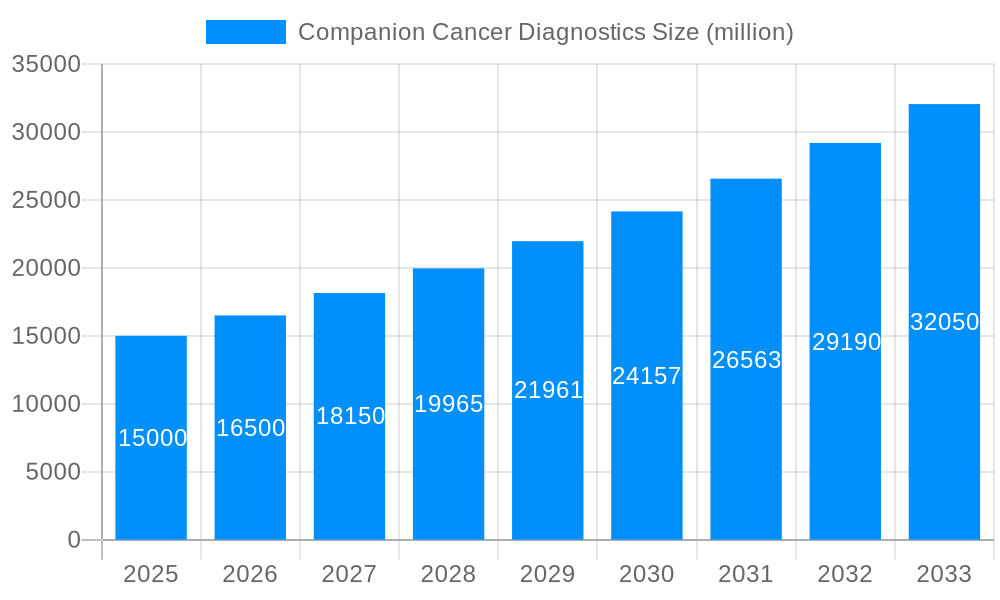

1. What is the projected Compound Annual Growth Rate (CAGR) of the Companion Cancer Diagnostics?

The projected CAGR is approximately 11.5%.

Companion Cancer Diagnostics

Companion Cancer DiagnosticsCompanion Cancer Diagnostics by Type (/> Breast Cancer, Lung Cancer, Colorectal Cancer, Melanoma, Gastric Cancer), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The companion cancer diagnostics market is experiencing robust growth, driven by the increasing prevalence of cancer globally, advancements in personalized medicine, and the rising demand for accurate and targeted cancer therapies. The market, segmented by cancer type (breast, lung, colorectal, melanoma, gastric), shows significant potential across all areas, with breast and lung cancer diagnostics currently holding the largest market share due to higher incidence rates and extensive research in these areas. Technological advancements, such as next-generation sequencing (NGS) and liquid biopsies, are revolutionizing diagnostics, enabling earlier and more precise detection, prognosis, and treatment selection. This leads to improved patient outcomes and reduced healthcare costs in the long run. The market is further propelled by favorable regulatory landscapes in key regions, including North America and Europe, which are fostering innovation and adoption of new diagnostic technologies.

However, high costs associated with advanced diagnostic tests, stringent regulatory approvals, and the need for skilled professionals to interpret complex results pose challenges to market expansion. Nevertheless, the increasing investment in R&D, collaborations between diagnostic companies and pharmaceutical firms, and the growing awareness among healthcare professionals and patients about the benefits of personalized medicine are expected to overcome these restraints. The market's future growth trajectory indicates a continued upward trend, particularly in emerging economies where healthcare infrastructure is rapidly improving and access to advanced diagnostic technologies is increasing. Regional variations in market share are expected, with North America maintaining a dominant position due to its advanced healthcare infrastructure and high adoption rates, while Asia-Pacific is anticipated to witness rapid growth in the coming years driven by rising disposable incomes and increasing healthcare spending.

The global companion cancer diagnostics market is experiencing robust growth, driven by the increasing prevalence of cancer, advancements in targeted therapies, and a rising demand for personalized medicine. The market, estimated at $XX billion in 2025, is projected to reach $YY billion by 2033, exhibiting a significant Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033). This growth is fueled by several key factors, including the increasing adoption of next-generation sequencing (NGS) technologies for comprehensive genomic profiling, the development of more accurate and sensitive diagnostic tests, and the rising investment in research and development within the companion diagnostics sector. The historical period (2019-2024) witnessed a steady growth trajectory, laying the foundation for the accelerated expansion predicted in the forecast period. Key market insights indicate a strong preference for tests providing actionable information that directly influences treatment decisions. This is leading to a shift towards multi-gene panels and comprehensive assays, rather than single-gene tests, reflecting the complex and heterogeneous nature of cancer. Furthermore, the integration of companion diagnostics into routine clinical pathways is gaining momentum, ensuring better patient outcomes and improved healthcare efficiency. The increasing regulatory approvals for novel companion diagnostic tests are also contributing to market expansion, streamlining the process for patients and healthcare professionals. The market’s growth is not uniform across all cancer types; certain cancers, due to their prevalence and the availability of targeted therapies, are driving disproportionately higher demand for companion diagnostics. This trend is likely to continue as research continues to unveil more targeted treatment options for various cancers.

Several factors are propelling the growth of the companion cancer diagnostics market. Firstly, the rising prevalence of cancer globally is a major driver. With increasing incidences of various cancer types, the need for accurate and timely diagnosis and treatment selection has intensified. Secondly, the remarkable advancements in targeted therapies are intrinsically linked to the growth of companion diagnostics. These therapies are highly effective against specific genetic mutations, necessitating accurate identification of these mutations through companion diagnostic tests. This personalized approach to cancer treatment has become a cornerstone of modern oncology, directly impacting the demand for companion diagnostics. Thirdly, the increasing emphasis on personalized medicine is transforming healthcare practices. Tailoring treatments to individual patients based on their unique genetic profiles enhances treatment efficacy and minimizes adverse effects. Companion diagnostics play a crucial role in achieving this personalized approach, driving its adoption. Fourthly, technological advancements in molecular diagnostics, particularly NGS and PCR technologies, have significantly improved the accuracy, speed, and affordability of companion diagnostic tests. This has broadened access to these tests, fueling market growth. Finally, increased regulatory support and reimbursement policies are creating a favorable environment for the development and adoption of companion diagnostics. This is ensuring that these crucial tools are readily available to healthcare providers and patients.

Despite its significant growth potential, the companion cancer diagnostics market faces several challenges. High costs associated with developing and implementing advanced diagnostic technologies, such as NGS, can limit accessibility, especially in resource-constrained settings. The complexity of interpreting genomic data and the need for specialized expertise to analyze and interpret results also pose a barrier. Ensuring accurate and consistent testing across different laboratories and platforms presents another challenge. Standardization and harmonization of testing procedures are crucial to guarantee reliable results and enable meaningful comparisons. Moreover, the evolving landscape of regulatory approvals and reimbursement policies can create uncertainty for companies investing in companion diagnostics. Navigating the regulatory processes in different regions can be complex and time-consuming. Furthermore, the limited availability of trained personnel to perform and interpret complex companion diagnostic tests, especially in developing countries, presents a critical hurdle. Finally, the frequent emergence of new cancer-related biomarkers necessitates constant updates to diagnostic tests, requiring continuous investment in research and development to maintain efficacy and relevance.

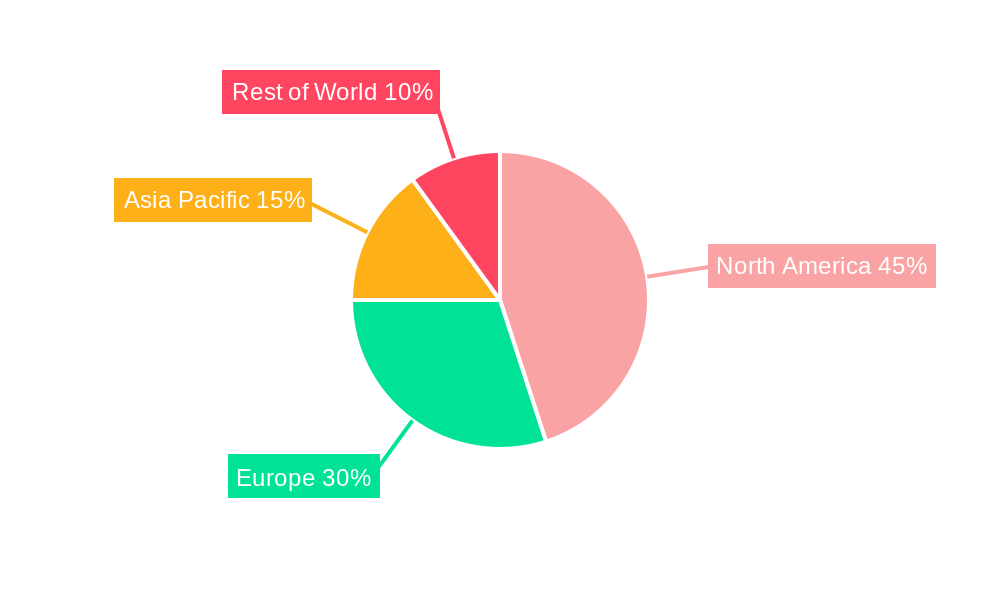

North America: This region is expected to hold a significant market share due to the high prevalence of cancer, advanced healthcare infrastructure, strong regulatory support, and high adoption of personalized medicine. The presence of major players in the diagnostics industry further strengthens the region’s dominance.

Europe: Significant investments in research and development, along with well-established healthcare systems, will contribute to the growth of the European market. However, stringent regulatory procedures may slightly hinder rapid market expansion compared to North America.

Asia-Pacific: Rapidly rising cancer incidence, a growing middle class with increased healthcare expenditure, and increasing awareness of advanced diagnostic tools are driving market growth in this region. However, limitations in healthcare infrastructure and regulatory frameworks in certain countries may pose challenges.

Dominant Cancer Segments:

Breast Cancer: This segment is projected to lead the market due to its high prevalence, the availability of several targeted therapies, and the extensive research focused on identifying relevant biomarkers. The continuous development of companion diagnostics for breast cancer further fuels market expansion in this area.

Lung Cancer: Lung cancer's high mortality rate and the emergence of targeted therapies for specific mutations create a substantial demand for companion diagnostics. This segment's growth is closely tied to the continued innovation in lung cancer treatment strategies.

Colorectal Cancer: Early detection and the availability of tailored therapies based on biomarker identification position colorectal cancer as a significant segment within the companion diagnostics market. Growing awareness and improved screening programs are also contributing to its growth.

The paragraph above points to the combined strengths of North America's advanced healthcare infrastructure and market access with the high prevalence and treatment-specific needs of Breast and Lung cancers as major factors contributing to market dominance. Other segments will experience notable growth, but the sheer size and advanced nature of these markets are expected to maintain their leadership in the foreseeable future. Geographical variations will occur, with Asia-Pacific showing rapid growth but possibly lagging behind in certain areas due to infrastructural or regulatory reasons.

Several factors are accelerating the growth of the companion cancer diagnostics industry. The increasing adoption of personalized medicine strategies, driven by the success of targeted therapies, is a primary growth catalyst. This approach ensures that treatments are precisely tailored to patients' genetic profiles, maximizing efficacy and minimizing adverse effects. Moreover, continuous advancements in molecular diagnostic technologies, such as NGS, are improving the accuracy, speed, and cost-effectiveness of companion diagnostic tests, thus expanding their accessibility. Growing regulatory support and the increasing reimbursement of companion diagnostic tests are further enhancing their adoption within healthcare systems. These catalysts collectively promote the widespread integration of companion diagnostics into clinical practice, leading to improved patient outcomes and a more efficient healthcare system.

This report offers a comprehensive analysis of the companion cancer diagnostics market, encompassing detailed market sizing, segmentation, trend analysis, and future projections. It provides in-depth insights into the key drivers and challenges impacting the market and identifies leading players and their strategic initiatives. The report also presents a thorough examination of the regulatory landscape and reimbursement policies that shape the industry's development. The information presented helps to understand the ongoing transformations, future projections, and the competitive dynamics within the companion cancer diagnostics sector, facilitating informed decision-making for stakeholders in the field.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.5%.

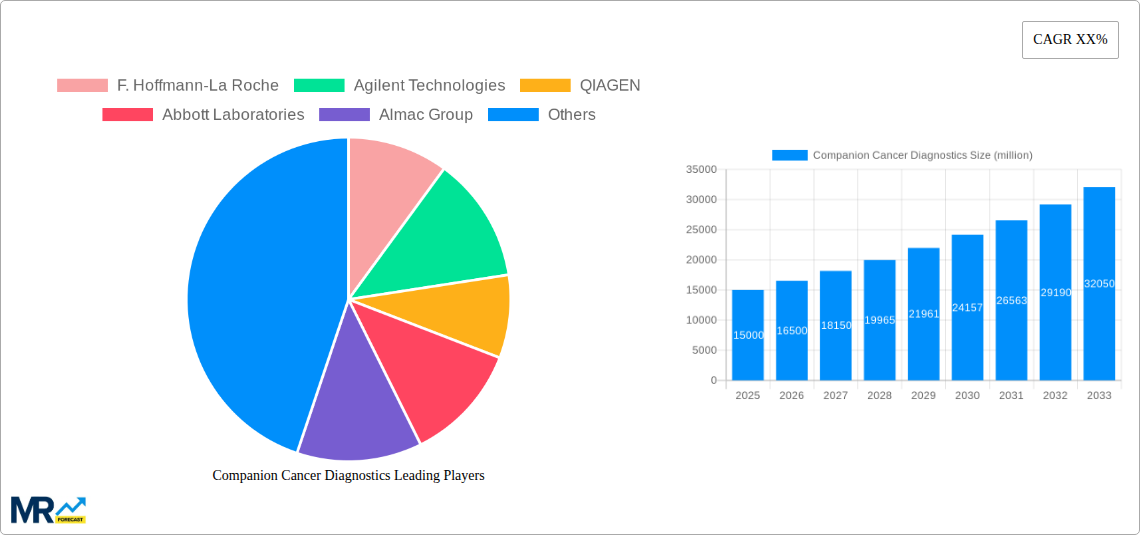

Key companies in the market include F. Hoffmann-La Roche, Agilent Technologies, QIAGEN, Abbott Laboratories, Almac Group, Danaher Corporation, bioMérieuxSA, Myriad Genetics, .

The market segments include Type.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Companion Cancer Diagnostics," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Companion Cancer Diagnostics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.