1. What is the projected Compound Annual Growth Rate (CAGR) of the Branded Generics?

The projected CAGR is approximately 6.5%.

Branded Generics

Branded GenericsBranded Generics by Type (Oral, Parenteral, Topical, Other), by Application (Oncology, Cardiovascular Diseases, Diabetes, Neurology, Gastrointestinal Diseases, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

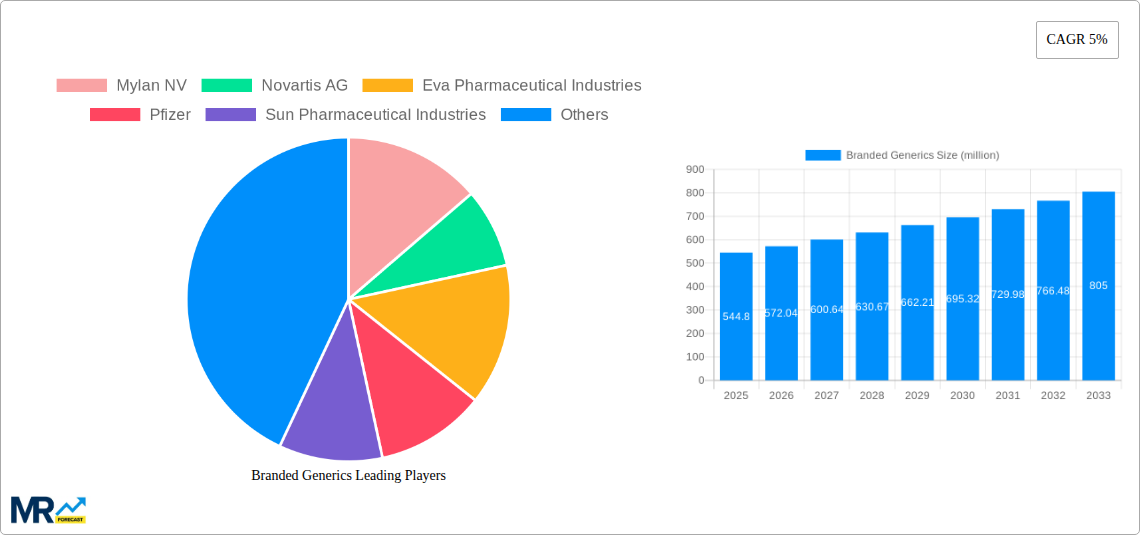

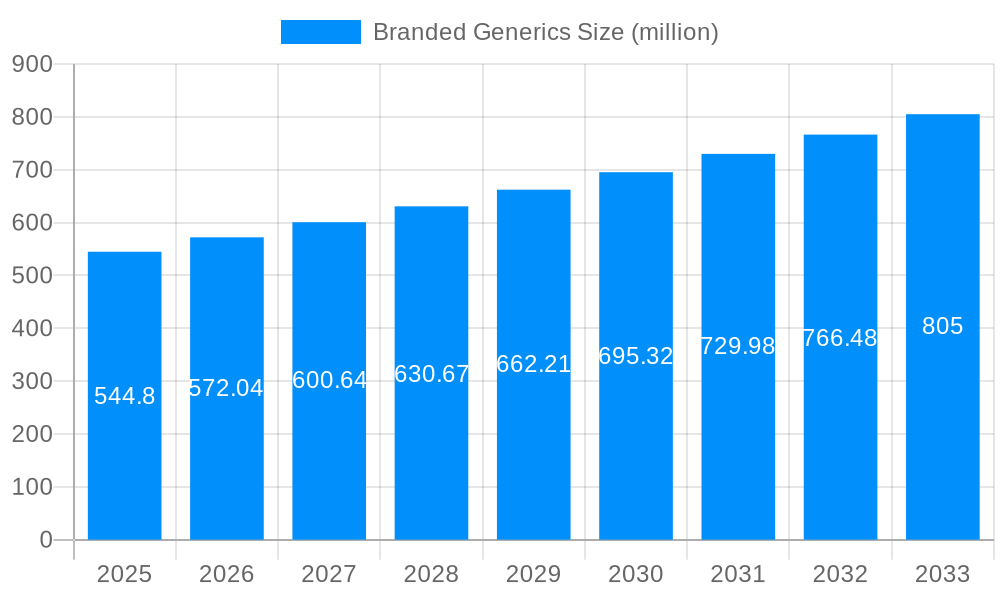

The branded generics market is projected to reach $276.98 billion by 2025, with a compound annual growth rate (CAGR) of 6.5% from 2025 to 2033. This significant growth is propelled by increasing global healthcare expenditure and the rising prevalence of chronic diseases, augmenting demand for accessible yet effective medications. Government and insurance provider initiatives favoring cost-efficient healthcare solutions further stimulate market expansion. Continuous advancements in generic drug development, including enhanced formulations and delivery mechanisms, also contribute to the sector's appeal. Leading companies such as Mylan, Novartis, Pfizer, and Sun Pharmaceutical Industries are actively pursuing R&D, broadening product offerings, and engaging in strategic acquisitions to solidify their market presence, fostering innovation and ensuring a steady supply of quality branded generics.

While detailed segmentation is not specified, it likely encompasses therapeutic areas (e.g., cardiovascular, oncology, diabetes), drug formulations (e.g., tablets, injectables), and geographical regions. Variations in healthcare infrastructure, regulatory environments, and pricing policies across North America, Europe, Asia-Pacific, and other regions will influence regional growth dynamics. Potential challenges include price pressures from escalating generic competition, rigorous regulatory approval processes, and volatile raw material costs. Nevertheless, the market's inherent stability, driven by the persistent demand for affordable healthcare, offsets these concerns. Future growth is anticipated to be led by emerging economies with expanding populations and improved healthcare access, alongside the ongoing development of innovative branded generic formulations addressing unmet medical needs.

The branded generics market, valued at approximately 1500 million units in 2024, is experiencing a period of significant transformation. This market segment, occupying a unique space between traditional generics and innovative branded pharmaceuticals, is driven by a confluence of factors, including increasing consumer demand for affordable yet trusted medications, strategic maneuvering by pharmaceutical companies, and evolving regulatory landscapes. While the historical period (2019-2024) saw steady growth fueled primarily by cost-conscious consumers and the entry of several major players, the forecast period (2025-2033) promises even more dynamic changes. The estimated market size for 2025 sits at 1800 million units, indicating a robust trajectory. This growth is not solely predicated on volume; it also reflects a shift in consumer perception, where the "generic" stigma is gradually eroding, replaced by a focus on efficacy and proven track records. The market is witnessing the rise of niche branded generics, focusing on specific therapeutic areas or patient populations, creating further segmentation and specialization within the industry. The success of these strategies hinges on successful brand building and targeted marketing campaigns that emphasize the unique advantages and quality control measures associated with these products, moving beyond a simple price-based competition. This requires innovative packaging, robust clinical data showcasing bioequivalence, and a strong emphasis on building trust with healthcare providers and patients. Ultimately, the future of branded generics lies in balancing cost-effectiveness with quality assurance and targeted marketing, resulting in greater accessibility and improved healthcare outcomes for a wider patient base.

Several key factors are propelling the growth of the branded generics market. Firstly, the increasing prevalence of chronic diseases globally necessitates affordable treatment options. Branded generics offer a compelling solution, providing quality medication at a lower cost compared to innovative branded drugs. Secondly, the strategic shift by major pharmaceutical companies towards diversification and expansion into this sector is injecting substantial capital and expertise. Companies like Mylan and Teva have already established a strong presence, and others are increasingly recognizing the market’s potential profitability. This influx of resources is fueling innovation in product development, packaging, and marketing. Furthermore, evolving regulatory frameworks in many regions are encouraging the development and adoption of branded generics, streamlining the approval process and promoting market competition. This encourages transparency and ensures that consumers have access to a wider range of high-quality options. Lastly, the growing awareness amongst consumers regarding the safety and efficacy of generics – specifically branded generics with strong brand recognition - is driving increased demand. This understanding is fostered by better education and information dissemination by healthcare professionals and through targeted marketing initiatives by the manufacturers.

Despite the promising growth trajectory, the branded generics market faces several challenges. Intense price competition from traditional generics remains a persistent hurdle, necessitating innovative strategies to differentiate and justify premium pricing. The need to invest substantially in establishing brand recognition and consumer trust can be a considerable capital expenditure, especially for new entrants. Navigating complex regulatory requirements and ensuring compliance across diverse geographical markets adds another layer of complexity. Regulatory pathways can be lengthy and often require substantial data collection and submission, impacting time-to-market and profitability. Furthermore, maintaining a consistent supply chain and guaranteeing product quality across different manufacturing sites is crucial, especially as the market expands globally. Any disruptions, either due to unforeseen circumstances or production bottlenecks, can severely impact sales and reputation. Lastly, effectively managing intellectual property rights and avoiding patent infringement disputes is critical for sustained success in this competitive landscape. Addressing these challenges requires strategic planning, robust risk management, and continuous investment in quality assurance, and marketing.

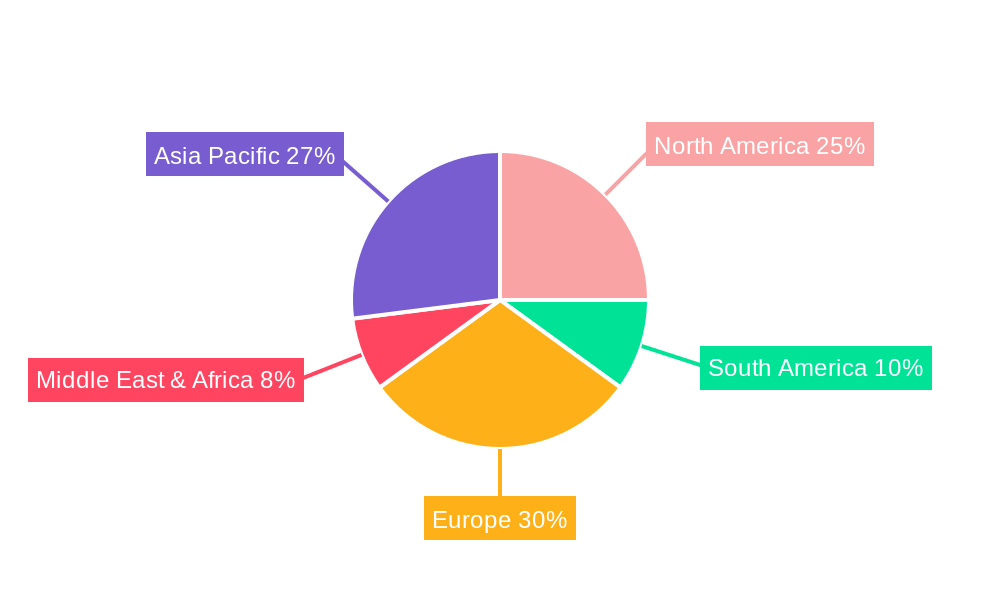

North America: The North American market, particularly the United States, is projected to maintain its dominance due to high healthcare expenditure, an aging population requiring more medications, and a relatively well-established regulatory framework for generics. The large market size and mature healthcare system provide a favorable environment for branded generic manufacturers to thrive. The segment of cardiovascular drugs is expected to remain highly significant given the prevalence of heart disease.

Europe: The European market exhibits substantial growth potential, driven by increasing pressure on healthcare systems to control costs and rising demand for affordable medications. The regulatory environment in Europe supports the development and introduction of branded generics. The diabetes segment is poised for rapid expansion given the increase in diabetes cases.

Asia-Pacific: This region is experiencing rapid growth fueled by a burgeoning middle class with increasing disposable income and improved access to healthcare. However, regulatory hurdles and varying levels of healthcare infrastructure across countries create challenges for market penetration. The segment focusing on anti-infectives is predicted to be of growing importance, reflecting the needs of this populous region.

Dominant Segments: Cardiovascular drugs, diabetes medications, and anti-infectives consistently rank among the leading segments within the branded generics market, owing to their large patient populations and considerable treatment costs. The ongoing research and development in these therapeutic areas will likely lead to new branded generic options entering the market, further fueling growth.

The above-mentioned geographical regions and therapeutic segments are projected to drive the largest share of the market during the forecast period. However, emerging markets in Latin America and Africa offer significant long-term growth opportunities, although these markets will be more susceptible to regulatory and infrastructural variations.

The branded generics industry is poised for significant growth due to several factors. Firstly, the increasing focus on cost-containment within healthcare systems worldwide creates a strong demand for affordable, high-quality alternatives to innovative branded drugs. Secondly, the ongoing innovation in manufacturing processes and drug delivery systems continues to improve the quality and efficacy of branded generics, thereby bolstering consumer confidence. Finally, strategic alliances and mergers and acquisitions within the pharmaceutical industry will continue to consolidate market share and drive further innovation and expansion.

This report provides a comprehensive overview of the branded generics market, analyzing historical trends, current market dynamics, and future growth projections. It offers detailed insights into key market drivers, challenges, and opportunities, providing valuable information for companies operating in this dynamic sector and those considering entering the market. The report includes detailed profiles of leading players, segment analysis, geographic market breakdowns, and a comprehensive forecast to 2033. It serves as a critical resource for strategic decision-making, investment analysis, and market planning within the branded generics industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.5%.

Key companies in the market include Mylan NV, Novartis AG, Eva Pharmaceutical Industries, Pfizer, Sun Pharmaceutical Industries, Aspen Pharmacare Holding, Abbott Laboratories, Bausch Health, .

The market segments include Type, Application.

The market size is estimated to be USD 276.98 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Branded Generics," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Branded Generics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.