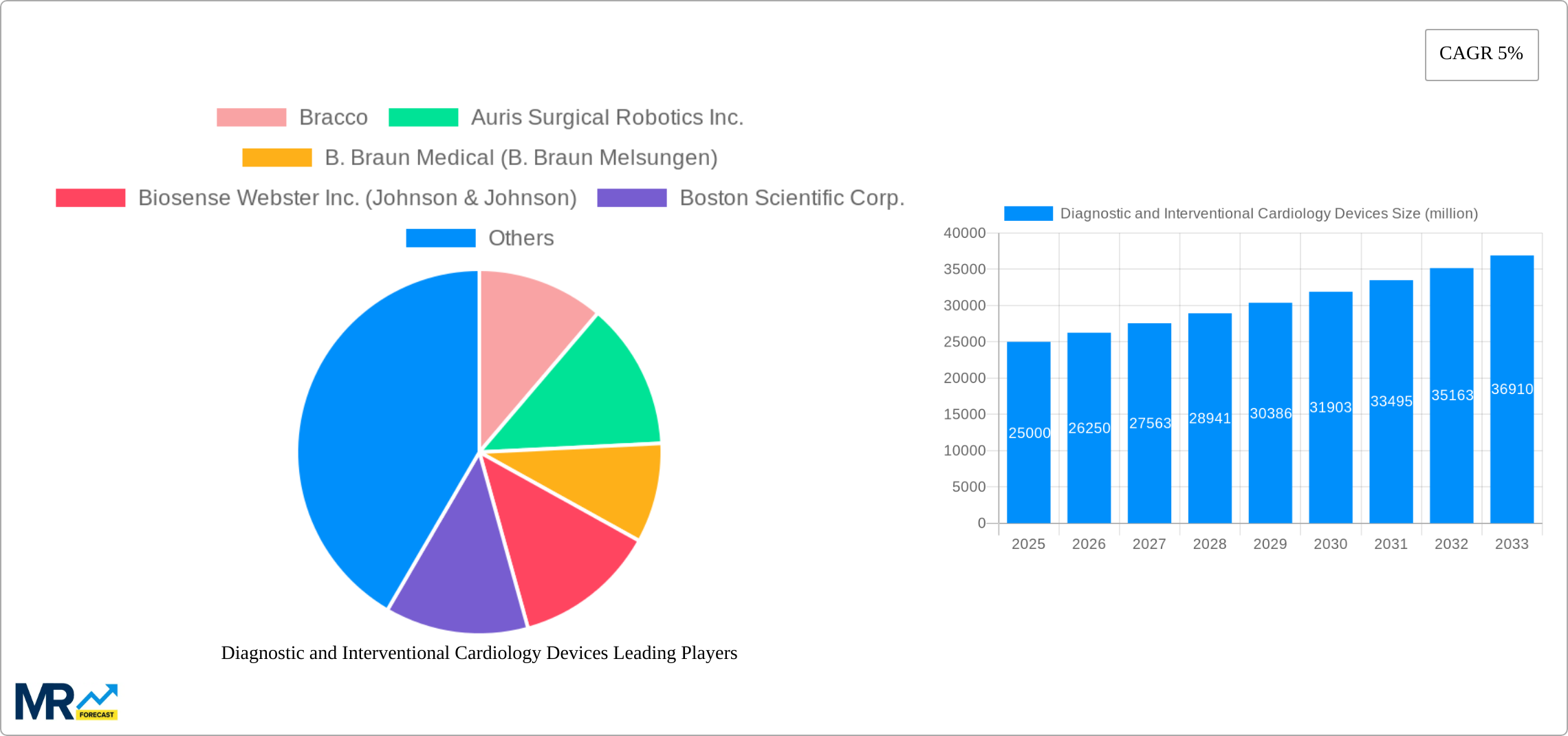

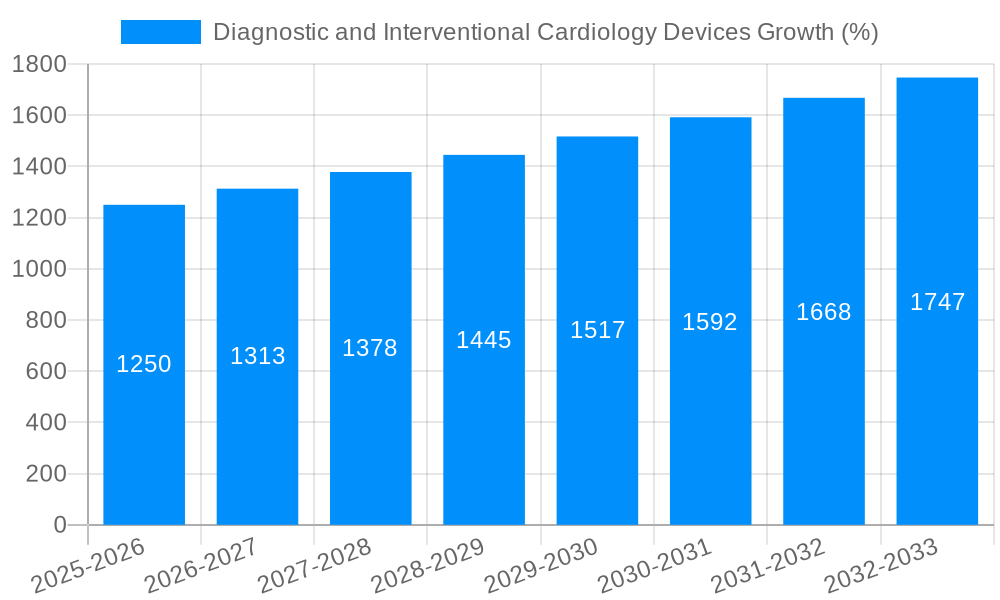

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diagnostic and Interventional Cardiology Devices?

The projected CAGR is approximately 5%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Diagnostic and Interventional Cardiology Devices

Diagnostic and Interventional Cardiology DevicesDiagnostic and Interventional Cardiology Devices by Type (Transcatheter Angiography Devices, Intravascular Ultrasound (IVUS) Devices, Guide Wire-Based Intravascular Stenosis Assessment Or Fractional Flow Reserve (FFR) Devices, Intracardiac Echocardiography (ICE) Devices, Optical Coherence Tomography (OCT) Devices, Robotic-Assisted Surgical Devices), by Application (Hospitals, Specialty Clinics), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global market for diagnostic and interventional cardiology devices is experiencing robust growth, driven by an aging population, rising prevalence of cardiovascular diseases, technological advancements, and increasing demand for minimally invasive procedures. The market, estimated at $X billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5% from 2025 to 2033, reaching a projected value of approximately $Y billion by 2033 (Note: X and Y represent estimated values derived from the provided 5% CAGR and a reasonable starting market size based on industry reports; specific numbers are not provided in the prompt). Key drivers include the increasing adoption of advanced imaging technologies like coronary CT angiography and cardiac MRI, the development of sophisticated catheters and stents with enhanced features, and the growing preference for robotic-assisted procedures that minimize trauma and improve patient outcomes. Technological innovations, such as the integration of artificial intelligence and machine learning for improved diagnostics and treatment planning, are further propelling market expansion.

However, market growth faces certain restraints. High costs associated with advanced devices, stringent regulatory approvals, and reimbursement challenges in various healthcare systems can limit accessibility and adoption rates, particularly in emerging markets. Furthermore, the market is characterized by intense competition among established players and emerging companies, requiring continuous innovation and strategic partnerships to maintain a competitive edge. Market segmentation reveals strong performance across various device categories, including coronary stents, cardiac catheters, pacemakers, implantable cardioverter-defibrillators (ICDs), and diagnostic imaging systems. Leading players like Medtronic, Boston Scientific, Abbott, and Johnson & Johnson are actively investing in research and development, strategic acquisitions, and geographic expansion to solidify their market positions and capture a greater share of this expanding market. Future growth will largely depend on continued technological advancements, regulatory approvals, and broader healthcare infrastructure developments globally.

The global diagnostic and interventional cardiology devices market is experiencing robust growth, driven by a confluence of factors including the rising prevalence of cardiovascular diseases, technological advancements, and an aging global population. The market, valued at several billion units in 2025, is projected to witness substantial expansion during the forecast period (2025-2033). Technological innovations, such as minimally invasive procedures and sophisticated imaging techniques, are significantly impacting the market landscape. The increasing adoption of robotic-assisted procedures and AI-powered diagnostic tools is streamlining workflows and improving patient outcomes. This trend is particularly noticeable in developed regions like North America and Europe, where advanced healthcare infrastructure and higher disposable incomes fuel demand. However, emerging economies in Asia-Pacific and Latin America are also exhibiting significant growth potential, driven by rising healthcare spending and increasing awareness about cardiovascular health. The market is characterized by intense competition among major players, who are constantly striving to innovate and develop cutting-edge devices. This competition fosters innovation and results in improved device efficacy, affordability, and accessibility. Over the historical period (2019-2024), the market experienced steady growth, setting the stage for even more substantial expansion during the forecast period. The market segmentation, encompassing various device types such as catheters, stents, pacemakers, and imaging systems, presents diverse opportunities for growth, with specific segments demonstrating faster growth rates than others based on factors like technological advancements and clinical adoption rates. Furthermore, strategic partnerships, mergers and acquisitions, and new product launches are contributing to the market's dynamic nature. The market's future trajectory hinges on sustained technological innovation, expanding healthcare infrastructure globally, and the continued focus on improving patient care and reducing healthcare costs. The projected growth signifies a significant opportunity for market participants to capitalize on the increasing demand for efficient and advanced cardiology solutions.

Several key factors are propelling the growth of the diagnostic and interventional cardiology devices market. The escalating global prevalence of cardiovascular diseases, including coronary artery disease, heart failure, and arrhythmias, is a primary driver. An aging global population, coupled with increasing risk factors like unhealthy lifestyles and obesity, is further exacerbating the problem. Technological advancements in minimally invasive procedures, such as transcatheter aortic valve replacement (TAVR) and percutaneous coronary intervention (PCI), are reducing the need for extensive open-heart surgeries, leading to faster recovery times and improved patient outcomes. The development of sophisticated imaging technologies, like advanced echocardiography and cardiac CT scans, enhances diagnostic accuracy and enables earlier detection of cardiovascular issues. The increasing adoption of robotic-assisted procedures and AI-powered diagnostic tools is streamlining workflows and improving precision, further boosting market growth. Furthermore, rising healthcare expenditure globally, particularly in emerging economies, is fueling the adoption of advanced cardiology devices. Government initiatives promoting preventive healthcare and increased awareness campaigns educating the public about cardiovascular health are also contributing to market expansion. Finally, the continuous efforts of leading players to innovate and launch cutting-edge devices keep the market dynamic and competitive.

Despite its strong growth trajectory, the diagnostic and interventional cardiology devices market faces certain challenges. High costs associated with advanced devices and procedures can pose a barrier to access, particularly in low- and middle-income countries. The stringent regulatory approvals and compliance requirements for new devices can prolong the time to market and increase development costs. Concerns regarding device complications and adverse events, although rare, can impact patient confidence and market adoption. The reimbursement policies and healthcare coverage variations across different regions can influence market penetration and affordability. Furthermore, the growing demand for cost-effective solutions and the pressure on healthcare systems to control expenses can put a strain on the market. The complexity of cardiovascular diseases and the need for specialized medical expertise further complicate the delivery of effective care. Competition among established players and the emergence of new entrants in the market can create pressure on pricing and profitability. Finally, the ethical considerations related to the use of advanced technologies in cardiology, such as AI-powered diagnosis, require careful consideration.

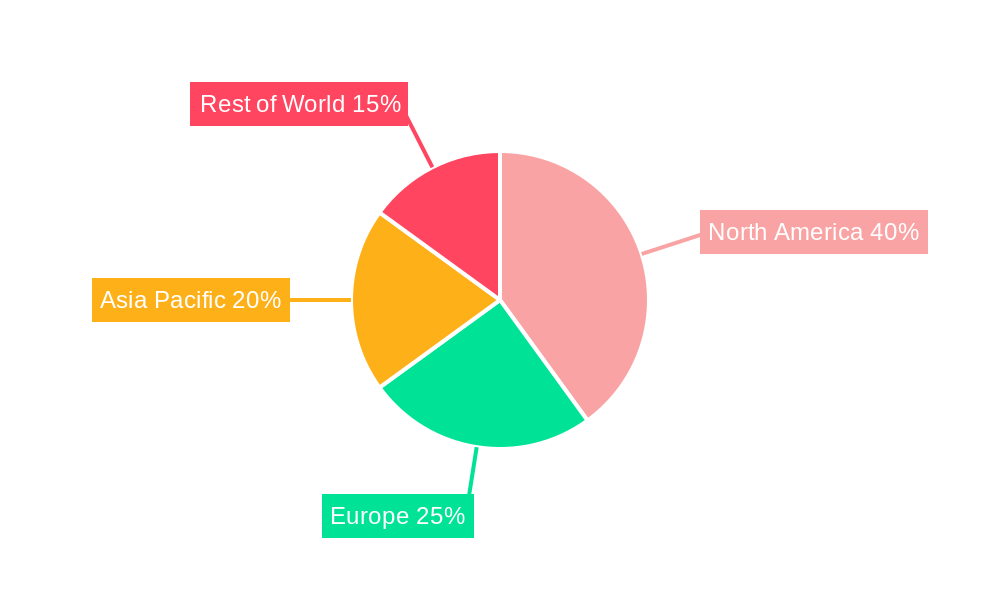

North America: This region is projected to maintain its dominance due to advanced healthcare infrastructure, high adoption rates of innovative technologies, and significant healthcare spending. The presence of major market players further contributes to its leadership.

Europe: Similar to North America, Europe is characterized by a strong healthcare infrastructure and a high level of technological adoption. However, variations in reimbursement policies across different countries may impact market growth differentially.

Asia-Pacific: This region shows exceptional growth potential, driven by the rapidly expanding aging population, increasing prevalence of cardiovascular diseases, and rising healthcare expenditure. However, some emerging economies might face challenges in infrastructural development and affordability.

Segments:

In summary, while North America and Europe are expected to retain their lead in terms of market size due to high per capita spending and established healthcare infrastructure, the Asia-Pacific region demonstrates the most promising potential for future expansion due to its growing elderly population and increasing affordability. Within the device segments, stents, catheters, and diagnostic imaging systems are poised for strong growth based on advancements in technology and demand.

Several factors are acting as growth catalysts for the diagnostic and interventional cardiology devices market. These include the rising prevalence of cardiovascular diseases worldwide, particularly in aging populations; continuous advancements in minimally invasive procedures and imaging technologies leading to better patient outcomes; increasing healthcare spending globally, making advanced technologies more accessible; growing adoption of telecardiology and remote patient monitoring, enhancing efficiency and access to care; and robust research and development activities leading to innovative devices and therapies. These factors collectively create a positive environment for significant market expansion in the coming years.

This report provides a comprehensive analysis of the diagnostic and interventional cardiology devices market, covering market size, growth trends, key drivers, challenges, and competitive landscape. It delves into detailed segmentation by device type and geographic region, offering valuable insights for market participants, investors, and healthcare professionals. The report includes a thorough analysis of the historical period (2019-2024), the base year (2025), the estimated year (2025), and a forecast for the period 2025-2033. By providing a holistic overview of the market, the report serves as an essential resource for understanding the current state and future trajectory of this vital sector within the healthcare industry.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5%.

Key companies in the market include Bracco, Auris Surgical Robotics Inc., B. Braun Medical (B. Braun Melsungen), Biosense Webster Inc. (Johnson & Johnson), Boston Scientific Corp., Catheter Precision, Cook Medical, Corindus Vascular Robotics Inc.(Siemens Healthcare), GE Healthcare, Hansen Medical Inc., Kaiser Permanente, Abbott Cardiovascular, C.R. Bard, Covidien, Edwards Lifescience, Johnson & Johnson, Medtronic, Plc Medical Systems, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Diagnostic and Interventional Cardiology Devices," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Diagnostic and Interventional Cardiology Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.