1. What is the projected Compound Annual Growth Rate (CAGR) of the Convertible Container Ship?

The projected CAGR is approximately 6.5%.

Convertible Container Ship

Convertible Container ShipConvertible Container Ship by Type (FCL Container Ship, LCL Container Ship, World Convertible Container Ship Production ), by Application (Commercial, Individual, World Convertible Container Ship Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

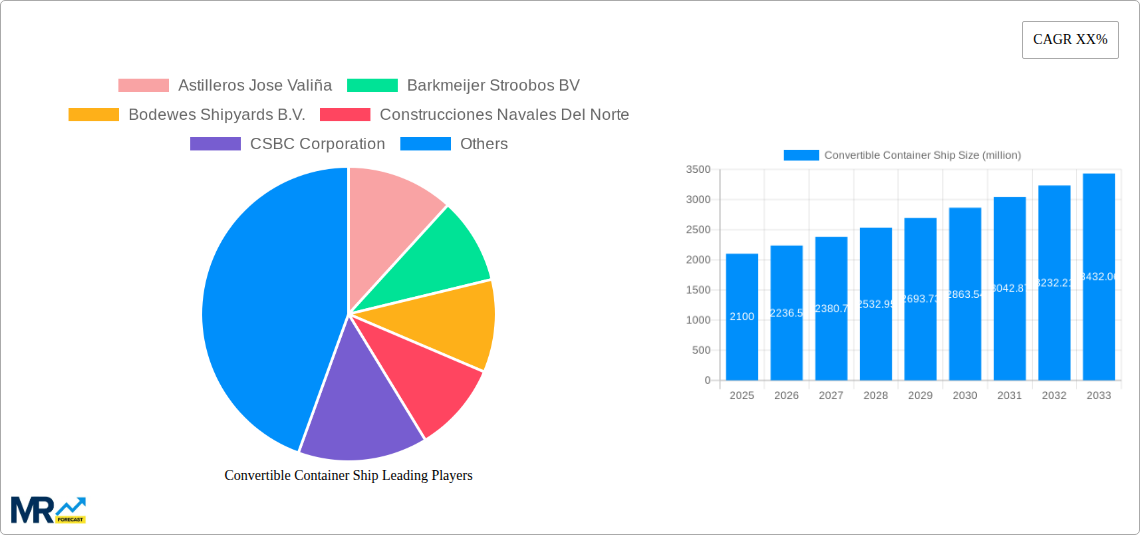

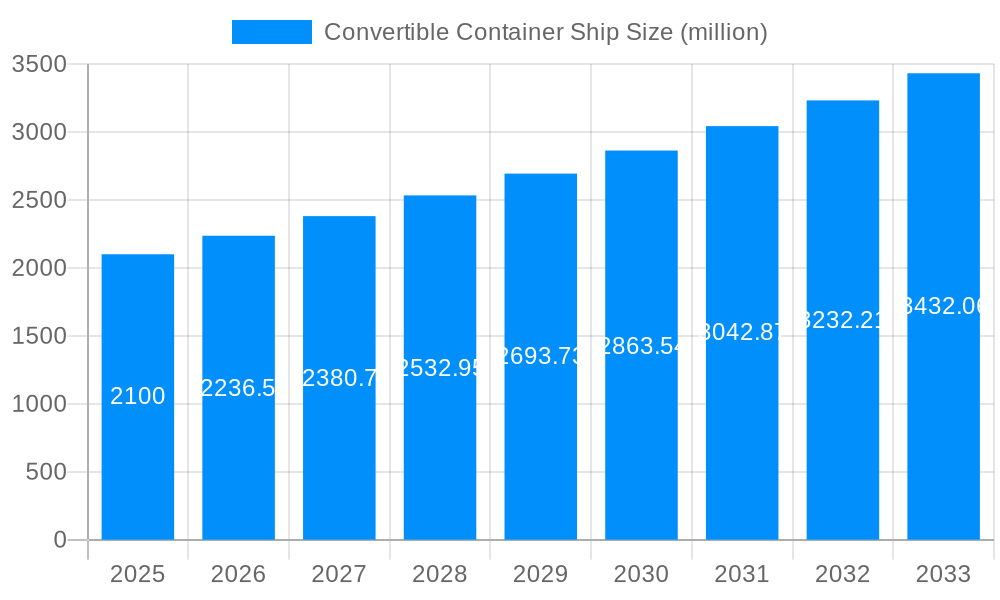

The global Convertible Container Ship market is poised for robust growth, projected to reach an estimated market size of $2.1 billion in 2025. This expansion is driven by a significant Compound Annual Growth Rate (CAGR) of 6.5% anticipated over the forecast period of 2025-2033. This upward trajectory is fueled by increasing global trade volumes, the ever-growing demand for efficient and flexible cargo transportation solutions, and advancements in shipbuilding technology. The versatility of convertible container ships, allowing for adaptability to various cargo types and shipping needs, makes them increasingly attractive to both commercial operators and individual stakeholders seeking optimized logistics. Key drivers include the need for enhanced intermodal connectivity, the growing complexity of global supply chains, and the continuous innovation in shipbuilding materials and design, leading to more fuel-efficient and environmentally friendly vessels.

The market is segmented into FCL (Full Container Load) Container Ships, LCL (Less than Container Load) Container Ships, and World Convertible Container Ship Production, catering to diverse application needs such as commercial and individual use. Geographically, the Asia Pacific region is expected to dominate the market share due to its status as a global manufacturing hub and a significant driver of international trade. North America and Europe are also projected to exhibit steady growth, supported by investments in port infrastructure and the adoption of advanced shipping technologies. While the market enjoys strong growth potential, potential restraints include the high initial capital investment required for shipbuilding, stringent environmental regulations that necessitate continuous technological upgrades, and the cyclical nature of the shipping industry, which can be influenced by global economic fluctuations. However, the overarching trend towards greater efficiency, sustainability, and flexibility in maritime logistics strongly favors the continued expansion of the convertible container ship market.

The global Convertible Container Ship market is poised for substantial expansion, driven by a confluence of evolving maritime logistics needs and technological advancements. Our comprehensive report, spanning the Study Period of 2019-2033, with a Base Year and Estimated Year of 2025, and a Forecast Period of 2025-2033, meticulously analyzes the market's trajectory. During the Historical Period of 2019-2024, we observed nascent adoption patterns and early technological integrations. Now, entering the forecast period, the market is anticipated to witness significant growth, with projections indicating a valuation well into the billions of dollars. This upward trend is fueled by the inherent flexibility of convertible container ships, which can seamlessly adapt to carrying either Full Container Load (FCL) or Less than Container Load (LCL) cargo, thereby optimizing vessel utilization and revenue generation.

The increasing complexity of global supply chains and the demand for more adaptable shipping solutions are primary drivers. Traditional container ships often face underutilization when cargo volumes fluctuate. Convertible container ships, however, offer a revolutionary solution by allowing operators to switch between configurations, maximizing cargo capacity and efficiency. This adaptability is particularly crucial for shipping lines serving diverse trade routes with varying cargo mixes and volumes. The market is segmented by ship type, encompassing FCL Container Ships and LCL Container Ships, as well as the broader category of World Convertible Container Ship Production. In terms of application, the market is primarily driven by Commercial use, with Individual applications remaining niche but potentially emerging. The World Convertible Container Ship Production segment itself is a critical indicator of the industry's overall health and future potential. Key market insights reveal a growing appetite for these versatile vessels, especially in regions with dynamic trade patterns. The report delves into the nuances of this evolving landscape, providing granular data on market size, share, and forecasts, ensuring stakeholders are equipped with the insights needed to navigate this promising sector. The projected market value, reaching tens of billions of dollars in the coming years, underscores the transformative potential of convertible container ships in the global maritime industry.

The surge in demand for convertible container ships is a direct response to the dynamic and often unpredictable nature of global trade. The inherent limitations of fixed-configuration vessels in a fluctuating cargo market have become increasingly apparent. Convertible container ships, with their ability to seamlessly transition between different cargo configurations—optimized for either FCL Container Ship or LCL Container Ship operations—offer unparalleled operational flexibility. This adaptability translates directly into improved vessel utilization rates, which is a critical metric for profitability in the shipping industry. As supply chains become more intricate and the need for cost-efficiency paramount, shipping companies are actively seeking solutions that can mitigate the financial impact of underutilized capacity. The prospect of maximizing returns on investment by adapting to varying cargo demands, whether it’s a large shipment of identical containers (FCL) or a mixed consignment of smaller shipments (LCL), is a powerful incentive. This operational agility not only enhances revenue potential but also contributes to more sustainable shipping practices by reducing empty sailings and optimizing resource allocation. The market is poised to reach multi-billion dollar valuations due to these compelling operational and economic advantages.

Furthermore, advancements in shipbuilding technology and naval architecture are making these versatile vessels more economically viable and technically feasible. The ability to reconfigure cargo holds and deck space efficiently, often through modular designs and advanced mechanical systems, is a testament to the innovation within the industry. The World Convertible Container Ship Production segment reflects this growing interest and investment in innovative vessel designs. As more shipyards, including prominent players like HYUNDAI HEAVY INDUSTRIES, SAMSUNG HEAVY INDUSTRIES, and MITSUBISHI HEAVY INDUSTRIES, invest in the research and development of these adaptable platforms, the availability and efficiency of convertible container ships are set to increase, further propelling their adoption across the global maritime trade routes. The economic incentives, coupled with technological progress, are creating a strong tailwind for this segment.

Despite the promising outlook, the widespread adoption of convertible container ships is not without its hurdles. One of the primary challenges revolves around the initial capital investment required for these specialized vessels. The advanced engineering and flexible design features that enable cargo conversion often translate to higher construction costs compared to conventional container ships. This can be a significant deterrent for some operators, particularly smaller shipping companies with limited financial resources. The World Convertible Container Ship Production segment, while growing, is still relatively nascent, meaning economies of scale in manufacturing have yet to be fully realized, contributing to these elevated costs. The projected market value, reaching into the billions of dollars, is tempered by this initial expenditure.

Another significant restraint lies in the complexity of the conversion mechanisms themselves. While designed for efficiency, these systems require rigorous maintenance and operational expertise. Any downtime or malfunction in the conversion machinery can lead to significant logistical disruptions and financial losses. Furthermore, the standardization of convertible container ship designs and operational protocols is still in its early stages. This lack of standardization can create interoperability issues and complicate port operations, which are often optimized for conventional container handling. The integration of these vessels into existing port infrastructure and global logistics networks requires careful planning and potentially further investment in port facilities. The regulatory landscape surrounding these innovative vessels is also an evolving area, and clear international guidelines are essential to foster confidence and encourage broader adoption. Overcoming these challenges will be critical for the market to achieve its full multi-billion dollar potential.

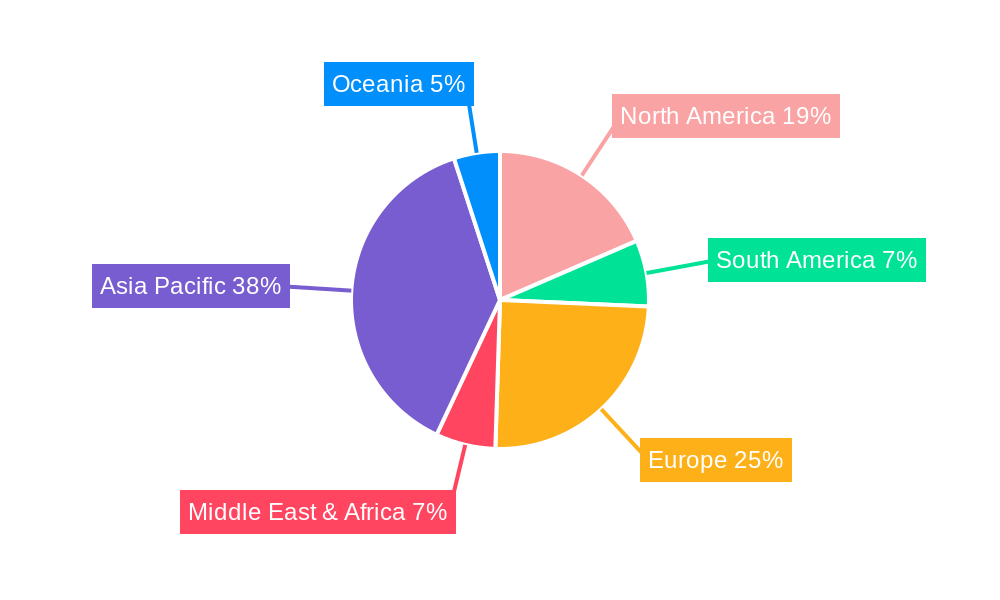

The global convertible container ship market is poised for dominance by key regions and specific segments that are strategically positioned to leverage the advantages of this innovative vessel type. Asia-Pacific, particularly East Asian nations with robust shipbuilding capabilities and significant global trade volumes, is expected to emerge as a frontrunner. Countries like South Korea, home to shipbuilding giants such as HYUNDAI HEAVY INDUSTRIES, SAMSUNG HEAVY INDUSTRIES, and DAEWOO SHIPBUILDING, alongside China with its massive shipbuilding capacity including CSBC Corporation and HANJIN HEAVY INDUSTRIES AND CONSTRUCTION, are not only leading in the production of these vessels but also in their deployment. Their extensive port networks, deep-sea trade routes, and high demand for efficient cargo handling solutions make them natural hubs for convertible container ship operations.

Within the segments, World Convertible Container Ship Production itself is a key indicator of regional strength and market dominance. Regions that possess advanced shipbuilding technologies, a skilled workforce, and significant investment capacity are best placed to lead this production. This includes the aforementioned Asian powerhouses, as well as European shipbuilding nations with established expertise, such as Spain (e.g., Astilleros Jose Valiña, Construcciones Navales Del Norte, Hijos de J. Barreras) and the Netherlands (e.g., Barkmeijer Stroobos BV, Bodewes Shipyards B.V.). These regions are likely to see substantial growth in the manufacturing and export of convertible container ships, contributing significantly to the global market value, which is projected to reach tens of billions of dollars.

The Commercial Application segment is expected to be the primary driver of market growth. The inherent economic benefits of flexible cargo handling—optimizing for either FCL Container Ship or LCL Container Ship loads—are most acutely felt in large-scale commercial shipping operations. Major shipping lines operating on transoceanic routes, those servicing diverse regional markets, and those involved in chartering operations will be the early and most significant adopters. The ability to dynamically adjust capacity based on market demand, thereby maximizing revenue and minimizing costs, is a compelling proposition for commercial entities. This focus on commercial viability will ensure that the World Convertible Container Ship Production in these dominant regions is geared towards meeting the needs of the global trade ecosystem.

Furthermore, the demand for these versatile vessels in emerging markets undergoing rapid economic expansion and trade liberalization will also contribute to regional dominance. As these economies integrate further into the global supply chain, the need for efficient and adaptable shipping solutions will grow, creating new opportunities for both production and deployment in regions like Southeast Asia and parts of Latin America. The interplay between strong shipbuilding infrastructure, significant trade volumes, and the adoption of advanced shipping technologies will solidify the dominance of these key regions and the commercial application segment in shaping the future of the convertible container ship market.

The convertible container ship industry is experiencing a potent surge of growth catalysts, primarily driven by the escalating demand for operational efficiency and supply chain resilience. The inherent flexibility of these vessels, allowing seamless transition between FCL Container Ship and LCL Container Ship configurations, directly addresses the inefficiencies of fixed-capacity ships in volatile trade environments. This adaptability optimizes vessel utilization, a critical factor for profitability, pushing the market towards significant billions of dollar valuations. Technological advancements in modular design and automated conversion systems are also making these ships more cost-effective and easier to operate, further accelerating adoption.

This report provides an exhaustive analysis of the convertible container ship market, offering a deep dive into trends, drivers, and restraints throughout the Study Period of 2019-2033. With a Base Year and Estimated Year of 2025, and a Forecast Period of 2025-2033, it meticulously details the market's evolution from its Historical Period of 2019-2024. The report highlights key insights into World Convertible Container Ship Production, exploring its trajectory towards multi-billion dollar valuations. It meticulously examines how segments like FCL Container Ship and LCL Container Ship, driven by Commercial Application, are shaping market dynamics. Stakeholders will gain unparalleled insights into growth catalysts, challenges, dominant regions, and leading players, enabling informed strategic decision-making in this rapidly advancing maritime sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.5%.

Key companies in the market include Astilleros Jose Valiña, Barkmeijer Stroobos BV, Bodewes Shipyards B.V., Construcciones Navales Del Norte, CSBC Corporation, DAE SUN SHIPBUILDING, DAEWOO SHIPBUILDING, General Dynamics NASSCO, HANJIN HEAVY INDUSTRIES AND CONSTRUCTION, Hijos de J. Barreras, HYUNDAI HEAVY INDUSTRIES, HYUNDAI MIPO DOCKYARD, Imabari Shipbuilding, MITSUBISHI HEAVY INDUSTRIES, Namura Shipbuilding, Nuovi Cantieri Apuania, Remontowa, SAMSUNG HEAVY INDUSTRIES, SembCorp Marine, STX SHIPBUILDING, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Convertible Container Ship," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Convertible Container Ship, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.