1. What is the projected Compound Annual Growth Rate (CAGR) of the Cargo Ship Repairing and Conversion?

The projected CAGR is approximately 5.4%.

Cargo Ship Repairing and Conversion

Cargo Ship Repairing and ConversionCargo Ship Repairing and Conversion by Type (/> Ship Repairing, Ship Conversion), by Application (/> Container Ships, Bulk Carriers, Tankers, Engineering Ships, Other Ships), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

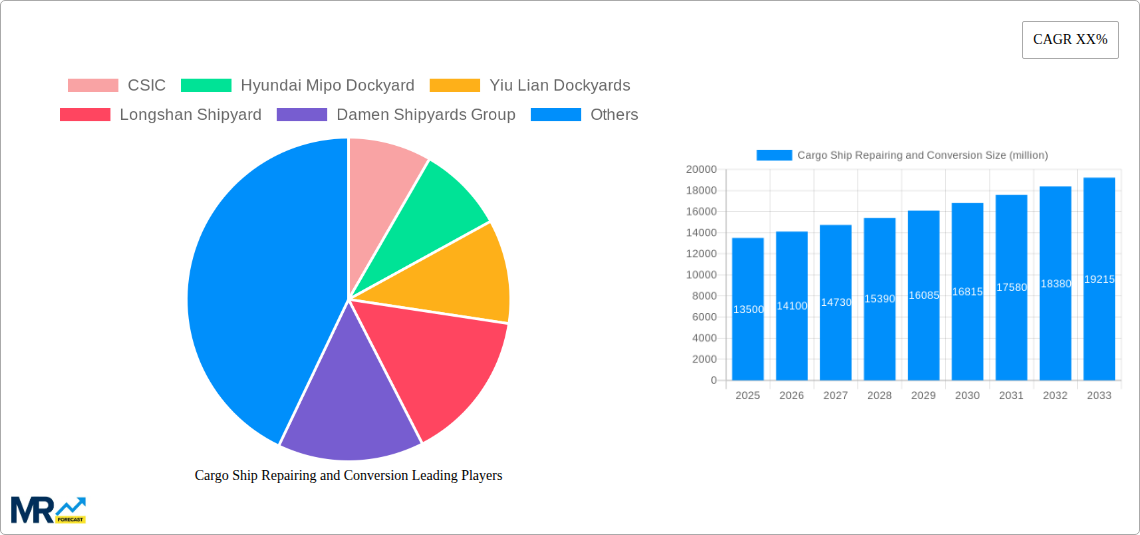

The global Cargo Ship Repairing and Conversion market is poised for significant expansion, projected to reach a valuation of approximately $13,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of around 4.5% expected to propel it to an estimated $19,500 million by 2033. This growth is primarily driven by the ever-increasing volume of global trade, which necessitates a larger and more efficient fleet of cargo vessels. The aging global fleet further fuels demand for repair services, as older ships require regular maintenance and upgrades to meet stringent environmental regulations and operational standards. Moreover, the ongoing evolution of shipping technology, including the transition towards more sustainable fuel sources and the adoption of advanced automation, is creating substantial opportunities for ship conversion services. This shift in industry requirements encourages vessel owners to invest in retrofitting existing ships to comply with new regulations and enhance their operational capabilities, thereby extending their lifespan and improving their economic viability.

Key segments contributing to this market dynamism include ship repairing, which forms the foundational demand due to the inherent need for vessel upkeep, and ship conversion, which represents a growing segment driven by technological advancements and environmental mandates. Container ships, bulk carriers, and tankers constitute the primary applications, reflecting their dominant presence in global maritime trade. Geographically, the Asia Pacific region, particularly China, is expected to lead the market due to its extensive shipbuilding infrastructure, a large number of shipyards, and a high concentration of cargo vessels. Europe and North America also represent significant markets, driven by established shipping routes and a focus on vessel modernization and compliance. While the market is robust, challenges such as high operational costs, skilled labor shortages, and the cyclical nature of the shipping industry can pose restraints. However, the overarching trend of increasing trade volumes and the continuous need for fleet modernization and regulatory compliance are expected to ensure sustained growth in the cargo ship repairing and conversion sector.

This report provides an in-depth analysis of the global Cargo Ship Repairing and Conversion market, offering critical insights and forecasts from 2019 to 2033. Examining trends, drivers, challenges, and key players, the study delves into the intricate dynamics shaping this vital maritime sector. With a base year of 2025 and a forecast period extending to 2033, this report equips stakeholders with the strategic intelligence needed to navigate market complexities and capitalize on emerging opportunities. The analysis encompasses various ship types, including Container Ships, Bulk Carriers, Tankers, and Engineering Ships, while also considering broader applications within the industry. Market valuations are presented in the millions of US dollars.

The global Cargo Ship Repairing and Conversion market is undergoing a significant transformation, driven by evolving industry needs and technological advancements. During the Study Period (2019-2033), with a keen focus on the Base Year (2025) and the Forecast Period (2025-2033), the market is witnessing a pronounced shift towards specialized services and environmentally compliant solutions. The Historical Period (2019-2024) laid the groundwork for this evolution, characterized by steady demand for routine maintenance and repairs. However, the present and future trajectory are increasingly defined by complex conversion projects aimed at enhancing vessel efficiency, adapting to new fuel technologies, and meeting stringent environmental regulations. For instance, the conversion of traditional fuel-powered vessels to operate on alternative fuels like LNG or methanol is becoming a dominant trend, reflecting the industry's commitment to decarbonization. This trend is not only driven by regulatory pressures but also by the long-term economic benefits of reduced fuel costs and improved marketability of greener fleets.

Furthermore, the surge in e-commerce and global trade, despite short-term fluctuations, continues to fuel the demand for container ships. Consequently, the repairing and conversion of these vessels to accommodate larger capacities or specialized cargo handling equipment remain a robust segment. Similarly, bulk carriers, essential for the global transportation of commodities, require continuous maintenance and periodic upgrades to optimize performance and safety. The tanker segment, while mature, is also seeing an uptick in conversion projects focused on enhancing safety features and adapting to the transportation of specialized chemicals and refined products. Engineering ships, crucial for offshore construction and maintenance, are increasingly being retrofitted with advanced equipment to meet the demands of complex offshore projects. The overall market value is projected to reach substantial figures in the millions, reflecting the scale and importance of these services. The increasing complexity of these projects necessitates advanced technical expertise and specialized facilities, favoring larger shipyards and those with a proven track record in complex engineering tasks.

Several powerful forces are driving the growth and evolution of the Cargo Ship Repairing and Conversion market. Foremost among these is the escalating global demand for maritime trade, a fundamental pillar of the world economy. As international commerce expands, so does the need for a robust and efficient shipping fleet, directly translating into consistent demand for repair and maintenance services to ensure operational continuity and safety. Coupled with this is the unwavering pressure from international regulatory bodies, such as the International Maritime Organization (IMO), to adhere to increasingly stringent environmental standards. The implementation of regulations like the IMO 2020 sulfur cap and the ongoing push for decarbonization are compelling shipowners to invest in retrofitting their fleets with ballast water treatment systems, scrubbers, and engines capable of running on cleaner fuels. This is a significant driver for conversion projects.

Moreover, the aging global fleet necessitates proactive maintenance and modernization to prolong vessel lifespans and avoid costly replacements. Shipowners are increasingly opting for cost-effective repair and conversion solutions to upgrade older vessels rather than investing in entirely new builds, especially in the face of economic uncertainties and fluctuating newbuild prices. Technological advancements in shipbuilding and repair techniques also play a crucial role, enabling more efficient and sophisticated repairs and conversions. The development of advanced welding techniques, digital diagnostic tools, and automation in shipyards contributes to faster turnaround times and higher quality of work. Finally, the strategic diversification of shipping operations, with owners seeking to adapt their vessels for different cargo types or operational requirements, further fuels the demand for conversion services, leading to a dynamic and responsive market.

Despite the robust growth drivers, the Cargo Ship Repairing and Conversion market faces several significant challenges and restraints that can impede its expansion. One of the primary hurdles is the volatility of global shipping rates and freight markets. Fluctuations in these markets can directly impact shipowners' profitability, leading to delayed or postponed repair and conversion decisions as they await more favorable economic conditions. The increasing complexity and cost of new environmental regulations also present a challenge. While driving conversions, the substantial investment required for retrofitting vessels with new technologies and compliance equipment can be a significant financial burden, particularly for smaller operators. This can lead to a market bifurcation, favoring larger companies with greater financial capacity.

Furthermore, the shortage of skilled labor and specialized technical expertise within the maritime repair and conversion sector poses a considerable restraint. The intricate nature of modern ship repairs and conversions demands a highly trained workforce, and a global deficit in such expertise can lead to project delays, increased labor costs, and compromises in quality. The geopolitical landscape and trade disputes can also disrupt supply chains and affect the availability of essential components and materials needed for repairs and conversions, leading to increased lead times and costs. Additionally, the intense competition among shipyards globally can exert downward pressure on pricing, potentially squeezing profit margins for many players. Finally, the long lead times and logistical complexities associated with dry-docking and undertaking major conversion projects can be a deterrent for shipowners seeking quick solutions, impacting the overall efficiency of the market.

The global Cargo Ship Repairing and Conversion market is characterized by regional hubs of excellence and segment-specific dominance, with Asia-Pacific, particularly China and Southeast Asia, emerging as the leading region.

Asia-Pacific: This region is the undisputed powerhouse due to several compelling factors.

Dominant Segments:

While the Middle East, with players like Drydocks World Dubai and Arab Shipbuilding and Repair Yard, and Europe, with companies like Damen Shipyards Group and Fincantieri, are significant players, particularly in specialized and high-value conversions and military vessel repairs, their overall market share in terms of volume and revenue is often outpaced by the Asia-Pacific region. However, regions like the Middle East are strategically important for their geographical location on major shipping routes, offering competitive repair services for vessels transiting these areas. Oman, with Oman Drydock Company, is also carving out a niche for itself.

The Cargo Ship Repairing and Conversion industry is poised for sustained growth, primarily fueled by the escalating imperative for decarbonization in the maritime sector. The global push for net-zero emissions is compelling shipowners to invest heavily in retrofitting their existing fleets to comply with stringent environmental regulations, leading to a surge in conversion projects for alternative fuels like LNG, methanol, and ammonia. Furthermore, the steady expansion of global trade, driven by increasing consumer demand and economic globalization, ensures a consistent requirement for ship repairs and maintenance to keep the vast merchant fleet operational and efficient. The aging global vessel population also necessitates ongoing repairs and modernization to extend their operational life and optimize performance, preventing premature decommissioning.

This report meticulously dissects the Cargo Ship Repairing and Conversion market, providing a holistic overview from 2019 to 2033. It delves into the critical Market Insights, highlighting the significant growth in conversion projects driven by environmental regulations and the demand for alternative fuel technologies. The report forecasts substantial market value in the millions, underscoring the sector's economic importance. It identifies the Driving Forces such as the expansion of global trade, stringent environmental compliance, and the need to modernize aging fleets. Conversely, it addresses the Challenges and Restraints, including market volatility, high conversion costs, and skilled labor shortages. The analysis pinpoints Asia-Pacific as the dominant region, with China and South Korea at the forefront, and highlights Ship Repairing and Ship Conversion for Container Ships and Tankers as key segments. Finally, it lists the Leading Players and outlines Significant Developments with specific timelines, offering a comprehensive strategic roadmap for industry stakeholders.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.4%.

Key companies in the market include CSIC, Hyundai Mipo Dockyard, Yiu Lian Dockyards, Longshan Shipyard, Damen Shipyards Group, COSCO SHIPPING Heavy Industry, Zhoushan Xinya Shipyard, Huadong shipyard, Huarun Dadong Dockyard, Sembcorp Marine, Drydocks World Dubai, PaxOcean Engineering Zhoushan, Oman Drydock Company, Cochin Shipyard Ltd (CSL), United Shipbuilding Corporation, Arab Shipbuilding and Repair Yard, Fincantieri, Keppel Shipyard, Swissco Holdings, Egyptian Ship Repair & Building Company, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Cargo Ship Repairing and Conversion," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cargo Ship Repairing and Conversion, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.