to its large and aging fleet of heavy-duty trucks, high freight transportation volume, and well-established infrastructure for repair and maintenance services. Within this market, the Class 8 segment is projected to hold the largest share because Class 8 trucks are heavily used in long-haul trucking, requiring more frequent maintenance and repair due to their higher mileage.

North America's Dominance: The robust trucking industry, significant fleet sizes, and well-developed aftermarket ecosystem contribute to this region's leadership.

Class 8 Segment Leadership: The high mileage and demanding operational conditions of Class 8 trucks necessitate more frequent repairs and part replacements.

DIFM (Do-It-For-Me) Application: The majority of heavy-duty vehicle maintenance and repairs are handled by professional repair shops and fleets, contributing to this segment's large share.

The DIFM segment is poised for continued expansion due to the specialized knowledge and equipment required for heavy-duty vehicle maintenance. Fleet operators often prioritize minimizing downtime and maximizing vehicle uptime, leading them to contract professional services. The complexity of modern heavy-duty trucks and the implementation of advanced technologies necessitate specialized expertise and tooling that independent garages often lack. This segment's growth is further enhanced by the evolving landscape of technological advancements within the industry, which often require specialized equipment and training to repair and maintain vehicles effectively. The DIFM segment's dominance also stems from the inherent risks associated with DIY repairs on heavy-duty vehicles, making professional service a safer and more reliable option for fleet operators.

The heavy-duty automotive aftermarket is experiencing robust growth fueled by factors such as the increasing age and mileage of the existing heavy-duty vehicle fleet, the rising demand for freight transportation services, and the increasing complexity of modern vehicles leading to more frequent maintenance requirements. Furthermore, government regulations promoting vehicle safety and emission control also contribute significantly to the market's growth by demanding regular inspections and repairs. Technological advancements in telematics and predictive maintenance are improving vehicle uptime and driving the demand for preventative maintenance services.

This report provides a comprehensive analysis of the heavy-duty automotive aftermarket, covering market trends, driving forces, challenges, key players, and significant developments. The study period spans from 2019 to 2033, providing both historical and future perspectives on the market's evolution. This in-depth analysis offers valuable insights for businesses operating within the sector and investors looking to capitalize on the growth potential of this dynamic market. The report also delves into regional market dynamics, providing a granular understanding of market segmentation and dominant players within various regions.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.99% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 15.99%.

Key companies in the market include Bridgestone, Michelin, Continental, Goodyear, Bosch, Tenneco, ZF, Denso, 3M Company, Delphi, .

The market segments include Type, Application.

The market size is estimated to be USD 13.33 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Heavy-Duty Automotive Aftermarket," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Heavy-Duty Automotive Aftermarket, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.