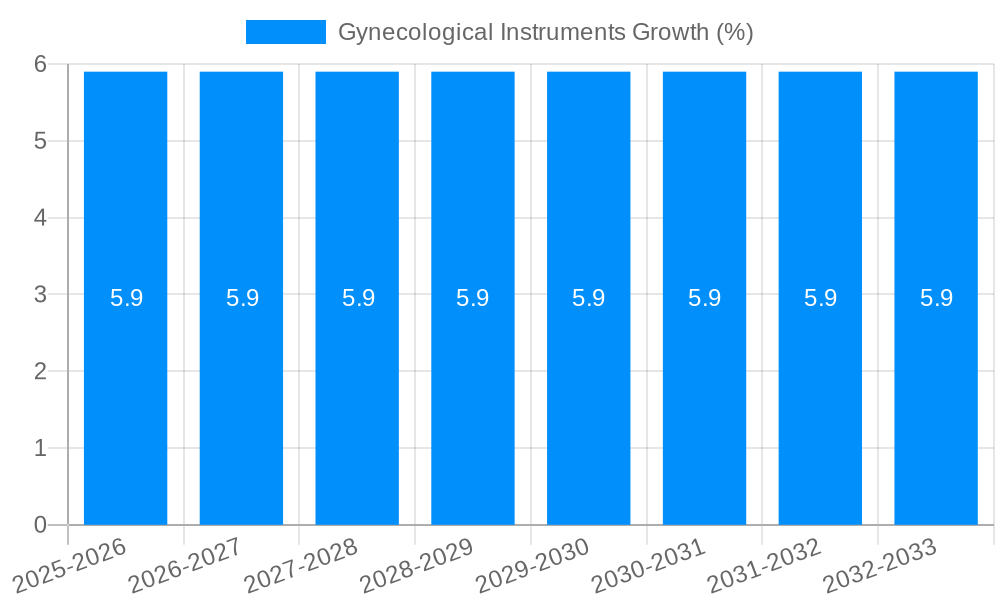

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gynecological Instruments?

The projected CAGR is approximately 5.9%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Gynecological Instruments

Gynecological InstrumentsGynecological Instruments by Type (Surgical Devices, Hand Instruments, Diagnostic Imaging Systems, Gynecological Chairs), by Application (Hospitals, Clinics and Ambulatory Surgical Centers), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

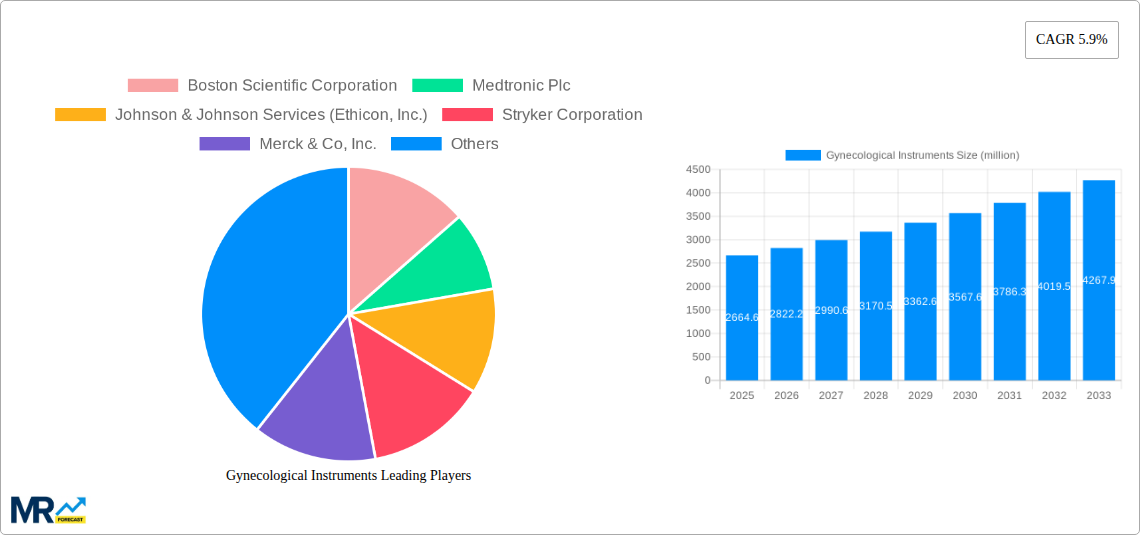

The global gynecological instruments market is poised for significant growth, projected to reach $2664.6 million by 2025 with a robust Compound Annual Growth Rate (CAGR) of 5.9% through 2033. This upward trajectory is fueled by an increasing global emphasis on women's reproductive health, rising awareness of various gynecological conditions, and advancements in diagnostic and surgical technologies. Key drivers include the growing incidence of gynecological cancers and other reproductive health issues, coupled with the expanding adoption of minimally invasive surgical techniques. These advancements, such as the development of sophisticated diagnostic imaging systems and precise surgical devices, are enhancing treatment efficacy and patient outcomes, thereby stimulating market demand. Furthermore, government initiatives promoting reproductive healthcare access and screening programs are also contributing to market expansion.

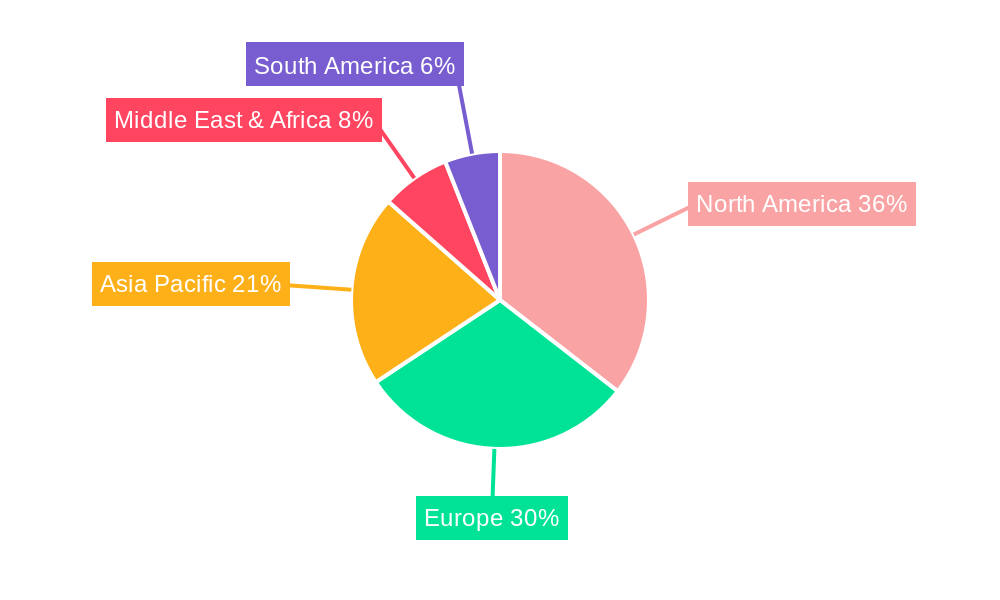

The market is segmented into crucial product categories, including advanced Surgical Devices, essential Hand Instruments, sophisticated Diagnostic Imaging Systems, and specialized Gynecological Chairs. Geographically, North America is anticipated to lead the market due to its well-established healthcare infrastructure, high disposable incomes, and early adoption of new medical technologies. Europe follows closely, driven by strong healthcare spending and an aging population requiring more advanced gynecological care. The Asia Pacific region, particularly China and India, presents substantial growth opportunities due to a large and growing female population, increasing healthcare expenditure, and a rising demand for better healthcare services. While the market benefits from technological innovation and increasing health consciousness, factors such as the high cost of advanced instruments and the need for skilled professionals to operate them could pose challenges.

The global gynecological instruments market is poised for significant expansion, driven by an increasing awareness of women's health, a rising incidence of gynecological disorders, and advancements in medical technology. XXX, the market is projected to reach a valuation of over \$15,000 million by 2033, showcasing a robust Compound Annual Growth Rate (CAGR) during the study period. This growth trajectory is underpinned by several key trends. Firstly, there's a pronounced shift towards minimally invasive surgical techniques. Patients and healthcare providers alike are increasingly favoring procedures that offer reduced recovery times, smaller incisions, and lower complication rates. This has spurred innovation in laparoscopic and hysteroscopic instruments, including advanced visualization systems and specialized surgical tools. Secondly, the integration of Artificial Intelligence (AI) and robotics is beginning to shape the future of gynecological diagnostics and surgery. AI-powered imaging analysis can aid in early detection of abnormalities, while robotic systems enhance precision and dexterity in complex procedures. Thirdly, the demand for advanced diagnostic imaging systems, such as ultrasound and MRI, tailored for gynecological applications, continues to surge. These technologies are crucial for accurate diagnosis and effective treatment planning for conditions ranging from fibroids and endometriosis to ovarian cysts and cancer. Furthermore, the market is witnessing a growing emphasis on patient comfort and accessibility, leading to innovations in gynecological chairs that offer enhanced ergonomics and integrated diagnostic capabilities. The increasing prevalence of chronic gynecological conditions, coupled with an aging global population, further fuels the demand for sophisticated and reliable gynecological instruments. The market is also benefiting from favorable reimbursement policies and increasing healthcare expenditure in emerging economies, expanding access to advanced gynecological care. The rising focus on preventive healthcare and routine screenings also contributes to the sustained demand for diagnostic instruments. Overall, the landscape is characterized by a dynamic interplay between technological innovation, evolving clinical needs, and a growing global commitment to women's reproductive health.

The substantial growth anticipated in the gynecological instruments market is propelled by a confluence of powerful driving forces. A primary catalyst is the increasing global burden of gynecological diseases. Conditions such as uterine fibroids, ovarian cysts, endometriosis, polycystic ovary syndrome (PCOS), and gynecological cancers are becoming more prevalent, necessitating a greater demand for diagnostic and surgical interventions. This escalating incidence directly translates into a higher need for specialized instruments to accurately diagnose, treat, and manage these conditions. Coupled with this is the growing awareness and advocacy surrounding women's health. Significant efforts by governmental organizations, non-profits, and healthcare providers have led to increased patient engagement and proactive health-seeking behaviors. Women are more informed about their reproductive health and are actively seeking regular check-ups and timely treatments, thereby boosting the demand for a wide array of gynecological instruments. Furthermore, the rapid pace of technological innovation is a critical engine of growth. Manufacturers are continuously investing in research and development to create more sophisticated, user-friendly, and effective instruments. This includes the development of advanced imaging technologies with higher resolution, smaller and more maneuverable surgical tools for minimally invasive procedures, and instruments incorporating smart features and connectivity. These advancements not only improve patient outcomes but also enhance the efficiency and capabilities of healthcare professionals. The supportive regulatory landscape and increasing healthcare investments, particularly in emerging economies, also play a pivotal role. Governments worldwide are recognizing the importance of women's health and are allocating more resources towards improving healthcare infrastructure and access to advanced medical technologies, further stimulating the market.

Despite the promising growth outlook, the gynecological instruments market is not without its challenges and restraints. A significant hurdle is the high cost associated with advanced gynecological instruments and procedures. Sophisticated diagnostic imaging systems, robotic surgical platforms, and specialized minimally invasive tools often come with a hefty price tag. This can limit their adoption, particularly in resource-constrained healthcare settings and developing nations, creating a disparity in access to cutting-edge treatments. Furthermore, the stringent regulatory approvals required for medical devices can prolong the time-to-market for new innovations. Companies must navigate complex approval processes from regulatory bodies like the FDA and EMA, which can be time-consuming and expensive, potentially slowing down the introduction of novel instruments. Reimbursement policies and healthcare economics also present a challenge. Inadequate reimbursement rates for certain procedures or devices can disincentivize healthcare providers from investing in the latest technologies. The constant pressure to control healthcare costs can lead to a preference for less expensive, albeit potentially less advanced, alternatives. Another restraint is the limited availability of skilled healthcare professionals. The effective use of advanced gynecological instruments, especially robotic systems and complex laparoscopic tools, requires specialized training and expertise. A shortage of adequately trained gynecologists and surgical staff can hinder the widespread adoption and utilization of these technologies. Finally, potential for complications and the need for extensive training associated with some advanced instruments, although often minimal in skilled hands, can create hesitancy among some practitioners and patients, acting as a subtle restraint on market expansion.

The global gynecological instruments market is projected to witness dominant growth in North America, with the Surgical Devices segment playing a pivotal role. This dominance is driven by a robust healthcare infrastructure, high disposable incomes, and a strong emphasis on advanced medical technologies. The United States, in particular, stands out as a key contributor due to its substantial investment in healthcare research and development, the presence of leading medical device manufacturers, and a proactive approach to adopting innovative surgical techniques. The increasing prevalence of gynecological disorders, coupled with a growing aging population, further fuels the demand for a wide range of gynecological instruments in this region.

Within the Surgical Devices segment, minimally invasive surgical instruments are expected to lead the market's expansion. This includes a wide array of laparoscopic instruments, hysteroscopes, and related accessories. The preference for minimally invasive procedures in North America is driven by their associated benefits, such as reduced patient trauma, shorter hospital stays, and quicker recovery times. This trend is further amplified by the increasing adoption of robotic-assisted surgery, which requires specialized instruments and significantly contributes to the growth of the Surgical Devices segment. Companies like Boston Scientific Corporation, Medtronic Plc, and Johnson & Johnson Services (Ethicon, Inc.) are at the forefront of innovation in this domain, offering a comprehensive portfolio of surgical devices.

The Diagnostic Imaging Systems segment is also a significant contributor to the market's growth in North America and is expected to maintain its strong position. Ultrasound, MRI, and other advanced imaging modalities are indispensable for the accurate diagnosis of a myriad of gynecological conditions, from routine screenings to complex cancer detection. The continuous advancements in imaging technology, leading to higher resolution, better visualization, and improved diagnostic capabilities, are key factors driving the demand for these systems. Companies such as Hologic, Inc. and Olympus Corporation are prominent players in this segment, offering state-of-the-art diagnostic imaging solutions.

The Application segment of Hospitals is expected to remain the largest end-user, followed by Clinics and Ambulatory Surgical Centers. Hospitals, with their comprehensive facilities and ability to handle complex surgical procedures, are primary consumers of a broad spectrum of gynecological instruments. However, the growing trend of outpatient procedures and the increasing focus on cost-effectiveness are leading to a significant expansion of the Clinics and Ambulatory Surgical Centers segment. These centers are increasingly investing in advanced instruments to offer a wider range of gynecological services, contributing to the overall market growth. The presence of established healthcare systems and a high patient volume makes North America a prime market for all segments, with Surgical Devices and Diagnostic Imaging Systems leading the charge in terms of market share and growth potential. The continuous efforts by leading players to develop and introduce novel instruments tailored for specific gynecological applications will further solidify the dominance of North America and the Surgical Devices segment in the coming years.

Several factors are acting as potent growth catalysts for the gynecological instruments industry. The rising global incidence of gynecological disorders such as endometriosis, uterine fibroids, and cancers directly translates into an increased need for diagnostic and therapeutic instruments. Furthermore, a growing emphasis on women's health and reproductive well-being is driving greater demand for regular screenings and advanced treatment options. Technological advancements, particularly in minimally invasive surgical techniques and advanced imaging technologies, are also crucial growth drivers, offering improved patient outcomes and reduced recovery times.

This comprehensive report offers an in-depth analysis of the global gynecological instruments market from 2019 to 2033, with a base year of 2025. It delves into key market insights, trends, and future projections, providing a holistic understanding of the industry landscape. The report meticulously examines the driving forces, challenges, and restraints shaping market dynamics, alongside identifying key regions and segments poised for dominance. Detailed information on leading players, significant industry developments, and growth catalysts ensures a thorough exploration of the market's trajectory. The study provides invaluable data for stakeholders seeking to navigate and capitalize on opportunities within this vital sector of women's healthcare.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.9% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.9%.

Key companies in the market include Boston Scientific Corporation, Medtronic Plc, Johnson & Johnson Services (Ethicon, Inc.), Stryker Corporation, Merck & Co, Inc., Olympus Corporation, Cooper Surgical, Inc., Hologic, Inc., Richard Wolf Gmbh, Karl Storz Gmbh & Co. KG, .

The market segments include Type, Application.

The market size is estimated to be USD 2664.6 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Gynecological Instruments," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Gynecological Instruments, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.