1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Liquid Cooling Equipment?

The projected CAGR is approximately XX%.

Commercial Liquid Cooling Equipment

Commercial Liquid Cooling EquipmentCommercial Liquid Cooling Equipment by Type (Cold Plate, Immersion, Spray), by Application (Industrial, Electronics, Communication, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The commercial liquid cooling equipment market is experiencing robust growth, driven by the increasing demand for high-performance computing (HPC) and data centers. The escalating heat generated by advanced processors and servers necessitates efficient cooling solutions, making liquid cooling a compelling alternative to traditional air cooling methods. This technology offers superior heat dissipation capabilities, enabling higher power densities and improved energy efficiency. Market expansion is further fueled by the adoption of edge computing, which necessitates localized cooling solutions, and the growing awareness of sustainability concerns within data centers. While the initial investment for liquid cooling systems might be higher, the long-term operational cost savings and improved system reliability offer a significant return on investment. Competition is fierce, with established players like Schneider Electric, Vertiv, and Rittal vying for market share alongside emerging innovative companies focused on next-generation liquid cooling technologies. Regional growth is expected to vary, with North America and Europe leading initially, followed by strong growth in Asia-Pacific, driven primarily by the expansion of data centers in China and other rapidly developing economies. The market is segmented by cooling method (direct-to-chip, immersion, cold plates), application (data centers, HPC, servers), and component type (pumps, chillers, heat exchangers). Challenges include the relatively higher upfront cost compared to air cooling and the complexity of implementation and maintenance. However, ongoing technological advancements and economies of scale are expected to mitigate these challenges over the forecast period (2025-2033).

The forecast period reveals continued market expansion, with a projected Compound Annual Growth Rate (CAGR) allowing for estimation of future market size based on the 2025 value. We anticipate a steady increase in demand across all major segments, fueled by the ongoing digital transformation and the need for more powerful and energy-efficient data center infrastructure. Strategic partnerships between cooling equipment manufacturers and data center operators are likely to further accelerate adoption. Further market segmentation analysis focusing on specific geographic regions and cooling methods will provide a clearer picture of emerging trends and opportunities. Focus on sustainable manufacturing practices and environmentally friendly refrigerants will also play a pivotal role in shaping the market’s future trajectory. The competitive landscape will continue to evolve, with both mergers and acquisitions and the entry of new players shaping the dynamics of the market.

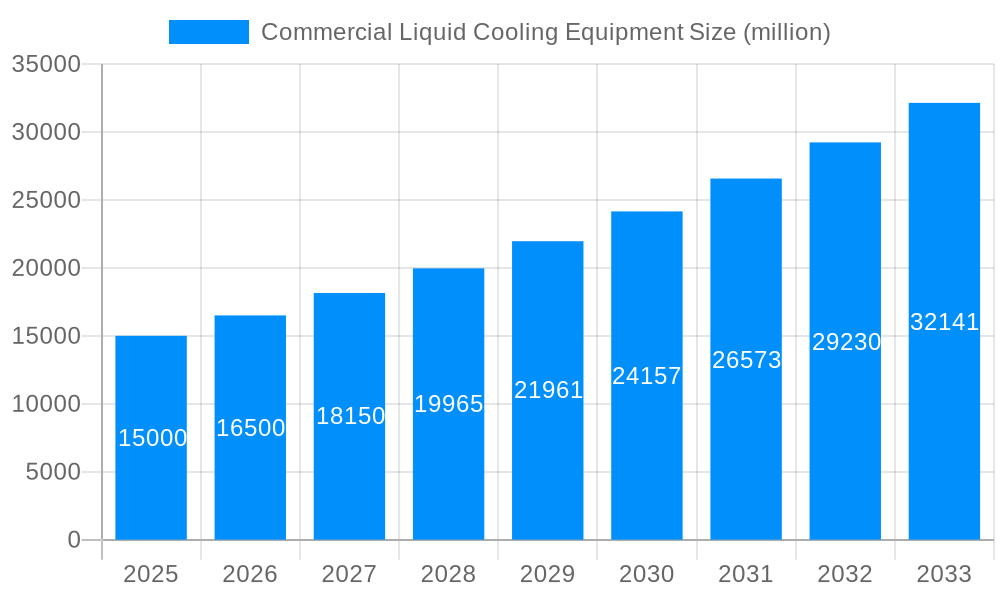

The commercial liquid cooling equipment market is experiencing explosive growth, projected to reach multi-billion dollar valuations by 2033. Driven by the increasing heat density of data centers and the escalating demand for energy-efficient cooling solutions, this sector shows remarkable promise. Over the historical period (2019-2024), the market witnessed a steady climb, with the estimated year (2025) marking a significant inflection point. The forecast period (2025-2033) anticipates a compound annual growth rate (CAGR) exceeding X%, fueled by several factors, including the burgeoning adoption of high-performance computing (HPC) and the expanding deployment of 5G networks. This heightened demand translates into a significant increase in the deployment of liquid cooling systems across various sectors, including data centers, telecommunications infrastructure, and industrial applications. Key market insights reveal a strong preference for direct-to-chip liquid cooling solutions, demonstrating a shift away from traditional air cooling methods. This trend is particularly pronounced in hyperscale data centers and high-performance computing environments where maximizing performance and minimizing energy consumption are paramount. Furthermore, the increasing integration of AI and machine learning in liquid cooling systems promises more efficient and predictive operational capabilities, further boosting market growth. The market is also witnessing the emergence of innovative cooling technologies, such as immersion cooling and two-phase cooling, which offer enhanced cooling performance and reduced energy costs compared to traditional methods. This innovation coupled with growing environmental concerns is accelerating the adoption of liquid cooling solutions as a sustainable alternative to traditional air cooling technologies. The market is becoming increasingly competitive, with both established players and new entrants vying for market share, driving innovation and price competitiveness.

Several factors are synergistically propelling the growth of the commercial liquid cooling equipment market. The relentless increase in data center density, driven by the exponential growth of data and the rising adoption of cloud computing, necessitates highly efficient cooling solutions. Traditional air cooling systems struggle to manage the heat generated by high-density servers, leading to decreased performance, increased energy consumption, and higher operational costs. Liquid cooling offers a superior alternative, providing significantly improved heat dissipation and allowing for higher server densities within a given space. Furthermore, the growing focus on energy efficiency and sustainability is another major driving force. Liquid cooling systems, when compared to air cooling, significantly reduce energy consumption, resulting in substantial cost savings and a smaller carbon footprint. This aligns with the global efforts towards reducing greenhouse gas emissions and promoting environmentally responsible practices. Government regulations and incentives promoting energy-efficient technologies also play a crucial role, encouraging the adoption of liquid cooling solutions. The continuous advancement in liquid cooling technology, leading to the development of more efficient and cost-effective systems, also contributes to the market's expansion. Innovations such as immersion cooling and two-phase cooling are gaining traction, further fueling market growth. Finally, the increasing demand for high-performance computing (HPC) applications in various industries, such as scientific research, financial modeling, and artificial intelligence, is driving the need for advanced cooling solutions capable of handling extremely high heat loads.

Despite the significant growth potential, the commercial liquid cooling equipment market faces several challenges and restraints. The high initial investment cost associated with implementing liquid cooling systems can be a barrier to entry for smaller companies and organizations with limited budgets. This often requires a significant upfront capital expenditure, which can be daunting for many potential adopters. The complexity of liquid cooling systems compared to air cooling systems also presents a challenge. Installation and maintenance require specialized expertise and skilled labor, potentially increasing operational costs. The potential for leaks and other fluid-related issues is another concern that needs to be addressed through robust system design, proper maintenance protocols, and the use of environmentally friendly coolants. The availability of qualified personnel to install, maintain, and troubleshoot liquid cooling systems is limited in some regions, which can hinder the widespread adoption of this technology. Moreover, the compatibility of liquid cooling systems with existing infrastructure can pose a challenge. Integrating liquid cooling into pre-existing data centers or server rooms can be complex and may require significant modifications, leading to additional expenses and downtime. Finally, the lack of standardized regulations and industry best practices for liquid cooling can create uncertainty and hinder the market's growth. Clearer guidelines and standardization would promote wider acceptance and facilitate smoother integration.

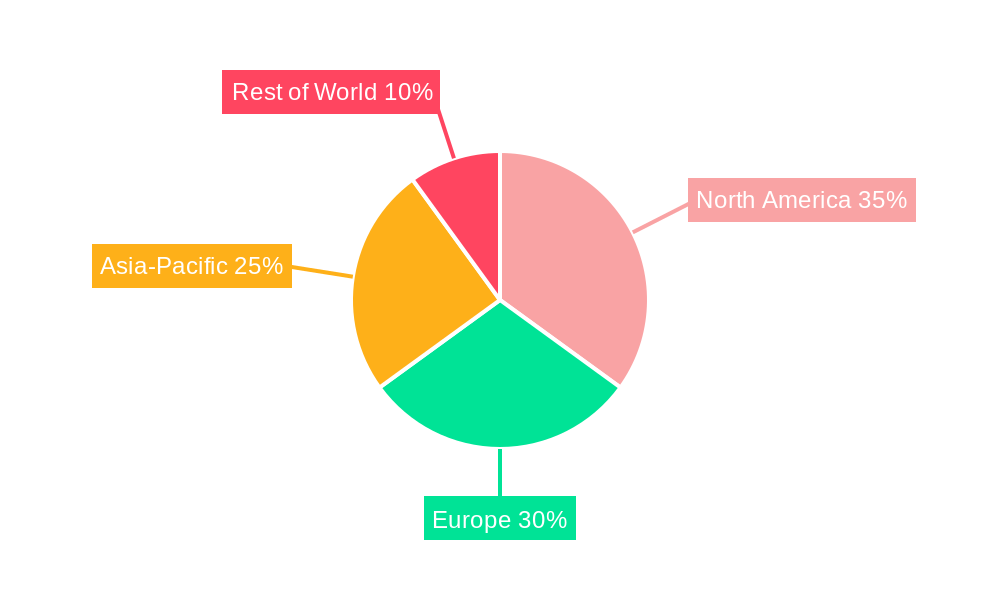

North America: This region is expected to dominate the market due to the high concentration of hyperscale data centers and the early adoption of advanced cooling technologies. The strong presence of major technology companies and a focus on energy efficiency drive the demand for liquid cooling solutions.

Asia-Pacific: This region is witnessing rapid growth, driven by the expanding data center infrastructure in countries like China, India, and Japan. The increasing demand for high-performance computing and the growing focus on digital transformation contribute to the market's expansion.

Europe: This region is showing significant growth potential, driven by the increasing adoption of cloud computing and the focus on sustainable data center operations. Stringent environmental regulations and incentives for energy-efficient technologies further stimulate the adoption of liquid cooling solutions.

Direct-to-Chip Cooling: This segment is expected to dominate the market due to its superior cooling efficiency and ability to handle high heat loads, particularly relevant in high-performance computing environments. The advancements in microfluidic technologies and the development of compact and reliable direct-to-chip coolers contribute to its market dominance.

Immersion Cooling: This segment is experiencing significant growth, driven by its ability to provide highly efficient cooling for high-density servers and GPUs. Immersion cooling offers exceptional heat dissipation and reduces the need for large cooling infrastructure.

The paragraph below combines the above points: The commercial liquid cooling equipment market is geographically diverse, with North America and the Asia-Pacific region leading the charge due to robust data center growth and technological advancements. Within these regions, and globally, direct-to-chip and immersion cooling segments are experiencing the most significant growth, surpassing other forms of liquid cooling. This is largely attributed to their superior cooling performance, energy efficiency, and applicability to the rapidly developing high-performance computing sector. The combination of geographic location and segment performance paint a picture of consistent market growth in the coming years.

The commercial liquid cooling equipment industry is poised for significant growth, fueled by several key catalysts. The rising demand for high-performance computing (HPC) and the expanding adoption of artificial intelligence (AI) are major drivers, demanding cooling solutions capable of handling extreme heat loads. Simultaneously, increasing concerns about energy efficiency and sustainability are pushing data center operators to adopt environmentally friendly cooling alternatives. Government regulations and initiatives further incentivize the transition to more energy-efficient technologies, thus accelerating the market's expansion. Finally, continuous innovation in liquid cooling technologies, such as advancements in immersion cooling and two-phase cooling techniques, is unlocking new possibilities for improved performance and cost savings.

This report offers an in-depth analysis of the commercial liquid cooling equipment market, covering historical data (2019-2024), the estimated year (2025), and detailed forecasts (2025-2033). It provides a comprehensive overview of market trends, driving forces, challenges, key players, and significant developments. The report also includes regional breakdowns and segment analysis, allowing for a nuanced understanding of market dynamics. The information provided enables informed decision-making for stakeholders across the commercial liquid cooling equipment value chain.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

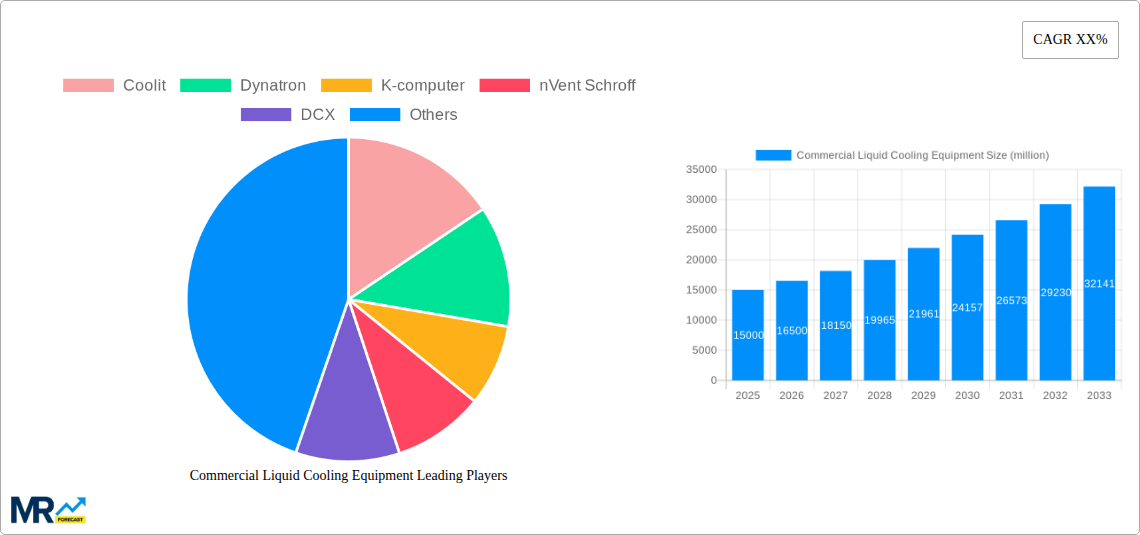

Key companies in the market include Coolit, Dynatron, K-computer, nVent Schroff, DCX, Nidec Corporation, Asetek, Schneider Electric, Rittal, Emerson, Mitsubishi Electric, EATON, Canatal, Airsys, Uniflair, Euroklimat, Inspur Electronic Information Industry, Dawning Information Industry, Lenovo Group, Envicool, Guangzhou Goaland Energy Conservation Tech, Unisplendour Corporation, Nanjing Canatal Data-centre Environmental Tech, Sugon Data Energy (Beijing), Alibaba Cloud, ZTE Corporation, Boyd, BLUEOCEAN, Vertiv, Delta, YMK, Gree, Stulz, Renovoair, Hisense, ITeaQ, Blackshields, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Commercial Liquid Cooling Equipment," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Commercial Liquid Cooling Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.