1. What is the projected Compound Annual Growth Rate (CAGR) of the Food & Beverage Metal Packaging Container?

The projected CAGR is approximately 5.1%.

Food & Beverage Metal Packaging Container

Food & Beverage Metal Packaging ContainerFood & Beverage Metal Packaging Container by Type (Three-Piece Can, Two-piece Can), by Application (Food Industry, Beverage Industry), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

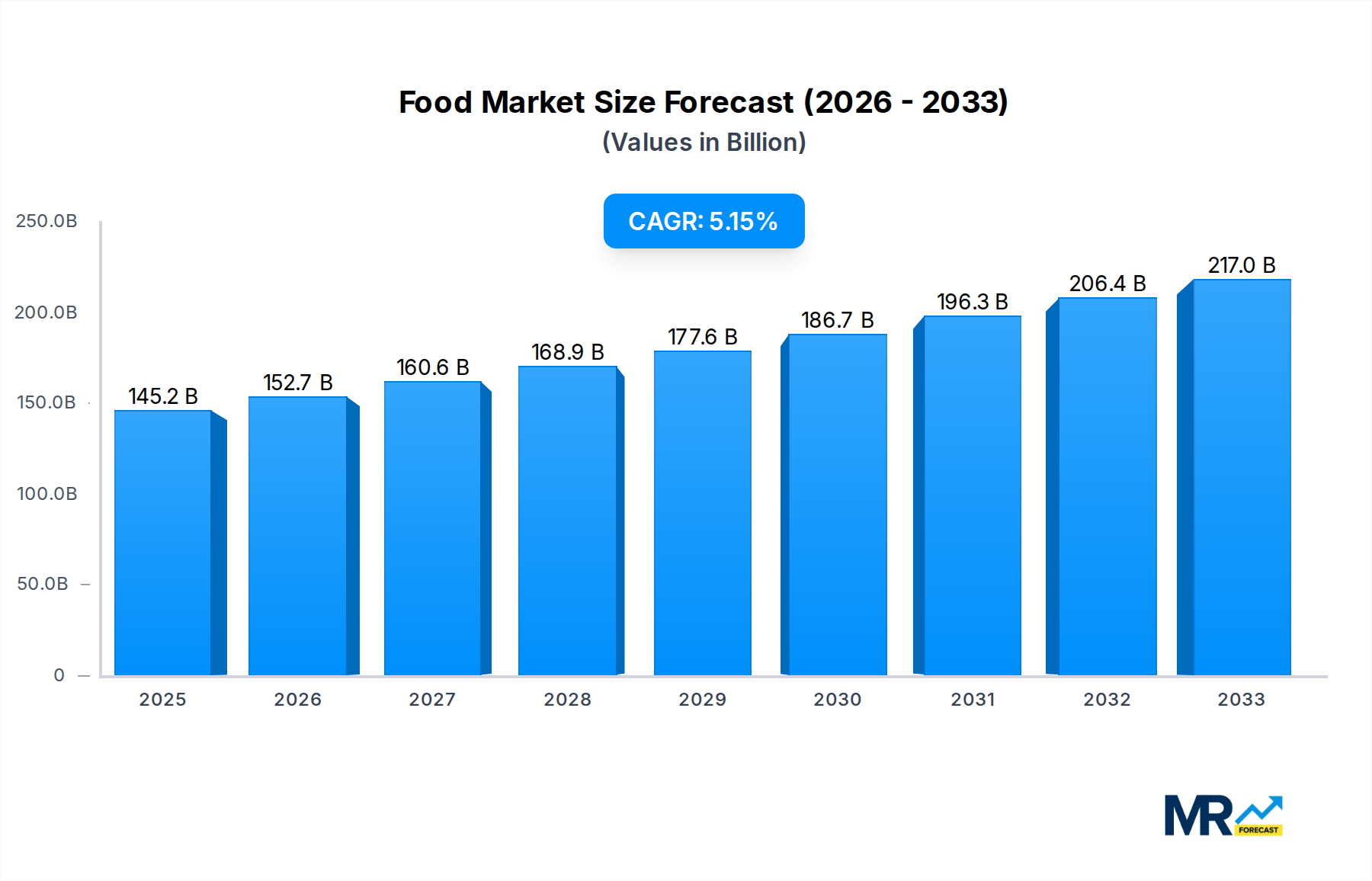

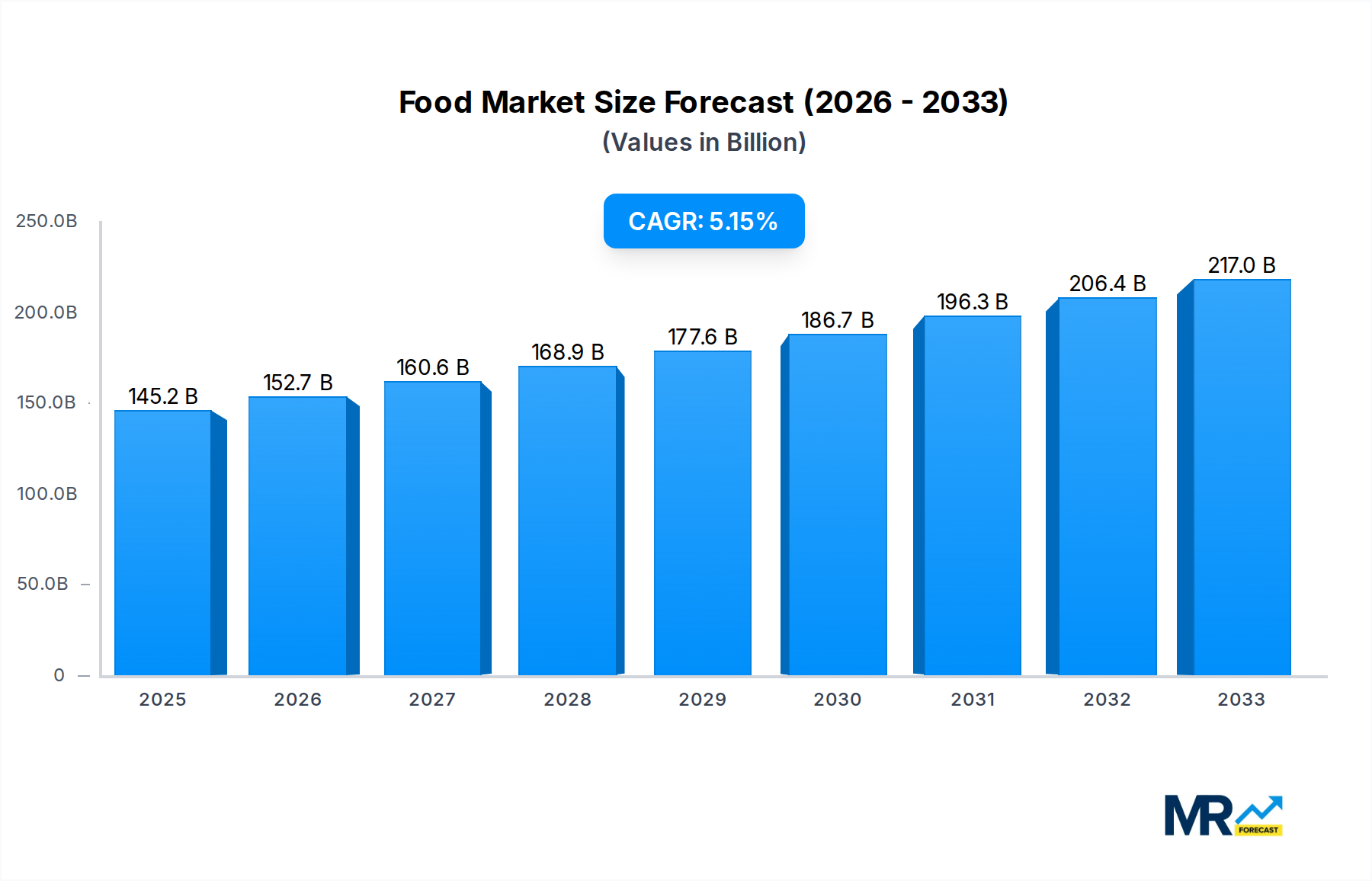

The global Food & Beverage Metal Packaging Container market is projected to experience robust growth, estimated at \$145.2 billion in 2025, with a Compound Annual Growth Rate (CAGR) of 5.1% anticipated between 2025 and 2033. This expansion is primarily fueled by the increasing consumer demand for convenient and durable packaging solutions in both the food and beverage sectors. The rising global population, coupled with evolving lifestyle trends favoring ready-to-eat meals and a growing preference for canned beverages due to their shelf-life and portability, are significant drivers. Furthermore, the inherent recyclability and sustainability aspects of metal packaging, particularly aluminum and steel, are aligning with growing environmental consciousness among consumers and stricter regulatory frameworks promoting circular economy principles, making metal containers a preferred choice for many manufacturers. The market's segmentation into Three-Piece Cans and Two-Piece Cans caters to diverse product needs, with the Food Industry and Beverage Industry representing the dominant application areas.

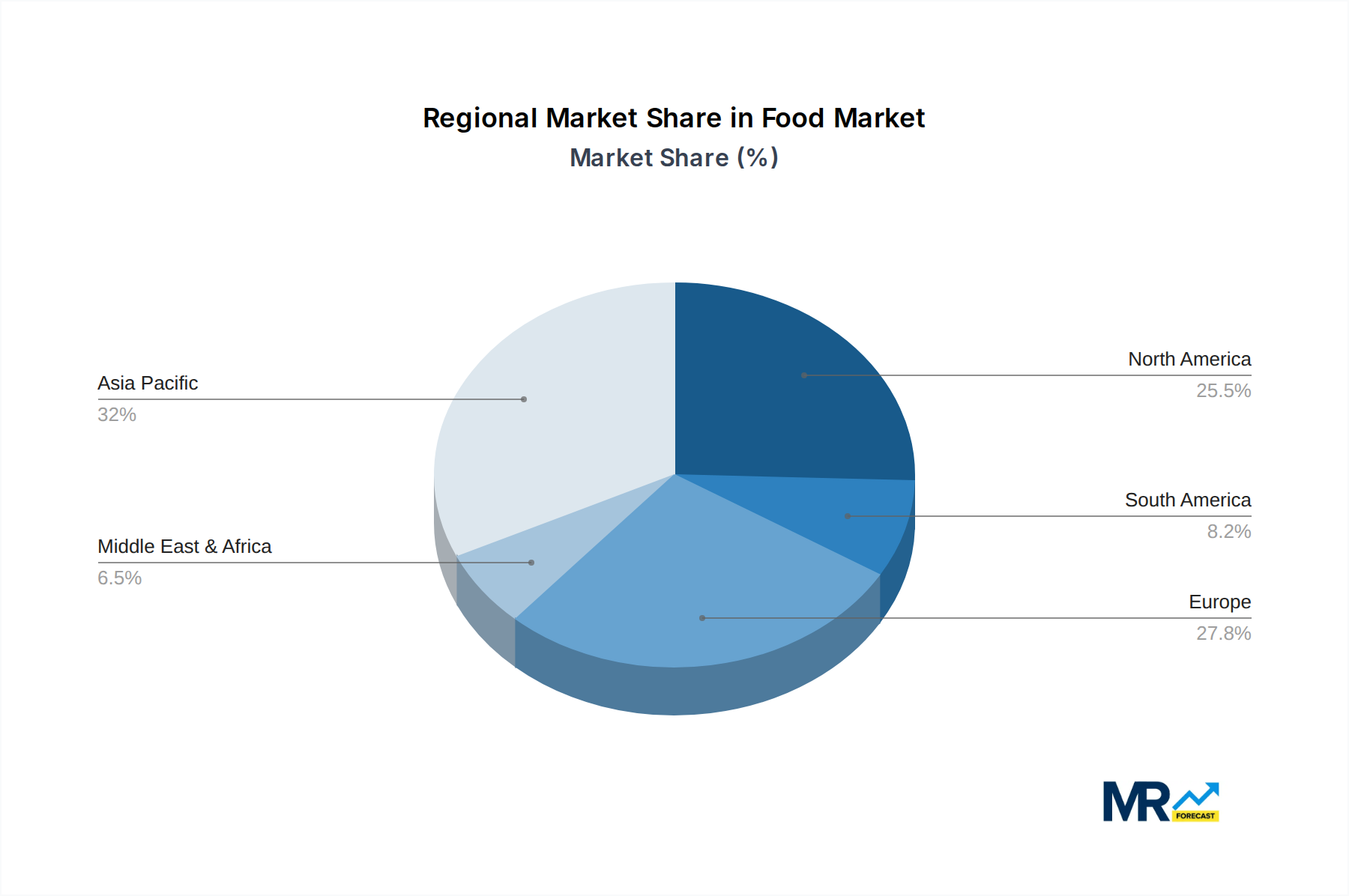

Key trends shaping the Food & Beverage Metal Packaging Container market include advancements in can manufacturing technologies leading to lighter yet stronger containers, the adoption of sophisticated printing and labeling techniques enhancing brand appeal, and a growing emphasis on sustainable practices throughout the supply chain. Companies are investing in research and development to optimize material usage and reduce their environmental footprint. However, the market is not without its challenges. Fluctuations in the prices of raw materials like aluminum and steel, as well as increasing competition from alternative packaging materials such as flexible packaging and glass, could present restraints. Despite these hurdles, the established infrastructure, proven efficacy, and ongoing innovation within the metal packaging industry are expected to sustain its upward trajectory, with significant growth opportunities anticipated across major regions like Asia Pacific, North America, and Europe.

This comprehensive report provides an in-depth analysis of the global Food & Beverage Metal Packaging Container market, meticulously examining trends, driving forces, challenges, and future growth trajectories. Spanning a detailed study period from 2019 to 2033, with a base year and estimated year of 2025, and a forecast period from 2025 to 2033, the report leverages historical data from 2019-2024 to offer robust market insights. The analysis delves into the intricate dynamics of the market, offering invaluable perspectives for stakeholders seeking to understand the evolving landscape of metal packaging solutions for the food and beverage industries. It aims to equip readers with the knowledge necessary to make informed strategic decisions in this dynamic sector.

XXX The global Food & Beverage Metal Packaging Container market is experiencing a significant evolution, driven by a confluence of consumer preferences, technological advancements, and increasing environmental consciousness. The market, which is expected to see substantial growth, is characterized by a discernible shift towards more sustainable and convenient packaging formats. Global market value is projected to reach several hundred billion units by the end of the forecast period, underscoring the immense scale and importance of this sector. A key trend is the increasing adoption of two-piece cans, which are gaining prominence over traditional three-piece cans due to their perceived aesthetic appeal, lighter weight, and superior sealing capabilities, especially within the beverage industry. This preference is fueled by brands seeking to enhance shelf appeal and optimize logistics.

Furthermore, the food industry is witnessing a renewed interest in metal packaging, particularly for premium and specialty products. The inherent barrier properties of metal, offering excellent protection against light, oxygen, and moisture, remain a significant draw for preserving the quality and extending the shelf-life of a wide array of food products, from ready-to-eat meals to sauces and pet food. Innovation in metal can design and functionality is another pivotal trend. Manufacturers are investing heavily in research and development to introduce cans with enhanced features such as easy-open lids, resealable options, and improved internal coatings that are free from harmful chemicals like BPA. These advancements directly address consumer demand for convenience and health-conscious packaging. The growing emphasis on recyclability and the circular economy is also a powerful driver. Metal, being infinitely recyclable without loss of quality, aligns perfectly with global sustainability goals, making metal containers a preferred choice for environmentally aware consumers and brands. This inherent recyclability is not just a trend but a fundamental characteristic that solidifies the long-term viability of metal packaging in the face of stringent environmental regulations and evolving consumer ethics.

The Food & Beverage Metal Packaging Container market is being propelled by a multifaceted array of factors that are collectively shaping its growth trajectory. Paramount among these is the ever-increasing global demand for packaged food and beverages. As populations grow and urbanization continues, the need for convenient, safe, and long-lasting food and beverage products rises, directly translating into higher demand for packaging solutions like metal cans. The superior barrier properties of metal remain a cornerstone of its appeal. Its ability to protect contents from light, oxygen, moisture, and other external contaminants is critical for maintaining product freshness, extending shelf life, and preventing spoilage, especially for sensitive food items and beverages. This inherent protective quality is a significant advantage over many alternative packaging materials, ensuring product integrity from production to consumption.

Moreover, the growing consumer preference for sustainable and recyclable packaging is a powerful catalyst. Metal, being infinitely recyclable, aligns with the global push towards a circular economy and reducing environmental impact. This inherent eco-friendliness resonates strongly with environmentally conscious consumers and incentivizes brands to opt for metal packaging to enhance their sustainability credentials. The convenience offered by metal cans is also a significant driving force. Their portability, durability, and ease of use, particularly with the advent of easy-open lids and resealable designs, cater to modern lifestyles and on-the-go consumption patterns. The cost-effectiveness and operational efficiencies associated with metal packaging production and transportation, when scaled, also contribute to its widespread adoption across various food and beverage segments.

Despite its robust growth, the Food & Beverage Metal Packaging Container market faces several challenges and restraints that can temper its expansion. A primary concern is the volatility in the prices of raw materials, particularly aluminum and steel. Fluctuations in global commodity markets can significantly impact production costs, leading to price pressures for manufacturers and potentially affecting the overall affordability of metal packaging. This unpredictability can make long-term strategic planning and pricing difficult for industry players. Another significant challenge is the increasing competition from alternative packaging materials. Plastics, particularly in the form of flexible pouches and PET bottles, offer perceived advantages such as lower weight, lower cost, and design flexibility, posing a substantial competitive threat, especially in certain beverage segments. While metal offers superior barrier properties, the marketing and convenience factors of plastics can sometimes outweigh these benefits for specific applications.

The environmental perception and actual waste management issues can also act as restraints. While metal is highly recyclable, the actual recycling rates can vary significantly by region due to differing infrastructure, consumer habits, and governmental policies. Instances of improper disposal and landfill accumulation can negatively impact the perception of metal packaging as a truly sustainable solution. Furthermore, technological limitations and capital investment requirements for advanced metal packaging technologies can be a barrier for smaller manufacturers. Developing and implementing new designs, coatings, and production processes often requires substantial upfront investment, which can be a deterrent. Finally, stringent regulatory landscapes and evolving standards related to food contact materials and environmental impact can impose compliance burdens on manufacturers, necessitating ongoing investment in research, development, and quality control to meet these ever-changing requirements.

The Food & Beverage Metal Packaging Container market is characterized by regional dominance and segment leadership, with specific areas and product types exhibiting exceptional growth and market share.

Dominant Region/Country:

Dominant Segment:

The Food & Beverage Metal Packaging Container industry is propelled by several key growth catalysts. The burgeoning global population and rising disposable incomes are driving increased consumption of packaged food and beverages, directly boosting demand for metal containers. Furthermore, a growing consumer preference for sustainable and recyclable packaging solutions aligns perfectly with metal's inherent recyclability, making it an attractive choice for environmentally conscious brands and consumers. Innovations in can technology, such as improved coatings, easy-open features, and enhanced aesthetic designs, are also contributing significantly by offering greater convenience and appeal.

This comprehensive report offers an exhaustive exploration of the global Food & Beverage Metal Packaging Container market. It meticulously analyzes market dynamics, encompassing historical performance, current trends, and future projections up to 2033. The report provides granular insights into driving forces, challenges, regional market landscapes, and dominant segments, offering a holistic view of the industry's ecosystem. Furthermore, it highlights key growth catalysts and the strategic developments undertaken by leading industry players. This in-depth analysis is designed to equip stakeholders with the essential knowledge for informed decision-making and strategic planning within this vital sector of the packaging industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.1%.

Key companies in the market include Ball Corporation, Crown Holdings, Ardagh Group, Toyo Seikan, Silgan Holdings Inc, Can Pack Group, BWAY Corporation, ORG Technology, CPMC Holdings, Hokkan Holdings, Baosteel Packaging, Showa Aluminum Can Corporation, ShengXing Group, .

The market segments include Type, Application.

The market size is estimated to be USD 145.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Food & Beverage Metal Packaging Container," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Food & Beverage Metal Packaging Container, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.