1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Airplane Wheels?

The projected CAGR is approximately 6.12%.

Commercial Airplane Wheels

Commercial Airplane WheelsCommercial Airplane Wheels by Type (Main Wheel, Nose Wheel, World Commercial Airplane Wheels Production ), by Application (Narrow Body Airplane, Wide Body Airplane, World Commercial Airplane Wheels Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

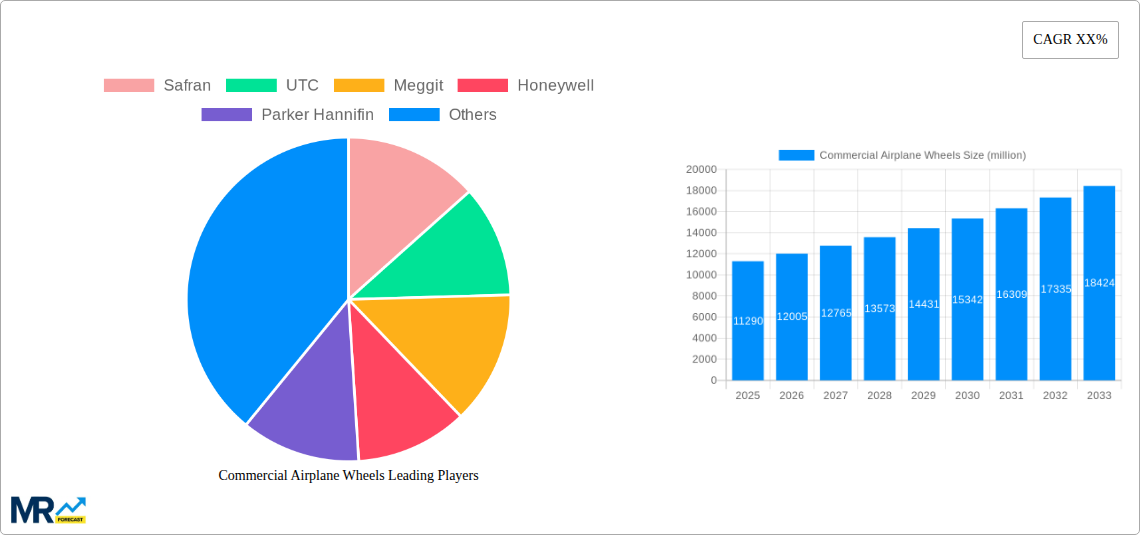

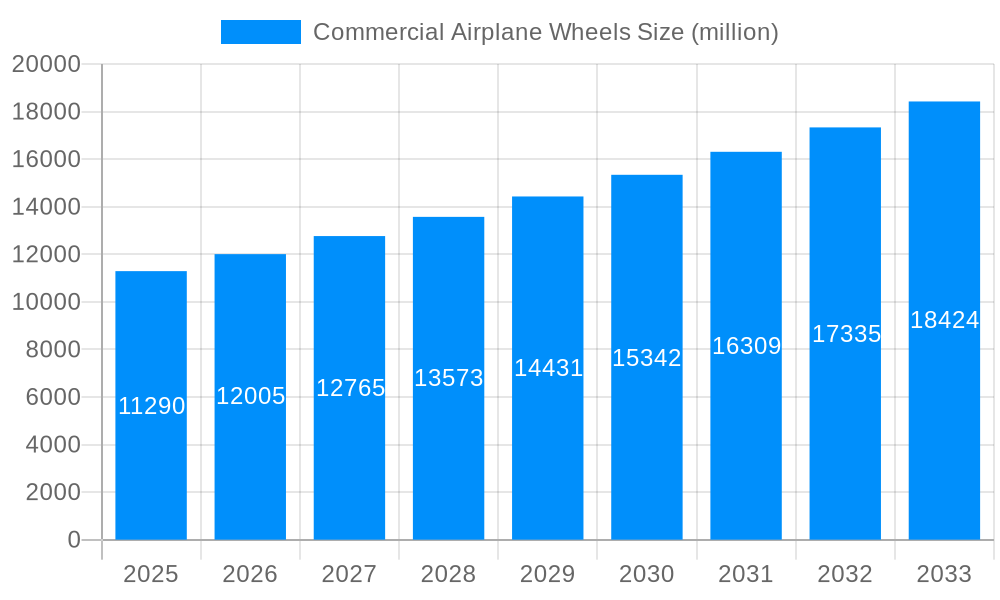

The global commercial airplane wheels market is projected for robust expansion, valued at approximately $11.29 billion in the base year 2025. With a projected Compound Annual Growth Rate (CAGR) of 6.12% from 2025 to 2033, the market is expected to witness substantial growth, driven by the increasing global demand for air travel and the subsequent expansion of commercial airline fleets. Factors such as rising disposable incomes in emerging economies, a growing middle class, and the resurgence of international tourism post-pandemic are fueling aircraft manufacturing and consequently, the demand for replacement and new aircraft wheels. Advancements in materials science, leading to lighter, more durable, and fuel-efficient wheel components, are also significant growth drivers, enabling manufacturers to offer enhanced performance and reduced maintenance costs for airlines.

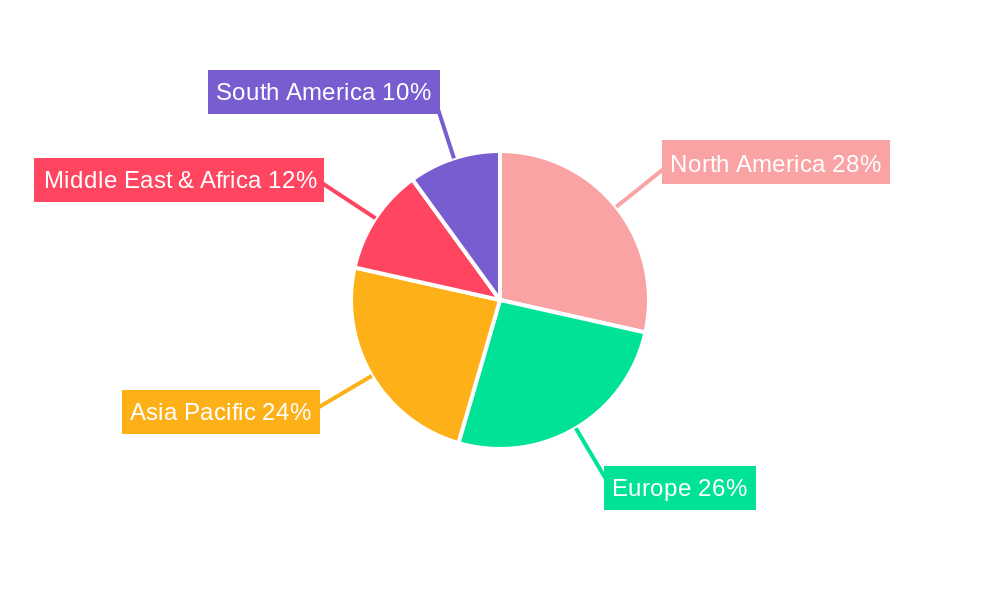

The market segmentation reveals key areas of focus, with the "Main Wheel" type dominating the production, alongside the critical "Nose Wheel" segment. In terms of application, both "Narrow Body Airplane" and "Wide Body Airplane" segments are expected to contribute significantly to market growth, reflecting the diverse fleet compositions of global airlines. Key players such as Safran, UTC, Meggitt, Honeywell, and Parker Hannifin are poised to capitalize on this growth, innovating and expanding their production capacities. Geographically, the Asia Pacific region is anticipated to emerge as a significant growth hub, propelled by rapid fleet expansion in countries like China and India, while North America and Europe will continue to hold substantial market shares due to established aviation infrastructure and ongoing fleet modernization. Potential restraints, such as stringent regulatory approvals for new materials and designs, and the cyclical nature of aircraft manufacturing, will need to be navigated by market participants.

Here's a unique report description for Commercial Airplane Wheels, incorporating the requested elements:

This comprehensive report delves deep into the dynamic global commercial airplane wheels market, offering a detailed analysis of its trajectory from 2019 to 2033. With a base year of 2025, the study meticulously examines historical trends, current market valuations, and future projections, providing invaluable insights for stakeholders. The market, estimated to be valued in the tens of billions of US dollars for 2025, is poised for substantial growth driven by the resurgence of air travel and continuous technological advancements. This report meticulously dissects the key drivers, challenges, and opportunities that shape this critical aviation component segment.

The analysis encompasses a granular breakdown of the market by product type, including Main Wheels and Nose Wheels, and by application, focusing on Narrow Body Airplanes and Wide Body Airplanes. Furthermore, it provides an in-depth understanding of the World Commercial Airplane Wheels Production landscape, identifying key manufacturing hubs and their respective contributions. The report also scrutinizes industry developments and the strategic initiatives undertaken by leading players like Safran, UTC, Meggitt, Honeywell, and Parker Hannifin. This detailed examination will equip businesses with the knowledge to make informed strategic decisions, identify emerging opportunities, and navigate the complex yet promising future of the commercial airplane wheels industry.

XXX The global commercial airplane wheels market is experiencing a significant upswing, driven by a confluence of factors that are redefining its landscape. The post-pandemic recovery in air travel has been a primary catalyst, with airlines worldwide gradually increasing their fleet utilization and placing new aircraft orders. This heightened demand translates directly into a greater need for new wheel assemblies and replacement parts, pushing the market value into the billions of US dollars. The study period, spanning from 2019 to 2033, with a base year of 2025, highlights a robust growth trajectory, with the forecast period (2025-2033) expected to witness sustained expansion. Trends indicate a growing preference for lighter, more durable, and technologically advanced wheel systems. Innovations in materials science, such as the increased adoption of advanced composites and high-strength alloys, are enabling manufacturers to produce wheels that offer improved fuel efficiency through weight reduction, enhanced safety features, and extended service life. This not only benefits airlines by reducing operational costs but also contributes to the industry's sustainability goals. The evolving airline fleet composition, with a strong emphasis on fuel-efficient narrow-body aircraft for short-to-medium haul routes and the continued demand for wide-body aircraft for long-haul travel, directly influences the type and volume of wheels required. The market is also witnessing an increasing focus on the integration of smart technologies within wheel systems, including sensor-equipped components that can monitor tire pressure, temperature, and wear in real-time. This predictive maintenance capability promises to revolutionize operational efficiency and safety protocols for airlines. Furthermore, the increasing complexity of aircraft designs and the stringent regulatory environment are driving continuous research and development efforts, ensuring that the commercial airplane wheels sector remains at the forefront of innovation. The historical period (2019-2024) laid the groundwork for this resurgence, characterized by initial disruptions and subsequent recovery.

The commercial airplane wheels market is being propelled by a powerful combination of factors that underscore its critical role in global aviation. Foremost among these is the robust recovery and projected growth of global air passenger traffic. As economies rebound and travel restrictions ease, airlines are witnessing a surge in demand, necessitating the expansion and modernization of their fleets. This directly translates into increased orders for new aircraft, each equipped with multiple wheel assemblies. The estimated market value in the billions of US dollars for 2025 is a testament to this burgeoning demand. Furthermore, technological advancements and innovation are playing a pivotal role. Manufacturers are continuously investing in research and development to produce lighter, stronger, and more efficient wheel systems. The adoption of advanced materials such as composite alloys and titanium, alongside sophisticated manufacturing techniques, is leading to improved performance, reduced aircraft weight, and consequently, enhanced fuel efficiency. This focus on sustainability and cost optimization is a key driver for airlines making purchasing decisions. The increasing production of new-generation aircraft, particularly fuel-efficient narrow-body jets like the Boeing 737 MAX and Airbus A320neo families, and the sustained demand for wide-body aircraft, are creating substantial and ongoing demand for their associated wheel components. These modern aircraft are designed with advanced aerodynamic features and lighter structures, requiring equally sophisticated and lightweight wheel systems to complement their design. Finally, the aging global aircraft fleet also contributes significantly, as a substantial number of aircraft are nearing the end of their operational lifespan, necessitating replacement parts and eventually, new wheel assemblies for newly ordered aircraft.

Despite the promising growth outlook, the commercial airplane wheels market faces several significant challenges and restraints that could temper its expansion. One of the most prominent is the stringent regulatory environment and certification processes. The aerospace industry is subject to rigorous safety standards and extensive testing requirements, meaning that the development and introduction of new wheel technologies are often time-consuming and costly. Any delay or failure in achieving certification can have a substantial impact on market entry and adoption. Furthermore, volatility in raw material prices, particularly for specialized alloys and composites used in wheel manufacturing, can significantly affect production costs and profit margins. Fluctuations in the prices of metals like aluminum, titanium, and specialty rubbers can create unpredictability for manufacturers and, in turn, for their pricing strategies. Geopolitical instability and global economic uncertainties also pose a threat. Disruptions to global supply chains, trade disputes, and economic downturns can lead to a reduction in airline profitability, potentially impacting new aircraft orders and maintenance, repair, and overhaul (MRO) spending, which directly influences demand for airplane wheels. The intense competition among key players can also exert downward pressure on prices and margins, forcing companies to focus on efficiency and innovation to maintain their market share. Moreover, the long lead times for aircraft production and wheel manufacturing mean that the market is sensitive to sudden shifts in demand, potentially leading to oversupply or undersupply situations. Lastly, the increasing demand for sustainable aviation practices puts pressure on manufacturers to develop wheels that are not only lighter and more durable but also contribute to reduced environmental impact throughout their lifecycle, which can require significant investment in R&D.

The global commercial airplane wheels market exhibits a complex interplay of regional dominance and segment leadership, driven by manufacturing capabilities, airline fleet sizes, and aviation infrastructure. Based on the analysis of World Commercial Airplane Wheels Production and Application: Narrow Body Airplane, North America is poised to be a dominant region, primarily due to the presence of major aircraft manufacturers like Boeing, a significant airline industry, and advanced MRO facilities. The United States, in particular, boasts a substantial portion of the global aircraft wheel production and a large installed base of narrow-body aircraft, which are the workhorses of many North American airlines for domestic and short-haul international routes. The sheer volume of Narrow Body Airplane operations in this region directly translates into consistent demand for both new wheel assemblies and extensive maintenance, repair, and overhaul services for existing fleets. This segment's dominance is further reinforced by the ongoing modernization of airline fleets, with a continuous influx of new-generation narrow-body aircraft that necessitate the latest in wheel technology.

In terms of specific segments, the Main Wheel segment within the Narrow Body Airplane application is expected to hold a significant market share. Main wheels bear the brunt of the aircraft's weight during landing and taxiing, requiring robust engineering and advanced materials. The high frequency of takeoffs and landings in narrow-body operations leads to higher wear and tear, thus driving a consistent demand for replacement main wheels and related services.

Furthermore, the World Commercial Airplane Wheels Production landscape highlights the strategic importance of countries with established aerospace manufacturing ecosystems. Besides North America, Europe also emerges as a key player, largely driven by the presence of Airbus and a strong network of tier-1 and tier-2 suppliers, including prominent players like Safran and Meggitt. This region benefits from significant aircraft production and a robust aftermarket service network. The focus on technological innovation and the adoption of advanced manufacturing techniques in both regions further solidifies their leading positions.

The Application: Wide Body Airplane segment, while potentially smaller in volume compared to narrow-body, represents a high-value market due to the complexity and specialized nature of the wheels required for these larger aircraft. The sustained demand for long-haul travel and the freighter market contributes to the ongoing relevance of wide-body aircraft and, consequently, their wheel systems. The Nose Wheel segment, though smaller in terms of individual unit complexity, is crucial for aircraft maneuverability and braking during ground operations. The continuous rotation and steering demands of nose wheels in commercial aviation contribute to a steady demand for their production and maintenance. Therefore, the interplay between North America and Europe as manufacturing and operational hubs, coupled with the high-volume demand from the Narrow Body Airplane segment, especially for Main Wheels, and the high-value contribution of the Wide Body Airplane segment, are expected to define the market's dominant forces.

Several key factors are acting as significant growth catalysts for the commercial airplane wheels industry. The most prominent is the projected resumption and sustained growth of global air travel, leading to increased aircraft production and fleet expansion. The advancements in material science and manufacturing technologies are enabling the development of lighter, more durable, and fuel-efficient wheel systems. Furthermore, the continuous replacement cycle of aging aircraft fleets and the demand for upgraded components for existing aircraft contribute to a steady aftermarket demand. The increasing focus on predictive maintenance and smart wheel technologies also presents a significant growth avenue.

This report provides an exhaustive examination of the commercial airplane wheels market, offering a holistic view of its intricate dynamics. It delves into the estimated market valuation in the billions of US dollars for 2025, providing a clear snapshot of the industry's current economic standing. The study meticulously forecasts market trends and growth projections from 2019 to 2033, with a focused analysis of the 2025-2033 forecast period. Detailed segmentation by product type (Main Wheel, Nose Wheel) and application (Narrow Body Airplane, Wide Body Airplane) ensures a granular understanding of specific market segments. The report also critically assesses World Commercial Airplane Wheels Production capabilities and industry developments, providing insights into the competitive landscape and the strategic initiatives of key players like Safran, UTC, Meggitt, Honeywell, and Parker Hannifin. This comprehensive coverage ensures that stakeholders receive actionable intelligence to navigate the evolving commercial airplane wheels sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.12% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.12%.

Key companies in the market include Safran, UTC, Meggit, Honeywell, Parker Hannifin, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Commercial Airplane Wheels," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Commercial Airplane Wheels, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.