1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Cars On-board Charger CPU?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Commercial Cars On-board Charger CPU

Commercial Cars On-board Charger CPUCommercial Cars On-board Charger CPU by Type (3.0 - 3.7 kw, Higher than 3.7 kw, Lower than 3.0 kw), by Application (EV, PHEV), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

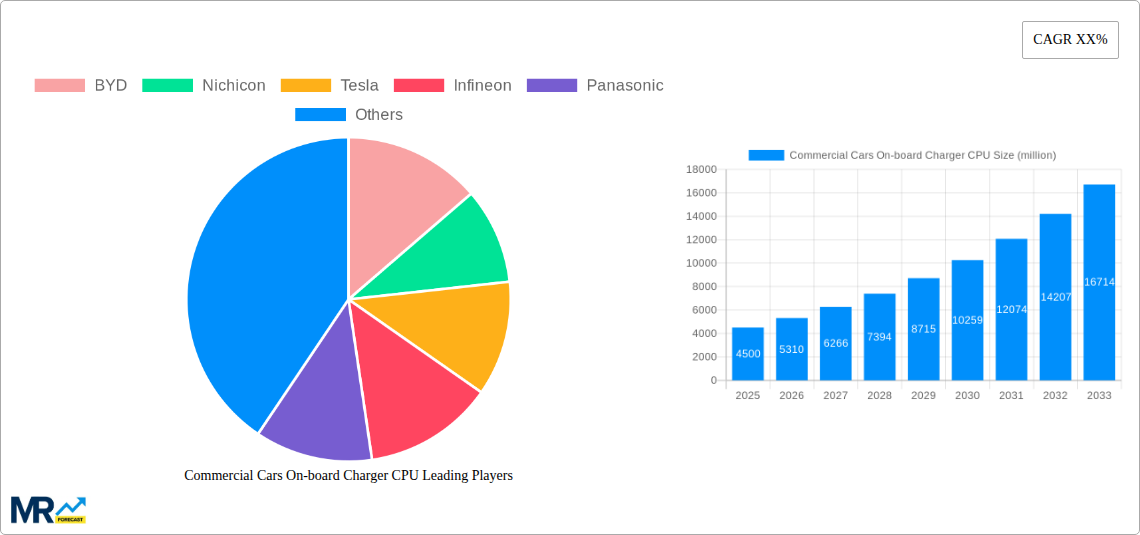

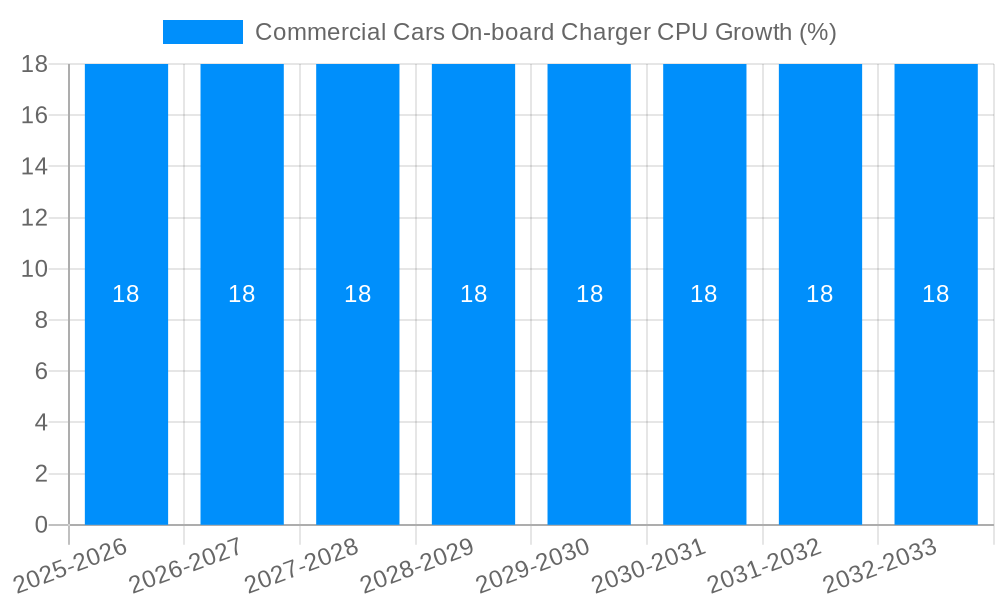

The global market for Commercial Cars On-board Charger (OBC) CPUs is experiencing robust growth, projected to reach an estimated market size of approximately $4,500 million by 2025, with a Compound Annual Growth Rate (CAGR) of around 18% during the 2025-2033 forecast period. This significant expansion is primarily driven by the accelerating adoption of electric vehicles (EVs) and plug-in hybrid electric vehicles (PHEVs) in commercial fleets. Increasing government incentives, stringent emission regulations, and a growing awareness of the operational cost savings associated with electric commercial vehicles are fueling this demand. The market is further propelled by advancements in charging technology, leading to higher power OBCs and faster charging times, essential for the operational efficiency of commercial fleets that require minimal downtime. Key segments include OBC CPUs for vehicles with power ratings between 3.0 kW and 3.7 kW, and those exceeding 3.7 kW, catering to a wide range of commercial vehicle types from light-duty vans to heavy-duty trucks.

The competitive landscape is characterized by the presence of major players like BYD, Nichicon, Tesla, Infineon, Panasonic, Aptiv, and LG, alongside specialized component manufacturers such as Dilong Technology and Tonhe Technology. These companies are actively investing in research and development to enhance the performance, efficiency, and cost-effectiveness of OBC CPUs. Emerging trends include the integration of advanced semiconductor technologies for improved thermal management and power density, as well as the development of smart charging solutions that optimize energy consumption and grid integration. Restraints, such as the initial high cost of electric commercial vehicles and the need for robust charging infrastructure expansion, are gradually being mitigated by technological progress and policy support. The Asia Pacific region, particularly China, is anticipated to lead market growth due to its established EV manufacturing ecosystem and aggressive government policies promoting electric mobility.

The global commercial vehicle on-board charger CPU market is poised for substantial growth, driven by the accelerating transition towards electrified fleets. Throughout the Study Period (2019-2033), with a Base Year of 2025 and a Forecast Period of 2025-2033, the market has witnessed significant advancements and adoption. In the Estimated Year of 2025, the market is projected to reach an impressive valuation, with unit shipments expected to surpass several million units globally. The Historical Period (2019-2024) laid the groundwork for this expansion, marked by initial investments in research and development and a growing awareness of the environmental and economic benefits of electric commercial vehicles. The increasing demand for zero-emission logistics and public transportation solutions is directly fueling the need for sophisticated and efficient on-board charging systems, where the CPU plays a pivotal role in managing power flow, ensuring safety, and optimizing charging cycles. Key players are continuously innovating to develop CPUs that can handle higher power outputs, faster charging times, and enhanced communication protocols, catering to the diverse needs of electric trucks, buses, and vans. The integration of advanced features like vehicle-to-grid (V2G) capabilities and intelligent charging algorithms are becoming increasingly important, further solidifying the CPU's central position in the on-board charger architecture. By 2025, the market is expected to see a notable increase in the average charging power supported by these CPUs, with a significant portion of new deployments focusing on charging capacities Higher than 3.7 kW. This trend is directly linked to the evolving battery technologies and the operational demands of commercial fleets that require faster turnaround times.

The burgeoning electric vehicle (EV) and plug-in hybrid electric vehicle (PHEV) segments for commercial applications are the primary engines driving the on-board charger CPU market. As governments worldwide implement stringent emission regulations and offer substantial incentives for fleet electrification, manufacturers are compelled to integrate advanced on-board charging solutions. This necessitates the adoption of powerful and intelligent CPUs capable of managing the complex charging processes for larger battery packs found in commercial vehicles. Furthermore, the growing awareness among fleet operators regarding the total cost of ownership (TCO) benefits of electric vehicles, including reduced fuel and maintenance costs, is accelerating their adoption. The increasing availability of charging infrastructure, coupled with advancements in battery technology that offer greater range and faster charging capabilities, directly translates into a higher demand for robust and efficient on-board charger CPUs. The ongoing technological evolution in power electronics and semiconductor manufacturing is also enabling the development of more compact, cost-effective, and higher-performance CPUs, making electrification a more viable option for a wider range of commercial vehicles. The need for seamless integration with fleet management systems and smart grid technologies further underscores the importance of sophisticated CPU solutions.

Despite the robust growth trajectory, the commercial vehicle on-board charger CPU market faces several hurdles. One of the primary challenges is the high initial cost associated with electric commercial vehicles and their associated charging infrastructure, which can be a significant deterrent for some fleet operators, especially smaller enterprises. The lack of standardized charging protocols and interoperability issues across different regions and manufacturers can also create complexities in deployment and maintenance. Furthermore, the rapid pace of technological advancement necessitates continuous investment in research and development, posing a challenge for smaller players in the market to keep up with innovation. The limited availability of skilled technicians for servicing and repairing complex on-board charging systems in remote areas can also be a concern. Extreme operating temperatures and harsh environmental conditions encountered by commercial vehicles require CPUs to be highly robust and reliable, adding to the development and manufacturing costs. Addressing these challenges through standardization efforts, government support for infrastructure development, and enhanced training programs will be crucial for sustained market expansion.

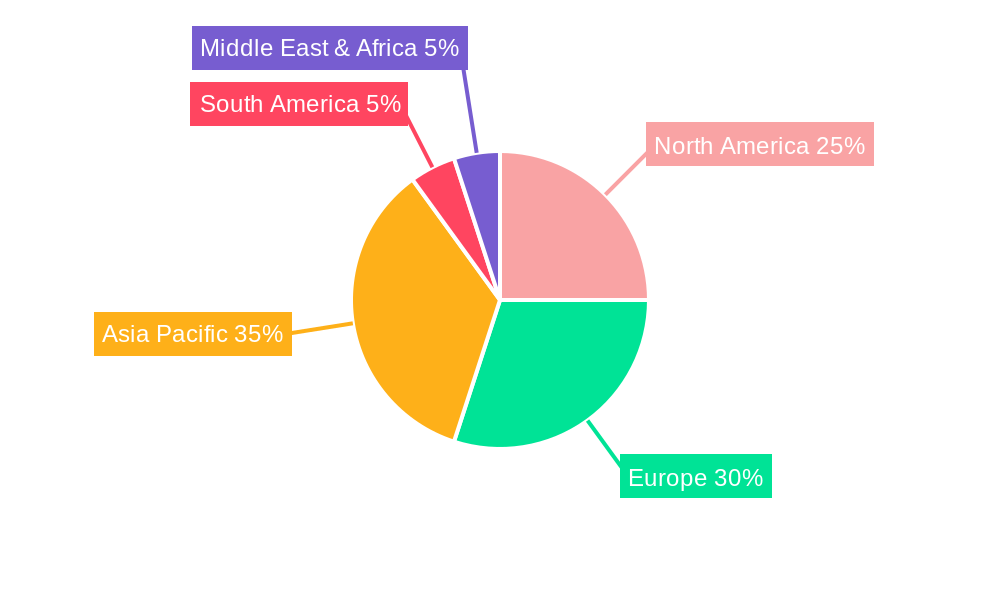

The global commercial vehicle on-board charger CPU market is expected to witness a significant dominance by Asia Pacific, particularly China, driven by a confluence of strong government support for EV adoption, a massive domestic automotive manufacturing base, and a growing logistics sector. China's ambitious targets for carbon neutrality and its substantial investments in electric vehicle infrastructure, including charging stations and battery manufacturing, provide a fertile ground for the growth of on-board charger CPUs. The region's established players like BYD and Dilong Technology are at the forefront of innovation, catering to the burgeoning demand for electric buses and trucks.

Within this dominant region, the Application segment of EV (Electric Vehicles) is projected to command the largest market share. This is directly attributable to the widespread adoption of fully electric buses for public transportation and an increasing number of electric trucks entering the logistics and delivery fleets. These vehicles typically require higher charging capacities and more advanced CPU functionalities to manage the power requirements of their larger battery packs and to ensure efficient operation throughout demanding duty cycles.

The Type segment of Higher than 3.7 kW is also anticipated to be a dominant force in the market. As commercial vehicles are deployed for longer routes and heavier payloads, the need for faster charging to minimize downtime becomes paramount. On-board chargers with capacities exceeding 3.7 kW are essential to meet these operational demands, enabling quicker replenishment of battery charge during operational breaks. This segment's growth is intrinsically linked to the evolution of battery technology and the increasing performance expectations from fleet operators. The combination of strong regional manufacturing capabilities in Asia Pacific, the robust adoption of fully electric commercial vehicles, and the increasing demand for higher-power charging solutions positions these segments for market leadership.

Companies like BYD, with its integrated approach to electric vehicle manufacturing, and Dilong Technology, specializing in power electronics for EVs, are well-positioned to capitalize on this trend. The sheer volume of commercial vehicle production and sales in China, coupled with supportive policies, will likely ensure the region's sustained dominance in the coming years.

Several factors are acting as significant growth catalysts for the commercial vehicle on-board charger CPU market. The increasing environmental consciousness and stricter emission regulations globally are compelling businesses to transition to electric fleets, directly boosting demand for on-board charging solutions. Technological advancements, particularly in battery density and charging speeds, are making EVs more practical for commercial applications. Furthermore, favorable government policies, including subsidies and tax credits for EV adoption, are reducing the cost barrier for fleet operators. The growing investments in charging infrastructure and the development of smart grid technologies also support the wider adoption of electric commercial vehicles.

This report offers an in-depth analysis of the commercial vehicle on-board charger CPU market, providing a comprehensive overview of trends, drivers, and challenges. It meticulously examines market segmentation by type, power output, and application, offering detailed insights into each category. The report leverages historical data from the Historical Period (2019-2024) and projects future market trajectories through the Forecast Period (2025-2033), with a strong emphasis on the Base Year of 2025 and the Estimated Year of 2025. It details the competitive landscape, highlighting the strategies and innovations of leading players like BYD, Nichicon, Tesla, and Infineon. Furthermore, the report explores significant industry developments and their potential impact, providing actionable intelligence for stakeholders to navigate this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include BYD, Nichicon, Tesla, Infineon, Panasonic, Aptiv, LG, Lear, Dilong Technology, Kongsberg, Kenergy, Wanma, IES, Anghua, Lester, Tonhe Technology, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Commercial Cars On-board Charger CPU," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Commercial Cars On-board Charger CPU, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.