1. What is the projected Compound Annual Growth Rate (CAGR) of the Car Audio Head Units?

The projected CAGR is approximately 8%.

Car Audio Head Units

Car Audio Head UnitsCar Audio Head Units by Type (OEM, Aftermarket, World Car Audio Head Units Production ), by Application (Passenger Vehicle, Commercial Vehicle, World Car Audio Head Units Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

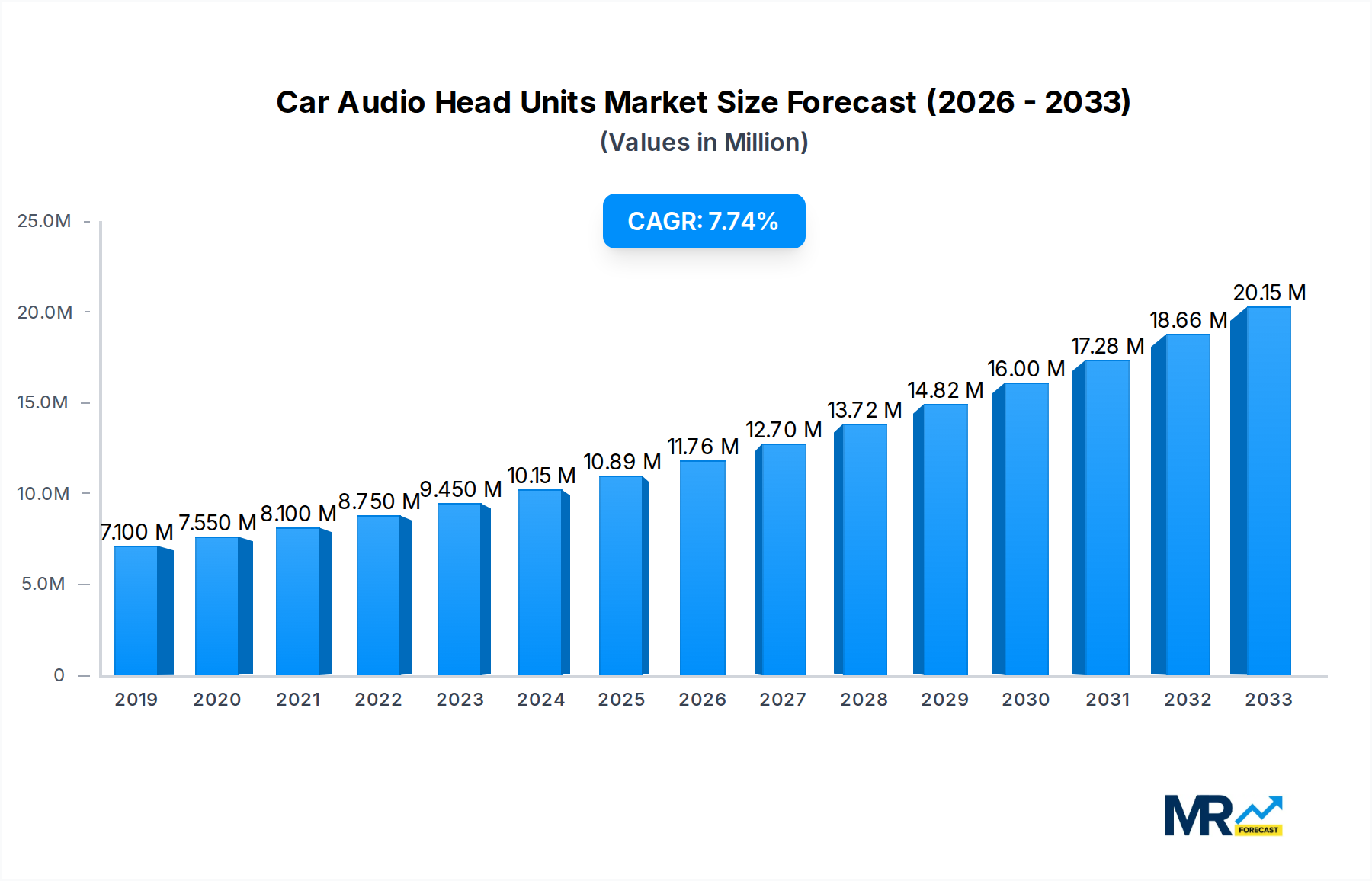

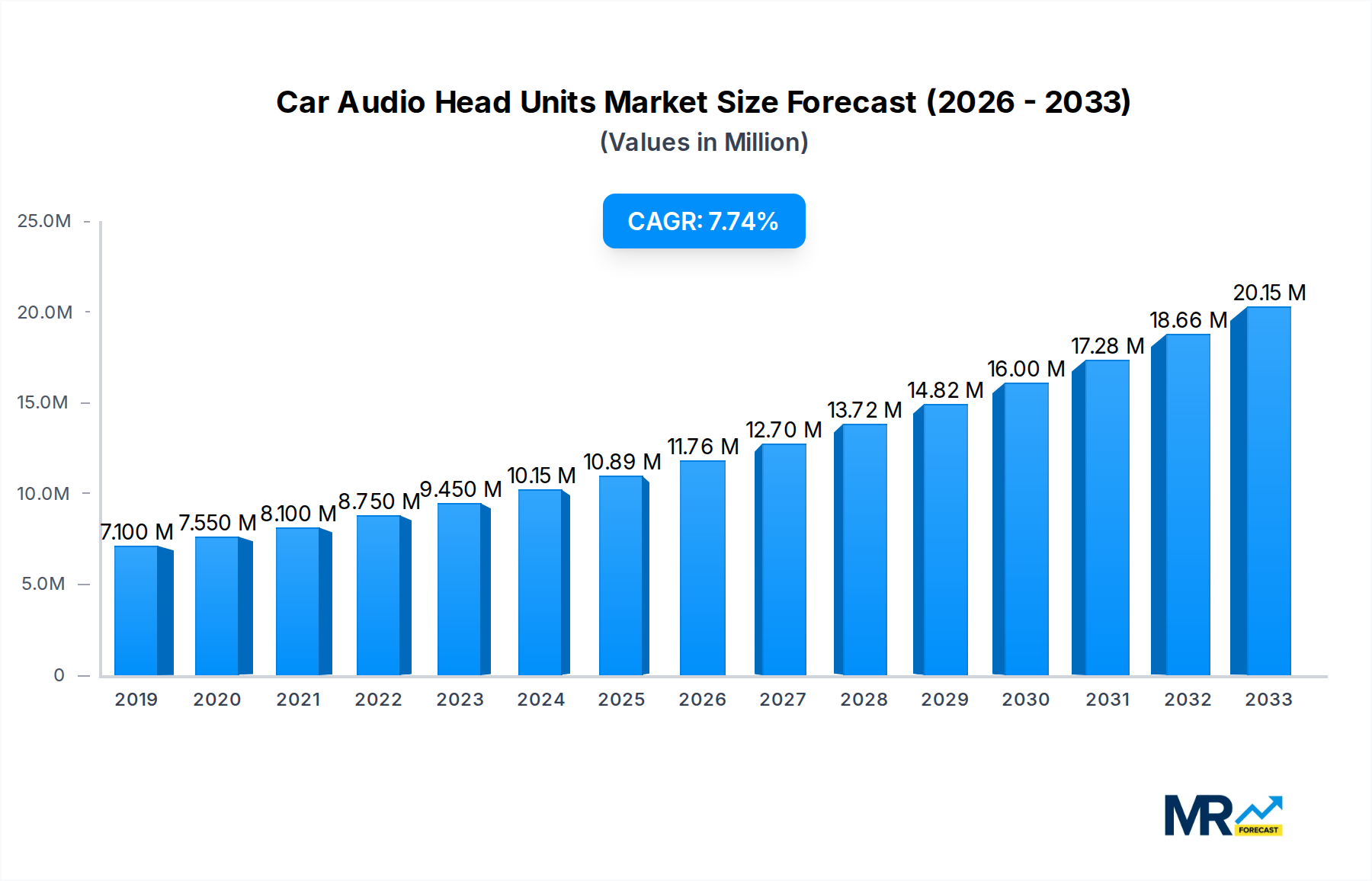

The global Car Audio Head Units market is poised for significant expansion, projected to reach approximately USD 10.89 billion by the base year of 2025, demonstrating a robust Compound Annual Growth Rate (CAGR) of 8%. This impressive growth trajectory, extending through to 2033, is fueled by several key drivers. The increasing integration of advanced technologies such as AI-powered voice assistants, seamless smartphone connectivity (Apple CarPlay, Android Auto), and enhanced audio processing capabilities is a primary catalyst. Consumers' growing preference for sophisticated in-car entertainment and connectivity solutions, coupled with rising disposable incomes in emerging economies, further bolsters demand. Furthermore, the automotive industry's relentless pursuit of innovation, incorporating larger, higher-resolution displays and sophisticated user interfaces into head units, contributes to market dynamism. The shift towards connected vehicles and the demand for integrated infotainment systems that offer navigation, communication, and entertainment in a single unit are fundamental to this market's upward trend.

The market segmentation reveals a healthy demand across both OEM (Original Equipment Manufacturer) and aftermarket channels. While OEM installations are driven by new vehicle production, the aftermarket segment benefits from consumers upgrading existing vehicle audio systems. Passenger vehicles represent the dominant application segment due to their sheer volume, but commercial vehicles are also showing increasing adoption of advanced audio head units for improved driver comfort and communication. Key market restraints include the high cost of advanced features, potential cybersecurity concerns related to connected head units, and the commoditization of basic audio functions, which can put pressure on pricing. However, the ongoing evolution of automotive electronics, the strategic alliances between technology providers and automotive manufacturers, and the introduction of innovative features like augmented reality navigation and personalized audio experiences are expected to mitigate these challenges and sustain the market's strong growth momentum. Prominent players like Panasonic, Continental, Harman, Pioneer, and Sony are at the forefront, investing heavily in R&D to capture a larger market share.

Here is a unique report description on Car Audio Head Units, incorporating your specified requirements:

The global Car Audio Head Units market is a dynamic and high-value sector, projected to experience substantial growth and transformation throughout the study period of 2019-2033. With a base year of 2025 and an estimated market value likely to reach billions of dollars, this comprehensive report delves into the intricate trends, driving forces, challenges, and opportunities that define this evolving industry. We will meticulously analyze the market's trajectory from its historical roots in 2019-2024 to its projected future from 2025-2033, providing unparalleled insights for stakeholders.

The car audio head unit market is experiencing a profound metamorphosis, driven by the relentless march of technological innovation and evolving consumer expectations. By the estimated year of 2025, the market's value is projected to be measured in the billions, a testament to its critical role in the modern automotive experience. A key trend is the seamless integration of advanced digital features, moving beyond traditional audio playback to encompass sophisticated infotainment systems. Consumers are increasingly demanding connected car experiences, with head units serving as the central hub for navigation, communication, smartphone integration (Apple CarPlay and Android Auto), and access to a plethora of streaming services. This shift is fueling a significant increase in the adoption of larger, high-resolution touchscreens and intuitive user interfaces that mimic the familiarity of mobile devices. Furthermore, the rise of voice control technology, powered by artificial intelligence, is transforming how drivers interact with their vehicles, enhancing safety and convenience. The incorporation of advanced audio processing capabilities, including surround sound technologies and personalized audio profiles, is also becoming a differentiator, catering to audiophiles and those seeking an immersive listening experience. The market is also witnessing a bifurcation between the OEM (Original Equipment Manufacturer) and aftermarket segments, each with its unique growth drivers and challenges. In the OEM space, manufacturers are prioritizing integrated solutions that offer a cohesive brand experience and advanced connectivity. Conversely, the aftermarket segment thrives on customization, offering consumers the ability to upgrade their existing systems with the latest technologies and features not available in factory-installed units. The burgeoning electric vehicle (EV) market presents a unique opportunity, with EV manufacturers often opting for highly integrated and feature-rich head units designed to complement the overall digital ecosystem of the vehicle, including battery management and charging status. The influence of software-defined vehicles is also paramount, where head units are no longer just hardware components but integral parts of a complex software architecture, enabling over-the-air updates and continuous feature enhancements. This continuous evolution ensures that the car audio head unit remains at the forefront of automotive innovation.

The exponential growth and increasing sophistication of the car audio head units market are propelled by a confluence of powerful driving forces. Foremost among these is the escalating demand for enhanced in-car connectivity and digital experiences. Consumers, accustomed to the seamless integration of technology in their daily lives, now expect their vehicles to offer similar levels of functionality and entertainment. This expectation translates directly into a need for head units that can effortlessly connect with smartphones, provide access to online services, and offer intuitive navigation and communication capabilities. The rapid advancement of automotive electronics and software engineering plays a pivotal role, enabling the development of more powerful processors, higher-resolution displays, and more sophisticated operating systems for head units. This technological leap allows for the seamless integration of features like advanced driver-assistance systems (ADAS) alerts, vehicle diagnostics, and personalized driver profiles, all managed through the head unit interface. The competitive landscape among automotive manufacturers also acts as a significant catalyst. To differentiate their offerings and attract discerning buyers, carmakers are investing heavily in cutting-edge infotainment systems, with the head unit serving as the primary interface for these innovations. This creates a continuous cycle of technological advancement and feature enhancement. Furthermore, the growing popularity of streaming services and digital content consumption within vehicles is creating a robust demand for head units that can deliver high-quality audio and video playback, along with robust internet connectivity. The aftermarket segment, in particular, is driven by consumer desire for personalization and upgrades, allowing individuals to customize their audio experience beyond factory specifications, thereby further fueling market expansion.

Despite the robust growth, the car audio head units market is not without its significant challenges and restraints. One of the primary hurdles is the increasing complexity of integrating diverse digital ecosystems. With the proliferation of different operating systems, connectivity standards, and proprietary software platforms from various smartphone manufacturers and service providers, ensuring seamless compatibility and a consistent user experience across all devices and applications remains a significant technical challenge. The rapid pace of technological obsolescence also poses a considerable restraint. What is considered cutting-edge today can become outdated within a few years, necessitating substantial and frequent R&D investments for manufacturers to stay competitive, particularly in the OEM segment where product cycles are longer. Cybersecurity threats are another growing concern. As head units become more connected and integral to vehicle functionality, they become potential targets for cyberattacks, requiring robust security measures to protect sensitive user data and vehicle systems. The high cost of advanced head unit technology can also be a limiting factor, especially for entry-level vehicle segments and in price-sensitive aftermarket consumer bases, potentially hindering widespread adoption. Furthermore, regulatory compliance across different global markets, particularly concerning data privacy and in-car distraction, adds another layer of complexity and cost for manufacturers. The global supply chain disruptions experienced in recent years have also impacted the availability and pricing of crucial components, creating production bottlenecks and impacting profit margins for some players in the industry.

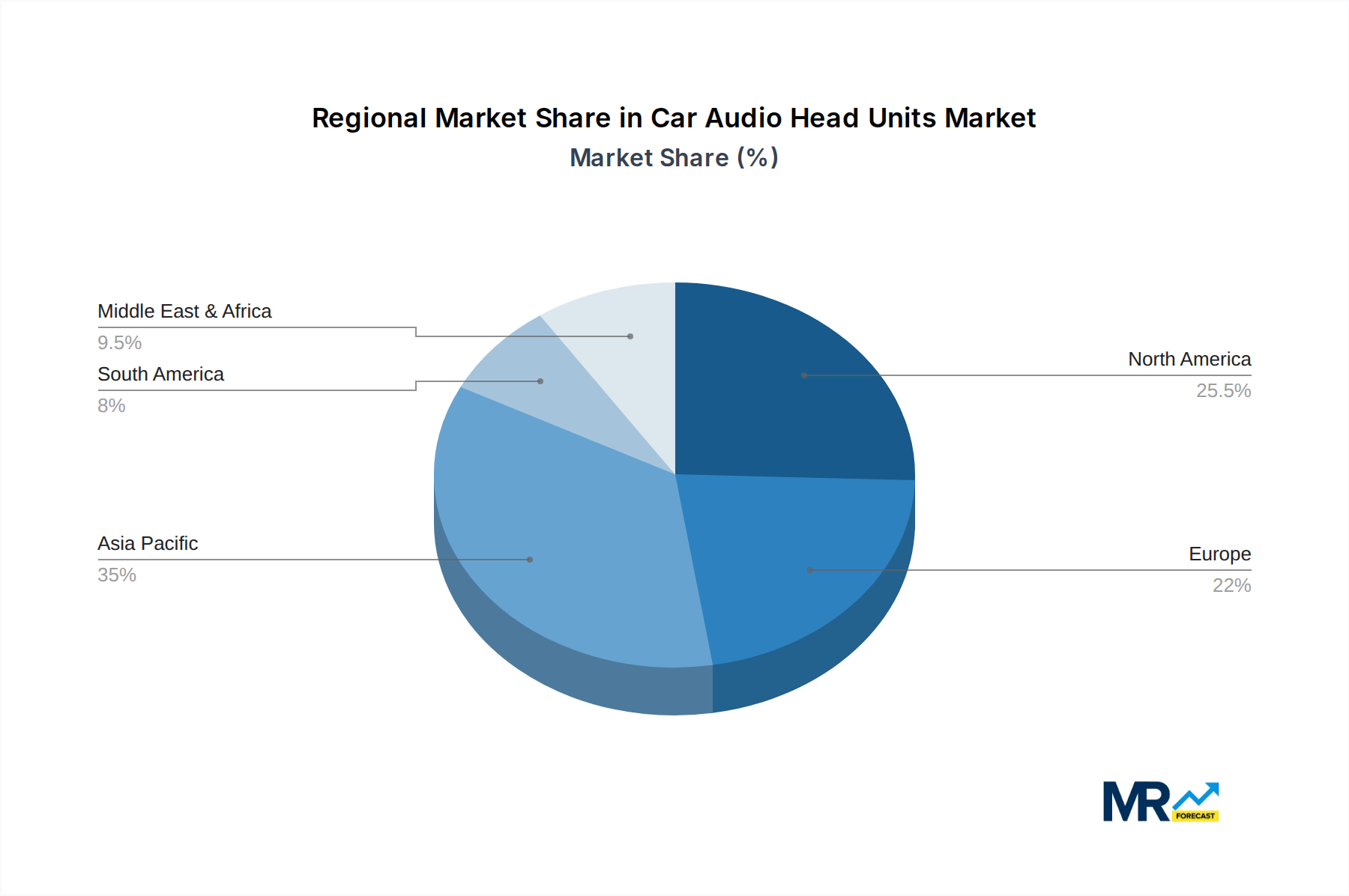

The global Car Audio Head Units market is characterized by the dominance of specific regions and segments, each contributing significantly to its overall valuation and growth trajectory. In terms of regions, North America and Asia-Pacific are poised to be the leading powerhouses.

North America: This region's dominance is fueled by a mature automotive market with a high consumer appetite for advanced automotive technology.

Asia-Pacific: This region is experiencing rapid growth due to the burgeoning automotive industry, particularly in countries like China, Japan, and South Korea, and a rising middle class with increasing disposable income.

The OEM segment is expected to continue its dominance throughout the forecast period (2025-2033). This is primarily due to the increasing standardization of in-car technology by automakers as a key selling proposition. Vehicles are increasingly being sold with integrated infotainment systems, making the OEM head unit the default choice for most new car buyers. As vehicles become more connected and software-defined, the tight integration of head units within the vehicle's electrical architecture further solidifies the OEM segment's lead. While the aftermarket segment will continue to thrive, offering customization and upgrade options, the sheer volume of new vehicle production ensures that the OEM market will remain the largest contributor to the global car audio head units market value, likely representing a market size in the billions by 2025 and continuing its expansion.

Several key growth catalysts are driving the car audio head units industry forward. The relentless pursuit of enhanced in-car connectivity and digital experiences by consumers is a primary driver, pushing for seamless integration with smartphones and access to a plethora of online services. Advancements in automotive software and processing power enable more sophisticated features, including AI-powered voice assistants and intuitive user interfaces. The competitive pressure among automakers to offer cutting-edge infotainment systems as a differentiator further fuels innovation. The growing popularity of streaming media and digital content consumption within vehicles also creates demand for higher-quality audio and video playback capabilities.

This comprehensive report offers an in-depth exploration of the global Car Audio Head Units market, providing a detailed analysis of its multifaceted landscape. It meticulously dissects the trends shaping the industry, from the pervasive integration of digital technologies and smartphone connectivity to the evolving demands for immersive audio experiences. The report illuminates the key driving forces, such as consumer desire for seamless connectivity and the competitive push among automakers for innovative infotainment systems, which are propelling market expansion. Conversely, it also scrutinizes the challenges and restraints, including technological complexity, cybersecurity risks, and cost considerations, that manufacturers and consumers navigate. Furthermore, the report identifies and analyzes the dominant regions and segments poised for significant growth, offering strategic insights into market penetration. It also highlights crucial growth catalysts and provides an exhaustive list of leading players. The report's coverage extends to significant industry developments with precise year-based timelines, ensuring readers are abreast of the latest advancements. Ultimately, this report provides a vital roadmap for stakeholders seeking to understand and capitalize on the billion-dollar opportunities within the dynamic Car Audio Head Units market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8%.

Key companies in the market include Panasonic, Continental, Fujitsu Ten, Harman, Clarion, Hyundai MOBIS, Visteon, Pioneer, Blaupunkt, Delphi, BOSE, Alpine, Garmin, Denso, Sony, Foryou, Desay SV Automotive, Hangsheng Electronic, E-LEAD Electronic, Burmester, Focal, Dynaudio, Bower & Wilkins, .

The market segments include Type, Application.

The market size is estimated to be USD 10.89 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Car Audio Head Units," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Car Audio Head Units, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.