1. What is the projected Compound Annual Growth Rate (CAGR) of the Civil Use Cockpit Voice & Flight Data Recorder?

The projected CAGR is approximately 3.3%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Civil Use Cockpit Voice & Flight Data Recorder

Civil Use Cockpit Voice & Flight Data RecorderCivil Use Cockpit Voice & Flight Data Recorder by Type (Flight Data Recorder (FDR), Cockpit Voice Recorder (CVR), Combined Voice and Flight Data Recorder (CVFDR)), by Application (Commercial Aircraft, Private Aircraft), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

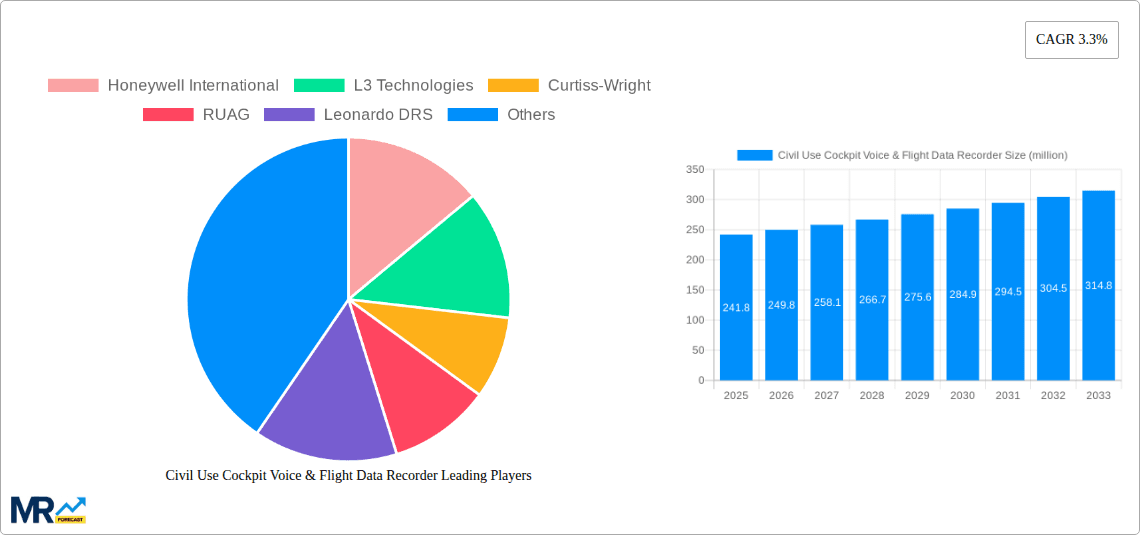

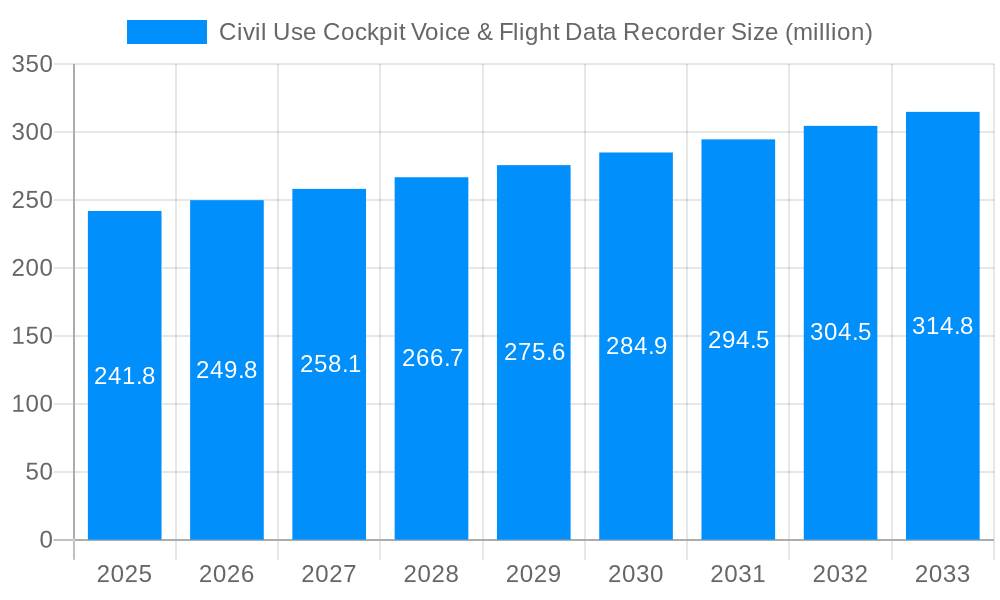

The Civil Use Cockpit Voice & Flight Data Recorder market is poised for steady expansion, projected to reach an estimated USD 241.8 million by 2025. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 3.3% anticipated over the forecast period from 2025 to 2033. A primary driver for this sustained upward trajectory is the ever-increasing emphasis on aviation safety regulations and mandates worldwide. Governments and international aviation authorities are continuously reinforcing and updating standards for flight data recording, necessitating the adoption and upgrade of these critical systems by airlines and aircraft manufacturers. Furthermore, the ongoing modernization of civil aviation fleets, including both commercial and private aircraft, contributes significantly to market demand. As older aircraft are retired and newer, technologically advanced models are introduced, the integration of state-of-the-art cockpit voice and flight data recorders becomes a standard requirement. The growing global air traffic, coupled with the inherent need for robust accident investigation and prevention tools, further solidifies the market's growth prospects.

The market segmentation reveals a diverse landscape, with the Flight Data Recorder (FDR) segment expected to hold a dominant share due to its comprehensive data logging capabilities crucial for flight analysis. The increasing sophistication of these recorders, offering more parameters and higher fidelity data, is a key trend. Combined Voice and Flight Data Recorders (CVFDRs) are also gaining traction as manufacturers strive for integrated, space-saving solutions that provide a holistic view of flight events. Geographically, North America and Europe are anticipated to remain leading markets, driven by mature aviation industries and stringent safety oversight. However, the Asia Pacific region is expected to witness the most rapid growth, fueled by burgeoning air travel demand, expanding airline fleets, and significant investments in aviation infrastructure and safety technologies. Key players like Honeywell International, L3 Technologies, and Safran are at the forefront, innovating and expanding their product portfolios to meet evolving regulatory requirements and customer demands for enhanced data security, durability, and real-time monitoring capabilities.

The global Civil Use Cockpit Voice & Flight Data Recorder (CVR/FDR) market, projected to reach an impressive USD 2.3 billion by 2033, is experiencing a dynamic evolution driven by a confluence of technological advancements, stringent safety regulations, and the ever-increasing global air traffic. During the historical period of 2019-2024, the market demonstrated steady growth, bolstered by routine aircraft fleet expansions and the mandatory integration of these critical safety devices. The base year of 2025 stands as a pivotal point, with the market estimated to be worth USD 1.9 billion, setting the stage for significant expansion in the subsequent forecast period of 2025-2033. A key trend observed is the increasing demand for Combined Voice and Flight Data Recorders (CVFDRs). This integration offers enhanced efficiency and reduced installation complexity, appealing strongly to aircraft manufacturers and operators alike. The shift towards more advanced recorder technologies, capable of capturing a wider array of data parameters and offering higher fidelity audio, is another prominent trend. This is being driven by the need for more comprehensive accident investigation capabilities and proactive safety monitoring. Furthermore, the growing emphasis on digital transformation within the aviation industry is spurring the development of "smarter" recorders, with enhanced connectivity features for real-time data offloading and remote diagnostics, though the full realization of these capabilities will unfold over the study period. The miniaturization of components and the drive for lighter, more robust recorder designs are also influencing product development, particularly for private aircraft segments where weight and space constraints can be more pronounced. The evolving regulatory landscape, with international bodies consistently updating their requirements for recorder capabilities and data retention, acts as a constant catalyst for market innovation and growth. The market is expected to see a compound annual growth rate (CAGR) of approximately 3.5% from 2025 to 2033.

The trajectory of the Civil Use Cockpit Voice & Flight Data Recorder market is undeniably propelled by the paramount importance of aviation safety. Global regulatory bodies, such as the FAA and EASA, continuously update and enforce mandates for the installation and operational integrity of CVRs and FDRs. These regulations are not static; they evolve to incorporate lessons learned from accident investigations and to leverage emerging technological capabilities for enhanced data acquisition and survivability. The steady growth in global air passenger traffic, particularly in emerging economies, directly translates into an increased demand for new aircraft, thereby creating a sustained need for these essential safety devices. Furthermore, the aging global aircraft fleet necessitates regular maintenance, upgrades, and replacements of existing CVR/FDR systems, contributing to a robust aftermarket segment. The increasing sophistication of flight operations, including the growing complexity of modern aircraft systems and flight envelopes, requires recorders capable of capturing a wider and more detailed spectrum of data to facilitate thorough accident investigations and contribute to proactive safety analysis. The ongoing commitment of aviation manufacturers to enhance aircraft reliability and operational efficiency also indirectly fuels the demand for advanced CVR/FDR technologies that can provide deeper insights into system performance and pilot decision-making.

Despite the strong growth drivers, the Civil Use Cockpit Voice & Flight Data Recorder market encounters several challenges and restraints that can influence its expansion. One significant restraint is the high initial cost associated with the development, manufacturing, and integration of advanced CVR/FDR systems. These sophisticated pieces of equipment require substantial investment in research and development, leading to premium pricing that can be a barrier, especially for smaller airlines or operators of older, smaller aircraft. The stringent certification processes imposed by aviation authorities, while crucial for safety, can be time-consuming and costly for manufacturers, potentially delaying product launches and market entry. Furthermore, the need for ongoing maintenance, calibration, and eventual replacement of these recorders throughout an aircraft's lifecycle adds to the operational expenses for airlines. In some instances, particularly in older aircraft or specific regional markets, regulatory compliance might be less stringently enforced, leading to a slower adoption rate of the latest technologies. The limited availability of skilled technicians trained to install, maintain, and troubleshoot these complex systems in certain geographical locations can also pose a challenge. Finally, the relatively long lifespan of existing CVR/FDR units within an aircraft's operational life can moderate the pace of new unit sales as airlines prioritize other capital expenditures.

The global Civil Use Cockpit Voice & Flight Data Recorder market is characterized by the dominance of certain regions and segments, driven by factors such as air traffic volume, regulatory stringency, and aircraft manufacturing activity.

Dominant Segments:

Commercial Aircraft Application: This segment consistently represents the largest share of the market. The sheer volume of commercial aircraft operating globally, coupled with stringent safety regulations mandating CVR/FDR installations for passenger safety, makes this application the primary revenue generator. The continuous expansion of commercial aviation fleets, particularly in Asia-Pacific and the Middle East, further solidifies its dominance. The demand for newer, more sophisticated recorders that can capture an extensive range of flight parameters and provide higher fidelity audio is a key driver within this segment.

Combined Voice and Flight Data Recorder (CVFDR): While Flight Data Recorders (FDRs) and Cockpit Voice Recorders (CVRs) have historically been separate units, the trend towards CVFDRs is gaining significant momentum. These combined units offer cost efficiencies, reduced installation complexity, and space savings, making them highly attractive to aircraft manufacturers and airlines. The market share of CVFDRs is projected to grow substantially as new aircraft designs increasingly incorporate these integrated solutions.

Dominant Regions/Countries:

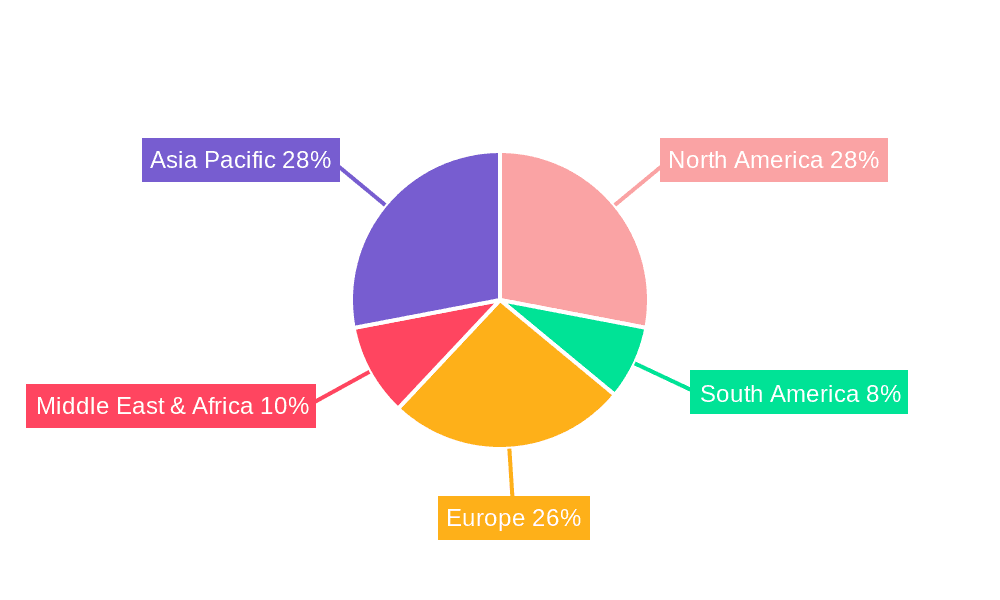

North America (United States & Canada): This region holds a significant market share due to the presence of a large, mature commercial aviation market and a robust private aircraft sector. The stringent regulatory environment enforced by the FAA, which consistently leads the world in aviation safety standards, ensures a high demand for compliant and advanced CVR/FDR systems. Furthermore, the presence of major aircraft manufacturers and leading CVR/FDR technology providers, such as Honeywell International and L3 Technologies, based in the United States, provides a strong domestic demand and innovation hub.

Europe: Similar to North America, Europe boasts a substantial commercial aviation industry and a well-established regulatory framework under the European Union Aviation Safety Agency (EASA). Countries like Germany, France, the UK, and others contribute significantly to the market through their active airlines and aircraft manufacturing presence (e.g., Airbus, which has substantial operations in Europe). The focus on harmonized safety standards across member states ensures a steady demand for CVR/FDRs.

Asia-Pacific (China, India, and Southeast Asia): This region is emerging as a powerhouse for the CVR/FDR market, driven by rapid air traffic growth and expanding airline fleets. Countries like China and India are experiencing unprecedented growth in their aviation sectors, necessitating massive aircraft procurements and, consequently, a surge in demand for CVR/FDRs. While regulatory frameworks are evolving, they are increasingly aligning with international standards to enhance aviation safety. The presence of emerging aircraft manufacturers also contributes to the regional market dynamics.

These regions and segments are expected to continue their dominance throughout the forecast period of 2025-2033, with the Asia-Pacific region exhibiting the highest growth potential due to ongoing fleet expansion and the increasing emphasis on aviation safety infrastructure. The interplay between evolving regulations, technological advancements in recorder capabilities, and the economic factors driving air travel will continue to shape the market landscape.

The Civil Use Cockpit Voice & Flight Data Recorder industry is propelled by several key growth catalysts. The unwavering focus on aviation safety by global regulatory bodies, leading to continuous updates and enforcement of stricter mandates for recorder data and survivability, is a primary driver. The projected increase in global air traffic, particularly with the expansion of commercial aviation in emerging economies, directly fuels demand for new aircraft and the integrated safety systems they require. Furthermore, the ongoing need to replace aging recorders in the existing global aircraft fleet, along with the integration of advanced technologies offering enhanced data capture and analysis capabilities, contributes significantly to market expansion.

This report offers an exhaustive examination of the Civil Use Cockpit Voice & Flight Data Recorder market, providing a detailed analysis of its current state and future trajectory. It delves into key market insights, identifying critical trends and their implications for stakeholders. The report meticulously breaks down the driving forces and challenges that shape market dynamics, offering a balanced perspective on the opportunities and hurdles faced by industry players. With a comprehensive regional and segment-wise analysis, the report highlights areas poised for significant growth, particularly focusing on the dominance of commercial aircraft applications and the burgeoning demand in the Asia-Pacific region. Furthermore, it identifies the key growth catalysts that are expected to fuel the market's expansion. The report also provides a robust overview of the leading companies actively participating in this sector and chronicles significant technological developments and innovations that are shaping the future of CVR/FDR technology. This holistic approach ensures a thorough understanding of the market for industry professionals, investors, and policymakers.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.3%.

Key companies in the market include Honeywell International, L3 Technologies, Curtiss-Wright, RUAG, Leonardo DRS, Safran, GE Aviation, UASC, .

The market segments include Type, Application.

The market size is estimated to be USD 241.8 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Civil Use Cockpit Voice & Flight Data Recorder," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Civil Use Cockpit Voice & Flight Data Recorder, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.