1. What is the projected Compound Annual Growth Rate (CAGR) of the Dual-Fuel Marine Engines?

The projected CAGR is approximately 23.5%.

Dual-Fuel Marine Engines

Dual-Fuel Marine EnginesDual-Fuel Marine Engines by Type (Four-Stroke Dual-Fuel Engines, Two-Stroke Dual-Fuel Engines, World Dual-Fuel Marine Engines Production ), by Application (Inland Vessel, Overseas Ship, World Dual-Fuel Marine Engines Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

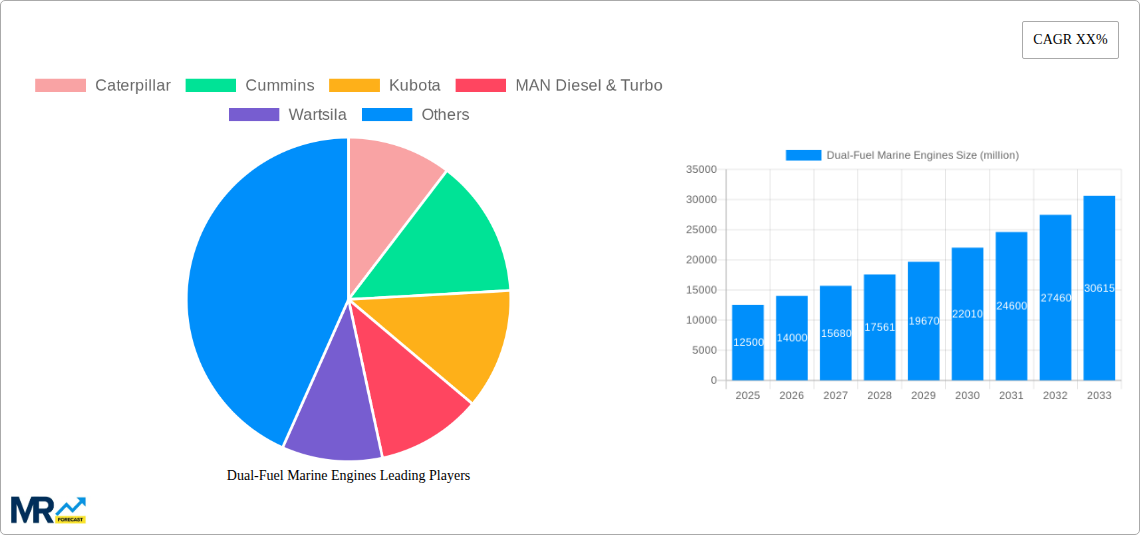

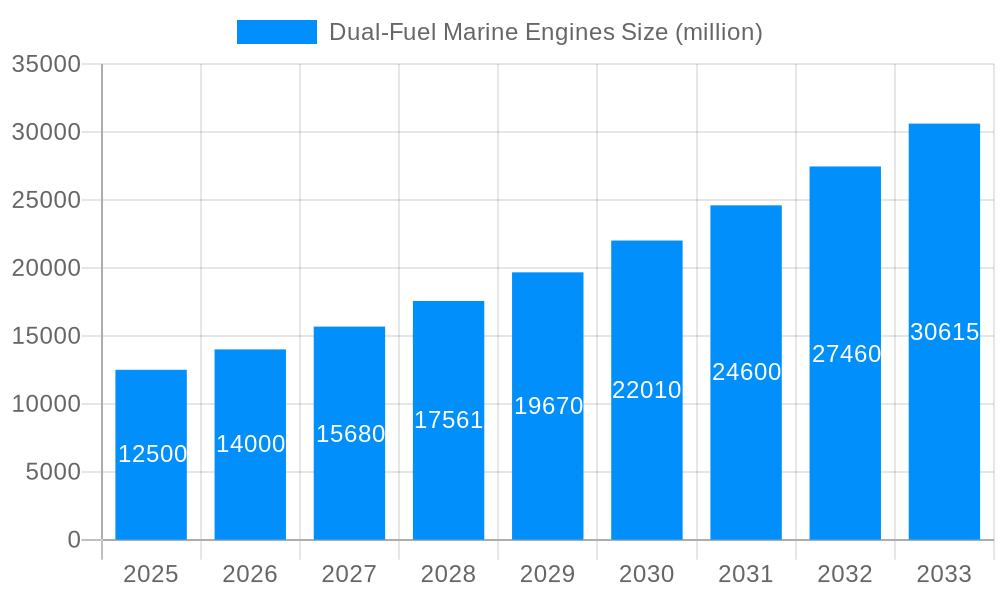

The global Dual-Fuel Marine Engines market is projected to achieve a size of $12,500 million by 2025, exhibiting a strong Compound Annual Growth Rate (CAGR) of 12%. This growth is propelled by increasingly stringent environmental regulations aimed at reducing maritime emissions, including sulfur oxides (SOx) and nitrogen oxides (NOx). The widespread adoption of cleaner fuels such as LNG, methanol, and ammonia as replacements for heavy fuel oil is a significant market driver. Moreover, the industry-wide push for decarbonization in maritime transport aligns with the inherent flexibility of dual-fuel engines, enabling the transition to future low-carbon and zero-carbon fuel options. The market is segmented into Four-Stroke and Two-Stroke Dual-Fuel Engines. Four-stroke engines are anticipated to lead due to their versatility across various vessel types and suitability for both inland and international shipping. The growing demand for retrofitting existing vessels and specifying dual-fuel engines for new builds will further accelerate market expansion.

Key industry players, including Wartsila, MAN Diesel & Turbo, and Caterpillar, are actively investing in research and development to enhance engine efficiency and broaden fuel compatibility, supporting the market's growth trajectory. Potential restraints include the initial capital investment for dual-fuel engine systems and the necessity for comprehensive bunkering infrastructure for alternative fuels. However, long-term operational cost savings and the imperative to comply with global environmental standards are expected to mitigate these challenges. The Asia Pacific region, notably China and Japan, is poised to lead in production and adoption, benefiting from substantial shipbuilding capabilities and a proactive approach to environmental regulations. Strategic investments in advanced engine technologies and evolving fuel standards will shape market competitiveness and foster innovation in the dual-fuel marine engine sector.

This report offers a detailed analysis of the Dual-Fuel Marine Engines market, including its size, growth prospects, and forecasts.

The global dual-fuel marine engines market is poised for substantial growth, driven by a confluence of stringent environmental regulations, evolving fuel landscapes, and a growing commitment to decarbonization within the maritime industry. The study period, spanning from 2019 to 2033, with a strong focus on the base and estimated year of 2025 and a forecast period from 2025 to 2033, indicates a trajectory of increasing adoption and innovation. During the historical period of 2019-2024, the market witnessed the initial stirrings of interest and early adoption, primarily in response to the International Maritime Organization's (IMO) emissions reduction targets. However, it is in the forecast period that the market is expected to truly mature. The demand for cleaner propulsion solutions, capable of running on both traditional marine fuels and alternative, lower-carbon fuels like LNG, methanol, and future ammonia, is becoming a non-negotiable aspect of new vessel construction and retrofitting projects. This trend is further amplified by rising fuel price volatility and the inherent operational flexibility offered by dual-fuel engines, allowing shipowners to adapt to changing fuel availability and cost dynamics. The estimated market size, projected to reach several million units, underscores the significant shift occurring in the marine propulsion sector. Key market insights reveal a growing preference for four-stroke dual-fuel engines in applications requiring higher speed and maneuverability, while two-stroke engines continue to dominate large, slow-moving vessels like container ships and tankers. The drive towards sustainability is not merely a regulatory push but a strategic imperative for the industry, with dual-fuel technology emerging as a crucial enabler for achieving significant reductions in SOx, NOx, and greenhouse gas emissions. The development of advanced fuel injection systems, robust engine control technologies, and improved gas handling systems are all contributing to the enhanced efficiency and reliability of these engines, making them an increasingly attractive investment for the maritime sector. The market is also witnessing a geographical shift, with Asia-Pacific emerging as a dominant force due to its extensive shipbuilding capabilities and increasing environmental awareness.

The propulsion of the dual-fuel marine engines market is a multifaceted phenomenon, predominantly fueled by the relentless pressure from international and regional environmental regulations aimed at curbing maritime emissions. The International Maritime Organization's (IMO) ambitious targets for reducing greenhouse gases (GHGs), sulfur oxides (SOx), and nitrogen oxides (NOx) have created an undeniable imperative for shipowners to transition towards cleaner propulsion technologies. Dual-fuel engines offer a pragmatic and immediate solution, enabling vessels to operate on liquefied natural gas (LNG), which significantly reduces SOx and NOx emissions, and provides a pathway towards lower-carbon operations. Furthermore, the increasing exploration and availability of alternative low-carbon fuels like methanol and, in the longer term, ammonia, position dual-fuel engines as a flexible and future-proof investment. The inherent operational flexibility afforded by these engines, allowing for seamless switching between fuels, provides shipowners with a critical advantage in navigating volatile fuel markets and ensuring compliance with evolving environmental standards. This adaptability reduces the risk associated with betting on a single future fuel and enhances the overall economic viability of vessel operations. The pursuit of enhanced operational efficiency and cost savings, especially in light of fluctuating fuel prices, also plays a significant role. By optimizing fuel consumption and offering the ability to utilize the most cost-effective fuel at any given time, dual-fuel engines contribute to the bottom line of shipping companies.

Despite the burgeoning growth, the dual-fuel marine engines market is not without its considerable challenges and restraints. A primary concern revolves around the infrastructure required for the widespread adoption of alternative fuels. The availability of bunkering facilities for LNG, methanol, and other low-carbon fuels remains limited in many key global shipping routes, creating significant operational hurdles for vessels relying on these fuels. This lack of comprehensive infrastructure necessitates careful route planning and can lead to extended transit times or limited operational flexibility. Another significant restraint is the higher initial capital expenditure associated with dual-fuel engines and the associated fuel storage systems compared to conventional diesel engines. While the long-term operational savings are often touted, the upfront investment can be a barrier for some shipowners, particularly smaller operators or those in capital-intensive segments. Safety considerations related to the handling and storage of alternative fuels, such as LNG, also present a challenge. While extensive safety protocols are in place, the perceived risks can lead to hesitancy among some stakeholders. Furthermore, the global regulatory landscape, while driving adoption, can also create uncertainty. The evolving nature of emissions standards and the emergence of new fuel technologies may require further upgrades or retrofits in the future, adding to the total cost of ownership. Finally, the availability of skilled personnel capable of operating and maintaining these advanced engines and their associated fuel systems is a growing concern that requires dedicated training programs and investment in human capital development.

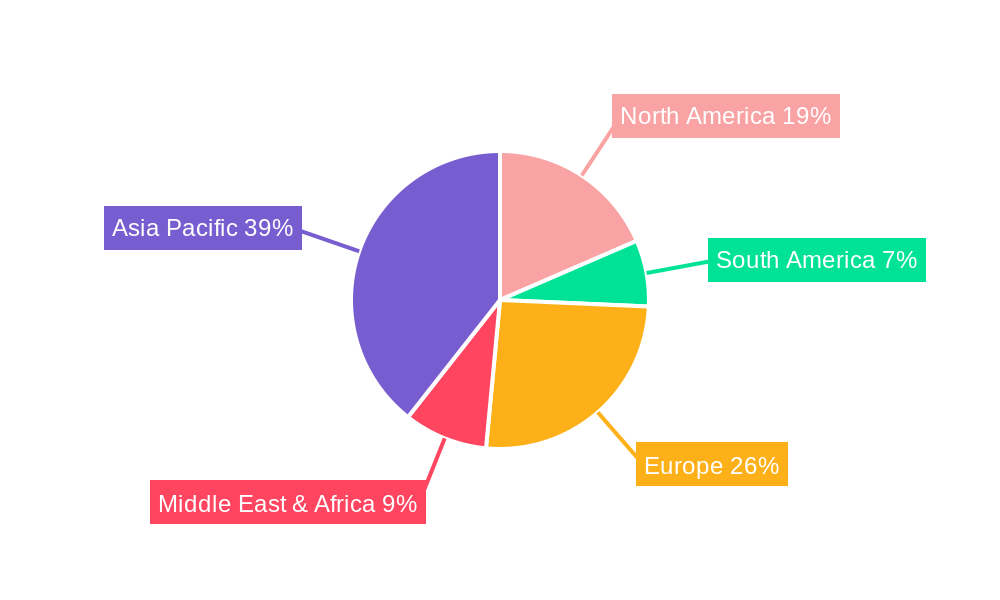

The global dual-fuel marine engines market is characterized by a dynamic interplay of regional strengths and segment dominance, with specific regions and engine types emerging as key drivers of growth.

Dominant Segments:

Four-Stroke Dual-Fuel Engines: This segment is poised for significant expansion, particularly in applications demanding higher speeds, greater maneuverability, and quicker response times.

Overseas Ship Application: The large-scale adoption of dual-fuel technology is most pronounced in the overseas shipping segment, driven by the need to comply with global emissions regulations and the availability of international fuel bunkering infrastructure.

Dominant Regions/Countries:

Asia-Pacific: This region is anticipated to be a powerhouse in the dual-fuel marine engines market, driven by its leading shipbuilding capabilities, substantial maritime trade, and a growing emphasis on environmental sustainability.

Europe: Europe is a key market for dual-fuel marine engines, particularly due to its stringent environmental regulations, proactive stance on decarbonization, and significant investments in alternative fuel infrastructure.

The dominance of these segments and regions is a testament to the evolving priorities of the global maritime industry, where environmental responsibility, operational efficiency, and future-proofing are paramount.

The growth catalysts for the dual-fuel marine engines industry are multifaceted, primarily driven by increasingly stringent global environmental regulations, notably from the IMO, pushing for drastic reductions in emissions. The growing availability and acceptance of lower-carbon fuels like LNG, methanol, and future options such as ammonia, provide a clear technological pathway. Furthermore, the economic advantages stemming from fuel flexibility, allowing operators to adapt to volatile fuel prices and secure long-term operational cost savings, act as a significant pull factor. Continuous advancements in engine technology, leading to improved efficiency and reliability, along with governmental incentives and subsidies for greener shipping solutions, further propel the industry forward.

This comprehensive report offers an in-depth analysis of the dual-fuel marine engines market, meticulously examining trends, drivers, and challenges from the historical period of 2019-2024 through the forecast period of 2025-2033, with a focus on the base and estimated year of 2025. It delves into the market dynamics, providing critical insights into the production, application, and technological advancements shaping the industry. The report highlights key regional and segment dominance, offering a granular view of where and how the market is evolving. Furthermore, it identifies the leading players and their strategic initiatives, alongside significant developments that are setting the pace for innovation. This report is designed to equip stakeholders with the essential information to navigate the complexities and capitalize on the opportunities within the rapidly transforming dual-fuel marine engines sector, projecting a substantial market valuation in the millions of units.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 23.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 23.5%.

Key companies in the market include Caterpillar, Cummins, Kubota, MAN Diesel & Turbo, Wartsila, ABC Diesel, Heinzmann, Hyundai, Rolls Royce, Westport, Woodward, Yanmar.

The market segments include Type, Application.

The market size is estimated to be USD 2447 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Dual-Fuel Marine Engines," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Dual-Fuel Marine Engines, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.