1. What is the projected Compound Annual Growth Rate (CAGR) of the Blood Coagulation Factor?

The projected CAGR is approximately XX%.

Blood Coagulation Factor

Blood Coagulation FactorBlood Coagulation Factor by Type (Blood Product, Non Plasma Derived Congulation Factor), by Application (Hospital, Laboratory, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

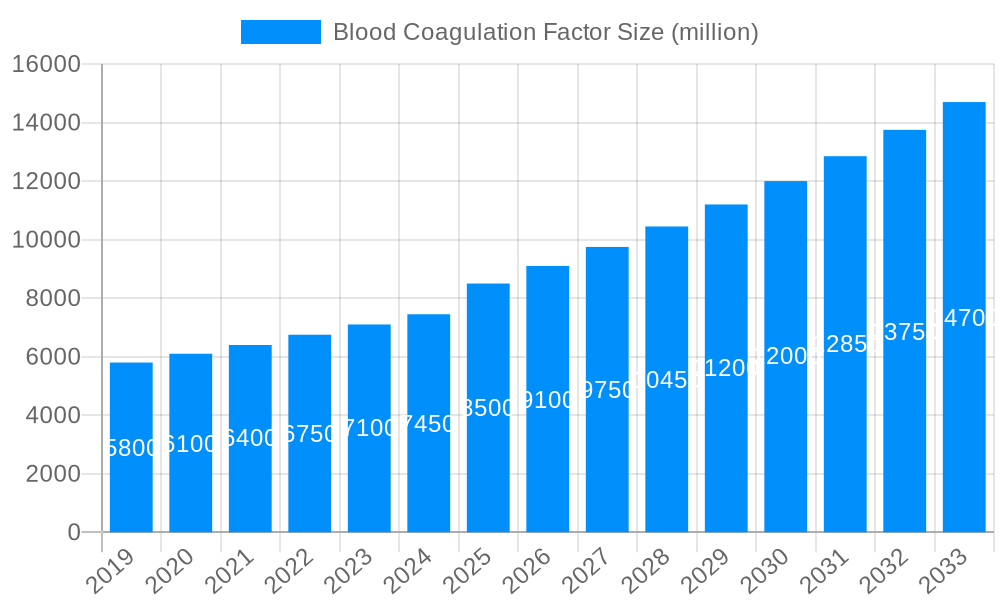

The global Blood Coagulation Factor market is poised for significant growth, projected to reach an estimated $8,500 million by 2025, expanding at a robust Compound Annual Growth Rate (CAGR) of 7.5% through 2033. This expansion is primarily driven by the increasing prevalence of bleeding disorders such as hemophilia and von Willebrand disease, coupled with advancements in recombinant factor therapies that offer enhanced safety and efficacy profiles compared to plasma-derived products. The growing awareness and diagnosis of these conditions, particularly in emerging economies, are further fueling market demand. Furthermore, the development of novel therapeutic agents and the expanding applications of coagulation factors in surgical procedures and trauma management are anticipated to contribute substantially to market expansion. The market is segmented into Blood Product and Non-Plasma Derived Congulation Factor types, with the latter segment expected to witness accelerated growth due to technological innovations and reduced risk of blood-borne infections. Hospitals represent the dominant application segment, owing to the critical need for these factors in managing acute bleeding events and chronic conditions.

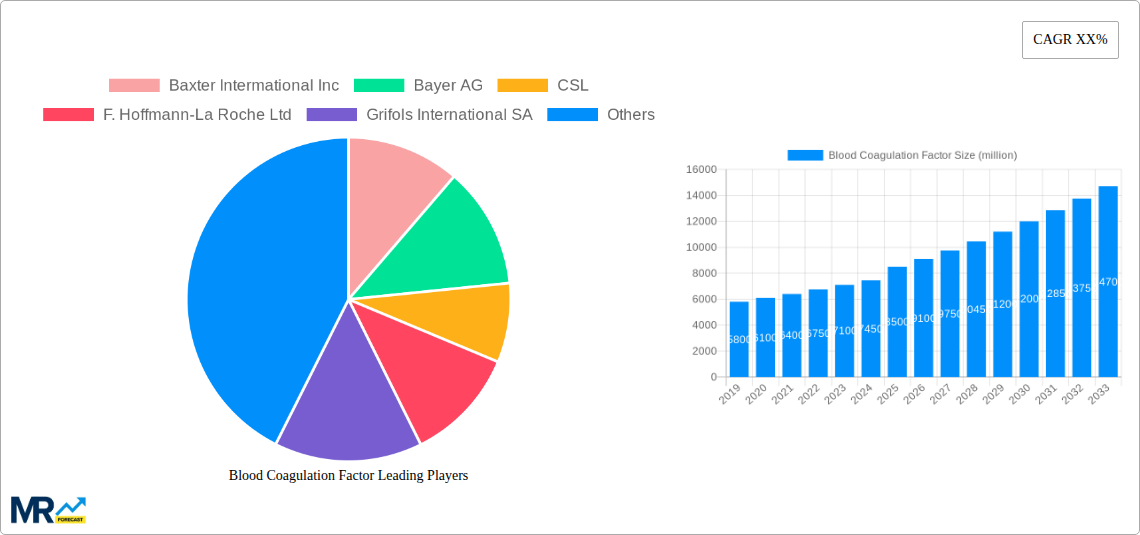

The market landscape is characterized by intense competition among key global players, including Baxter International Inc., Bayer AG, CSL, F. Hoffmann-La Roche Ltd, Grifols International SA, and Novo Nordisk A/S, among others. These companies are actively investing in research and development to introduce next-generation coagulation factor therapies, including long-acting formulations and gene therapies, which aim to improve patient convenience and treatment outcomes. Geographically, North America currently leads the market share, owing to a well-established healthcare infrastructure and high disease prevalence. However, the Asia Pacific region is expected to exhibit the fastest growth rate, driven by increasing healthcare expenditure, a rising number of diagnosed cases, and government initiatives to improve access to specialized treatments. Restraints such as the high cost of therapies and potential side effects associated with certain factor replacements are being addressed through ongoing research and development aimed at optimizing treatment strategies and product innovation.

The global Blood Coagulation Factor market is poised for substantial growth, with projections indicating a robust expansion from approximately \$3,200 million in the base year of 2025 to an estimated \$5,100 million by the end of the forecast period in 2033. This signifies a Compound Annual Growth Rate (CAGR) of over 5.9% during the 2025-2033 forecast period. The historical performance from 2019 to 2024 has laid a strong foundation, demonstrating a consistent demand for these critical therapeutic agents. The market's trajectory is largely influenced by an increasing prevalence of bleeding disorders, coupled with advancements in recombinant factor therapies that offer enhanced safety and efficacy profiles compared to traditional plasma-derived products. The study period, spanning 2019-2033, encompasses both past innovations and future potential, highlighting a dynamic landscape. The estimated year of 2025 serves as a crucial benchmark, showcasing the current market size and the momentum that will carry through the forecast. A key trend observed is the shift towards personalized medicine, where factors are increasingly tailored to individual patient needs, leading to improved treatment outcomes. Furthermore, the rising awareness about hemophilia and other rare bleeding disorders, driven by advocacy groups and improved diagnostic capabilities, is expanding the patient pool and consequently the market demand. The development of novel delivery methods and extended half-life formulations is also contributing to market expansion, offering greater convenience and reducing the frequency of infusions for patients. The interplay between technological innovation, evolving clinical practices, and a growing global patient population underpins the optimistic outlook for the blood coagulation factor market over the next decade. The market's resilience is further underscored by its critical role in managing life-threatening conditions, ensuring sustained demand even amidst economic fluctuations.

The blood coagulation factor market is experiencing a significant upward trajectory, primarily driven by the escalating global incidence of inherited bleeding disorders, such as hemophilia A and B, as well as von Willebrand disease. The increasing awareness and improved diagnostic tools have led to earlier and more accurate identification of affected individuals, thereby expanding the patient pool requiring regular factor replacement therapy. Furthermore, the substantial advancements in biotechnology have paved the way for the development and widespread adoption of recombinant blood coagulation factors. These bioengineered products offer a safer alternative to plasma-derived factors by eliminating the risk of pathogen transmission, a major concern with earlier treatments. The superior safety and efficacy profiles of recombinant factors are compelling healthcare providers and patients to favor them, thus fueling market growth. Additionally, the introduction of extended half-life (EHL) formulations represents a groundbreaking development. These innovative therapies significantly prolong the therapeutic effect of the administered factor, allowing for less frequent infusions and improving patients' quality of life by reducing treatment burden and enhancing adherence. The growing demand for prophylactic treatment regimens, aimed at preventing bleeding events before they occur, is also a significant market driver, especially for severe hemophilia patients.

Despite the promising growth trajectory, the blood coagulation factor market faces several significant challenges and restraints that could impede its full potential. A primary hurdle is the extraordinarily high cost associated with the manufacturing and procurement of both plasma-derived and recombinant coagulation factors. This financial burden can limit access to these life-saving treatments, particularly in low- and middle-income countries where healthcare budgets are constrained and reimbursement policies may not adequately cover the expenses. The complexity of regulatory approvals for new factor products, often involving extensive clinical trials and stringent safety evaluations, can also lead to lengthy development timelines and significant investment risks for pharmaceutical companies. Furthermore, the reliance on plasma-derived factors, although decreasing, still presents a potential supply chain vulnerability. Sourcing and processing human plasma is a complex and resource-intensive endeavor, susceptible to variations in donor availability and strict screening protocols. The emergence of alternative therapies, such as gene therapy, while offering long-term curative potential, is still in its nascent stages of clinical application and widespread adoption. These therapies, if successful and accessible, could eventually disrupt the demand for traditional factor replacement therapies. Lastly, the lack of widespread awareness and diagnostic infrastructure for rare bleeding disorders in certain geographical regions continues to limit the identification and treatment of many patients, thus capping the market's growth.

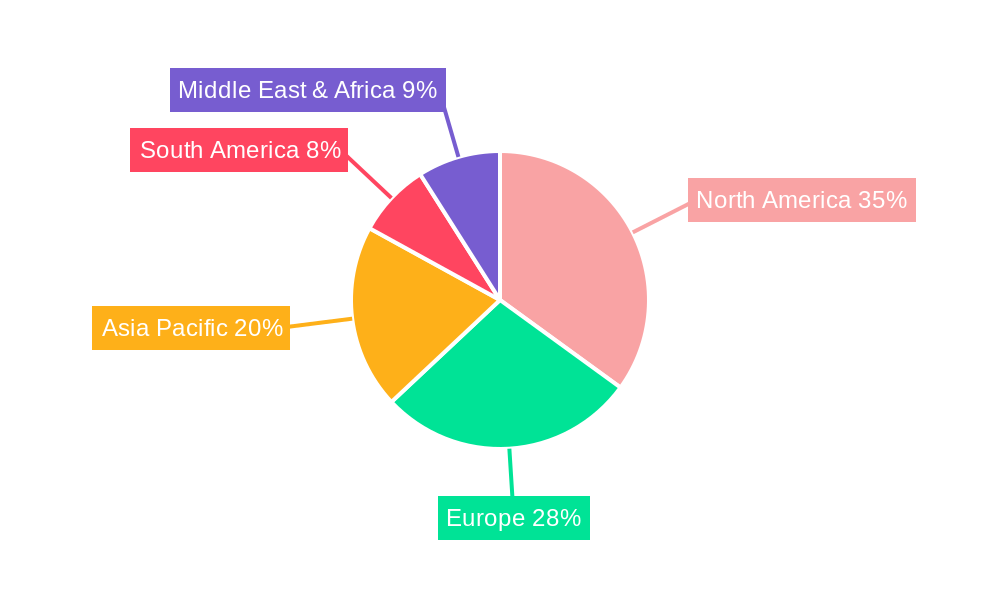

The global Blood Coagulation Factor market is characterized by regional disparities and segment dominance, with a clear indication that North America, particularly the United States, is expected to maintain its leading position throughout the forecast period (2025-2033). This dominance is attributed to several interconnected factors: a highly developed healthcare infrastructure, robust reimbursement policies for rare disease treatments, and a high prevalence of diagnosed bleeding disorders. The presence of major pharmaceutical companies with extensive research and development capabilities in the region further bolsters its market share.

Within North America, the Hospital application segment is poised to be the primary driver of demand. Hospitals are central to the diagnosis, treatment, and management of acute bleeding episodes and the initiation of prophylactic therapy for patients with coagulation factor deficiencies. The availability of specialized hematology centers and the concentration of highly trained medical professionals within hospital settings ensure optimal utilization of blood coagulation factors.

In terms of Type, the Blood Product segment, which encompasses both plasma-derived and recombinant factors, will continue to hold a substantial market share. However, the Non Plasma Derived Congulation Factor segment, predominantly recombinant factors, is projected to witness a faster growth rate. This is driven by the ongoing shift towards safer and more efficacious bioengineered products, as well as the increasing preference for extended half-life formulations that reduce treatment frequency. The advanced research and development capabilities in North America are instrumental in the early introduction and widespread adoption of these innovative recombinant factors.

Beyond North America, Europe is anticipated to be another significant contributor to the market. Countries like Germany, the United Kingdom, and France possess well-established healthcare systems that support patients with bleeding disorders. However, the pace of growth in Europe might be slightly moderated by varying reimbursement landscapes and economic conditions across different nations.

The Other application segment, which can encompass specialized clinics, infusion centers, and home-care settings, will also witness steady growth. As home-based therapy becomes more prevalent for managing chronic bleeding disorders, this segment's importance will increase. The convenience and improved quality of life offered by self-infusion at home, coupled with the development of user-friendly delivery devices, will fuel this expansion.

While North America and Europe are expected to lead, the Asia Pacific region presents a significant untapped potential for future market expansion. Factors such as a large and growing population, increasing awareness of bleeding disorders, and improving healthcare access are expected to drive demand. Countries like China and India, with their expanding economies and investments in healthcare, are becoming increasingly important markets for blood coagulation factors.

The blood coagulation factor industry is propelled by several key growth catalysts. The increasing incidence of hemophilia and other rare bleeding disorders, coupled with enhanced diagnostic capabilities, is expanding the patient pool. Advancements in recombinant DNA technology have led to the development of safer and more efficacious bioengineered factors, significantly reducing the risk of pathogen transmission. Furthermore, the introduction of extended half-life formulations offers improved patient convenience and adherence by requiring less frequent infusions.

This comprehensive report delves into the intricate dynamics of the global Blood Coagulation Factor market, providing an in-depth analysis of its trends, drivers, challenges, and future outlook. The study meticulously examines the market landscape across the historical period (2019-2024), base year (2025), and forecast period (2025-2033). It offers valuable insights into the market segmentation by Type (Blood Product, Non Plasma Derived Congulation Factor), Application (Hospital, Laboratory, Other), and geographical regions. The report also highlights significant industry developments and showcases the leading players contributing to the market's evolution. This detailed coverage empowers stakeholders with the knowledge to make informed strategic decisions in this critical therapeutic sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Baxter Intermational Inc, Bayer AG, CSL, F. Hoffmann-La Roche Ltd, Grifols International SA, Kedrion S.p.A, Novo Nordisk A/S, Octapharma AG, Siemens Healthineers, Thermo Fisher Scientific Inc., .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Blood Coagulation Factor," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Blood Coagulation Factor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.