1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Control System Integrator?

The projected CAGR is approximately 8.2%.

Electronic Control System Integrator

Electronic Control System IntegratorElectronic Control System Integrator by Application (Commercial Vehicle, Passenger Vehicle, World Electronic Control System Integrator Production ), by Type (Vehicle Factory, Third Party Integrators, World Electronic Control System Integrator Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The Electronic Control System Integrator (ECSI) market is experiencing robust growth, driven by the increasing demand for advanced driver-assistance systems (ADAS) and electric vehicles (EVs). The integration of complex electronic systems in modern vehicles necessitates specialized integrators capable of managing the intricate interplay of various components. This market is segmented by application (commercial and passenger vehicles) and type of integrator (vehicle factory and third-party). While precise figures are unavailable, the market's substantial size and Compound Annual Growth Rate (CAGR) suggest a lucrative and expanding sector. The prominence of companies like BYD, Hyundai, and several Chinese automotive technology firms highlights the significant presence of both established automotive manufacturers and specialized technology providers. The geographic distribution shows a strong concentration in Asia-Pacific, particularly China, reflecting the region's rapid growth in vehicle production and technological advancement. North America and Europe also represent significant markets, driven by the increasing adoption of advanced safety features and the transition towards electric mobility. Continued growth hinges on factors such as increasing automation in vehicle production, the rising demand for connected car features, and the ongoing development of autonomous driving technologies. However, challenges remain including the complexities of integrating diverse systems, potential supply chain disruptions, and the high initial investment required for advanced technology adoption.

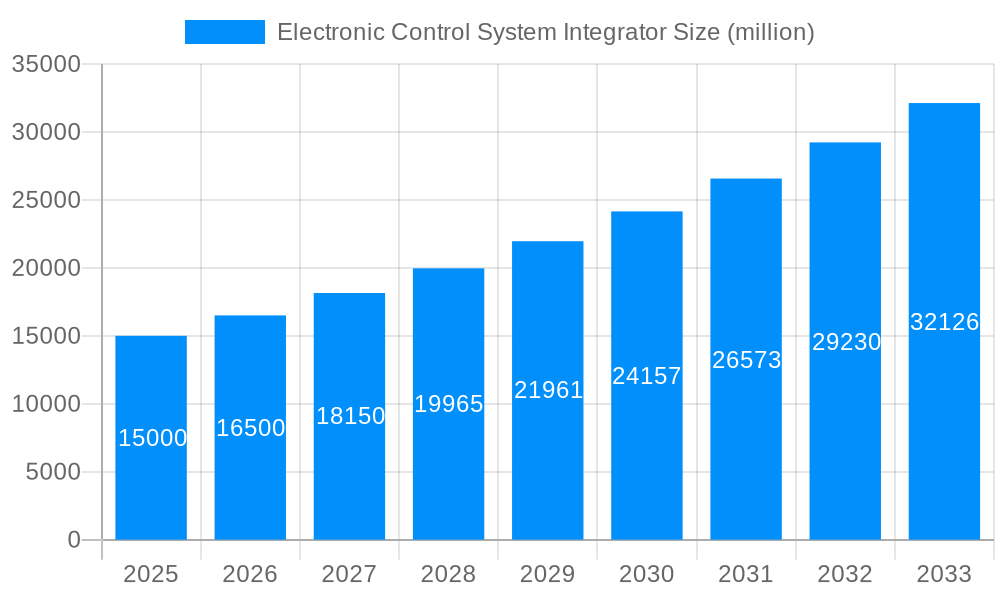

The ECSI market's future trajectory is promising, predicting steady growth throughout the forecast period (2025-2033). Factors like government regulations promoting fuel efficiency and emission reduction will further propel market expansion. The competitive landscape is dynamic, with both established automotive giants and innovative technology companies vying for market share. Strategic partnerships and mergers and acquisitions are likely to play a crucial role in shaping the market's future. The continuing emphasis on technological innovation, such as the development of more efficient and reliable electronic control systems, will be critical to sustained growth. Furthermore, the expansion into new geographical markets, particularly in developing economies, offers significant potential for expansion and growth.

The global electronic control system (ECS) integrator market is experiencing robust growth, driven by the burgeoning automotive industry and the increasing demand for advanced driver-assistance systems (ADAS) and electric vehicles (EVs). The market, valued at over 100 million units in 2024, is projected to surpass 250 million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 10%. This expansion is fueled by several factors, including stricter emission regulations globally, prompting automakers to adopt more sophisticated ECS to optimize engine performance and reduce emissions. Furthermore, the rising consumer preference for feature-rich vehicles, such as those equipped with autonomous driving capabilities and improved safety features, significantly boosts the demand for integrated ECS solutions. The market is witnessing a shift towards more sophisticated and integrated systems, moving away from standalone components. This trend is driven by the increasing complexity of modern vehicles and the need for seamless communication between various subsystems. This integration necessitates specialized expertise and skills, leading to the growth of third-party integrators alongside in-house teams within vehicle factories. The shift towards electric and hybrid vehicles is a particularly significant trend, as these vehicles rely heavily on complex electronic control units (ECUs) to manage battery power, motor control, and other critical functions. This increased complexity is directly linked to the growth of the ECS integrator market. Finally, the ongoing development of advanced technologies, such as artificial intelligence (AI) and machine learning (ML), is further pushing the boundaries of ECS functionality, creating new opportunities for innovation and growth within the industry. This continuous technological advancement ensures that the market will remain dynamic and lucrative in the coming years.

Several key factors are driving the expansion of the electronic control system integrator market. Firstly, the global push towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) is a major catalyst. EVs require far more sophisticated electronic control systems to manage battery power, motor control, and charging processes than traditional internal combustion engine (ICE) vehicles. This increased complexity translates directly into higher demand for specialized integrators with the expertise to design, install, and maintain these systems. Secondly, the growing adoption of advanced driver-assistance systems (ADAS) features, such as adaptive cruise control, lane departure warning, and autonomous emergency braking, necessitates intricate ECS integration. These systems require seamless communication between various sensors, actuators, and control units, creating opportunities for both vehicle manufacturers and specialized integrators. Thirdly, stringent government regulations worldwide aimed at reducing vehicle emissions and improving fuel efficiency are impacting the automotive landscape. Meeting these increasingly stringent standards necessitates sophisticated ECS capable of optimizing engine performance and reducing harmful emissions. This regulatory pressure is a crucial driver for innovation and adoption of advanced ECS solutions, leading to higher demand for skilled integrators. Lastly, the continuous advancements in electronic components and software, including the adoption of artificial intelligence and machine learning within vehicle systems, are creating a more dynamic and complex market, requiring specialized expertise to manage integration and optimization.

Despite the significant growth potential, the electronic control system integrator market faces several challenges. The increasing complexity of modern vehicles and the resulting need for highly specialized expertise poses a significant hurdle for many integrators. Attracting and retaining skilled engineers and technicians with the necessary expertise in software, hardware, and automotive systems is a persistent challenge. Moreover, the highly competitive nature of the automotive industry necessitates constant innovation and cost optimization, placing pressure on integrators to deliver efficient and cost-effective solutions. The rapid pace of technological advancements necessitates ongoing investments in research and development to keep up with emerging trends and technologies, which can be resource-intensive. Furthermore, ensuring the cybersecurity of increasingly complex electronic systems is a critical concern. Vulnerabilities in the ECS can expose vehicles to cyberattacks, potentially leading to serious safety and security risks. Addressing these cybersecurity challenges requires substantial investment in robust security protocols and measures. Finally, the global supply chain disruptions and component shortages witnessed in recent years have highlighted the fragility of the automotive supply chain. These disruptions can impact the availability of critical components and delay project timelines, affecting the profitability and efficiency of integrators.

The Asia-Pacific region, particularly China, is poised to dominate the electronic control system integrator market due to its substantial automotive manufacturing base and the rapid growth of its EV sector. China's strong government support for the EV industry, coupled with its massive consumer market, creates a significant demand for ECS integrators.

Asia-Pacific (China): This region is the global leader in terms of both vehicle production and the adoption of EVs, creating substantial demand for ECS integrators. The sheer volume of vehicles produced translates into a high demand for integration services.

Europe: While slightly behind Asia-Pacific, Europe is a significant market, driven by stringent emission regulations and the growing popularity of EVs. European automakers are early adopters of advanced technologies, contributing to the high demand for sophisticated integration services.

North America: The North American market shows steady growth, driven by increased demand for advanced driver-assistance systems (ADAS) and a growing transition toward EVs.

Dominant Segment: Passenger Vehicles

The passenger vehicle segment currently holds the largest share of the electronic control system integrator market and is expected to continue its dominance in the forecast period. The increasing complexity of modern passenger cars, with advanced features like ADAS and infotainment systems, drives demand for highly specialized ECS integration. The rise of EVs further reinforces this dominance, as these vehicles are heavily reliant on complex ECS to manage battery, motor, and charging systems.

High volume of passenger car production: The sheer scale of passenger car manufacturing worldwide fuels the demand for ECS integration services.

Increased adoption of advanced features: Features like ADAS, infotainment systems, and connected car technologies necessitate comprehensive ECS integration.

Rising popularity of EVs: EVs necessitate sophisticated ECS integration far beyond what traditional ICE vehicles require, enhancing the demand within the passenger vehicle segment.

The third-party integrators segment is also expected to witness significant growth due to the increasing demand for specialized expertise and cost-effective solutions.

The electronic control system integrator industry's growth is propelled by several key factors. The rapid advancements in automotive technologies, particularly in areas like autonomous driving and electric vehicles, necessitate specialized integration services. Stringent government regulations worldwide pushing for reduced emissions and improved safety standards also create a significant need for sophisticated electronic control systems. Moreover, the growing consumer demand for enhanced vehicle features and improved fuel efficiency directly contributes to the market’s expansion.

This report provides a comprehensive analysis of the electronic control system integrator market, covering key trends, growth drivers, challenges, and leading players. It offers detailed insights into market segmentation, regional performance, and future growth prospects, providing valuable information for businesses operating in this dynamic sector. The report covers the historical period of 2019-2024, the base year of 2025, and forecasts up to 2033. This in-depth analysis helps stakeholders make informed business decisions and capitalize on emerging opportunities within the rapidly evolving landscape of electronic control system integration.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.2%.

Key companies in the market include BYD, HYUNDAI, Zhengzhou Yutong Bus, JMC, Zotye Automobile, Shanghai Edrive, Shanghai DAJUN Technologies, Jing-Jin Electric Technologies, Shenzhen Inovance Technology, INVT, .

The market segments include Application, Type.

The market size is estimated to be USD 29.1 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Electronic Control System Integrator," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Electronic Control System Integrator, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.