1. What is the projected Compound Annual Growth Rate (CAGR) of the Fuel Cell Vehicles?

The projected CAGR is approximately 54.2%.

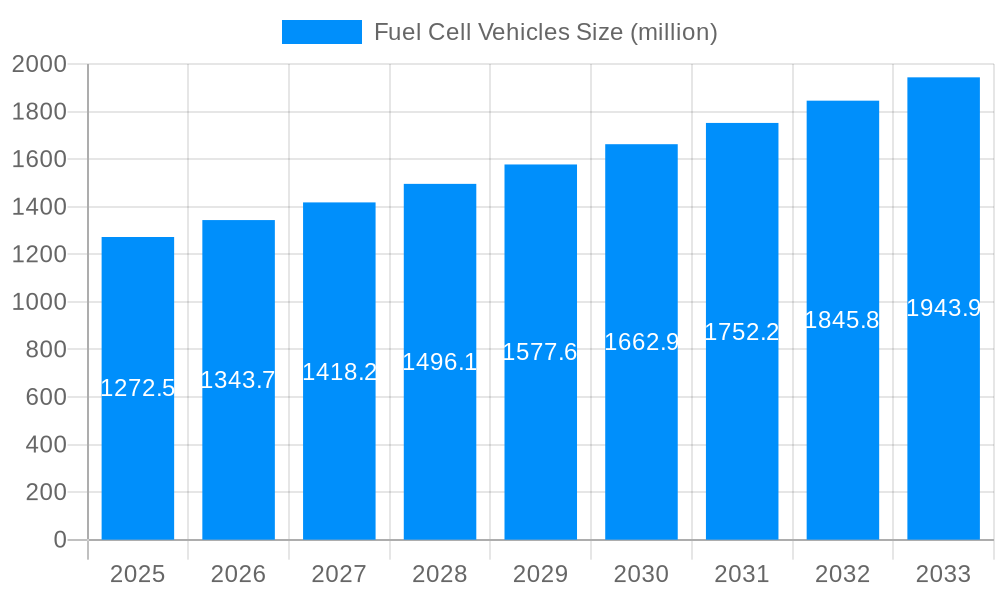

Fuel Cell Vehicles

Fuel Cell VehiclesFuel Cell Vehicles by Type (Proton Exchange Membrane Fuel Cell, Alkaline Fuel cell, Solid Oxide Fuel Cell), by Application (Forklifts, Airplanes, Submarines, Buses, Motorcycles & Bicycles, Trams, Boats), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The fuel cell vehicle (FCV) market is poised for significant growth, projected to reach a substantial size in the coming years. The market's Compound Annual Growth Rate (CAGR) of 5.3% from 2019 to 2033 indicates a steady expansion, driven by increasing concerns about environmental sustainability and the need for cleaner transportation solutions. Government regulations promoting emission reduction and incentives for adopting eco-friendly vehicles are further stimulating market growth. Technological advancements in fuel cell technology, leading to improved efficiency, durability, and reduced costs, are also key drivers. While the initial high cost of FCVs remains a restraint, economies of scale and continuous technological innovation are expected to mitigate this challenge. Furthermore, the development of a robust hydrogen refueling infrastructure is crucial for widespread FCV adoption, and significant investments in this area are paving the way for broader market penetration. Key players like Toyota, Honda, Hyundai, and various automotive component suppliers are actively engaged in research, development, and commercialization efforts, intensifying competition and fostering innovation within the sector.

The market segmentation likely involves various vehicle types (cars, buses, trucks), power output ranges, and application sectors (passenger transport, commercial transport). Regional variations in market penetration will depend on factors like government policies, infrastructure development, and consumer preferences. North America and Europe are expected to be leading markets, driven by strong environmental regulations and a focus on renewable energy. Asia-Pacific is also anticipated to witness notable growth, spurred by increasing urbanization, industrialization, and rising environmental awareness. However, challenges remain, including the need for continued improvement in fuel cell technology, the expansion of hydrogen refueling infrastructure, and addressing consumer concerns about range anxiety and refueling time. Despite these challenges, the long-term outlook for the FCV market remains positive, driven by the inherent advantages of fuel cell technology in terms of efficiency, performance, and reduced emissions.

The fuel cell vehicle (FCV) market, while still nascent compared to battery electric vehicles (BEVs), is experiencing a period of significant transformation. The study period from 2019 to 2033 reveals a market trajectory marked by both promising advancements and persistent challenges. While the historical period (2019-2024) showed relatively slow growth, primarily due to high production costs and limited refueling infrastructure, the estimated year of 2025 signals a potential inflection point. By 2025, several key factors, including technological improvements, increasing government support, and growing environmental concerns, are projected to spur a more rapid expansion. The forecast period (2025-2033) anticipates substantial growth, with projections of millions of units sold annually by the end of the decade. This growth, however, is not uniform across all regions or vehicle segments. Early adoption is expected in regions with strong government incentives and existing hydrogen infrastructure, while certain vehicle segments, particularly heavy-duty vehicles and buses, are projected to see faster uptake than passenger cars. The market's success hinges on resolving several critical challenges, including reducing the cost of fuel cell stacks and increasing the availability of hydrogen refueling stations. Overcoming these obstacles will be crucial to unlocking the full potential of FCVs and enabling them to compete effectively with established automotive technologies. This report delves into the multifaceted dynamics of the FCV market, providing insights into the driving forces, challenges, key players, and future growth prospects. The analysis is based on extensive research, encompassing technological advancements, market trends, competitive landscapes, and regulatory frameworks impacting the industry, aiming to offer a comprehensive understanding of the FCV market's evolution and future trajectory. The estimated market size in millions of units by 2025 forms a key benchmark for analyzing growth.

Several powerful forces are propelling the growth of the fuel cell vehicle market. Firstly, the increasing urgency to mitigate climate change and reduce carbon emissions is a major catalyst. FCVs offer a compelling zero-tailpipe emission solution, aligning perfectly with global sustainability goals. Governments worldwide are implementing supportive policies, including tax incentives, subsidies, and the development of hydrogen infrastructure, further boosting market adoption. Technological advancements are also crucial, with continuous improvements in fuel cell efficiency, durability, and cost-effectiveness making FCVs a more attractive proposition. The longer driving range and faster refueling times compared to BEVs are significant advantages, particularly for heavy-duty vehicles and long-distance travel. Furthermore, the growing demand for sustainable transportation solutions in various sectors, from passenger vehicles to commercial fleets and public transportation, presents a vast market opportunity for FCVs. The strategic investments by major automotive manufacturers and fuel cell technology companies indicate a strong belief in the long-term viability of this technology. The convergence of these factors—environmental concerns, governmental support, technological progress, and expanding market demand—is creating a powerful synergy driving the expansion of the FCV market.

Despite the promising outlook, the FCV market faces several significant challenges and restraints. The high initial cost of fuel cell vehicles remains a major barrier to widespread adoption. The cost of producing fuel cell stacks, a core component of the vehicle, is considerably higher than that of battery packs for BEVs. This cost differential translates into higher vehicle prices, impacting affordability and consumer appeal. The limited availability of hydrogen refueling infrastructure is another critical bottleneck. The lack of a widespread network of hydrogen fueling stations restricts the practicality and convenience of FCVs, particularly for long-distance travel. The infrastructure development requires substantial investment and time, posing a significant hurdle to market penetration. Furthermore, safety concerns related to hydrogen storage and handling need to be addressed effectively to build consumer confidence. Concerns about hydrogen embrittlement and the potential for explosions need to be mitigated through improved safety protocols and regulatory frameworks. The relatively low energy density of hydrogen compared to gasoline also presents a challenge in terms of storage space and weight, potentially impacting vehicle performance and efficiency. Overcoming these obstacles requires collaborative efforts from governments, industry players, and research institutions to develop cost-effective technologies, build robust infrastructure, and address safety concerns.

The FCV market is expected to witness diverse growth patterns across different regions and segments.

Regions: Countries with strong government support for hydrogen infrastructure and environmental regulations are likely to lead the adoption curve. For example, Japan, South Korea, and certain European nations have already made significant investments in hydrogen technology and are likely to witness faster market growth. North America, driven by increasing environmental awareness and supportive policies, will also see considerable growth. China’s expanding hydrogen infrastructure and focus on clean energy also positions it for substantial market share.

Segments: The heavy-duty vehicle (HDV) segment is projected to experience faster growth compared to passenger cars. The longer driving ranges, faster refueling, and reduced emissions offered by FCVs make them particularly attractive for applications such as long-haul trucking, buses, and other commercial vehicles where battery-electric solutions may be less practical. The material handling and stationary power segments are also expected to show significant growth, as fuel cells offer efficient and clean power solutions for these applications. Passenger cars, while a significant market potential in the long term, will likely see a slower initial uptake due to factors such as price and infrastructure limitations.

In summary: While specific market shares will depend on various factors, including technological advancements and government policies, a multi-regional approach to market growth is likely with a leading role for countries actively promoting hydrogen infrastructure. The HDV segment will probably lead the way in terms of growth rate due to its unique advantages over battery-electric alternatives. The passenger car segment, though important, will require further developments in cost reduction and infrastructure expansion before achieving widespread adoption.

Several factors are poised to accelerate the growth of the FCV industry. Continued technological advancements, particularly in fuel cell stack efficiency and durability, are crucial for cost reduction and performance enhancement. Government incentives, such as tax credits and subsidies, play a key role in stimulating market demand. The development and expansion of hydrogen refueling infrastructure is essential for increasing the practicality and convenience of FCVs. Growing public awareness of environmental issues and the desire for sustainable transportation options are driving consumer interest in fuel cell technology. Finally, strategic collaborations and investments by major automotive manufacturers and energy companies demonstrate the increasing confidence in the long-term viability of FCVs.

This report provides a comprehensive overview of the fuel cell vehicle market, encompassing historical data, current market dynamics, and future projections. It covers key market trends, driving forces, challenges, and growth catalysts. The report also analyzes the competitive landscape, highlighting leading players and their strategies. Furthermore, it provides detailed regional and segment-level analysis, offering insights into the diverse growth patterns within the industry. The report's in-depth analysis and forecasts offer valuable guidance to stakeholders in the fuel cell vehicle sector, including manufacturers, investors, and policymakers. The comprehensive coverage ensures a thorough understanding of the market's evolution and future potential.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 54.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 54.2%.

Key companies in the market include Acumentrics SOFC Corporation, Automotive Fuel Cell Cooperation Corp, Ballard Power Systems, BMW, Audi, GreenGT, Proton Power Systems, Hydrogenics, Nissan, Toyota Motor Corporation, Daimler, Ballard, VW Group, .

The market segments include Type, Application.

The market size is estimated to be USD 3.74 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Fuel Cell Vehicles," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Fuel Cell Vehicles, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.