1. What is the projected Compound Annual Growth Rate (CAGR) of the Cell Counter for Hospitals and Universities?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Cell Counter for Hospitals and Universities

Cell Counter for Hospitals and UniversitiesCell Counter for Hospitals and Universities by Type (Benchtop Cell Counters, Handheld Cell Counters), by Application (Hospitals, Universities), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

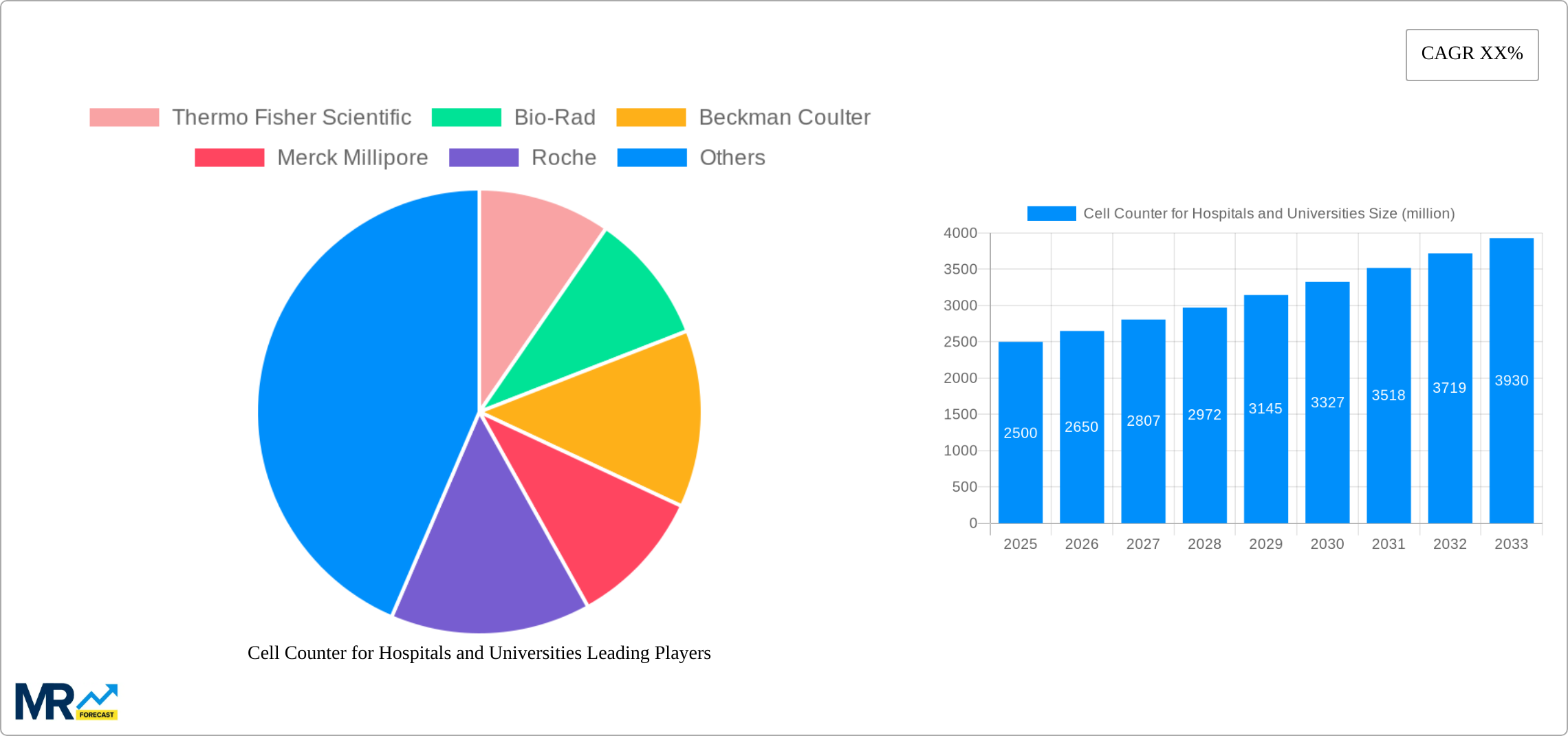

The global cell counter market for hospitals and universities is experiencing robust growth, driven by increasing research activities, advancements in life sciences, and a rising prevalence of infectious diseases demanding rapid and accurate diagnostic tools. The market, segmented by type into benchtop and handheld cell counters and by application into hospitals and universities, shows a strong preference for benchtop systems in research-intensive settings like universities, while hospitals often opt for a blend depending on their specific needs (high throughput vs. point-of-care testing). The market is highly competitive, with key players like Thermo Fisher Scientific, Bio-Rad, and Beckman Coulter holding significant market share due to their established brand reputation and comprehensive product portfolios. However, smaller companies specializing in innovative technologies, such as automated cell counting and image analysis, are emerging as strong contenders, particularly in niche applications. The North American and European regions currently dominate the market, fueled by robust funding for research and development, advanced healthcare infrastructure, and stringent regulatory frameworks promoting technological advancements. However, significant growth potential exists in the Asia-Pacific region, driven by rapid economic expansion, growing healthcare expenditure, and a burgeoning life sciences sector. Continued technological innovations, including the development of more user-friendly, portable, and cost-effective cell counters, along with increasing collaborations between research institutions and manufacturers, will propel future market expansion.

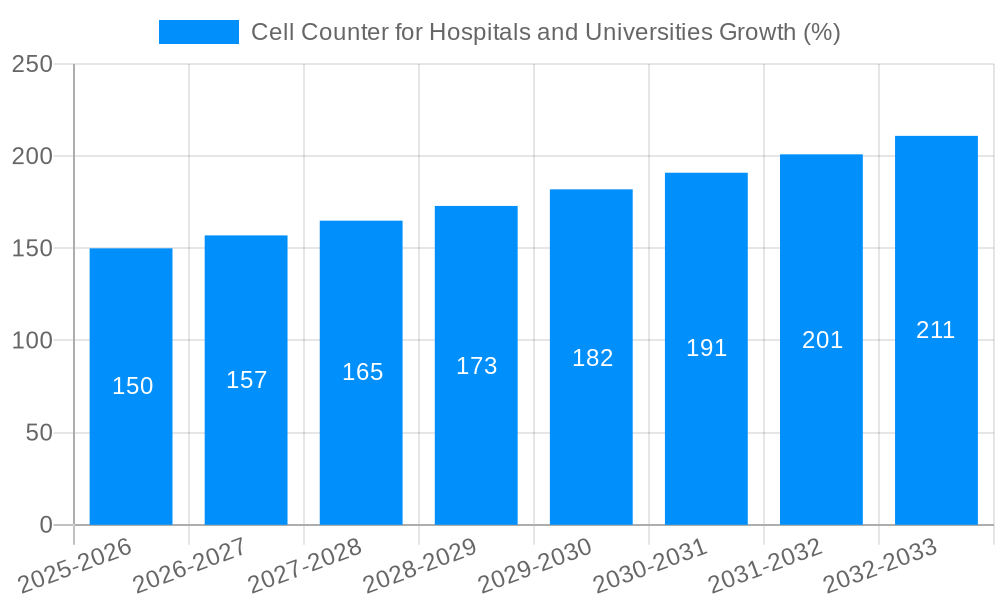

Over the forecast period (2025-2033), the market is projected to maintain a healthy Compound Annual Growth Rate (CAGR), largely influenced by the adoption of advanced cell counting techniques in various research and clinical applications. Factors like the increasing demand for personalized medicine, expanding genomic research, and the need for high-throughput screening in drug discovery are key drivers. However, certain restraints, such as the high cost of advanced cell counters and the need for skilled personnel for operation and maintenance, might partially temper growth. To mitigate these, manufacturers are increasingly focusing on developing cost-effective models and providing comprehensive training and support services. Furthermore, the market is expected to witness a rise in strategic partnerships, mergers, and acquisitions among industry players, aiming to enhance their product portfolio and market reach. This competitive landscape, coupled with ongoing technological innovations, ensures a dynamic and evolving market with continuous opportunities for growth and innovation.

The global cell counter market for hospitals and universities is experiencing robust growth, projected to reach multi-million unit sales by 2033. The market's expansion is driven by several converging factors. Firstly, the increasing prevalence of chronic diseases necessitates more sophisticated diagnostic and research tools, boosting demand for accurate and efficient cell counting technologies. This is particularly true in hospitals, where rapid and reliable cell counts are crucial for various procedures, including blood analysis, cancer research, and drug development. Universities, meanwhile, rely heavily on cell counters for cutting-edge research in areas such as immunology, stem cell biology, and genetics. The historical period (2019-2024) saw steady growth, setting the stage for even more significant expansion during the forecast period (2025-2033). Technological advancements, such as the development of automated and high-throughput cell counters, are further fueling market expansion. These innovations not only increase efficiency but also minimize human error, leading to more reliable results and reducing overall operational costs. Furthermore, the growing adoption of personalized medicine necessitates more precise cell analysis, creating a demand for advanced cell counters capable of handling diverse sample types and providing detailed analytical data. The estimated market size in 2025 is significant, indicating the substantial current demand, with expectations for continued growth throughout the forecast period. Competition among leading manufacturers is fierce, prompting ongoing innovation and the development of user-friendly, cost-effective solutions. This competitive landscape is benefiting end-users by offering a wider range of choices and pushing technological advancement. The market is segmented by type (benchtop and handheld) and application (hospitals, universities, and other research institutions), creating opportunities for niche players to cater to specific customer needs. The base year for this analysis is 2025, offering a robust foundation for projecting future market trends and growth potential.

Several key factors are driving the growth of the cell counter market within hospitals and universities. The increasing prevalence of diseases requiring precise cell analysis, such as cancer and infectious diseases, is a major driver. Hospitals and research facilities are constantly seeking more advanced tools for diagnosis, treatment monitoring, and research. The demand for high-throughput screening and automated cell counting is also growing rapidly. Automated cell counters significantly increase efficiency and reduce human error, leading to improved accuracy and faster turnaround times. This is crucial in high-volume settings like large hospital labs and research institutions conducting large-scale experiments. The advancement in cell counter technology itself plays a significant role. New models offer improved precision, higher throughput, and more sophisticated analysis capabilities, attracting institutions seeking cutting-edge solutions. Furthermore, increasing research funding in the life sciences and biomedical sectors is providing substantial resources for acquiring new equipment, including advanced cell counters. Finally, the growing emphasis on personalized medicine and the need for individualized treatment strategies require precise cell analysis, thereby bolstering demand for advanced cell counting technologies that can provide detailed information about individual cellular properties. This interplay of increasing disease prevalence, technological advancement, and research funding forms a robust foundation for continued market growth.

Despite the promising growth trajectory, several challenges and restraints hinder the cell counter market's full potential. High initial investment costs associated with purchasing advanced cell counters can be a significant barrier, particularly for smaller hospitals and universities with limited budgets. This price sensitivity often leads to a preference for older, less efficient technologies or delays in upgrading equipment. The need for specialized training and technical expertise to operate and maintain these sophisticated instruments also presents a hurdle. Insufficient training can lead to incorrect results and compromise the reliability of the data generated. The complex regulatory landscape surrounding medical devices and research equipment adds another layer of complexity. Compliance with stringent regulations and obtaining necessary approvals can be time-consuming and expensive, potentially slowing down market penetration. Furthermore, the potential for technological obsolescence poses a challenge. Rapid technological advancements in the field necessitate frequent upgrades and replacements, requiring significant capital expenditure and adding to the overall operational costs. Finally, the competitive landscape itself can present challenges for manufacturers. Intense competition necessitates continuous innovation and the development of advanced features to differentiate products and attract customers.

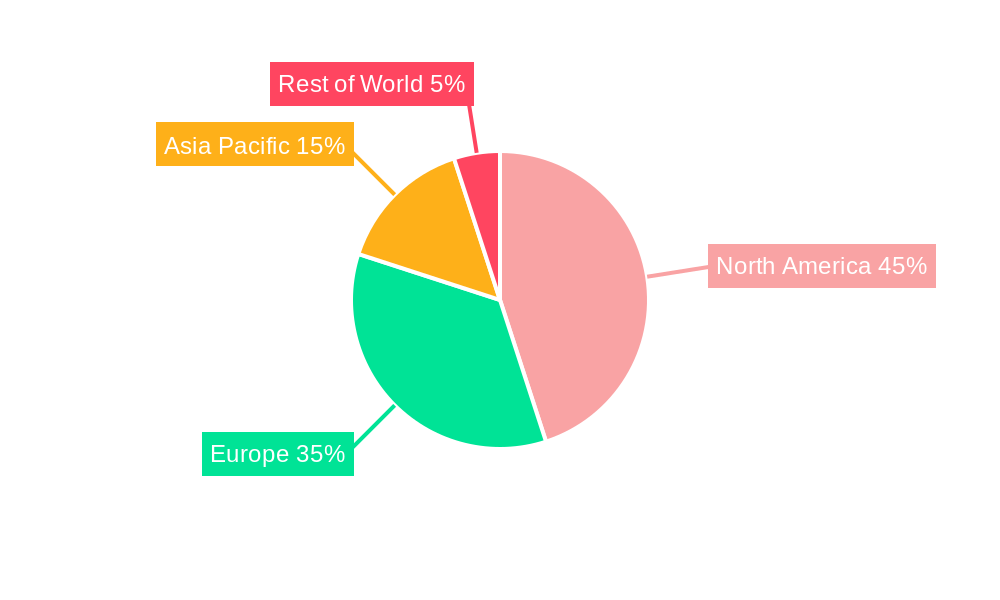

The North American and European regions are currently leading the global market for cell counters in hospitals and universities, driven by robust healthcare infrastructure, high research funding, and a strong presence of key market players. However, the Asia-Pacific region is expected to witness significant growth during the forecast period due to the rising prevalence of chronic diseases, increasing investments in healthcare infrastructure, and expanding research activities in this region.

Dominant Segment: Benchtop Cell Counters: Benchtop cell counters are expected to dominate the market due to their superior performance, versatility, and capacity to handle higher sample volumes compared to handheld devices. They provide greater accuracy and more advanced analytical capabilities, making them preferred choices for high-throughput labs in hospitals and universities. The increased adoption of advanced features, such as automated cell identification and image analysis capabilities, further enhances their appeal. The sophisticated functionalities of benchtop counters cater to the complex demands of research settings and high-volume diagnostic applications in hospitals. Furthermore, benchtop models typically offer greater flexibility and adaptability to various applications and cell types, making them a cost-effective long-term investment compared to multiple handheld devices for diverse needs.

Dominant Application: Hospitals: Hospitals represent a significant market segment due to the critical need for rapid and accurate cell counts in various diagnostic procedures, disease monitoring, and therapeutic applications. The high volume of samples processed daily in hospital laboratories makes efficient and automated cell counting crucial. The demand for reliable, high-throughput cell counters is constantly increasing in hospitals due to the rising incidence of diseases requiring immediate cell analysis, such as blood cancers and infections. Hospitals require high reliability and minimal downtime for diagnostic testing, which benchtop counters excel at providing. The accuracy and precision offered by these instruments are essential for accurate diagnosis and treatment planning, solidifying their crucial role within the hospital setting.

Several factors are catalyzing growth in this sector. Firstly, continuous technological advancements are leading to improved accuracy, higher throughput, and more user-friendly interfaces. Secondly, the increasing prevalence of chronic diseases is driving demand for rapid and reliable diagnostic tools. Thirdly, rising research funding in life sciences is fueling investments in advanced cell counting technologies. Finally, the growing adoption of personalized medicine requires precise cell analysis, which further supports market expansion.

This report provides a detailed analysis of the cell counter market for hospitals and universities, covering market trends, growth drivers, challenges, key players, and significant developments. It offers a comprehensive overview of the market landscape, enabling informed decision-making for stakeholders in this dynamic sector. The forecast period extends to 2033, providing a long-term perspective on market growth potential. The detailed segmentation by type and application allows for a granular understanding of market dynamics, providing insights into specific niche opportunities. The report combines quantitative data with qualitative analysis, offering a well-rounded perspective on market trends and future prospects.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Thermo Fisher Scientific, Bio-Rad, Beckman Coulter, Merck Millipore, Roche, Olympus, ChemoMetec, Advanced Instruments, Corning, Nexcelom Bioscience, Logos Biosystems, Oxford Optronix, DeNovix, Countstar (ALIT Life Sciences), NanoEntek.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Cell Counter for Hospitals and Universities," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cell Counter for Hospitals and Universities, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.